0001047862 ed:ElectricEnergyDerivativeMember 2019-06-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

|

| |

| ☒ | Quarterly Report Pursuant To Section 13 or 15(d) of the Securities Exchange Act of 1934 |

FOR THE QUARTERLY PERIOD ENDED June 30, 2019March 31, 2020

OR

|

| |

| ☐ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

|

| | | | | | | | | | |

Commission File Number | | Exact name of registrant as specified in its charter and principal executive office address and telephone number | | State of Incorporation | | I.R.S. Employer ID. Number |

| 1-14514 | | Consolidated Edison, Inc. | | New York | | 13-3965100 |

| | | 4 Irving Place, | New York, | New York | 10003 | | | | |

| | | (212) | 460-4600 | | | | | | |

| 1-1217 | | Consolidated Edison Company of New York, Inc. | | New York | | 13-5009340 |

| | | 4 Irving Place, | New York, | New York | 10003 | | | | |

| | | (212) | 460-4600 | | | | | | |

Securities Registered Pursuant to Section 12(b) of the Act:

|

| | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Consolidated Edison, Inc., | | ED | | New York Stock Exchange |

| Common Shares ($.10 par value) | | | | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

| | | |

| Consolidated Edison, Inc. (Con Edison) | Yes | ☒ | No ☐ |

| Consolidated Edison Company of New York, Inc. (CECONY) | Yes | ☒ | No ☐ |

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

|

| | | |

| Con Edison | Yes | ☒ | No ☐ |

| CECONY | Yes | ☒ | No ☐ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | | | |

| Con Edison |

| Large accelerated filer | ☒ | | Accelerated filer ☐

| | Non-accelerated filer | ☐ |

| Smaller reporting company | ☐ | Emerging growth company | ☐ | | |

| CECONY |

Large accelerated filer | ☐ | | Accelerated filer ☐ | | Non-accelerated filer | ☒ |

Smaller reporting company | ☐ | Emerging growth company | ☐ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

| | | | |

| Con Edison | Yes | ☐ | No | ☒ |

| CECONY | Yes | ☐ | No | ☒ |

As of July 31, 2019,April 30, 2020, Con Edison had outstanding 332,144,207334,102,042 Common Shares ($.10 par value). All of the outstanding common equity of CECONY is held by Con Edison.

Filing Format

This Quarterly Report on Form 10-Q is a combined report being filed separately by two different registrants: Consolidated Edison, Inc. (Con Edison) and Consolidated Edison Company of New York, Inc. (CECONY). CECONY is a wholly-owned subsidiary of Con Edison and, as such, the information in this report about CECONY also applies to Con Edison. As used in this report, the term the “Companies” refers to Con Edison and CECONY. However, CECONY makes no representation as to the information contained in this report relating to Con Edison or the subsidiaries of Con Edison other than itself.

Glossary of Terms

The following is a glossary of abbreviations or acronyms that are used in the Companies’ SEC reports:

|

| | |

| Con Edison Companies |

| Con Edison | | Consolidated Edison, Inc. |

| CECONY | | Consolidated Edison Company of New York, Inc. |

| Clean Energy Businesses | | Con Edison Clean Energy Businesses, Inc., together with its subsidiaries |

Con Edison Development | | Consolidated Edison Development, Inc. |

Con Edison Energy | | Consolidated Edison Energy, Inc. |

Con Edison Solutions | | Consolidated Edison Solutions, Inc. |

Con Edison Transmission | | Con Edison Transmission, Inc., together with its subsidiaries |

