UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 20142016

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 1-2958

HUBBELL INCORPORATED

(Exact name of registrant as specified in its charter)

|

| |

| STATE OF CONNECTICUT | 06-0397030 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 40 Waterview Drive, Shelton, CT | 06484 |

| (Address of principal executive offices) | (Zip Code) |

| (475) 882-4000 |

| (Registrant's telephone number, including area code) |

|

| |

| SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: |

| Title of each Class | Name of Exchange on which Registered |

Class A Common Stock — $.01 par value (20 votes$0.01 per share)share | New York Stock Exchange |

Class B Common — $.01 par value (1 vote per share) | New York Stock Exchange |

Series A Junior Participating Preferred Stock Purchase Rights | New York Stock Exchange |

Series B Junior Participating Preferred Stock Purchase Rights | New York Stock Exchange |

| |

| SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: |

| NONE |

|

| | | | | |

| Indicate by check mark | Yes | No |

| if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | þ | ¨ |

| if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. | ¨ | þ |

| if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such report), and (2) has been subject to such filing requirements for the past 90 days. | þ | ¨ |

| whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | þ | ¨ |

| if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | þ¨ |

| whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one): |

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

• whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | ¨ | þ |

The approximate aggregate market value of the voting stock held by non-affiliates of the registrant as of June 30, 20142016 was $$7,152,795,896*$5,763,377,247*. The number of shares outstanding of the Class A Common Stock and Class BHubbell Common Stock as of February 11, 2015 was 7,167,506 and 51,339,048 respectively.10, 2017 is 55,446,167.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the annual meeting of shareholders scheduled to be held on May 5, 2015,3, 2017, to be filed with the Securities and Exchange Commission (the “SEC”), are incorporated by reference in answer to Part III of this Form 10-K.

*Calculated by excluding all shares held by Executive Officers and Directors of registrant and the Louie E. Roche Trust, the Harvey Hubbell Trust, the Harvey Hubbell Foundation and the registrant’s pension plans, without conceding that all such persons or entities are “affiliates” of registrant for purpose of the Federal Securities Laws.

|

| |

| 2 | HUBBELL INCORPORATED- Form 10-K | 2 |

Hubbell Incorporated (herein referred to as “Hubbell”, the “Company”, the “registrant”, “we”, “our” or “us”, which references shall include its divisions and subsidiaries as the context may require) was founded as a proprietorship in 1888, and was incorporated in Connecticut in 1905. Hubbell is primarily engaged in the design, manufacture and sale of quality electrical and electronic products for a broad range of non-residential and residential construction, industrial and utility applications. Products are either sourced complete, manufactured or assembled by subsidiaries in the United States, Canada, Switzerland, Puerto Rico, Mexico, the People’s Republic of China (“China”), Italy, the United Kingdom (“UK”), Brazil, Australia and Australia.Ireland. Hubbell also participates in joint ventures in Taiwan and Hong Kong, and maintains offices in Singapore, China, India, Mexico, South Korea and countries in the Middle East.

The Company’s reporting segments consist of the Electrical segment (comprised of electrical systems products and lighting products) and the Power segment,segments, as described below. See also

Item 7. Management’s Discussion and Analysis – “Executive Overview

of the Business”, and “Results of Operations” as well

as Note 20 –19 — Industry Segments and Geographic Area Information in the Notes to Consolidated Financial Statements.

The Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports are made available free of charge through the Investor Relations section of the Company’s website at http://www.hubbell.com as soon as practicable after such material is electronically filed with, or furnished to, the SEC. These filings are also available for reading and copying at the SEC’s Public Reference Room at 100 F Street N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. In addition, the Company’s SEC filings can be accessed from the SEC’s homepage on the Internet at http://www.sec.gov. The information contained on the Company’s website or connected to our website is not incorporated by reference into this Annual Report on Form 10-K and should not be considered part of this report.

Electrical Segment

The Electrical segment (71%, 71% and 69%(70% of consolidated revenues in 2014, 20132016 and 2012, respectively)2015 and 71% in 2014) is comprised of businesses that sell stock and custom products including standard and special application wiring device products, rough-in electrical products, connector and grounding products, lighting fixtures and controls, components and assemblies for the natural gas distribution market, as well as other electrical equipment. The products

Products of the Electrical segment are typically used in and around industrial, commercial and institutional facilities by electrical contractors, maintenance personnel, electricians, utilities, and telecommunications companies. In addition, certain businesses design and manufacture a variety of high voltage test and measurement equipment, industrial controls and communication systems used in the non-residential and industrial markets. Many of these products are designed such that they can also be used in harsh and hazardous locations where a potential for fire and explosion exists due to the presence of flammable gasses and vapors. Harsh and hazardous products are primarily used in the oil and gas (onshore and offshore) and mining industries. There are also a

variety of lighting fixtures, wiring devices and electrical products that have residential and utility applications.

These products are primarily sold through electrical and industrial distributors, home centers, retail and hardware outlets, lighting showrooms and residential product oriented internet sites. Special application products are sold primarily through wholesale distributors to contractors, industrial customers and original equipment manufacturers (“OEMs”). High voltage products are sold primarily by direct sales to customers through our sales engineers.

Hubbell maintains a sales and marketing organization to assist potential users with the application of certain products to their specific requirements, and with architects, engineers, industrial designers, OEMs and electrical contractors for the design of electrical systems to meet the specific requirements of industrial, non-residential and residential users. Hubbell is also represented by independent manufacturers’ sales agents for many of its product offerings.

|

| |

HUBBELL INCORPORATED - Form 10-K | 3 |

Hubbell Electrical Systems

Hubbell designs,The Electrical segment, manufactures and sells thousands of wiring and electrical products, which are supplied principally to industrial, non-residential and residential customers. These products include items such as:

|

| | | | | |

• | Cable reels | • | Wiring devices & accessories | • | Junction boxes, plugs & receptacles |

• | Cable glands & fittings | • | Switches & dimmers | • | Datacom connectivity & enclosures |

• | Connectors & tooling | • | Pin & sleeve devices | • | Speciality communications equipment |

• | Floor boxes | • | Electrical motor controls | • | High voltage test systems |

• | Ground fault devices | • | Steel & plastic enclosures | • | Mining communication & controls |

These wiring and electrical products are sold under various brands and/or trademarks, including:

|

| | | | | | | |

• | Hubbell®

| • | Bell®

| • | Victor™

| • | Rig Power |

• | Kellems®

| • | TayMac®

| • | GAI-Tronics®

| • | Powerohm |

• | Bryant®

| • | Wiegmann®

| • | Gleason Reel®

| • | Chalmit™ |

• | Burndy®

| • | Killark®

| • | Haefely®

| • | Austdac™ |

• | CMC®

| • | Hawke™

| • | Hipotronics®

| • | Raco® |

Lighting Products

Hubbell manufactures and sells lighting fixtures and controls for indoor and outdoor applications.applications as well as specialty lighting and communications products. The markets served include non-residential and residential. Forproducts within the segment have applications in the non-residential, market the Company typically targets products that would be considered specification grade.residential, industrial, and energy-related (oil and gas) markets. A fast growing trend within the lighting industry is the adoption of light emitting diode (“LED”) technology as the light source. LED technology is both energy

efficientsource and long–lived and as a result offers customers the economic benefits of lower energy and maintenance costs. The Company has a broad array of LED-luminaire products within its portfolio and the majority of new product development efforts are oriented towards expanding those offerings. Examples of these lightingThese products or applications include:include items such as:

|

| | | | | |

| Commercial and Industrial | | |

| • | Wiring devices & accessories | • | Junction boxes, plugs & receptacles | • | Cable reels |

| • | Switches & dimmers | • | Steel & plastic enclosures | • | Datacom connectivity & enclosures |

| • | Ground fault devices | • | Pin & sleeve devices | • | High voltage test systems |

| • | Electrical motor controls | | | | |

| Lighting | | |

| • | Canopy lights | • | Parking lot/parking garage fixtures | • | Decorative landscape fixtures |

| • | Emergency lighting/exit signs | • | Bollards | • | Fluorescent fixtures |

| • | Floodlights & poles | • | Bath/vanity fixtures & fans | • | Ceiling fans |

| • | LED components | • | Chandeliers & sconces | • | Site & area lighting |

| • | Recessed, surface mounted & track fixtures | • | Athletic & recreational field fixtures | • | Occupancy, dimming & daylight harvesting sensors |

