PART I - FINANCIAL INFORMATION

FORWARD-LOOKING STATEMENTS

In addition to historical information, this Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the federal Securities Act and Section 21E of the Exchange Act, which are subject to the “safe harbor” created by those sections. All statements, other than statements of historical facts, included in this Annual Report on Form 10-K are forward-looking statements. You canForward-looking statements are generally identify forward-looking statementsidentified by our use of forward-looking terminology, such as “anticipate”, “believe”, “continue”, “could”, “estimate”, “expect”, “intend”, “may”, “might”, “plan”, “potential”, “predict”, “seek”,including the terms “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “potential,” “predict,” “seek,” or “should”, or the“should,” and, in each case, their negative thereof or other variations thereonvarious orcomparable terminology. In particular, statements about the markets in which we operate, including growth of our various markets, and our expectations, beliefs, plans, strategies, objectives, prospects, assumptions, or future events or performance contained under the headings Item 1A- Risk Factors, Item 7- 7 - Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Item 1- 1 - Business are forward-looking statements. In addition, statements regarding the potential outcome and impact of pending litigation are forward-looking statements.

We have based these forward-looking statements on our current expectations, assumptions, estimates, and projections. While we believe these expectations, assumptions, estimates, and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our control. These and other important factors, including those discussed under the headings Item 1A- 1A - Risk Factors, Item 7- Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Item 1- Business, in this Form 10-K may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements. Some of the factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements include:

•negative trends in overall business, financial market and economic conditions, and/or activity levels in our end markets;

•our highly competitive business environment;

increases in interest rates and reduced availability of financing for the purchase of new homes and home construction and improvements;

•our highly competitive business environment;

•failure to timely identify or effectively respond to consumer needs, expectations, or trends;

•failure to successfully implement our strategic initiatives, including our productivity, cost reduction and global footprint rationalization initiatives;

•disruptions in our operations due to natural disasters, public health issues, such as COVID-19, and armed conflicts, including the ongoing conflict between Russia and Ukraine and instabilities in the Middle East;

•economic and geopolitical uncertainty and risks that arise from operating a multinational business;

•acquisitions, divestitures, or investments in other businesses that may not be successful;

•adverse outcome of pending or future litigation;

•declines in our relationships with and/or consolidation of our key customers;

•fluctuations in the prices of raw materials used to manufacture our products;

•delays or interruptions in the delivery of raw materials or finished goods;

•failure to retain and recruit executives, managers, and employees;

•seasonal business andwith varying revenue and profit;

•changes in weather patterns;patterns and related extreme weather conditions;

•political, economic, and other risks that arise from operating a multinational business;

•disruptions in our operations;

•our new Enterprise Resource Planning system that we anticipate implementing in the future proving ineffective;

•increases in labor costs, potential labor disputes, and work stoppages at our facilities;

•changes in building codes that could increase the cost of our products or lower the demand for our windows and doors;

•compliance costs and liabilities under environmental, health, and safety laws and regulations;

7

•lack of transparency, threat of fraud, public sector corruption, and other forms of criminal activity involving government officials;

•product liability claims, product recalls, or warranty claims;

•inability to protect our intellectual property;

•loss of key officers or employees;

•availability and cost of credit;

•our current level of indebtedness;indebtedness and the effect of restrictive covenants under our existing or future indebtedness including our Credit Facilities, Senior Secured Notes, and Senior Notes; and

•risks associated with the material weaknesses that have been identified;

Given these risks and uncertainties, you are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements contained in this Form 10-K are not guarantees of future performance and our actual results of operations, financial condition, and liquidity, and the development of the industry in which we operate, may differ materially from the forward-looking statements contained in herein. In addition, even if our results of operations, financial condition, and liquidity, and events in the industry in which we operate, are consistent with the forward-looking statements contained in this Form 10-K, they may not be predictive of results or developments in future periods.

Any forward-looking statement in this Form 10-K speaks only as of the date of this Form 10-K or as of the date such statement was made.10-K. We do not undertake any obligation to update or revise, or to publicly announce any update or revision to, any of the forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

8

Item 1 - Business.

Our Company

We are onea leading global designer, manufacturer, and distributor of the world’s largest door and window manufacturers. We design, produce, and distribute an extensive range ofhigh-performance interior and exterior doors, wood, vinyl, and aluminum windows, and related building products, for use inserving the new construction and R&R sectors.

The JELD-WEN family of residential homesbrands includes JELD-WEN worldwide; LaCantina and to a lesser extent, non-residential buildings.

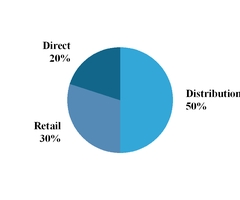

| Channel | Geography | Construction Application(1) | ||||||||||||

(1)Percentage of net revenues by construction application is management’s estimate based on the end markets into which our customers sell.

As onea leading global manufacturer of the largest doorinterior and window companies in the world,exterior building products, we have invested significant capital to build a business platform that we believe is unique among our competitors. We operate 12384 manufacturing and distribution facilities in 1915 countries located primarily in North America Europe, and Australia. OurEurope. We are focused on optimizing our global manufacturing footprint is strategically sizedto enhance performance and located to meetimprove profit margins. On July 2, 2023, we completed the delivery requirementssale of our customers. Australasia business (“JW Australia”). The net assets and operations of the disposal group met the criteria to be classified as “discontinued operations” and are reported as such in all periods. Unless otherwise indicated, the description of our business provided in Part I pertains to continuing operations only (seeNote 1 - Description of Company and Summary of Significant Accounting Policies and Note 2 - Discontinued Operationsto our consolidated financial statements for further information).

For many product lines, our manufacturing processes are vertically integrated, enhancing our range of capabilities, our ability to innovate, and our quality control, as well as providing us with supply chain, transportation, and working capital savings. We believe that our manufacturing network allows us to deliver our broad portfolio of products to a wide range of customers across the globe, improveswhile improving our customer service and strengthensstrengthening our market positions.

Our History

We were founded in 1960 by Richard L. Wendt, when he, together with four business partners, bought a millwork plant in Oregon. The subsequent decades were a time of successful expansion and growth as we added different businesses and product categories such as interior doors, exterior steel doors, and vinyl windows. Our first overseas acquisition was Norma Doors in Spain in 1992 and since then we have acquired or established numerous businesses in Europe, Australia, Asia, Canada, and Mexico, and Chile, making usJELD-WEN a truly global company.

In October 2011, certain funds managed by affiliates of Onex acquired a majority of JELD-WEN’sthe combined voting interests. power in the Company through the acquisition of convertible debt and convertible preferred equity. After the Onex investment, we began the transformation of our business from a family-run operation to a global organization with independent, professional management. The transformation accelerated after 2013 with the hiring of a new senior management team strategically recruited from a number of world-class industrial companies. Our newcurrent management team has decades ofextensive experience driving operational improvement, innovation, and growth, both organically and through acquisitions. As of December 31, 2020, Onex owned approximately 32.6% of our outstanding shares of Common Stock. In 2021, Onex exercised its rights under its Registration Rights Agreement and requested

9

Directors.