| CET Electric | | Consolidated Edison Transmission, LLC |

| CET Gas | | Con Edison Gas Pipeline and Storage, LLC |

| O&R | | Orange and Rockland Utilities, Inc. |

| RECO | | Rockland Electric Company |

| The Companies | | Con Edison and CECONY |

| The Utilities | | CECONY and O&R |

| |

| Regulatory Agencies, Government Agencies and Other Organizations |

| CPUC | | California Public Utilities Commission |

| EPA | | U.S. Environmental Protection Agency |

| FASB | | Financial Accounting Standards Board |

| FERC | | Federal Energy Regulatory Commission |

| IASB | | International Accounting Standards Board |

| IRS | | Internal Revenue Service |

| NERC | | North American Electric Reliability Corporation |

| NJBPU | | New Jersey Board of Public Utilities |

| NJDEP | | New Jersey Department of Environmental Protection |

| NYISO | | New York Independent System Operator |

| NYPA | | New York Power Authority |

| NYSDEC | | New York State Department of Environmental Conservation |

| NYSERDA | | New York State Energy Research and Development Authority |

| NYSPSC | | New York State Public Service Commission |

| NYSRC | | New York State Reliability Council, LLC |

| PHMSA | | U.S. Department of Transportation’s Pipeline and Hazardous Materials Safety Administration |

| PJM | | PJM Interconnection LLC |

| SEC | | U.S. Securities and Exchange Commission |

| | |

| Accounting | | |

| AFUDC | | Allowance for funds used during construction |

| ASU | | Accounting Standards Update |

| GAAP | | Generally Accepted Accounting Principles in the United States of America |

| HLBV | | Hypothetical liquidation at book value |

| OCI | | Other Comprehensive Income |

| VIE | | Variable Interest Entity |

|

| | |

| Environmental | | |

| CO2 | | Carbon dioxide |

| GHG | | Greenhouse gases |

| MGP Sites | | Manufactured gas plant sites |

| PCBs | | Polychlorinated biphenyls |

| PRP | | Potentially responsible party |

| RGGI | | Regional Greenhouse Gas Initiative |

| Superfund | | Federal Comprehensive Environmental Response, Compensation and Liability Act of 1980 and similar state statutes |

| | | |

| Units of Measure | | |

| AC | | Alternating current |

| Bcf | | Billion cubic feet |

| Dt | | Dekatherms |

| kV | | Kilovolt |

| kWh | | Kilowatt-hour |

| MDt | | Thousand dekatherms |

| MMlb | | Million pounds |

| MVA | | Megavolt ampere |

| MW | | Megawatt or thousand kilowatts |

| MWh | | Megawatt hour |

| | | |

| Other | | |

| AMI | | Advanced metering infrastructure |

| CARES Act | | Coronavirus Aid, Relief, and Economic Security Act, as enacted on March 27, 2020 |

| COSO | | Committee of Sponsoring Organizations of the Treadway Commission |

| COVID-19 | | Coronavirus Disease 2019 |

| DER | | Distributed energy resources |

| Fitch | | Fitch Ratings |

| First Quarter Form 10-Q | | The Companies' combined Quarterly Report on Form 10-Q for the quarterly period ended March 31 of the current year |

| Form 10-K | | The Companies’ combined Annual Report on Form 10-K for the year ended December 31, 20182019 |

| LTIP | | Long Term Incentive Plan |

| Moody’s | | Moody’s Investors Service |

| REV | | Reforming the Energy Vision |

| S&P | | S&P Global Ratings |

| TCJA | | The federal Tax Cuts and Jobs Act of 2017, as enacted on December 22, 2017 |

| VaR | | Value-at-Risk |

TABLE OF CONTENTS

|

| | |

| | PAGE |

| |

| ITEM 1 | Financial Statements (Unaudited) | |

| | Con Edison | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | CECONY | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| ITEM 2 | | |

| ITEM 3 | | |

| ITEM 4 | | |

| |

| ITEM 1 | | |

| ITEM 1A | | |

| ITEM 6 | | |

| | | |

FORWARD-LOOKING STATEMENTS

This report includes forward-looking statements intended to qualify for the safe-harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are statements of future expectation and not facts. Words such as “forecasts,” “expects,” “estimates,” “anticipates,” “intends,” “believes,” “plans,” “will” and similar expressions identify forward-looking statements. Forward-looking statements are based on information available at the time the statements are made, and accordingly speak only as of that time. Actual results or developments might differ materially from those included in the forward-looking statements because of various factors including, but not limited to:

the Companies are extensively regulated and are subject to penalties;

the Utilities’ rate plans may not provide a reasonable return;

the Companies may be adversely affected by changes to the Utilities’ rate plans;

the intentional misconduct of employees or contractors could adversely affect the Companies;

the failure of, or damage to, the Companies’ facilities could adversely affect the Companies;

a cyber attack could adversely affect the Companies;

the Companies are exposed to risks from the environmental consequences of their operations;operations, including increased costs related to climate change;

a disruption in the wholesale energy markets or failure by an energy supplier or customer could adversely affect the Companies;

the Companies have substantial unfunded pension and other postretirement benefit liabilities;

Con Edison’s ability to pay dividends or interest depends on dividends from its subsidiaries;

the Companies require access to capital markets to satisfy funding requirements;

changes to tax laws could adversely affect the Companies;

the Companies’ strategies may not be effective to address changes in the external business environment;

the Companies face risks related to health epidemics and other outbreaks, including the COVID-19 pandemic; and

the Companies also face other risks that are beyond their control.

The Companies assume no obligation to update forward-looking statements.

Consolidated Edison, Inc.

CONSOLIDATED INCOME STATEMENT (UNAUDITED)

| | | | For the Three Months Ended June 30, | For the Six Months Ended June 30, | For the Three Months Ended March 31, |

| (Millions of Dollars/Except Share Data) | 2019 | 2018 |

| 2019 | 2018 |

| 2020 | 2019 |

| OPERATING REVENUES | | | | | |

| Electric | $1,971 | $1,951 | $3,912 | $3,828 | $1,906 | $1,941 |

| Gas | 449 | 489 | 1,484 | 1,428 | 931 | 1,034 |

| Steam | 90 | 96 | 411 | 410 | 250 | 321 |

| Non-utility | 234 | 160 | 451 | 394 | 147 | 218 |

| TOTAL OPERATING REVENUES | 2,744 | 2,696 | 6,258 | 6,060 | 3,234 | 3,514 |

| OPERATING EXPENSES | | | | | |

| Purchased power | 352 | 388 | 719 | 742 | 308 | 368 |

| Fuel | 26 | 38 | 133 | 162 | 78 | 106 |

| Gas purchased for resale | 131 | 194 | 573 | 572 | 232 | 442 |

| Other operations and maintenance | 781 | 756 | 1,575 | 1,592 | 700 | 794 |

| Depreciation and amortization | 418 | 354 | 831 | 702 | 470 | 413 |

| Taxes, other than income taxes | 578 | 540 | 1,183 | 1,110 | 638 | 605 |

| TOTAL OPERATING EXPENSES | 2,286 | 2,270 | 5,014 | 4,880 | 2,426 | 2,728 |

| OPERATING INCOME | 458 | 426 | 1,244 | 1,180 | 808 | 786 |

| OTHER INCOME (DEDUCTIONS) | | | | | | |

| Investment income | 22 | 36 | 45 | 57 | 26 | 24 |

| Other income | 4 | 6 | 15 | 11 | 2 | 11 |

| Allowance for equity funds used during construction | 4 | 3 | 7 | 7 | 5 | 3 |

| Other deductions | (27) | (48) | (50) | (92) | (72) | (24) |

| TOTAL OTHER INCOME (DEDUCTIONS) | 3 | (3) | 17 | (17) | (39) | 14 |

| INCOME BEFORE INTEREST AND INCOME TAX EXPENSE | 461 | 423 | 1,261 | 1,163 | 769 | 800 |

| INTEREST EXPENSE | | | | | |

| Interest on long-term debt | 219 | 190 | 440 | 380 | 224 | 221 |

| Other interest | 47 | 9 | 77 | 16 | 101 | 29 |

| Allowance for borrowed funds used during construction | (3) | (2) | (7) | (5) | (3) |