| Construction and Energy | | |

| • | Mechanical connectors | • | Gas connectors and assemblies | • | Specialty communications equipment |

| • | Mechanical grounding devices | • | Installation tooling | • | Mining communication & controls |

| • | Compression connectors | • | Specialty lighting | • | Cable glands & fittings |

| • | Safety equipment | | | | |

These lighting products are sold under various brands and/or trademarks, including:

|

| | | | | | | | | |

| Commercial and Industrial | | | | |

| • | Hubbell® | • | Bell® | • | Raco® | • | Gleason Reel® | • | ACME Electric® |

| • | Kellems® | • | TayMac® | • | Hipotronics® | • | Powerohm™ | • | EC&M Design™ |

| • | Bryant® | • | Wiegmann® | • | Haefely® | | | | |

| Lighting | | | | |

| • | Kim Lighting® | • | Security Lighting Systems™Beacon Products™ | • | Spaulding Lighting™ | • | Kurt Versen™ | • | Litecontrol™

|

| • | Sportsliter Solutions™ | • | Columbia Lighting® | • | Alera Lighting® | • | Prescolite® | • | Dual-Lite®

|

| • | Beacon Products™Hubbell Building Automation™ | • | Precision Paragon™[P2]™ P2™ | • | Progress Lighting®Lighting Design® | • | Dual-Lite®Security Lighting Systems™ | • | Hubbell® Outdoor Lighting™ |

| • | Architectural Area Lighting™ | | | | | | | | |

| Construction and Energy | | | | |

| • | Hubbell Building Automation™Burndy® | • | Hubbell Outdoor Lighting™Killark® | • | LitecontrolGAI-Tronics® | • | Gas Breaker® | • | R.W. Lyall™ |

| • | CMC® | • | Hawke™ | • | Chalmit® | • | Vantage Technology® | • | Continental® |

| • | Austdac™ | | | | | | | | |

Power Segment

The Power segment (29%, 29% and 31%(30% of consolidated revenues in 2014, 20132016 and 2012, respectively)2015 and 29% in 2014) consists of operations that design and manufacture various distribution, transmission, substation and telecommunications products primarily used by the electrical utility industry. In addition, certain of these products are used in the civil construction and transportation industries. Products are sold to distributors and

directly to users such as electric utilities, telecommunication companies, pipeline and mining operations,

industrial firms, construction and engineering firms. While Hubbell believes its sales in this area are not materially dependent upon any customer or group of customers, a substantial decrease in purchases by electrical utilities would affect this segment.

|

| |

| 4 | HUBBELL INCORPORATED- Form 10-K | 4 |

Distribution, Transmission and Substation Utility Products

Hubbell manufactures and sells a wide variety of electrical distribution, transmission, substation utility and telecommunications products. These products include items such as:

|

| | | | | |

| • | Arresters | • | High voltage bushingsBushings | • | Grounding & bonding equipment |

| • | Cutouts & fuse links | • | Insulators | • | Programmable reclosers |

| • | Pole line hardware | • | Cable terminations & accessories | • | Sectionalizers |

| • | Helical anchors & foundations | • | Formed wire products | • | Lineman tools, hoses & gloves |

| • | Overhead, pad mounted & capacitor switches | • | Splices, taps & connectors | • | Polymer concrete & fiberglass enclosures and equipment pads |

These products are sold under the following brands and/or trademarks:

|

| | | | | | | |

| • | Ohio Brass® | • | Chance® | • | Anderson® | • | PenCell® |

| • | Fargo® | • | Hubbell® | • | Polycast® | • | Opti-loop Design™ |

| • | Quazite® | • | Quadri*sil® | • | Trinetics® | • | Reuel™ |

| • | Electro Composites™ | • | USCO™ | • | CDR™ | • | RFL Design® |

| • | Hot Box® | • | PCORE® | • | Delmar™ | • | Turner Electric® |

| • | EMC™ | • | Longbow™ | | | | |

Information Applicable to All General Categories

International Operations

The Company has several operations located outside of the United States. These operations manufacture, assemble and/or procure and market Hubbell products and service for both the Electrical and Power segments.

As a percentage of total net sales, shipments from foreign operations directly to third parties were 10% in 2016, 11% in 2015 and 14% in 2014, 16% in 2013 and 17% in 2012, with the Canadian and UK operations representing approximately 31%33% and 26%21%, respectively, of 20142016 total international net sales. Of the remaining 2016 international sales Switzerland, Brazil, and Mexico each represent 12%, 10% of 2014 total international sales., and 9%, respectively. See also Note 20-Industry19 — Industry Segments and Geographic Area Information in the Notes to Consolidated Financial Statements and Item 1A. Risk Factors relating to manufacturing in and sourcing from foreign countries.

Customers

The Company does not have any customers whose annual consolidated purchases exceed 10 percent of our total net sales in 2016, 2015 nor 2014.

Raw Materials

Raw materials used in the manufacture of Hubbell products primarily include steel, aluminum, brass, copper, bronze, plastics, phenolics, zinc, nickel, elastomers and petrochemicals. Hubbell also purchases certain electrical and electronic components, including solenoids, lighting ballasts, printed circuit boards, integrated circuit chips and cord sets, from a number of suppliers. Hubbell is not materially dependent upon any one supplier for raw materials used in the manufacture of its products and equipment, and at the present time, raw materials and components essential to its operation are in adequate supply. However, some of these principal raw

materials are sourced from a limited number of suppliers. See also Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

Patents

Hubbell has approximately 1,6001,700 active United States and foreign patents covering many of its products, which expire at various times. While Hubbell deems these patents to be of value, it does not consider its business to be dependent upon patent protection. Hubbell also licenses products under patents owned by others, as necessary, and grants licenses under certain of its patents.

Working Capital

Inventory, accounts receivable and accounts payable levels, payment terms and, where applicable, return policies are in accordance with the general practices of the electrical products industry and standard business procedures. See also Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Backlog

Substantially all of the backlog existing at December 31, 20142016 is expected to be shipped to customers in 2015.2017. Backlog of orders believed to be firm at December 31, 20142016 was approximately $333.7$297.4 million compared to $295.4$319.4 million at December 31, 2013.2015. Although this backlog is important, the majority of Hubbell’s revenues result from sales of inventoried products or products that have short periods of manufacture.

|

| |

HUBBELL INCORPORATED- Form 10-K | 5 |

Competition

Hubbell experiences substantial competition in all categories of its business, but does not compete with the same companies in all of its product categories. The number and size of competitors vary considerably depending on the product line. Hubbell cannot specify with precision the number of competitors

|

| |

HUBBELL INCORPORATED- Form 10-K

| 5 |

in each product category or their relative market position. However, some of its competitors are larger companies with substantial financial and other resources. Hubbell considers product performance, reliability, quality and technological innovation as important factors relevant to all areas of its business, and considers its reputation as a manufacturer of quality products to be an important factor in its business. In addition, product price, service levels and other factors can affect Hubbell’s ability to compete.

Research and Development

Research and development expenditures represent costs to discover and/or apply new knowledge in developing a new product or process, or in bringing about significant improvement in an existing product or process. Research and development expenses are recorded as a component of Cost of goods sold. Expenses for research and development were approximately 2% of Cost of goods sold for each of the years 2014, 20132016, 2015 and 2012.2014.

Environment

The Company is subject to various federal, state and local government requirements relating to the protection of employee health and safety and the environment. The Company believes that, as a general matter, its policies, practices and procedures are properly designed to prevent unreasonable risk of

environmental damage and personal injury to its employees and its customers’ employees and that the handling, manufacture, use and disposal of hazardous or toxic substances are in accordance with environmental laws and regulations.

Like other companies engaged in similar businesses, the Company has incurred or acquired through business combinations, remedial response and voluntary cleanup costs for site contamination and is a party to product liability and other lawsuits and claims associated with environmental matters, including past production of product containing toxic substances. Additional lawsuits, claims and costs involving environmental matters are likely to continue to arise in the future. However, considering past experience and reserves, the Company does not anticipate that these matters will have a material impact on earnings, capital expenditures, financial condition or competitive position. See also Item 1A. Risk Factors and Note 1514 — Commitments and Contingencies in the Notes to Consolidated Financial Statements.