Our Business Strategy and Operating Model

We seekstrive to achieve best-in-industry financial performance and shareholder returns through the disciplined execution of:of our strategy which includes:

•enhancing performance and improving profit margins through strategic cost-reduction and productivity initiatives, such as the JEM,upgrading go-to-market processes, optimizing our sales force through training, right-sizing and consolidating our manufacturing network, investing in automation and leveraging our scale to improve our profit marginsstreamline sourcing;

•disciplined capital allocation and freeworking capital management designed to maximize shareholder returns, cash flow;flows, and return on invested capital in a balanced manner;

•investing in our brands and marketing, channel management, and pricingcommercial excellence programs such as customer segmentation, and price optimization; and

Our Products

We provide a broad portfolio of interior and exterior doors, windows, and related building products manufactured from a variety of wood, metal, and composite materials and offered across a full spectrum of price points. In the year ended December 31, 2017,2023, our door sales accounted for 67%63% of net revenues, our window sales accounted for 24%21% of net revenues, and our other ancillary products and services accounted for 9%16% of net revenues.

Doors

We are a leading global manufacturer of residential doors. We offer a full line of residential interior and exterior door products, including patio doors and folding or sliding wall systems. Our non-residential door product offering is concentrated in Europe, where we are a leading non-residential door provider by net revenues in Germany, Austria, Switzerland, and Scandinavia. In order toWe also offer non-residential doors across North America in certain markets. To meet the style, design, durability, and durability needsenergy efficiency requirements of our customers, across a broad range of price points, our product portfolio encompasses many types of materials, including wood veneer, composite wood, steel, glass, and fiberglass. Our interior and exterior residential door models generally retail at prices rangingfiberglass that satisfy a range of price points from $30entry-level to $40 for our most basic products to several thousand dollars for our high-end exterior doors.high-end. Our highest volume products include molded interior doors, which are made from two composite molded door skins joined by a wooden frame and filled with a hollow honey-cell core or other solid core materials. These low-costvalue doors are the most popular choice for interior residential applications in North America, and also are prevalent in France and the U.K. In the U.S., we manufacture exterior doors primarily made from fiberglass and steel. Our fiberglass product line has grown in popularity due to its attractive thermal properties, aesthetics, and durability. We have dedicated additional resources to our exterior fiberglass door business, which includes door slabs and door systems, and believe we have a leading product offering based on quality, breadth of design options, and range of price points. We also manufacturer stile and rail doors in our U.S. manufacturing facilities. In Europe, we also sell highly engineeredhigh performance residential and non-residential doors, with features such as soundproofing, fire resistance, radiation resistance, security, and added security. We alsoin Scandinavia we design and manufacture stiledoors which can withstand extreme environmental conditions in coastal and rail doors in our Southeast Asia manufacturing facilities, as well as in the U.S. through our 2015 acquisition of Karona. In the U.S., our 2015 acquisition of LaCantina added a line of folding and sliding wall systems to our product offerings.arctic environments. Additionally, we offer profitable value-added distribution services for residential and non-residential products in all of our markets, including customizable configuration services, specialized component options, and multiple finishing options. These services are valued by labor constrained customers and allow us to capture more profit from the sale of our door products. In the U.S., our recent acquisitionacquisitions of ABS and MMI Door is an exampleare examples of our increased focus on value-added services. Our newest door product offering includes steel doors, steel door frames, and fire doors for commercial and residential markets through our recent acquisition of Domoferm, which closed in February 2018.

Windows

We are a leading global manufacturer of residential windows.windows in North America. We manufacture a full line of residential wood, vinyl, and aluminumwood composite windows in North America, wood and aluminum windows in Australia, and wood windows in the U.K.America. Our window product lines comprise a full range of styles, features, and energy-saving options in order to meet the varied needs of our customers in each of our regional end markets. For example, our high performancehigh-performance wood and vinyl windows with multi-pane glazing and superior energy efficiency properties are in greater demand in Canada and the northern U.S. By contrast,In addition, our lower-cost aluminum framedvalue windows are popular in somewith production builders and the remodel and replacement markets. In select coastal regions, of the southern U.S., while in coastal Florida certain local building codes requirewe offer impact windows that can withstand the impact of debris propelled by hurricane-force winds. Woodhurricane force winds and satisfy local building codes. Our wood windows areremain prevalent as a high-end option in all of our markets because they possess both insulating qualities and the beauty of natural wood. In North America, our wood windows and patio doors include our proprietary AuraLast treatment, which is a unique water-based wood protection process that provides protection against wood rot and decay. We believe AuraLast is unique in its

10

ability to penetrate and protect the wood through to the core, as opposed to being a shallow or surface-only treatment. Our newest window product offerings include sashless window systems through our 2015With the acquisition of AneetaLaCantina Doors, the Company added LaCantina’s innovative folding, multi-slide, and louver windowswing patio doors and wall systems through our 2016to its already robust windows product offering. We also offer a non-residential line of vinyl windows for a broad assortment of commercial applications. With the acquisition of Breezway. OurVPI, we added vinyl windows typically retail at prices ranging from $100for mid-rise, multi-family, institutional, hospitality, and commercial properties to $200 for a basic vinyl window to over $1,000 for a custom energy-efficient wood window.our product lineup. We believe that our innovative energy-efficient windows position us to benefit from increasing environmental awareness among consumers and from changes in local building codes. In recognition of our expansive energy-efficient product line, we have been an ENERGY STAR partner since 1998. We have received ENERGY STAR Canada’s Excellence Award in 2023 and have won 7 ENERGY STAR Canada Manufacturer of the Year Awards.

Other Ancillary Products and Services

In certain regions, we sell a variety of other products that are ancillary to our door and window offerings, which we do not classify as door or window sales. These products include shower enclosures and wardrobes, moldings, trim board, lumber, cutstock, glass, staircases, hardware and locks, cabinets, and window screens. Molded door skins sold to certain third-party manufacturers, as well as miscellaneous installation and other services, areWe also included in this category.

Our Segments

We operate within the global market for residential and non-residential doors and windows with sales spanning 81approximately 71 countries. While we operate globally, the markets for doors and windows are regionally distinct with suppliers manufacturing finished goods in proximity to their customers. Finished doors and windows are generally bulky, expensive to ship, and, in the case of windows, fragile. Designs and specifications of doors and windows also vary from country to country due to differing construction methods, building codes, certification requirements, and consumer preferences. Customers also demand short delivery times and can require special order customizations. We believe that we are well-positioned to meet the global demands of our customers due to our market leadership, strong brands, broad product line, and strategically located manufacturing and distribution facilities.

Our operations are managed and reported in threetwo reportable segments, organized and managed principally by geographic region. Our reportable segments are North America Europe and Australasia.Europe. We report all other business activities in Corporate and unallocated costs. Factors considered in determining the threetwo reportable segments include the nature of business activities, the management structure accountable directly to the CODM for operating and administrative activities, the discrete financial information available, and the information regularly presented toreviewed by the CODM.

North America

In our North America segment, we compete primarily in the new construction and R&R market for residential doors and windows in the U.S. and Canada. We are the only manufacturer that offers a full line of interior and exterior door and window products, allowing us to offer a more complete solution to our customer base. We believe thatWhile we expect to realize some benefit from share gains and continued growth from pricing strategies to offset inflation, our leading position in the North American market will enable usis expected to benefit fromcontinue to face headwinds during 2024 primarily due to heightened interest rates and continued recovery in residential construction activity over the next several years.labor inflation. We believe that our total market opportunity in North America also includeswill continue to include non-residential applications and other related building products, and value-added services.products.