| NET INTEREST EXPENSE | 263 | 197 | 510 | 391 | 322 | 247 |

| INCOME BEFORE INCOME TAX EXPENSE | 198 | 226 | 751 | 772 | 447 | 553 |

| INCOME TAX EXPENSE | 19 | 38 | 127 | 156 | 55 | 108 |

| NET INCOME | $179 | $188 | $624 | $616 | $392 | $445 |

| Income attributable to non-controlling interest | 27 | — |

| 48 | — |

| 17 | 21 |

| NET INCOME FOR COMMON STOCK | $152 | $188 | $576 | $616 | $375 | $424 |

| Net income per common share—basic | $0.46 | $0.60 | $1.77 | $1.98 | $1.13 | $1.31 |

| Net income per common share—diluted | $0.46 | $0.60 | $1.77 | $1.98 | $1.12 | $1.31 |

| AVERAGE NUMBER OF SHARES OUTSTANDING—BASIC (IN MILLIONS) | 328.3 | 310.8 | 325.2 | 310.6 | 333.6 | 322.5 |

| AVERAGE NUMBER OF SHARES OUTSTANDING—DILUTED (IN MILLIONS) | 329.2 | 311.9 | 326.1 | 311.7 | 334.6 | 323.4 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison, Inc.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME (UNAUDITED)

| | | | Three Months Ended June 30, | Six Months Ended June 30, | Three Months Ended March 31, |

| (Millions of Dollars) | 2019 | 2018 |

| 2019 | 2018 |

| 2020 | 2019 |

| NET INCOME | $179 | $188 | $624 | $616 | $392 | $445 |

| INCOME ATTRIBUTABLE TO NON-CONTROLLING INTEREST | (27) | — |

| (48) | — |

| (17) | (21) |

| OTHER COMPREHENSIVE INCOME, NET OF TAXES | | |

|

| |

| Pension and other postretirement benefit plan liability adjustments, net of taxes | 1 | 2 | 5 | 6 | 5 | 4 |

| TOTAL OTHER COMPREHENSIVE INCOME, NET OF TAXES | 1 | 2 | 5 | 6 | 5 | 4 |

| COMPREHENSIVE INCOME | $153 | $190 | $581 | $622 | $380 | $428 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison, Inc.

CONSOLIDATED STATEMENT OF CASH FLOWS (UNAUDITED)

| | | For the Six Months Ended June 30, | | For the Three Months Ended March 31, | |

| (Millions of Dollars) | 2019 | 2018 |

| 2020 |

| 2019 |

|

| OPERATING ACTIVITIES | | | |

| Net income | $624 | $616 | $392 | $445 |

| PRINCIPAL NON-CASH CHARGES/(CREDITS) TO INCOME | | | |

| Depreciation and amortization | 831 | 702 | 470 | 413 |

| Deferred income taxes | 126 | 155 | 60 | 108 |

| Rate case amortization and accruals | (59) | (56) | (11) | (29) |

| Common equity component of allowance for funds used during construction | (7) | (7) | (5) | (3) |

| Net derivative gains | 31 | 2 | |

| Net derivative losses | | 83 | 10 |

| Unbilled revenue and net unbilled revenue deferrals | (4) | 113 | 51 | 11 |

| Gain on sale of assets | (5) | — |

| — |

| (5) |

| Other non-cash items, net | (17) | (55 | ) | 45 | (4) |

| CHANGES IN ASSETS AND LIABILITIES | | | |

| Accounts receivable – customers | 165 | 5 | (87) | (43) |

| Materials and supplies, including fuel oil and gas in storage | 14 | 16 | 26 | 31 |