Employees

As of December 31, 2014,2016, Hubbell had approximately 15,40017,400 salaried and hourly employees of which approximately 8,4007,500 of these employees, or 54%43%, are located in the United States. Approximately 2,4002,100 of these U.S. employees are represented by 1715 labor unions. Hubbell considers its labor relations to be satisfactory.

|

| |

| 6 | HUBBELL INCORPORATED- Form 10-K | 6 |

Executive Officers of the Registrant

|

| | | | |

| Name | Age(1) | Present Position | Business Experience | |

| David G. Nord | 5759 | Chairman of the Board, President and Chief Executive Officer | Present position since May 2014; President and Chief Executive Officer since January 2013; President and Chief Operating Officer from June 2012 to January 2013, and Senior Vice President and Chief Financial Officer from September 2005 to June 2012. Previously, various positions, including Vice President, Controller, of United Technologies and its subsidiaries, 2000-2005. | |

| William R. Sperry | 5254 | Senior Vice President and Chief Financial Officer | Present position since June 6, 2012; Vice President, Corporate Strategy and Development August 15, 2008 to June 6, 2012; previously, Managing Director, Lehman Brothers August 2006 to April 2008, various positions, including Managing Director, of J.P. Morgan and its predecessor institutions, 1994-2006. |

Gary N. Amato | 63 | Executive Vice President

(Electrical Segment)

| Present position since June 30, 2014; Group Vice President (Electrical Systems) December 2008- June 30, 2014; Group Vice President (Electrical Products) October 2006-December 2008; Vice President October 1997-September 2006; Vice President and General Manager of the Company’s Industrial Controls Divisions (ICD) 1989-1997; Marketing Manager, ICD, April 1988-March 1989. |

| Gerben W. Bakker | 5052 | Group Vice President, (Power Systems)Systems

| Present position since February 1, 2014; previously, Division Vice President, Hubbell Power Systems, Inc. (“HPS”) August 2009 - February 1, 2014; President, HPS Brazil June 2005 – July 2009; Vice President, Sourcing, HPS March 2004 – May 2005. |

James H. Biggart, Jr. | 62 | Vice President and Treasurer | Present position since January 1, 1996; Treasurer since 1987; Assistant Treasurer 1986-1987; Director of Taxes 1984-1986. |

| Joseph A. Capozzoli | 4042 | Vice President and

Controller | Present position since April 22, 2013; previously, Assistant Corporate Controller of Stanley Black & Decker, Inc. (“Stanley”) April 2011 to April 2013; Global Operations Controller at Stanley 2010-2011; Director of Cost Accounting at Stanley, 2006-2010. | |

| An-Ping Hsieh | 5456 | Senior Vice President, General

Counsel | Present position since May 3, 2016; previously Vice President, General Counsel, September 4, 2012; previously,2012 - May 2016; Vice President, Secretary and Associate General Counsel of United Technologies Corporation (“UTC”) February 2008 to September 2012; Vice President and General Counsel, UTC Fire and Security 2003-2008; Deputy General Counsel, Otis Elevator Company, a United Technologies company 2001-2003. | |

| Maria R. Lee | 41 | Treasurer and Vice President, Corporate Strategy and Investor Relations | Present position since January 1, 2016; previously Vice President, Corporate Strategy and Investor Relations, March 2015-December 2015; Director, Investor Relations of United Technologies Corporation (“UTC”) 2011-2012; various positions, including Director, Financial Planning & Analysis, North and South America Area, Otis Elevator Company, at UTC, 2006-2011; various positions at Duff & Phelps, Affiliated Managers Group, Inc., and Booz Allen Hamilton, 1997-2006. | |

| Stephen M. Mais | 5052 | Senior Vice President,

Human Resources | Present position since May 3, 2016, previously Vice President, Human Resources, August 22, 2005; previously2005 - May 2016; Director, Staffing and Capability, Pepsi Bottling Group (“Pepsi”) 2001-2005; Director, Human Resources Southeastern U.S., Pepsi 1997-2001. | |

W. Robert MurphyKevin A. Poyck | 6547 | Executive ViceGroup President,

Marketing and Sales Lighting | Present position since OctoberJune 1, 2007; Senior Group2015; previously, Vice President, 2001-2007; GroupGeneral Manager, Commercial and Industrial Lighting, Hubbell Lighting, Inc. ("HLI") 2014 - 2015; Vice President, 2000-2001; SeniorBrand Management, Commercial and Industrial, HLI 2012-2014; Vice President, Marketing and Sales (Wiring Systems) 1985-1999; and various sales positions (Wiring Systems) 1975-1985.Operations, HLI 2009 - 2012; Vice President, Engineering, HLI 2005-2009. | |

William T. TolleyRodd R. Ruland | 5759 | Senior ViceGroup President,

Growth Construction and InnovationEnergy | Present position since FebruaryJune 1, 2014,2015; previously, GroupPresident, BURNDY LLC, Hubbell Canada (HCLP) & Hubbell de Mexico (HdM) 2012-2015; President, BURNDY LLC 2009-2012; Corporate Vice President (Power Systems) December 23, 2008-February& General Manager, Electrical Power Interconnect Division, FCI (BURNDY) 2003-2009, Director, Business Development 2001-2003; various positions in Sales & Marketing, Business Development, and General Management and TycoElectronics/AMP Incorporated 1979-2000. | |

| Darrin S. Wegman | 49 | Group President, Commercial and Industrial | Present position since June 1, 2014; Group2015; previously, Vice President, (Wiring Systems) October 1, 2007-December 23, 2008; SeniorGeneral Manager, Wiring Device and Industrial Electrical business, 2013-2015; Vice President, of Operations and Administration (Wiring Systems) October 2005-October 2007; Director of Special Projects April 2005-October 2005; administrative leave November 2004-April 2005; SeniorController, Hubbell Incorporated, 2008-2013; Vice President and Chief Financial Officer February 2002-November 2004.Controller, Hubbell Industrial Technology, 2002-2008; Controller, GAI-Tronics Corporation, 2000-2002. | |

| |

| (1) | As of February 19, 2015.16, 2017. |

There are no family relationships between any of the above-named executive officers. For information related to our Board of Directors, refer to Item 10. Directors, Executive Officers and Corporate Governance.

|

| |

HUBBELL INCORPORATED - Form 10-K | 7 |

ITEM 1A Risk Factors

Our business, operating results, financial condition, and cash flows may be impacted by a number of factors including, but not limited to those set forth below. Any one of these factors could cause our actual results to vary materially from recent results or future anticipated results. See also Item 7. Management’s Discussion and Analysis — “Executive Overview of the Business”, “Outlook”, and “Results of Operations”.

Global economic uncertainty could adversely affect us.

During periods of prolonged slow growth, or a downturn in conditions in the worldwide or domestic economies, we could experience reduced orders, payment delays, supply chain disruptions or other factors caused by economic challenges faced by our customers, prospective customers and suppliers. Depending upon their severity and duration, these conditions could have an adverse impact on our results of operations, financial condition and cash flows.

We operate in markets that are subject to competitive pressures that could affect selling prices or demand for our products.

We compete on the basis of product performance, quality, service and/or price. Competitors' behavior related to these areas could potentially have significant impacts on our financial results. Our competitive strategy is to design and manufacture high quality products at the lowest possible cost. Our strategy is to also increase selling prices to offset rising costs of raw materials and components. Competitive pricing pressures may not allow us to offset some or all of our increased costs through pricing actions. Alternatively, if raw material and component costs decline, the Company may not be able to maintain current pricing levels. Competition could also affect future selling prices or demand for our products which could have an adverse impact on our results of operations, financial condition and cash flows.

Global economic uncertainty could adversely affect us.

During periods of prolonged slow growth, or a downturn in conditions in the worldwide or domestic economies, we could experience reduced orders, payment delays, supply chain disruptions or other factors caused by economic challenges faced by our customers, prospective customers and suppliers. Depending upon their severity and duration, these conditions could have an adverse impact on our results of operations, financial condition and cash flows.

We may not be able to successfully implement initiatives, including our restructuring activities, that improve productivity and streamline operations to control or reduce costs.