Europe

The European market for doors is highly fragmented, and we have the only platform in the industry capable of serving nearly all European countries. In our Europe segment, we compete primarily in the market for residential and non-residential doors in Germany, the U.K., France, Austria, Switzerland, and Scandinavia. We believeDuring 2024, we expect headwinds in our residential and non-residential markets due to general economic weakness and as interest rates that our total market opportunity in Europe also includes other European countries, other door product lines, related building products, and value-added services. Although

Financial information regarding our segments is included in Note 1914 - Segment Information to our financial statements included in this Form 10-K.

Materials

We generally maintain a diversified supply base for the materials used in our manufacturing operations. Materials represented approximately 50% of our cost of sales in the year ended December 31, 2017. The primary materials used for our door business include wood, wood veneers, wood composites, steel, glass, internally produced door skins, fiberglass compound, and hardware, as well as petroleum-based products such as resin and binders. The primary materials for our window business include wood, wood components, glass, and hardware, as well as aluminum extrusions, and vinyl extrusions. Wood components for our window operations are sourced primarily from our own manufacturing plants, which allow us to improve margins and take advantage of our proprietary technologies such as our AuraLast wood treatment process.

11

We track commodities in order to understand our vendors’ costs, realizing that our costs are determined by the broader competitive market as well as by increases in the inputs to our vendors. In order to manage the risk in material costs, we develop strategic relationships with suppliers, routinely evaluate substitute components, develop new products, vertically integrate, where applicable, and seek alternative sources of supply from multiple vendors and often from multiple geographies.

Seasonality

In a typical year, our operating results are impacted by seasonality. Historically, peak season for home construction and remodeling in our North America and Europe segments, which represent the substantial majority of our revenues, generally corresponds with the second and third calendar quarters, and therefore our sales volume is usually higher during those quarters. Seasonal variations in operating results may be impacted by inclement weather conditions, such as cold or wet weather, which can delay construction projects.

Sales and Marketing

We actively market and sell our products directly to our customers around the world through our global sales force and indirectly through our marketing and branding initiatives.initiatives, which includes our enhanced social media presence. Our global sales force, which is organized and managed regionally, focuses on building and maintaining relationships with key customers as well as managing customer supply needs and arranging in-store promotional initiatives. In North America and Europe, we also have a dedicated teamteams that focusesfocus on our large home centerretail customers.

We have recently made significantcontinue to make investments in tools and technologies to enhance the effectiveness of our sales force and improve ease of doing business.our customers’ purchasing experience. For example, we are continuing to invest and utilize Salesforce in the process of deploying Salesforce.com on a global basis, which will provide us with a common globalNorth America and Europe to enhance our customer relationshiprelationships and support. We continue to leverage Salesforce for improved data management, platform. In addition, we are in the process of simplifying our order entry process by implementing online configuration tools. We have introduced an electronic ordering system for easy order placement,service level tracking, Ecommerce, and we intend to expand our online retail sales. Our new strategy also includes initiatives focused on expanding our market through the use of social media. To date, these initiatives have included hosting videos and increasing our presence on Facebook.

We believe that our broad product portfolio of both doors and windows in North America and Australasia is a competitive advantage as it allows us to cross-sell our door and window products to our end customers, many of whom find it more efficient to choose one supplier for their door and window needs on a given project. None of our primary competitors in these regions offers a similarly complete range of windows as well as interior and exterior doors.

Research and Development

Although product specifications and certifications vary from country to country, the global nature of our operations allows us to leverage our global innovation capabilities and create product platforms which enable us to share new product designs across our markets. We believe that the global nature of our research and development capabilities is unique among our door and window competition. An example of global sharing of innovation is the “soft close” door system, which is based on hardware originally designed and manufactured by our European operations that is now being offered in North America and Australia. Additionally, we have successfully launched new door designs into our North American and Australian markets that were originally developed in our European operations.

Customers

We sell our products worldwide and have well-established relationships with numerous customers throughout the door and window distribution chain in each of our end markets, including retail home centers, wholesale distributors, and building product dealers that supply homebuilders, contractors, and consumers. Our wholesale customers include such industry leaders as BMC/Stock Building Supply, ProBuild/Builders First Source, American Building Supply, Saint-Gobain, and the Holzring group. Our home center customers include, among others, The Home Depot, Lowes,Lowe’s Companies, and Menards in North America; and B&Q, Howdens, and Bauhaus in Europe; and Bunnings Warehouse in Australia.Europe. We have maintained relationships with the majority of our top ten customers for over 1925 years and believe that the strength and tenure of our customer relationships is based on the total value we provide, including the quality and breadth of our ability to produceproduct offering, our customer service, innovation, and deliver high-quality products quickly and in the desired volumes for a reasonable cost.delivery capabilities. Our top ten customers together accounted for approximately 36%43%, 44% and 43% of our net revenues in the yearyears ended December 31, 2017,2023, 2022 and our largest customer,2021, respectively. The Home Depot, accounted for approximatelya customer of our North America segment, represents 15%, 16%, and 17% of our consolidated net revenues induring the yearyears ended December 31, 2017.2023, 2022, 2021, respectively. Lowe’s Companies, another customer of our North America segment, represents 11%, 11%, and 10% of our consolidated net revenues during the years ended December 31, 2023, 2022, 2021, respectively.

12

Competition

The door and window industry is highly competitive and includes a number of regional and international competitors. Competition is largely based on the functional and aesthetic quality of products, service quality, distribution capability, and price. We believe that we are well-positioned in our industry due to our leading brands, our broad product lines, our consistently high product quality and service, our global manufacturing and distribution capabilities, and our extensive multi-channel distribution. For North American interior doors, our major competitors include Masonite, Steves & Sons, Inc. and several smaller independent door manufacturers. For North American exterior doors, competitors include Masonite, Therma-Tru (a division of Fortune Brands), Plastpro and Plastpro.Steves & Sons, Inc. The North American window market is highly fragmented, with sizable competitors including Anderson,Andersen, Pella, Marvin, Ply-Gem (a division of Cornerstone Building Brands, formerly NCI Building Systems), and Milgard (a division of Masco)MI Windows and Doors). The door manufacturers that we primarily compete with in our European markets include Huga, Prüm/Garant (a division of Arbonia Group), Viljandi, Masonite, Keyor, Herholz, and Herholz. The competitive landscape in Australia is varied across the door and window markets. In the Australian door market, Hume Doors is our primary competitor, while in the window, shower screen, and wardrobe markets we largely compete against a fragmented set of smaller companies.Hormann.

Intellectual Property

We rely primarily on patent, trademark, copyright, and trade secret laws and contractual commitments to protect our intellectual property and other proprietary rights. Generally, registered trademarks have a perpetual life, provided that they are renewed on a timely basis and continue to be used properly as trademarks. We intend to maintain the trademark registrations listed below so long as they remain valuable to our business.