| Revenue decoupling mechanism | (127) | — |

| |

| Revenue decoupling mechanism receivable | | (32) | (55) |

| Other receivables and other current assets | 125 | (68) | 28 | 19 |

| Taxes receivable | $19 | 49 | (1) | — |

|

| Prepayments | (35) | (36) | (479) | (448) |

| Accounts payable | (156) | (61) | (156) | (108) |

| Pensions and retiree benefits obligations, net | 168 | 171 | 4 | 93 |

| Pensions and retiree benefits contributions | (78) | (368) | (4) |

| Accrued taxes | (15) | (63) | (45) | (19) |

| Accrued interest | 25 | (4) | 85 | 97 |

| Superfund and environmental remediation costs, net | (7) | (6) | (3) | (1) |

| Distributions from equity investments | 27 | 54 | 11 | 14 |

| System benefit charge | (1) | 94 | (19) | 6 |

| Deferred charges, noncurrent assets and other regulatory assets | (213) | (233) | (38) | (34) |

| Deferred credits and other regulatory liabilities | 162 | 244 | 116 | 94 |

| Other current and noncurrent liabilities | (55) | (224) | (79) | (124) |

| NET CASH FLOWS FROM OPERATING ACTIVITIES | 1,538 | 1,040 | 412 | 464 |

| INVESTING ACTIVITIES | | | |

| Utility construction expenditures | (1,613) | (1,602) | (767) | (783) |

| Cost of removal less salvage | (142) | (121) | (68) | (72) |

| Non-utility construction expenditures | (92) | (109) | (130) | (48) |

| Investments in electric and gas transmission projects | (88) | (51) | (8) | (38) |

| Proceeds from sale of assets | 48 | — |

| — |

| 48 |

| Other investing activities | 11 | 17 | 5 |

| NET CASH FLOWS USED IN INVESTING ACTIVITIES | (1,876) | (1,866) | (968) | (888) |

| FINANCING ACTIVITIES | | | |

| Net issuance/(payment) of short-term debt | (1,405) | 292 | |

| Net payment of short-term debt | | (484) | (1,131) |

| Issuance of long-term debt | 1,989 | 1,640 | 1,600 | 825 |

| Retirement of long-term debt | (657) | (619) | (38) | (11) |

| Debt issuance costs | (17) | (16) | (22) | (1) |

| Common stock dividends | (455) | (420) | (243) | (226) |

| Issuance of common shares - public offering | 825 | — |

| 88 | 425 |

| Issuance of common shares for stock plans | 27 | 26 | 14 | 13 |

| Distribution to noncontrolling interest | (5) | — |

| (2) |

| NET CASH FLOWS FROM FINANCING ACTIVITIES | 302 | 903 | |

| NET CASH FLOWS FROM (USED IN) FINANCING ACTIVITIES | | 913 | (108) |

| CASH, TEMPORARY CASH INVESTMENTS, AND RESTRICTED CASH: | | | |

| NET CHANGE FOR THE PERIOD | (36) | 77 | 357 | (532) |

| BALANCE AT BEGINNING OF PERIOD | 1,006 | 844 | 1,217 | 1,006 |

| BALANCE AT END OF PERIOD | $970 | $921 | $1,574 | $474 |

| SUPPLEMENTAL DISCLOSURE OF CASH INFORMATION | | | |

| Cash paid/(received) during the period for: | | | |

| Cash paid during the period for: | | |

| Interest | $422 | $389 | $143 | $130 |

| Income taxes | $(15) | $(2) | $2 | $3 |

| SUPPLEMENTAL DISCLOSURE OF NON-CASH INFORMATION | | | |

| Construction expenditures in accounts payable | $332 | $333 | $343 | $300 |

| Issuance of common shares for dividend reinvestment | $24 | $24 | $12 |

| Software licenses acquired but unpaid as of end of period | $80 | $94 | $80 | $100 |

| Equipment acquired but unpaid as of end of period | | $33 | — |

|

The accompanying notes are an integral part of these financial statements.

Consolidated Edison, Inc.