Achieving our long-term profitability goals depends significantly on our ability to control or reduce our operating costs. Because many of our costs are affected by factors outside, or substantially outside, our control, we generally must seek to control or reduce costs through productivity initiatives. If we are not able to identify and implement initiatives that control or reduce costs and increase operating efficiency, or if the cost savings initiatives we have implemented to date do not generate expected cost savings, our financial results could be adversely impacted. Our efforts to control or reduce costs may include restructuring activities involving workforce reductions, facility consolidations and other cost reduction initiatives. If we do not successfully manage our current restructuring activities, or any other restructuring activities that we may undertake in the future, expected efficiencies and benefits may be delayed or not realized, and our operations and business could be disrupted.

We manufacture and source products and materials from various countries throughout the world. A disruption in the availability, price or quality of these products or materials could impact our operating results.

Our business is subject to risks associated with global manufacturing and sourcing. We use a variety of raw materials in the production of our products including steel, aluminum, brass, copper, bronze, zinc, nickel and plastics. We also purchase certain electrical and electronic components, including solenoids,lighting ballasts, printed circuit boards and integrated circuit chips and cord sets from third party providers.a number of suppliers. Significant shortages in

the availability of these materials or significant price increases could increase our operating costs and adversely impact the competitive positions of our products, which could adversely impact our results of operations.

We continue to increase the amount ofrely on materials, components and finished goods that are sourced from or manufactured in foreign countries including Mexico, China, and other international countries. Political instability in any country where we do business could have an adverse impact on our results of operations.

We rely on our suppliers to produce high quality materials, components and finished goods according to our specifications. Although we have quality control procedures in place, there is a risk that products may not meet our specifications which could impact our ability to ship quality products to our customers on a timely basis, which could adversely impact our results of operations.

Future tax law changes could increase our prospective tax expense. In addition, tax payments may ultimately differ from amounts currently recorded by the Company.

We are subject to income taxes as well as non-income based taxes, in both the United States and variousnumerous foreign jurisdictions. The determination of the Company's worldwide provision for income taxes and other tax liabilities requires judgment and is based on diverse legislative and regulatory structures that exist in the various jurisdictions where the company operates. As a result of the U.S. federal elections, there may be changes in tax policy pursued by the new administration, and the nature and outcome of those potential changes is uncertain at this time. Although management believes its estimates are reasonable, the ultimate tax outcome may differ from the amounts recorded in its financial statements and may adversely affect the Company's financial results for the period when such determination is made. We are subject to ongoing tax audits in various jurisdictions. Tax authorities may disagree with certain positions we have taken and assess additional taxes. We regularly assess the likely outcomes of these audits in order to determine the appropriateness of our tax provisions. However, there can be no assurance that we will accurately predict the outcomes of these audits, and the future outcomes of these audits could adversely affect our results of operations, financial condition and cash flows.

|

| |

| 8 | HUBBELL INCORPORATED - Form 10-K |

Significant developments stemming from the recent U.S. federal elections could have a material adverse effect on us.

As a result of the recent U.S. federal elections, there may be changes to existing trade agreements, like the North American Free Trade Agreement ("NAFTA"), and proposed trade agreements, like the Trans-Pacific Partnership ("TPP"), greater restrictions on free trade generally, significant increases in tariffs on goods imported into the United States particularly tariffs on products manufactured in Mexico, among other possible changes. Changes in U.S. social, political, regulatory and economic conditions or in laws and policies governing foreign trade, manufacturing, development and investment in the territories and countries where we currently manufacture and sell products, and any resulting negative sentiments towards the United States as a result of such changes, could have an adverse effect on our business.

We engage in acquisitions and strategic investments and may encounter difficulty in obtaining appropriate acquisitions and in integrating these businesses.

Part of the Company’s future growth strategy involves acquisitions. We have pursued and will continue to seek acquisitions and other strategic investments to complement and expand our existing businesses. The rate and extent to which acquisitions become available may impact our growth rate. The success of these transactions will depend on our ability to integrate these businesses into our operations and realize the planned synergies. We may encounter difficulties in integrating acquisitions into our operations and in managing strategic investments.investments and foreign acquisitions and joint ventures may also present additional risk related to the integration of operations across different cultures and languages. Failure to effectively complete or manage

|

| |

HUBBELL INCORPORATED- Form 10-K

| 8 |

acquisitions may adversely affect our existing businesses as well as our results of operations, financial condition and cash flows.

We are subject to risks surrounding our information systems.systems failures, network, disruptions and breaches in data security.

The proper functioning of Hubbell’s information systems is critical to the successful operation of our business. Although our information systems are protected with robust backup and security systems, these systems are still susceptible to cyber threats, outages due to fire, floods, power loss, telecommunications failures, viruses, break-ins and similar events, or breaches of physical security. A failure of our information technology systems could impact our ability to process orders, maintain proper levels of inventory, collect accounts receivable and pay expenses; all of which could have an adverse effect on our results of operations, financial condition and cash flows. In addition, security breaches could result in unauthorized disclosure of confidential information that may result in financial or reputational damage to the Company.

We have continued to work on improving our utilization of our enterprise resource planning system, expanding standardization of business processes and performing implementations at our remaining businesses. We expect to incur additional costs related to future implementations, process reengineering efforts as well as enhancements and upgrades to the system. These system modifications and implementations

could result in operating inefficiencies which could adversely impact our operating results and/or our ability to perform necessary business transactions.

Our success depends on attracting and retaining qualified personnel.

Our ability to sustain and grow our business requires us to hire, retain and develop a highly skilled and diverse management team and workforce. Failure to ensure that we have the depth and breadth of personnel with the necessary skill set and experience, or the loss of key employees, could impede our ability to deliver our growth objectives and execute our strategy.

Deterioration in the credit quality of our customers could have a material adverse effect on our operating results and financial condition.

We have an extensive customer base of distributors, wholesalers, electric utilities, OEMs, electrical contractors, telecommunications companies and retail and hardware outlets. We are not dependent on a single customer, however, our top ten customers account for approximately one-third of our net sales. Deterioration in the credit quality of several major customers could adversely affect our results of operations, financial condition and cash flows.

Inability to access capital markets or failure to maintain our credit ratings may adversely affect our business.

Our ability to invest in our business and make strategic acquisitions may require access to the capital markets. If general economic and capital market conditions deteriorate significantly, it could impact our ability to access the capital markets.capital. Failure to maintain our credit ratings could also impact our ability to access credit markets and could adversely impact our cost of borrowing. While we have not encountered significant financing difficulties recently, the capital and credit markets have experienced significant volatility in recent years. Market conditions could make it more difficult for us to access capital to finance our investments and acquisitions. This could adversely affect our results of operations, financial condition and cash flows.

If the underlying investments of our defined benefit plans do not perform as expected, we may have to make additional contributions to these plans.

We sponsor certain pension and other postretirement defined benefit plans. The performance of the financial markets and interest rates impact these plan expenses and funding obligations. Significant changes in market interest rates, investment losses on plan assets and reductions in discount rates may increase our funding obligations and could adversely impact our results of operations, cash flows, and cash flows.financial condition. Furthermore, there can be no assurance that the value of the defined benefit plan assets will be sufficient to meet future funding requirements.

|

| |

HUBBELL INCORPORATED- Form 10-K | 9 |

Volatility in currency exchange rates may adversely affect our financial condition, results of operations and cash flows.

Our international operations accounted for approximately 14%10% of our net sales in 2014.2016. We are exposed to the effects (both positive and negative) that fluctuating exchange rates have on translating the financial statements of our international operations, most of which are denominated in local currencies, into the U.S. dollar. Fluctuations in exchange rates may affect

product demand and reported profits in our international operations. In addition, currency fluctuations may affect the prices we pay suppliers for materials used in our products. As a result, fluctuating exchange rates may adversely impact our results of operations and cash flows.

Our success depends on attracting and retaining qualified personnel.

Our ability to sustain and grow our business requires us to hire, retain and develop a highly skilled and diverse management team and workforce. Failure to ensure that we have the depth and breadth of personnel with the necessary skill set and experience could impede our ability to deliver our growth objectives and execute our strategy.

Our reputation and our ability to conduct business may be impaired by improper conduct by any of our employees, agents or business partners.