Our U.S. window and door trademarks include JELD-WEN®, AuraLast®, MiraTEC®, Extira®, LaCANTINA Karona, ImpactGard, JW, Aurora,®, MMI Door®, KaronaTM, ImpactGard®, JW®, Aurora®, IWP®, True BLU®, ABSTM, Siteline®, National Door®, Low-Friction Glider®, Hydrolock®, VPITM, AURALINE®, FINISHIELD®, MILLENNIUM®,TRUFIT®, EPICVUE®, and IWP.EVELIN®. Our trademarks are either registered or have long been used as a common law trademarktrademarks by the

Environmental, Social, and Swedoor, Dooria, DANA, MattioviGovernance Matters

Human Capital Management

We believe that the success of our mission is realized by the engagement and Alupanempowerment of our employees and we are committed to investing in Europe.

As of December 31, 2017,2023, we employed approximately 21,00017,700 people. Of our total number of employees, approximately 10,90011,000 are employed in operations included in our North America segment and corporate operations, and approximately 6,0006,700 are employed in operations included in our Europe segment, and approximately 4,100 are employed in operations included in our Australasia segment.

In total, approximately 1,020,1,200, or 10%11%, of our employees in the U.S. and Canada are unionized. Two facilities in the U.S., representing approximately 420350 employees, are covered by collective bargaining agreements. In Canada, approximately 47%68% of our employees work at facilities covered by collective bargaining agreements. As is common in Europe, and Australia, the majority of our facilities are covered by work councils and/or labor agreements. We believe we have satisfactory relationships with our employees and our organized labor unions.

13

Diversity, Equity, and Inclusion (DE&I)

We believe that a diverse and engaged workforce is a strong competitive advantage and we strive to create an environment where individuals of the environment. Many of our productsall backgrounds can fully contribute and maximize their potential. Our employees are also subjectencouraged to various laws and regulations such as building and construction codes, product safety regulations, and regulations and mandates related to energy efficiency.

TrainingandTalentDevelopment

We strive to not only attract and retain great talent but are committed to the continued development of our workforce. We invest in formal leadership development programs that help prepare senior leaders for succession into executive roles, in regional programs to accelerate the leadership conversion of mid-level managers, and in focused efforts to upskill our front-line leaders. Retaining and developing early career talent is an additional focus. Across our teams, we welcome apprenticeship and work study arrangements that seed talent into manufacturing and team lead roles. In North America specifically, we offer a summer internship program and a multi-year, cross-functional rotational program to identify, attract, and accelerate the growth of an internal pipeline of future managers. In our regions, we seek out, seed, and utilize financial grants and social educational investment requirements to reinvest in the ongoing learning and development needs of our diverse global workforce.

Internal job opportunities are posted for employees to review and our internal mobility philosophy encourages employees to apply for roles after they have passed twelve months on a job. As part of the annual performance management process, managers and employees meet to review goals and performance and discuss actions for ongoing growth and development. The Company continues to invest in its employees through new global learning platforms, content libraries, and additional formal and informal training programs.

Organizational Health

We manage and measure our organizational health with a view to gaining insight into our employees’ experiences, levels of workplace satisfaction, and safety lawsfeelings of engagement within the Company. Organizational health is driven through an “enterprise-guided” approach that includes both global and regulations, Item 1A - Risk Factors - Risks Relatinglocal initiatives in line with the Company’s overall cultural vision and strategy. We measure organizational health annually through our global employee survey and strive to Our Businesscontinually develop our culture and Industry, Item 1A - Risk Factors -We may be subjectemployee engagement. Results of the annual survey are communicated as global themes across the Company, with managers sharing more detailed insights from their areas of the business directly with their teams. The senior leadership team demonstrates their commitment to significant compliance costs with respect to legislativeengagement through transparent communications in town halls and regulatory proposals to restrict emissions of GHGs, and Item 3 - Legal Proceedings - Environmental Regulatory Actions.leadership team meetings; they also carry cultural targets on their individual annual goal plans.

Environmental Sustainability

We strive to conduct our business in a manner that is environmentally sustainable and demonstrates environmental stewardship. Toward that end, we pursue processes that are designed to minimize waste, maximize efficient utilization of materials, and conserve resources, including using recycled and reused materials to produce portions of our products. We are taking steps to mitigate climate change by measuring and reducing our GHG emissions, implementing renewable energy solutions and pursuing efficiency projects. We offer a variety of products that contain pre-consumer recycled content, such as our vinyl windows, aluminum cladding, and window glass. In January 2023, we launched a new primer formula developed by our coatings division designed to decrease volatile organic compounds (“VOC”) emissions in coatings applied to interior door skins. Our U.S. produced pine wood windows and select patio doors and door frames are made from AuraLast® pine, which is a proprietary, water-based wood protection process that results in a decrease of VOCs released during production. In addition, we manufacture many products that meet local green building provisions and top nationally recognized environmental programs. We continue to evaluate and modify our manufacturing and other processes on an ongoing basis to further reduce our impact on the environment. We believe it is important for our employees to share our commitment and we strive to recruit, educate, and train our employees in these values on an ongoing basis throughout their careers with us.

Environmental Regulatory Actions

The geographic breadth of our facilities and the nature of our operations subject us to extensive environmental, health, and safety laws and regulations in jurisdictions throughout the world. Such laws and regulations relate to, among other things, air emissions, the treatment and discharge of wastewater, the discharge of hazardous materials into the environment, the handling, storage, use and disposal of solid, hazardous and other wastes, worker health and safety, or otherwise relate to health, safety, and protection of the environment. Many of our products are also subject to various laws and regulations, such as building and construction codes, product safety regulations, and regulations and mandates related to energy efficiency.

The nature of our operations, which involve the handling, storage, use, and disposal of hazardous wastes, exposes us to the risk of liability and claims associated with contamination at our current and former facilities or sites where we have disposed of or

14

arranged for the disposal of waste, or with the impact of our products on human health and safety and the environment. Laws and regulations with respect to the investigation and remediation of contaminated sites can impose joint and several liability for releases or threatened releases of hazardous materials upon statutorily defined parties, including us, regardless of fault or the lawfulness of the original activity or disposal. We have been subject to claims, including having been named as a potentially responsible party, in certain proceedings initiated pursuant to the Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) and similar state and foreign laws, regulations, and statutes, and may be named a potentially responsible party in other similar proceedings in the future. Unforeseen expenditures or liabilities may arise in connection with such matters.

We have also been the subject of certain environmental regulatory actions by the EPA and state regulatory agencies in the U.S. and foreign governmental authorities in jurisdictions in which we operate and are obligated to make certain expenditures in settlement of those actions. We do not expect expenditures for compliance with environmental laws and regulations to have a material adverse effect on our financial position or competitive position. However, the discovery of a presently unknown environmental condition, changes in environmental requirements or their enforcement, or other unanticipated events, may give rise to unforeseen expenditures and liabilities which could be material.