We cannot provide absolute assurance that our internal controls and compliance systems will always protect us from acts committed by our employees, agents or business partners that would violate U.S. and/or non-U.S. laws, including the laws governing payments to government officials, bribery, fraud, anti-kickback and false claims rules, competition, export and import compliance, money laundering and data privacy. In particular, the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act, and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to government officials for the purpose of obtaining or retaining business, and we operate in parts of the world that have experienced governmental corruption to some degree. Despite meaningful measures that we undertake to facilitate lawful conduct, which include training and internal control policies, these measures may not always prevent reckless or criminal acts by our employees or agents. Any such improper actions could damage our reputation and subject us to civil or criminal investigation in the United States and in other jurisdictions, could lead to substantial civil and criminal,

|

| |

HUBBELL INCORPORATED- Form 10-K

| 9 |

monetary and non-monetary penalties and could cause us to incur significant legal and investigative fees.

Our inability to effectively develop and introduce new products could adversely affect our ability to compete.

New product introductions and enhancement of existing products and services are key to the Company’s competitive strategy. The success of new product introductions is dependent on a number of factors, including, but not limited to, timely and successful development of new products, market acceptance of these products and the Company’s ability to manage the risks associated with these introductions. These risks include production capabilities, management of inventory levels to support anticipated demand, the risk that new products may have quality defects in the early stages of introduction, and obsolescence risk of existing products. The Company cannot predict with certainty the ultimate impact new product introductions could have on our results of operations, financial condition or cash flows.

We could incur significant and/or unexpected costs in our efforts to successfully avoid, manage, defend and litigate intellectual property matters.

The Company relies on certain patents, trademarks, copyrights, trade secrets and other intellectual property of which the Company cannot be certain that others have not and will not infringe upon. Although management believes that the loss or expiration of any single intellectual property right would not have a material impact on its operating results, intellectual property litigation could be costly and time consuming and the Company could incur significant legal expenses pursuing these claims against others.

From time to time, we receive notices from third parties alleging intellectual property infringement. Any dispute or litigation involving intellectual property could be costly and time-consuming due to the complexity and the uncertainty of intellectual property litigation. Our intellectual property portfolio may not be useful in asserting a counterclaim, or negotiating a license, in response to a claim of infringement or misappropriation. In addition, as a result of such claims, the Company may lose its rights to utilize critical technology or may be required to pay substantial damages or license fees with respect to the infringed rights or be required to redesign our products at a substantial cost, any of which could negatively impact our operating results. Even if we successfully defend against claims of infringement, we may incur significant costs that could adversely affect our results of operations, financial condition and cash flow. See Item 3 “Legal Proceedings” for a discussion of our legal proceedings.

We may be required to recognize impairment charges for our goodwill and other intangible assets.

As of December 31, 2014,2016, the net carrying value of our goodwill and other intangible assets totaled approximately $1.2$1.4 billion. As required by generally accepted accounting principles, we periodically assess these assets to determine if they are impaired. Impairment of intangibles assets may be triggered by developments both within and outside the Company’s control. Deteriorating economic conditions, technological changes, disruptions to our business, inability to effectively integrate acquired businesses, unexpected significant changes or

planned changes in use of the assets, intensified competition, divestitures, market capitalization declines and other factors may impair our goodwill and other intangible assets. Any charges relating to such impairments could adversely affect our results of operations in the periods an impairment is recognized.

We have two classes of common stock with different voting rights, which results in a concentration of voting power of our common stock.

As of December 31, 2014, the holders of our Class A Common Stock (with 20 votes per share) held approximately 74% of the voting power represented by all outstanding shares of our common stock and approximately 13% of the Company’s total equity value, and the Hubbell Trust and Roche Trust collectively held approximately 49% of our Class A Common Stock. The holders of the Class A Common Stock thus are in a position to influence matters that are brought to a vote of the holders of our common stock, including, among others, the election of the board of directors, any amendments to our charter documents, and the approval of material transactions. In order to further the interests of our shareholders, the Company routinely reviews various alternatives to meet its capital structure objectives, including equity, reclassification and debt transactions. |

| |

| 10 | HUBBELL INCORPORATED - Form 10-K |

We are subject to litigation and environmental regulations that may adversely impact our operating results.

We are a party to a number of legal proceedings and claims, including those involving product liability, intellectual property and environmental matters, which could be significant. It is not possible to predict with certainty the outcome of every claim and lawsuit. In the future, we could incur judgments or enter into settlements of lawsuits and claims that could have a materially adverse effect on our results of operations, cash flows. and financial condition. In addition, while we maintain insurance coverage with respect to certain claims, such insurance may not provide adequate coverage against such claims. We establish reserves based on our assessment of contingencies, including contingencies related to legal claims asserted against us. Subsequent developments in legal proceedings may affect our assessment and estimates of the loss contingency recorded as a reserve and require us to make additional payments, which could have a materially adverse effect on our results of operations, financial condition and cash flow.

We are also subject to various laws and regulations relating to environmental protection and the discharge of materials into the environment, and we could incur substantial costs as a result of the noncompliance with or liability for clean up or other costs or damages under environmental laws. In addition, we could be affected by future laws or regulations, including those imposed in response to climate change concerns. Compliance with any future laws and regulations could result in a materially adverse affecteffect on our business and financial results. See Item 3 “Legal Proceedings” for a discussion of our legal proceedings.

|

| |

HUBBELL INCORPORATED- Form 10-K

| 10 |

New regulationsRegulations related to conflict-free minerals may cause us to incur additional expenses and may create challenges with our customers.

The Dodd-Frank Wall Street Reform and Consumer Protection Act contains provisions to improve transparency and accountability regarding the use of “conflict” minerals mined from the Democratic Republic of Congo and adjoining countries (“DRC”). In August 2012 theThe SEC has established annual disclosure and reporting requirements for those companies who use “conflict” minerals sourced from the DRC in their products. These new requirements could limit the pool of suppliers who can provide conflict-free minerals and as a result, we cannot ensure that we will be able to obtain these conflict-free minerals at competitive prices. Compliance with these new requirements may also increase our costs. In addition, we may face challenges with our customers if we are unable to sufficiently verify the origins of the minerals used in our products.

Health care reform could adversely affect our operating results.

In 2010, the United States federal government enacted comprehensive health care reform legislation. Due to the breadth and complexity of this legislation, as well as its phased-in nature of implementation and lack of interpretive guidance, it

is difficult for the Company to predict the overall effects it will have on our business. To date, the Company has not experienced material costs related to the health care reform legislation, however, it is possible that our operating results could be adversely affected in the future by increased costs, expanded liability exposure and requirements that change the ways we provide healthcare and other benefits to our employees.

We face the potential harms of natural disasters, terrorism, acts of war, international conflicts or other disruptions to our operations.

Natural disasters, acts or threats of war or terrorism, international conflicts, and the actions taken by the United States and other governments in response to such events could cause damage to or disrupt our business operations, our suppliers or our customers, and could create political or economic instability, any of which could have an adverse effect on our business. Although it is not possible to predict such events or their consequences, these events could decrease demand for our products, make it difficult or impossible for us to deliver products, or disrupt our supply chain.