In 2007, we were identified by the WADOE as a PLP with respect to our former manufacturing site in Everett, Washington. In 2008, we entered into an Agreed Order with the WADOE to assess historic environmental contamination and remediation feasibility at our former manufacturing site in Everett, Washington.the site. As part of this agreement,the order, we also agreed to develop a CAP, arising from the feasibility assessment. We are currently workingIn December 2020, we submitted to the WADOE a draft feasibility assessment with an array of remedial alternatives, which we considered substantially complete. During 2021, several comment rounds were completed as well as the identification of the Port of Everett and W&W Everett Investment LLC as additional PLPs, with respect to this matter with each PLP being jointly and severally liable for the cleanup costs. The WADOE received the final feasibility assessment on December 31, 2021, containing various remedial alternatives with its preferred remedial alternatives totaling $23.4 million. Based on this study, we have determined our range of possible outcomes to be $11.8 million to $33.4 million. On March 1, 2022, we delivered a draft CAP consistent with the preferred alternatives which was approved by WADOE in August 2023. The existing Agreed Order of 2008 was also modified with WADOE in July 2023 to finalize our RI/FS, and, once final, we will developsupport the CAP. We estimate the remaining cost to complete our RI/FS and develop the CAP at $0.5 million, which we have fully accrued.

In 2015,December 2020, we entered into a COA with the PaDEP to remove a pile of wood fiber waste from our site in Towanda, Pennsylvania, which we acquired in connection with our acquisition of CMI in 2013,2012, by using it as fuel for a boiler at that site. The COA replaced a 19952018 Consent Decree between CMI’s predecessor Masonite, Inc.PaDEP and PaDEP.us. Under the COA, we are required to achieve certain periodic removal objectives and ultimately remove the entire pile by August 31, 2022. There are currently $11.02025. As of December 31, 2023 and December, 31, 2022 there was $1.4 million and $2.3 million, respectively in bonds posted in connection with these obligations. If we are unable to remove this pile by August 31, 2022,2025, then the bonds will be forfeited, and we may be subject to penalties by PaDEP. We currently anticipate meeting all applicable removal deadlines;deadlines; however, if our operations at this site decrease and we burn less fuel than currently anticipated, we may not be able to meet such deadlines.

For more information regarding the risks associated with environmental, health, and safety laws and regulations, see Item 1A - Risk Factors.

Government Regulation

As a public company with global operations, we are subject to the laws and regulations of the United States and multiple foreign jurisdictions. These regulations, which differ among jurisdictions, include those related to financial and other disclosures, accounting standards, corporate governance, intellectual property, tax, trade, antitrust, employment, privacy, and anti-corruption, in addition to the environmental laws and regulations described above.

For a more detailed description of the various laws and regulations that affect our business, see Item 1A - Risk Factors.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Exchange Act, are filed with the SEC. We are subject to the informational requirements of the Exchange Act and file or furnish reports, proxy statements and other information with the SEC. Such reports and other information filed by us with the SEC are available free of charge on our website at investors.jeld-wen.com when such reports are made available and on the SEC’s website. The public may read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SECwebsite at www.sec.gov. The contents of these websites are not incorporated into this filing. Further, our references to the URLs for these websites are intended to be inactive textual references only.

15

Executive Officers of the Registrant

Set forth below is certain information about our executive officers. Ages are as of February 20, 2024. There are no family relationships among the following executive officers.

Julie C. Albrecht,Executive Vice President and Chief Financial Officer. Ms. Albrecht, age 56, joined the Company as Executive Vice President and Chief Financial Officer in July 2022. Previously, Ms. Albrecht joined Sonoco Products Company in 2017 as Vice President, Treasurer / Assistant Chief Financial Officer before being named Vice President, Chief Financial Officer in which role she served until June 2022. Prior to Sonoco, Ms. Albrecht served as Vice President, Finance, Investor Relations and Treasurer for Esterline Technologies Corporation (acquired by TransDigm in 2019). She began her finance career at PricewaterhouseCoopers. Ms. Albrecht earned a bachelor’s degree in accounting from Wake Forest University.

Peggie Bolan, Vice President and General Manager, North America Building Products and Fiber. Ms. Bolan, age 52, joined the Company in October 2012 as Vice President and General Manager, North American Building Products and Fiber. She is a seasoned executive with experience in sales, marketing and operations. She earned a bachelor’s degree in English from Vanderbilt University.

William J. Christensen,Chief Executive Officer and Director. Mr. Christensen, age 51, joined the Company in April 2022 as Executive Vice President and President, Europe. In December 2022, he was appointed to his current role as Chief Executive Officer and Director of the Company. Prior to joining the Company, Mr. Christensen was Chief Executive Officer and Group Executive Board Chair of REHAU AG, a Swiss-based global manufacturer, from 2018 to 2021. Prior to his appointment as Chief Executive Officer in 2018, Mr. Christensen served as its Chief Marketing Officer. Prior to joining REHAU AG, Mr. Christensen was Chief Executive Officer of AFG Holding, a Swiss-based global building products manufacturer from 2014 to 2015. In addition, he spent ten years at Geberit International AG, a global plumbing manufacturer, in several executive roles including Group Executive Board Member and Head of International Sales, as well as President and Chief Executive Officer of The Chicago Faucets Company. He also served in various finance and business development roles at J.P. Morgan Securities and Rieter Automotive Systems. Mr. Christensen earned a bachelor’s degree in economics from Rollins College and an MBA from the University of Chicago’s Booth School of Business.

James S. Hayes,Executive Vice President, General Counsel and Corporate Secretary. Mr. Hayes, age 51, joined the Company in August 2018 as Vice President, Deputy General Counsel. In August 2022, he was promoted to Senior Vice President, Deputy General Counsel and Corporate Secretary. He was appointed to his current role in June 2023. Mr. Hayes leads the global legal team, providing legal advice and guidance to the Board of Directors and the senior leadership team. Mr. Hayes earned a bachelor’s degree in English and history from Emory University and a law degree from Villanova University School of Law.

Daniel Jacobs,Vice President and General Manager, North America Windows. Mr. Jacobs, age 38, joined the Company in September 2008 as a Sales Representative and was promoted to Sales Manager in 2010. He has held roles of increasing responsibility as a National Account Manager and Director of National Accounts from 2010 to 2016. In December 2016, Mr. Jacobs was promoted to Director of Product Management. He was promoted to Vice President and General Manager, Exterior Doors in June 2020 until May 2022 and was promoted to his current role in May 2022. Mr. Jacobs earned a bachelor’s degree in economics from Rollins College.

Michael Leon,Senior Vice President and Chief Accounting Officer. Mr. Leon, age 43, joined the Company as Senior Vice President and Chief Accounting Officer in March 2023. Prior to joining the Company, Mr. Leon was the Chief Accounting Officer and Corporate Controller at Sealed Air, a global provider of packaging solutions, from June 2018 to March 2023, where he was also the Assistant Corporate Controller from December 2014 to June 2018. Mr. Leon earned a master’s degree in accounting from the University of South Carolina.

Kevin C. Lilly, Executive Vice President, Global Transformation. Mr. Lilly, age 63, joined the Company as Senior Vice President and Chief Information Officer in February 2019 and was promoted to Executive Vice President and Chief Information Officer in July 2022. Mr. Lilly served as the Company’s Interim Chief Executive Officer from August 2022 until December 2022 when he was named Executive Vice President, Global Transformation. Mr. Lilly leads the Company’s enterprise transformation initiatives and has responsibility for the global information technology organization. Prior to joining the Company, he served as Vice President of IT at Trane Technologies (formerly Ingersoll Rand) from 2011 to 2019. Previously, he was VP and Chief Information Officer for AGCO Corporation and served in a number of IT and finance positions of increasing responsibility for global companies including KPMG, Xerox, Delphi Automotive, General Motors, and EDS. Mr. Lilly earned a bachelor’s degree in business administration from Houghton College and attended the executive graduate program at the Thunderbird School of Global Management.