ITEM 1B Unresolved Staff Comments

None

|

| |

HUBBELL INCORPORATED - Form 10-K | 11 |

ITEM 2 Properties

As of January 31, 2017, Hubbell’s global headquarters are located in leased office space in Shelton, Connecticut. Other principal administrative offices are in Columbia, South Carolina, Greenville, South Carolina and Manchester, New Hampshire. Hubbell's manufacturing and warehousing facilities, classified by reporting segment, are located in the following countries. The Company believes its manufacturing and warehousing facilities are adequate to carry on its business activities.

| | | | | Number of Facilities | Total Approximate Floor Area in Square Feet | | Number of Facilities | Total Approximate Floor Area in Square Feet |

| Segment | Location | Warehouses |

| Manufacturing |

| Owned |

| | Leased |

| Location | Warehouses |

| Manufacturing |

| Owned |

| Leased |

|

| Electrical segment | United States | 12 |

| 33 |

| 3,511,100 |

| | 1,677,600 |

| United States | 11 |

| 25 |

| 3,089,800 |

| 2,052,300 |

|

| | Australia | 1 |

| 2 |

| — |

| | 39,600 |

| Australia | — |

| 2 |

| — |

| 31,700 |

|

| | Brazil | — |

| 1 |

| 105,900 |

| | — |

| Brazil | — |

| 1 |

| 105,900 |

| — |

|

| | Canada | 2 |

| 3 |

| 178,700 |

| | 24,700 |

| Canada | 1 |

| 2 |

| 178,700 |

| 2,300 |

|

| | Italy | — |

| 1 |

| — |

| | 8,100 |

| Italy | — |

| 1 |

| — |

| 8,100 |

|

| | Mexico | 1 |

| 3 |

| 665,700 |

| | 43,300 |

| Mexico | 1 |

| 4 |

| 828,800 |

| 174,300 |

|

| | China | — |

| 2 |

| — |

| | 287,900 |

| China | — |

| 2 |

| — |

| 287,900 |

|

| | Puerto Rico | — |

| 1 |

| 162,400 |

| | — |

| Puerto Rico | — |

| 1 |

| 162,400 |

| — |

|

| | Singapore | 1 |

| — |

| — |

| | 8,700 |

| Singapore | 1 |

| — |

| — |

| 8,700 |

|

| | Switzerland | — |

| 1 |

| 95,000 |

| | — |

| Switzerland | — |

| 1 |

| 95,000 |

| — |

|

| | United Kingdom | 1 |

| 4 |

| 133,600 |

| | 53,600 |

| United Kingdom | 2 |

| 3 |

| 122,200 |

| 64,600 |

|

| Power segment | United States | 1 |

| 13 |

| 2,438,500 |

| | 157,000 |

| United States | 1 |

| 14 |

| 2,638,300 |

| 149,700 |

|

| | Brazil | — |

| 1 |

| 138,300 |

| | — |

| Brazil | — |

| 2 |

| 188,100 |

| 24,000 |

|

| | Canada | — |

| 1 |

| 30,000 |

| | — |

| Canada | — |

| 1 |

| 30,000 |

| — |

|

| | Mexico | 1 |

| 1 |

| 167,300 |

| (1) | 181,100 |

| Mexico | 1 |

| 1 |

| 167,300 |

| 181,200 |

|

| | China | 1 |

| 1 |

| — |

| | 74,600 |

| China | — |

| 3 |

| — |

| 226,100 |

|

| TOTAL | | 21 |

| 68 |

| 7,626,500 |

| | 2,556,200 |

| | 18 |

| 63 |

| 7,606,500 |

| 3,210,900 |

|

(1) The Power segment shares an owned manufacturing building in Mexico with the Electrical segment. The building is included in the Electrical segment facility count.

|

| |

| 12 | HUBBELL INCORPORATED - Form 10-K |

ITEM 3 Legal Proceedings

The Company is subject to various legal proceedings arising in the normal course of its business. These proceedings include claims for damages arising out of use of the Company’s products, intellectual property, workers’ compensation and environmental matters. The Company is self-insured up to specified limits for certain types of claims, including product liability and workers’ compensation, and is fully self-insured for certain other types of claims, including environmental and intellectual property matters. The Company recognizes a liability for any contingency that in management’s judgment is probable of occurrence and can be reasonably estimated. We continually reassess the likelihood of adverse judgments and outcomes in these matters, as well as estimated ranges of possible losses based upon an analysis of each matter which includes

consideration of outside legal counsel and, if applicable, other experts. Information required by this item is incorporated herein by reference to the section captioned “Notes to Consolidated Financial Statements, Note 14 — Commitments and Contingencies” of this Form 10-K.

In the fourth quarter of 2014, the Company settled litigation involving Powerweb Energy, Inc. (“Powerweb”). The lawsuit had alleged claims arising from the Company’s development and sale of wiHUBB wireless lighting technology. The Company believes that it had meritorious defenses against the claims and had vigorously defended itself in the matter. During 2013, the Company recorded an accrual equal to the low end of its estimated range of outcome. During the third quarter of 2014 the parties engaged in settlement discussions and the Company increased the accrual by $4.0 million based on those discussions. In view of several considerations including the inherent uncertainty of litigation, and the expense of a trial, the Company settled the litigation. The settlement payment made by the Company did not exceed the amounts previously reserved for the litigation.

ITEM 4 Mine Safety Disclosures

Not applicable.

|

| |

HUBBELL INCORPORATED - Form 10-K | 1213 |

ITEM 5 Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company’sOn December 23, 2015 the Company completed the Reclassification of its dual-class common stock into a single class of Common Stock. Trading in the Class A common stock and Class B common stock ceased after markets closed on December 23, 2015 and trading in the Company's single class of Common Stock commenced on the New York Stock Exchange ("NYSE") on December 24, 2015. The Company’s Common Stock is principally traded on the New York Stock ExchangeNYSE. Prior to the Reclassification the Company's Class A common stock traded under the symbols “HUBA”symbol “HUB.A” and “HUBB”the Company's Class B common stock traded under the symbol “HUB.B”. The Common Stock, resulting from the Reclassification, trades under the symbol "HUBB". See Note 15 — Capital Stock in the Notes to Consolidated Financial Statements for more information about the Reclassification.

The information required by Item 5 with respect to securities authorized for issuance under equity compensation plans is incorporated herein by reference to Part III, Item 12 of this Form 10-K.

The following tables provide information on market prices, dividends declared, number of common shareholders, and repurchases by the Company of shares of its Class A andcommon stock, Class B common stock, and the Common Stock.Stock resulting from the Reclassification.

| | Market Prices (Dollars Per Share) | | Class A Common | | Class B Common | | Class A Common | | Class B Common | | Common Stock |