Wendy Livingston,Executive Vice President, Chief Human Resources Officer. Ms. Livingston, age 50, joined the Company as Executive Vice President, Chief Human Resources Officer in June 2023. Prior to joining the Company, Ms. Livingston was the Chief People Officer for Spreetail, a multinational e-commerce company, from August 2022 to June 2023 and the Senior Vice President and Chief Human Resources Officer for Harsco Corporation (now Enviri Corporation), a global environmental services company, from August 2020 to August 2022. She held leadership roles of increasing responsibility at The Boeing Company, a global aerospace company, from 1996 to 2020, including interim Senior Vice President, Human Resources in 2020 and Vice President, Corporate Human Resources from 2017 to 2020. Ms. Livingston earned a bachelor’s degree in business administration from Peru State College,

16

a master’s degree in human resource management from Lindenwood University and is certified by the Society for Human Resource Management.

Matthew Meier,Executive Vice President, Chief Digital and Information Officer. Mr. Meier, age 51, joined the Company as Executive Vice President, Chief Digital and Information Officer in January 2024. Previously, he was Executive Vice President, Chief Digital and Data Officer at Driven Brands Holding, Inc., an automotive services company, from October 2021 to January 2024. Prior to joining Driven Brands, Mr. Meier was employed at Whirlpool Corporation, a manufacturer of home appliances, as the Vice President, Global Technology Value Streams from 2020 to 2021 and as Vice President, Chief Information Officer from 2016 to 2020. Mr. Meier earned a bachelor’s degree in industrial engineering from Purdue University, a master’s degree in information systems management from Carnegie Mellon University and an MBA from the Massachusetts Institute of Technology Sloan School of Management.

Daniel Valenti,Executive Vice President and General Manager, North America Doors & Distribution. Mr. Valenti, age 46, joined the Company as Executive Vice President and General Manager, North America Doors & Distribution in January 2024. Previously, Mr. Valenti was employed at Whirlpool Corporation, a manufacturer of home appliances, as the Senior Vice President and General Manager, KitchenAid Small Appliances from September 2018 to December 2023. Mr. Valenti earned a bachelor’s degree in business administration from the University of North Carolina at Chapel Hill.

Gustavo Vianna,Executive Vice President and President, Europe. Mr. Vianna, age 55, joined the Company as Executive Vice President and President, Europe in January 2024. Prior to joining the Company, Mr. Vianna was employed at Aliaxis Group SA, a global manufacturer of advanced fluid management solutions, as Chief Executive Officer, EMEA from November 2020 to September 2022 and as Chief Business Officer from September 2019 to November 2020. Previously, he was the Chief Executive Officer, Pipe Business for Saint-Gobain Europe du Nord, a manufacturer and distributor of construction materials, from September 2016 to February 2019. Mr. Vianna earned a bachelor’s degree in electrical engineering from Pontifical Catholic University and a master’s degree in business administration from Fundacão Getúlio Vargas.

17

Item 1A - Risk Factors

Investing in our common stockCommon Stock involves a high degree of risk. These risks include those described below and may include additional risks and uncertainties not presently known to us or that we currently deem immaterial. You should carefully consider the following factors, as well as other information contained or incorporated by reference in this Annual Report on Form 10-K, before deciding to invest in shares of our common stock. TheCommon Stock. Our business, financial condition, and results of operations could be materially adversely affected by any of these risks, and the trading price of our common stockCommon Stock could decline due to any of these risks, and you may lose all or part of your investment in our common stock.Common Stock.

Risks Relating to Our Business and Industry

Negative trends in overall business, financial market and economic conditions, and/orand activity levels in our end markets may reduce demand for our products, which could have a material adverse effect on our business, financial condition, and results of operations.

Negative trends in overall business, financial market, and economic conditions globally or in the regions where we operate may reduce demand for our doors and windows, which is tied to activity levels in the R&R and new residential and non-residential construction end markets. In particular, the following factors may have a direct impact on our business in the regions where our products are marketed and sold:

•the strength of the economy;

•employment rates, and consumer confidence, and spending rates;

•the availability and cost of credit;

•interest rate fluctuations (including mortgage and credit card interest rates) and the availability of financing for our customers and consumers;

•the amount and type of residential and non-residential construction;

•housing sales and home values;

•the age of existing home stock, home vacancy rates, and foreclosures;

•volatility in both debt and equity capital markets;

•increases in the cost of raw materials or any shortage in supplies or labor;labor, including as a result of tariffs or other trade restrictions;

•the effects of governmental regulation and initiatives to manage economic conditions;

•geographical shifts in population and other changes in demographics; and

•changes in weather patterns.patterns and extreme weather events.

While cyclicalitycyclicity in our new residential and non-residential construction end markets is moderated to a certain extent by R&R activity, much R&R spending is discretionary and can be deferred or postponed entirely when economic conditions are poor. We have experienced sales declines in all of our end markets during this recent economic downturn.downturns.

The ability of consumers to finance home construction and improvements is affected by the nearability of consumers to procure third-party financing and the interest rates available for home mortgages, credit card debt, home equity or long-term. Moreover, uncertain economic conditions continue in our Australasia segmentother lines of credit, and certain countries in our Europe segment.other sources of third-party financing. Negative business, financial market, and economic conditions, including rising inflation, interest rates and difficulty for consumers to procure financing, globally and within the industries or in the regions where we operatecompete in may materially and adversely affect demand for or costs to produce our products andwhich could have a material adverse effect on our business, financial condition, and results of operationsoperations.

A decline in our relationships with our key customers, the amount of products they purchase from us, or a decline in our key customers’ financial condition could be materially negatively impactedhave a material adverse effect on our business, financial condition, and results of operations.

Our business depends on our relationships with our key customers, which consist mainly of wholesale distributors and retail home centers. Our top ten customers together accounted for approximately 43%, 44% and 43% of our net revenues in the years ended

18

December 31, 2023, 2022 and 2021, respectively. The Home Depot, a customer of our North America segment, represents 15%, 16%, and 17% of our consolidated net revenues during the years ended December 31, 2023, 2022, and 2021, respectively. Lowe’s Companies, another customer of our North America segment, represents 11%, 11%, and 10% of our consolidated net revenues during the years ended December 31, 2023, 2022, and 2021, respectively. Although we have established and maintain significant long-term relationships with our key customers, we cannot assure you that all of these relationships will continue or will not diminish. We generally do not enter into long-term contracts with our customers and they generally do not have an obligation to purchase products from us. Accordingly, sales from customers that have accounted for a significant portion of our sales in past periods, individually or as a result.group, may not continue in future periods, or if continued, may not reach or exceed historical levels in any period. For example, certain of our large customers perform periodic line reviews to assess their product offering, which have in the past and may in the future lead to loss of business and pricing pressures. Some of our large customers may also experience economic difficulties or otherwise default on their obligations to us. Furthermore, our pricing optimization strategy, which requires maintaining pricing discipline in order to improve or maintain profit margins, has in the past and may in the future lead to the loss of certain customers, including key customers, who do not agree to our pricing terms. The loss of, or a diminution in our relationship with, any of our largest customers could lower our sales volumes and could have a material adverse effect on our business, financial condition, and results of operations.