| Years Ended December 31, | | High |

| Low |

| | High |

| Low |

| | High |

| Low |

| | High |

| High |

| | High |

| Low |

|

| 2014 — Fourth quarter | |

| 131.60 |

| 105.27 |

| | 127.29 |

| 101.44 |

| |

| 2014 — Third quarter | |

| 129.50 |

| 120.22 |

| | 126.96 |

| 115.34 |

| |

| 2014 — Second quarter | |

| 125.68 |

| 104.20 |

| | 125.40 |

| 112.71 |

| |

| 2014 — First quarter | |

| 114.00 |

| 94.24 |

| | 122.55 |

| 106.47 |

| |

| 2013 — Fourth quarter | |

| 97.98 |

| 91.02 |

| | 109.29 |

| 101.51 |

| |

| 2013 — Third quarter | |

| 99.91 |

| 89.40 |

| | 110.90 |

| 99.63 |

| |

| 2013 — Second quarter | |

| 93.51 |

| 83.08 |

| | 102.68 |

| 91.94 |

| |

| 2013 — First quarter | |

| 88.00 |

| 78.62 |

| | 97.73 |

| 84.80 |

| |

| 2016 — Fourth quarter | | | — |

| — |

| | — |

| — |

| | 119.05 |

| 101.15 |

|

| 2016 — Third quarter | | |

| — |

| — |

| | — |

| — |

| | 109.33 |

| 101.72 |

|

| 2016 — Second quarter | | |

| — |

| — |

| | — |

| — |

| | 111.23 |

| 97.35 |

|

| 2016 — First quarter | | |

| — |

| — |

| | — |

| — |

| | 106.66 |

| 83.16 |

|

| 2015 — Fourth quarter (After the Reclassification) | | |

| — |

| — |

| | — |

| — |

| | 104.47 |

| 99.60 |

|

| 2015 — Fourth quarter (Prior to Reclassification) | | | 128.17 |

| 108.12 |

| | 100.73 |

| 100.73 |

| | — |

| — |

|

| 2015 — Third quarter | | |

| 122.02 |

| 91.67 |

| | 109.40 |

| 109.40 |

| | — |

| — |

|

| 2015 — Second quarter | | |

| 118.84 |

| 105.48 |

| | 112.84 |

| 112.84 |

| | — |

| — |

|

| 2015 — First quarter | | |

| 113.02 |

| 104.50 |

| | 117.03 |

| 117.03 |

| | — |

| — |

|

| | | | | | | |

Dividends Declared (Dollars Per Share) | |

| Class A Common | | Class B Common | |

| Class A Common | | Class B Common | | Common Stock |

| Years Ended December 31, | |

| 2014 |

| 2013 |

| | 2014 |

| 2013 |

| |

| 2016 |

| 2015 |

| | 2016 |

| 2015 |

| | 2016 |

| 2015 |

|

| Fourth quarter | | |

| — |

| 0.63 |

| | — |

| — |

| | 0.70 |

| — |

|

| Third quarter | | |

| — |

| 0.56 |

| | — |

| — |

| | 0.63 |

| — |

|

| Second quarter | | |

| — |

| 0.56 |

| | — |

| — |

| | 0.63 |

| — |

|

| First quarter | |

| 0.50 |

| 0.45 |

| | 0.50 |

| 0.45 |

| |

| — |

| 0.56 |

| | — |

| — |

| | 0.63 |

| — |

|

| Second quarter | |

| 0.50 |

| 0.45 |

| | 0.50 |

| 0.45 |

| |

| Third quarter | |

| 0.50 |

| 0.45 |

| | 0.50 |

| 0.45 |

| |

| Fourth quarter | |

| 0.56 |

| 0.50 |

| | 0.56 |

| 0.50 |

| |

| | | | | | | |

| Number of Common Shareholders of Record | |

| |

| |

| | |

| |

| |

| |

| |

| | |

| |

| | |

| At December 31, | 2014 |

| 2013 |

| 2012 |

| | 2011 |

| 2010 |

| 2016 |

| 2015 |

| 2014 |

| | 2013 |

| 2012 |

| | |

| Class A | 369 |

| 394 |

| 426 |

| | 458 |

| 483 |

| — |

| — |

| 369 |

| | 394 |

| 394 |

| | |

| Class B | 2,093 |

| 2,225 |

| 2,389 |

| | 2,549 |

| 2,731 |

| — |

| — |

| 2,093 |

| | 2,225 |

| 2,225 |

| | |

| Common Stock | | 2,003 |

| 2,548 |

| — |

| | — |

| — |

| | |

Our dividends are declared at the discretion of our Board of Directors. In October 2014,2016, the Company’s Board of Directors approved an increase in the common stock dividend rate from $0.50$0.63 to $0.56$0.70 per share per quarter. The increased quarterly dividend payment commenced with the December 15, 20142016 payment made to the shareholders of record on November 28, 2014.30, 2016.

|

| |

| 14 | HUBBELL INCORPORATED - Form 10-K |

Purchases of Equity Securities

In September 2011,As of December 31, 2015, we had $141.4 million of remaining share repurchase authorization under the share repurchase program authorized by our Board of Directors approved a stockon October 21, 2014 (the "October 2014 program") and $250 million of remaining share repurchase authorization under the share repurchase program and authorized the repurchase of up to $200 million of Class A and Class B Common Stock. During

2014, the Company spent $35.0 million on the repurchase of

common shares under the September 2011 program prior to its expiration in September 2014. In October 2014, theby our Board of Directors approvedon August 23, 2015 (the "August 2015 program"), for a new stocktotal remaining share repurchase program ("October 2014 program") and authorizedauthorization of $391.4 million. In 2016, the Company repurchased shares for an aggregate purchase price of $237.8 million. As a result, as of December 31, 2016, our remaining share repurchase of up to $300 million of Class A and Class B Common Stock. The October 2014 programauthorization was $153.6 million. Our remaining share repurchase authorization expires in October 2017. As of December 31, 2014, approximately $229.5 million remains authorized for future repurchases under the October 2014 program. Depending uponSubject to numerous factors, including market conditions and alternative uses of cash, we may conduct discretionary repurchases through open market andor privately negotiated transactions, during our normal trading windows. which may include repurchases under plans complying with Rules 10b5-1 and 10b-18 under the Securities Exchange Act of 1934, as amended.

The Company did notfollowing table summarizes the Company's repurchase any Class Aactivity of Common Stock during 2014.the quarter ended December 31, 2016:

|

| | | | | | | | |

| | Total Number of Shares of Common Stock Purchased |

| Average Price Paid Per Share of Common Stock |

| Approximate Value of Shares that May Yet Be Purchased Under the Programs |

|

| Period | (000’s) |

| Share |

| (in millions) |

|

| BALANCE AS OF SEPTEMBER 30, 2016 | |

| |

| $ | 153.6 |

|

| October 2016 | — |

| $ | — |

| $ | 153.6 |

|

| November 2016 | — |

| $ | — |

| $ | 153.6 |

|

| December 2016 | — |

| $ | — |

| $ | 153.6 |

|

| TOTAL FOR THE QUARTER ENDED DECEMBER 31, 2016 | — |

| $ | — |

| |

|

| |

HUBBELL INCORPORATED - Form 10-K | 1315 |

The following table summarizes the Company's repurchase activity of Class B Common Stock during the quarter ended December 31, 2014:

|

| | | | | | | | | | | |

| | | Total Number of Class B Shares Purchased (000's) | | Average Price Paid per Class B Share | | Approximate Value of Shares that May Yet Be Purchased Under the Programs (in millions) |

| BALANCE AS OF SEPTEMBER 30, 2014 | | | | | | $ | — |

|

| October 2014 | | 200 |

| | $ | 109.35 |

| | $ | 278.1 |

|

| November 2014 | | 431 |

| | $ | 111.67 |

| | $ | 230.0 |

|

| December 2014 | | 5 |

| | $ | 102.09 |

| | $ | 229.5 |

|

| TOTAL FOR THE QUARTER ENDED DECEMBER 31, 2014 | | 636 |

| | $ | 110.87 |

| | $ | 229.5 |

|

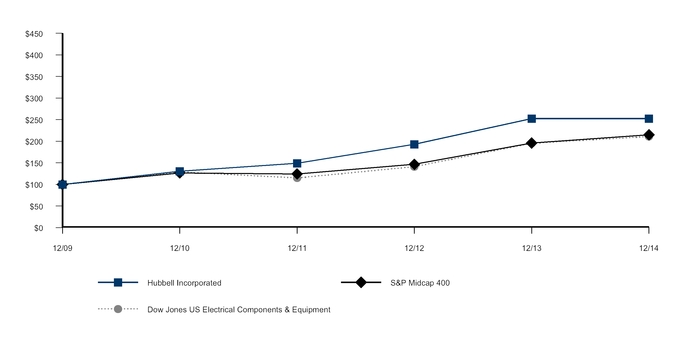

Corporate Performance Graph

The following graph compares the total return to shareholders on the Company’s Class B Common Stockcommon stock during the five years ended December 31, 2014,2016, with a cumulative total return on the (i) Standard & Poor’s MidCap 400 (“S&P MidCap 400”), (ii) The Weighted Average of Hubbell Class A and Class B common stock, and (ii) the Dow Jones U.S. Electrical Components & Equipment Index (“DJUSEC”). The Company is a member of the S&P MidCap 400. As of December 31, 2014,2016, the DJUSEC reflects a group of

fourteen company stocks in the electrical components and equipment market segment, and serves as the Company’s peer group for purposes of this graph. The comparison assumes $100 was invested on December 31, 20092011 in the Company’s Class B Common Stock and in each of the foregoing indices and assumes reinvestment of dividends.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Hubbell Incorporated, the S&P Midcap 400 Index,

and the Dow Jones US Electrical Components & Equipment Index

The Hubbell Incorporated line above uses the weighted average of Hubbell Class A and Class B shares for the three annual periods from December 2012 through December 2014.

|

|

*$100 invested on 12/31/0911 in stock or index, including reinvestment of dividends. Fiscal year ending December 31.

Copyright© 2015 S&P,2017 Standard & Poor's, a division of The McGraw-Hill Companies Inc.S&P Global. All rights reserved.

Copyright© 20152017 S&P Dow Jones & Co.Indices LLC, a division of S&P Global. All rights reserved.reserved

|

|

| |

| 16 | HUBBELL INCORPORATED- Form 10-K | 14 |

ITEM 6 Selected Financial Data

The following summary should be read in conjunction with the consolidated financial statements and notes contained herein (dollars and shares in millions, except per share amounts).

| | | OPERATIONS, years ended December 31, | 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

| | 2016 |

| 2015 |

| 2014 |

| 2013 |

| 2012 |

| |

| Net sales | $ | 3,359.4 |

| $ | 3,183.9 |

| $ | 3,044.4 |

| $ | 2,871.6 |

| $ | 2,541.2 |

| | $ | 3,505.2 |

| $ | 3,390.4 |

| $ | 3,359.4 |

| $ | 3,183.9 |

| $ | 3,044.4 |

| |

| Gross profit | $ | 1,109.0 |

| $ | 1,070.5 |

| $ | 1,012.2 |

| $ | 923.7 |

| $ | 828.7 |

| | $ | 1,100.7 |

| $ | 1,091.8 |

| $ | 1,109.0 |

| $ | 1,070.5 |

| $ | 1,012.2 |

| |

| Operating income | $ | 517.4 |

| $ | 507.6 |

| $ | 471.8 |

| $ | 423.8 |

| $ | 367.8 |

| | $ | 477.8 |

| $ | 474.6 |

| $ | 517.4 |

| $ | 507.6 |

| $ | 471.8 |

| |

Adjusted operating income (1) | | $ | 512.8 |

| $ | 513.5 |

| $ | 522.5 |

| $ | 507.6 |

| $ | 471.8 |

| |

| Operating income as a % of sales | 15.4 | % | 15.9 | % | 15.5 | % | 14.8 | % | 14.5 | % | | 13.6 | % | 14.0 | % | 15.4 | % | 15.9 | % | 15.5 | % | |

| Loss on extinguishment of debt | $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | (14.7 | ) | (1) | |

Adjusted operating income as a % of sales (1) | | 14.6 | % | 15.1 | % | 15.6 | % | 15.9 | % | 15.5 | % | |

| Net income attributable to Hubbell | $ | 325.3 |

| $ | 326.5 |

| $ | 299.7 |

| $ | 267.9 |

| $ | 217.2 |

| (1) | $ | 293.0 |

| $ | 277.3 |

| $ | 325.3 |

| $ | 326.5 |

| $ | 299.7 |

| |

| Net income attributable to Hubbell as a % of net sales | 9.7 | % | 10.3 | % | 9.8 | % | 9.3 | % | 8.5 | % | | 8.4 | % | 8.2 | % | 9.7 | % | 10.3 | % | 9.8 | % | |

| Net income attributable to Hubbell as a % of Hubbell shareholders’ average equity | 17.0 | % | 18.3 | % | 19.2 | % | 18.3 | % | 15.8 | % | | 17.6 | % | 15.1 | % | 17.0 | % | 18.3 | % | 19.2 | % | |

| Earnings per share — diluted | $ | 5.48 |

| $ | 5.47 |

| $ | 5.00 |

| $ | 4.42 |

| $ | 3.59 |

| (1) | $ | 5.24 |

| $ | 4.77 |

| $ | 5.48 |

| $ | 5.47 |

| $ | 5.00 |

| |

Adjusted earnings per share - diluted (1) | | $ | 5.66 |

| $ | 5.52 |

| $ | 5.54 |

| $ | 5.47 |

| $ | 5.00 |

| |

| Cash dividends declared per common share | $ | 2.06 |

| $ | 1.85 |

| $ | 1.68 |

| $ | 1.52 |

| $ | 1.44 |

| | $ | 2.59 |

| $ | 2.31 |

| $ | 2.06 |

| $ | 1.85 |

| $ | 1.68 |

| |

| Average number of common shares outstanding — diluted | 59.2 |

| 59.6 |

| 59.8 |

| 60.4 |

| 60.3 |

| | 55.7 |

| 58.0 |

| 59.2 |

| 59.6 |

| 59.8 |

| |

| Cost of acquisitions, net of cash acquired | $ | 183.8 |

| $ | 96.5 |

| $ | 90.7 |

| $ | 29.6 |

| $ | — |

| | $ | 173.4 |

| $ | 163.4 |

| $ | 183.8 |

| $ | 96.5 |

| $ | 90.7 |

| |

| FINANCIAL POSITION, AT YEAR-END | |

| |

| |

| |

| |

| | |

| |

| |

| |

| |

| |

| Working capital | $ | 1,130.3 |

| $ | 1,165.4 |

| $ | 1,008.9 |

| $ | 861.4 |

| $ | 781.1 |

| | |

Working capital (2) | | $ | 961.7 |

| $ | 784.7 |

| $ | 1,130.3 |

| $ | 1,165.4 |

| $ | 1,008.9 |

| |

| Total assets | $ | 3,322.8 |

| $ | 3,187.2 |

| $ | 2,947.0 |

| $ | 2,846.5 |

| $ | 2,705.8 |

| | $ | 3,525.0 |

| $ | 3,208.7 |

| $ | 3,320.1 |

| $ | 3,184.0 |

| $ | 2,943.3 |

| |

| Total debt | $ | 599.0 |

| $ | 597.5 |

| $ | 596.7 |

| $ | 599.2 |

| $ | 597.7 |

| | $ | 993.7 |

| $ | 644.1 |

| $ | 596.3 |

| $ | 594.3 |

| $ | 593.0 |

| |

| Total Hubbell shareholders’ equity | $ | 1,927.1 |

| $ | 1,906.4 |

| $ | 1,661.2 |

| $ | 1,467.8 |

| $ | 1,459.2 |

| | $ | 1,592.8 |

| $ | 1,740.6 |

| $ | 1,927.1 |

| $ | 1,906.4 |

| $ | 1,661.2 |

| |

| NUMBER OF EMPLOYEES, AT YEAR-END | 15,400 |

| 14,300 |

| 13,600 |

| 13,500 |

| 13,000 |

| | 17,400 |

| 16,200 |

| 15,400 |

| 14,300 |

| 13,600 |

| |

(1) The selected non-GAAP measures of adjusted operating income, adjusted operating income as a percent of sales (adjusted operating margin), and adjusted earnings per share-diluted should be read in conjunction with Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations".

(2) Defined as current assets less current liabilities.

|

| |

(1)HUBBELL INCORPORATED- Form 10-K | In 2010, the Company recorded a $14.7 million pre-tax charge ($9.1 million after-tax) related to its early extinguishment of debt. The earnings per diluted share impact of this charge was $0.15.17 |

ITEM 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations

Executive Overview of the Business

The Company is primarily engaged in the design, manufacture and sale of quality electrical and electronic products for a broad range of non-residential and residential construction, industrial and utility applications. Products are either sourced complete, manufactured or assembled by subsidiaries in the United States, Canada, Switzerland, Puerto Rico, China, Mexico, Italy, the United Kingdom, Brazil, Australia and Australia.Ireland. The Company also participates in joint ventures in Taiwan and Hong Kong, and maintains offices in Singapore, China, India, Mexico, South Korea and countries in the Middle East. The Company employs approximately 15,40017,400 individuals worldwide.

The Company made the following management changes in 2014 as part of its succession planning program.

In February 2014, the Company promoted Mr. Gerben W. Bakker to Group Vice President, Power Systems. Mr. William T. Tolley, the previous Group Vice President, Power Systems, has been named to the newly created position of Senior Vice President, Growth and Innovation.

On May 6, 2014, the Board of Directors appointed Mr. David G. Nord to the position of Chairman of the Board, in addition to his role as President and Chief Executive Officer. Mr. Nord succeeded Mr. Timothy H. Powers, the former Chairman of the Board, who retired from the Board in May 2014.

On June 30, 2014, Mr. Gary N. Amato was appointed to the position of Executive Vice President, Hubbell Electrical Segment. In this role, he acquired oversight of the Hubbell

|

| |

HUBBELL INCORPORATED- Form 10-K

| 15 |

Lighting business, in addition to his leadership role over the Electrical Systems businesses. Mr. Amato assumed responsibility for the Lighting business following the announcement of the retirement of Mr. Scott H. Muse.

The Company’s reporting segments consist of the Electrical segment and the Power segment. Results for 2014, 20132016, 2015 and 20122014 by segment are included under “Segment Results” within this Management’s Discussion and Analysis.

The Company's long-term strategy is to serve its customers with reliable and innovative solutions delivered through a competitive cost structure; to complement organic growth with acquisitions that enhance its product offerings; and to allocate capital effectively to create shareholder value. In executing this strategy the Company is focused on growing profits and delivering attractive returns to our shareholders by executing a business plan focused on the following key initiatives: growing revenue, growth, price realization,aligning the cost structure, improving productivity, improvements and deploying capital deployment.effectively.