We operate in a highly competitive business environment. Failure to compete effectively could cause us to lose market share and/or force us to reduce the prices we chargeand any decrease in demand for our products. This competitionproducts could have a material adverse effect on our business, financial condition, and results of operations.

We operate in a highly competitive business environment. Some of our competitors may have greater financial, marketing, and distribution resources and may develop stronger relationships with customers in the markets where we sell our products. Some of our competitors may be less leveraged than we are, providing them with more flexibility to invest in new facilities and processes and also making them better able to withstand adverse economic or industry conditions.

In addition, some of our competitors, regardless of their size or resources, may choose to compete in the marketplace by adopting more aggressive sales policies, including price cuts, or by devoting greater resources to the development, promotion, and sale of their products. This could result in our loss of customers and/or market share to these competitors, or being forcedwhich may cause us to reduce the prices at which we sell our products to remain competitive.

As a result of competitive bidding processes, we may have to provide pricing concessions to our significant customers in order for us to keep their business. Reduced pricing would result in lower product margins on sales to those customers. There is no guarantee that a reduction in prices would be offset by sufficient gains in market share and sales volume to those customers.

The loss of, or a reduction in orders from, any significant customers, or decreases in the prices of our products due to lower demand, could have a material adverse effect on our business, financial condition, and results of operations.

Failure to implement our strategic cost reduction and productivity initiatives could adversely impact our business, financial condition, and results of operations.

Our future financial performance depends in part on our management’s ability to successfully implement our strategic initiatives, including our productivity, cost reduction, and global footprint rationalization initiatives. We cannot guarantee the successful implementation of these initiatives and related strategies throughout the geographic regions in which we operate or that such implementation will improve our operating results. Any failure to successfully implement these initiatives and related strategies could adversely affect our business, financial condition, and results of operations, including increases in our severance and asset related charges. We may, in addition, decide to alter or discontinue certain aspects of our business strategy at any time.

A disruption in our operations due to natural disasters, unstable geopolitical conditions or armed conflicts could have a material adverse effect on our business, financial condition, and results of operations.

We operate facilities worldwide. We have facilities located in areas that are vulnerable to hurricanes, earthquakes, wildfires, and other natural disasters. In the event that a hurricane, earthquake, natural disaster, fire, pandemic, or other catastrophic event were to interrupt our operations for any extended period of time, it could delay shipment of merchandise to our customers, damage our reputation, or otherwise have a material adverse effect on our business, financial condition, and results of operations.

In addition, our operations may be interrupted by armed conflicts, terrorist attacks or other acts of violence or war. These attacks may directly impact our suppliers’ or customers’ physical facilities. Furthermore, these attacks may make travel and the transportation of our supplies and products more difficult and more expensive and ultimately have a material adverse effect on our business, financial condition, and results of operations. Political and economic instability in some regions of the world may also negatively impact the global economy and, therefore, our business. For instance, instabilities in the Middle East and the ongoing conflict between Russia and Ukraine, including sanctions imposed on Russia, has had and could continue to have an adverse impact on our business, such as shortages in materials and heightened inflation on materials, freight, and other variable costs, such as utilities. The consequences of any of these armed conflicts are unpredictable, and we may not be able to foresee events that could have an adverse effect on our business or your investment. More generally, any of these events could cause consumer confidence and spending

19

to decrease or result in increased volatility in the worldwide financial markets. They could also result in economic recessions. Any of these occurrences could have a material adverse effect on our business, financial condition, and results of operations.

We may not identify or effectively respond to consumer needs, expectations, or trends in a timely fashion, which could adversely affect our relationship with customers, our reputation, the demand for our brands, products, and services, and our market share.

Accordingly, the success of our business depends in part on our ability to maintain strong brands and identify and respond promptly to evolving trends in demographics, consumer preferences, and expectations and needs, while also managing inventory levels. It is difficult to successfully predict the products and services our customers will demand. Even if we are successful in anticipating consumer preferences, our ability to adequately react to and address those preferences will in part depend upon our continued ability to develop and introduce innovative, high-quality products and acquire or develop the intellectual

property necessary to develop new products or improve our existing products. There can be no assurance that the products we develop, even those to which we devote substantial resources, will be successful. While we continue to invest in innovation, brand building, and brand awareness, and intend to increase our investments in these areas in the future, these initiatives may not be successful. Failure to anticipate and successfully react to changing consumer preferences could have a material adverse effect on our business, financial condition, and results of operations.

In addition, our competitors could introduce new or improved products that would replace or reduce demand for our products or create new proprietary designs and/or changes in manufacturing technologies that may render our products obsolete or too expensive for efficient competition in the marketplace. Our failure to competitively respond to changing consumer and customer trends, demands, and preferences could cause us to lose market share, which could have a material adverse effect on our business, financial condition, and results of operations.

We continually review our manufacturing operations to maintainaddress market changes and to implement efficiencies presented by past acquisitions. Effects of periodic manufacturing integrations, realignments, and cost savings programs have in the performance, reliability, quality,past and service standards required bycould in the future result in a decrease in our customers,short-term earnings, cash flows, and operating efficiency until the expected results are achieved. Such programs may include the consolidation, integration, and upgrading of facilities, functions, systems, and procedures. Such programs involve substantial planning, often require capital investments, and may result in charges for fixed asset impairments or to timely deliver our products, could have a material adverse effect on our business, financial condition,obsolescence and results of operations.

Our business is seasonal, and revenue and profit can vary significantly throughout the year, which may adversely impact the timing of our cash flows and limit our liquidity at certain times of the year.

Our business is seasonal, and our net revenues and operating results can vary significantly from quarter to quarter based upon the timing of the building season in our markets. Our sales typically follow seasonal new construction and R&R industry patterns. The peak season for home construction and R&R activity in the majority of the geographies where we market and sell our products generally corresponds with the second and third calendar quarters, and therefore our sales volume is typically higher during those quarters. Our first and fourth quarter sales volumes are generally lower due to reduced R&R and new construction activity as a result of less favorable climate conditions in the majority of our geographic end markets. Failure to effectively manage our inventory in anticipation of or in response to seasonal fluctuations could negatively impact our liquidity profile during certain seasonal periods.

We may be unable to protect our intellectual property, and we may face claims of intellectual property infringement.

We rely on a combination of patent, copyright, trademark, and trade secret laws, as well as confidentiality agreements, nondisclosure agreements, and other contractual commitments, to protect our intellectual property rights. However, these measures may not be adequate or sufficient, and third parties may not always respect these legal protections even if they are aware of them. In addition, our competitors may develop similar technologies and know-how without violating our intellectual property rights. Furthermore, the laws of foreign countries may not protect our intellectual property rights to the same extent as the laws of the U.S. The failure to obtain worldwide patent and trademark protection may result in other companies copying and marketing products based on our technologies or under brand or trade names similar to ours outside the jurisdictions in which we are protected. This could

20

impede our growth in existing regions, create confusion among consumers, and result in a greater supply of similar products that could erode prices for our protected products.

Litigation may be necessary to protect our intellectual property rights. Intellectual property litigation can result in substantial costs, could distract our management, and could impinge upon other resources. Our failure to enforce and protect our intellectual property rights may cause us to lose brand recognition and result in a decrease in sales of our products.

Moreover, while we are not aware that any of our products or brands infringes upon the proprietary rights of others, third parties may make such claims in the future. From time to time, third parties may claim that we have infringed upon their intellectual property rights and we may receive notices from such third parties asserting such claims. Any such infringement claims are thoroughly investigated and, regardless of merit, could be time-consuming and result in costly litigation or damages, undermine the exclusivity and value of our brands, decrease sales, or require us to enter into royalty or licensing agreements that may not be on acceptable terms and that could have a material adverse effect on our business, financial condition, and results of operations.

Changes in weather patterns and related extreme weather events, including as a result of global climate change, could significantly affect our financial results or financial condition.

Weather patterns may affect our operating results and our ability to maintain our sales volume throughout the year. Because our customers depend on suitable weather to engage in construction projects, increased frequency or duration of extreme weather conditions could have a material adverse effect on our financial results or financial condition. For example, unseasonably cool weather or extraordinary amounts of rainfall may decrease construction activity, thereby decreasing our sales. Also, we cannot predict the effects that global climate change may have on our business. In addition to changes in weather patterns, it might, for example, reduce the demand for construction, destroy forests (increasing the cost and reducing the availability of wood products used in construction), and increase the cost and reduce the availability of raw materials and energy. New laws and regulations related to global climate change may also increase our expenses or reduce our sales.

We are exposed to political, economic, and other risks that arise from operating a multinational business.

We have operations in North America South America, Europe, Australia, and Asia.Europe. In the year ended December 31, 2017,2023, our North America segment accounted for approximately 57%73% of net revenues and our Europe segment accounted for approximately 28%27% of net revenues, and our Australasia segment accounted for approximately 15% of our net revenues. Further, certain of our businesses obtain raw materials and finished goods from foreign suppliers. Accordingly, our business is subject to political, economic, and other risks that are inherent in operating in numerous countries.

These risks include:

•the difficulty of enforcing agreements and collecting receivables through foreign legal systems;

•trade protection measures and import or export licensing requirements;

•the imposition of, or increases in, tariffs or other trade restrictions;

•required compliance with a variety of foreign laws and regulations, including the application of foreign labor regulations;

•tax rates in foreign countries and the imposition of withholding requirements on foreign earnings;

•difficulty in staffing and managing widespread operations;

•the imposition of, or increases in, currency exchange controls; and

•potential inflation and interest rate fluctuation in applicable non-U.S. economies; and

The success of our business depends in part on our ability to anticipate and effectively manage these and other risks. We cannot assure you that these and other factors will not have a material adverse effect on our international operations or ultimately on our global business, financial condition, and results of operations.

Certain of our customers may expand through consolidation and internal growth, which may increase their buying power. The notice given by the U.K.increased size of its intent to withdraw from the E.U.our customers could have a material adverse effect on our business, financial condition, and results of operations.

We are subject to the credit risk of our customers, suppliers, and other counterparties.

We are subject to the credit risk of our customers, because we provide credit to our customers in the normal course of business. Any failure by our customers to meet their obligations to us may have a material adverse effect on our business, financial

21

condition, and results of operations. In addition, we may incur increased expenses related to collections in the future if we find it necessary to take legal action to enforce the contractual obligations of a significant number of our customers.

Exchange rate fluctuations may impact our business, financial condition, and results of operations.

Our operations expose us to both transaction and translation exchange rate risks. In the year ended December 31, 2017, 49%2023, 34% of our net revenues came from sales outside of the U.S., and we anticipate that our operations outside of the U.S. will continue to represent a significant portion of our net revenues for the foreseeable future. In addition, the nature of our operations often requires that we incur expenses in currencies other than those in which we earn revenue. Because of the mismatch between revenues and expenses, we are exposed to significant currency exchange rate risk and we may not be successful in achieving balances in currencies throughout our operations. In addition, if the effective price of our products were to increase as a result of fluctuations in foreign currency exchange rates, demand for our products could decline, which could adversely affect our business, financial condition, and results of operations. Also, because our financial statements are presented in U.S. dollars, we must translate the financial statements of our foreign subsidiaries and affiliates into U.S. dollars at exchange rates in effect during or at the end of each reporting period, and increases or decreases in the value of the U.S. dollar against other major currencies will affect our reported financial results, including the amount of our outstanding indebtedness. Exchange rates had a positive impact of 1% on our consolidated net revenues in the year ended December 31, 2017 as compared to a 1% negative impact in the year ended December 31, 2016. We cannot assure you that fluctuations in foreign currency exchange rates, particularly the strengthening of the U.S. dollar against major currencies, such as the Euro, the Australian dollar, the Canadian dollar, the British pound, or the currencies of large developing countries, would not materially adversely affect our business, financial condition, and results of operations.

We may be the subject of product liability claims or product recalls and we may not accurately estimate costs related to warranty claims. Expenses associated with product liability claims and lawsuits and related negative publicity or warranty claims in excess of our reserves could have a material adverse effect on our business, financial condition, and results of operations.

Our products are used in a wide variety of residential, non-residential, and architectural applications. We face the risk of exposure to product liability or other claims, including class action lawsuits, in the event our products are alleged to be defective or have resulted in harm to others or to property. We may in the future incur liability if product liability lawsuits against us are successful. Moreover, any such lawsuits, whether or not successful, could result in adverse publicity to us, which could cause our sales to decline materially. In addition, it may be necessary for us to recall defective products, which would also result in adverse publicity, as well as resulting in costs connected to the recall and loss of sales. We maintain insurance coverage to protect us against product liability claims, but that coverage may not be adequate to cover all claims that may arise, or we may not be able to maintain adequate insurance coverage in the future at an acceptable cost. Any liability not covered by insurance could have a material adverse effect on our business, financial condition, and results of operations.

In addition, consistent with industry practice, we provide warranties on many of our products and we may experience costs associated with warranty claims if our products have defects in manufacture or design or they do not meet contractual specifications. We estimate our future warranty costs based on historical trends and product sales, but we may fail to accurately estimate those costs and thereby fail to establish adequate warranty reserves for them. If warranty claims exceed our estimates, it may have a material adverse effect on our business, financial condition, and results of operations.

We may make acquisitions, divestitures, or investments in other businesses, which may involve risks or may not be successful.

Generally, we may seek to acquire businesses that broaden our existing product lines and service offerings or expand our geographic reach. There can be no assurance that we will be able to identify suitable acquisition candidates or that our acquisitions or investments in other businesses will be successful. We may also seek to divest business that do not align with our goal to streamline and simplify our operations. These acquisitions or investments in other businesses may also involve risks, many of which may be unpredictable and beyond our control, and which may have a material adverse effect on our business, financial condition, and results of operations, including risks related to:

•the nature of the acquired company’s business;

•any acquired business not performing as well as anticipated;

•the potential loss of key employees of the acquired company;

•any damage to our reputation as a result of performance or customer satisfaction problems relating to an acquired business;