CONSOLIDATED BALANCE SHEET (UNAUDITED)

| | | (Millions of Dollars) | June 30,

2019 | December 31,

2018 |

| March 31,

2020 | December 31,

2019 |

| ASSETS | | | |

| CURRENT ASSETS | | | |

| Cash and temporary cash investments | $831 | $895 | $1,395 | $981 |

| Accounts receivable – customers, less allowance for uncollectible accounts of $65 and $62 in 2019 and 2018, respectively | 1,099 | 1,267 | |

| Other receivables, less allowance for uncollectible accounts of $4 and $5 in 2019 and 2018, respectively | 148 | 285 | |

| Accounts receivable – customers, less allowance for uncollectible accounts of $75 and $70 in 2020 and 2019, respectively | | 1,318 | 1,236 |

| Other receivables, less allowance for uncollectible accounts of $5 and $4 in 2020 and 2019, respectively | | 188 | 184 |

| Taxes receivable | 30 | 49 | 21 | 20 |

| Accrued unbilled revenue | 550 | 514 | 443 | 599 |

| Fuel oil, gas in storage, materials and supplies, at average cost | 344 | 358 | 326 | 352 |

| Prepayments | 222 | 187 | 739 | 260 |

| Regulatory assets | 97 | 76 | 143 | 128 |

| Restricted cash | 139 | 111 | 179 | 236 |

| Revenue decoupling mechanism receivable | 127 | — |

| |

| Revenue decoupling mechanism | | 108 | 76 |

| Other current assets | 120 | 122 | 166 | 200 |

| TOTAL CURRENT ASSETS | 3,707 | 3,864 | 5,026 | 4,272 |

| INVESTMENTS | 1,899 | 1,766 | 2,011 | 2,065 |

| UTILITY PLANT, AT ORIGINAL COST | | | |

| Electric | 31,245 | 30,378 | 32,186 | 31,866 |

| Gas | 9,614 | 9,100 | 10,300 | 10,107 |

| Steam | 2,580 | 2,562 | 2,625 | 2,601 |

| General | 3,428 | 3,331 | 3,606 | 3,562 |

| TOTAL | 46,867 | 45,371 | 48,717 | 48,136 |

| Less: Accumulated depreciation | 10,149 | 9,769 | 10,530 | 10,322 |

| Net | 36,718 | 35,602 | 38,187 | 37,814 |

| Construction work in progress | 1,898 | 1,978 | 2,005 | 1,937 |

| NET UTILITY PLANT | 38,616 | 37,580 | 40,192 | 39,751 |

| NON-UTILITY PLANT | | | |

| Non-utility property, less accumulated depreciation of $329 and $275 in 2019 and 2018, respectively | 3,961 | 4,000 | |

| Non-utility property, less accumulated depreciation of $423 and $391 in 2020 and 2019, respectively | | 3,797 | 3,829 |

| Construction work in progress | 168 | 169 | 446 | 309 |

| NET PLANT | 42,745 | 41,749 | 44,435 | 43,889 |

| OTHER NONCURRENT ASSETS | | | |

| Goodwill | 440 | 440 | 446 |

| Intangible assets, less accumulated amortization of $79 and $29 in 2019 and 2018, respectively | 1,605 | 1,654 | |

| Intangible assets, less accumulated amortization of $152 and $126 in 2020 and 2019, respectively | | 1,532 | 1,557 |

| Regulatory assets | 4,237 | 4,294 | 4,732 | 4,859 |

| Operating lease right-of-use asset | 842 | — |

| 848 | 857 |

| Other deferred charges and noncurrent assets | 127 | 153 | 129 | 134 |

| TOTAL OTHER NONCURRENT ASSETS | 7,251 | 6,541 | 7,687 | 7,853 |

| TOTAL ASSETS | $55,602 | $53,920 | $59,159 | $58,079 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison, Inc.

CONSOLIDATED BALANCE SHEET (UNAUDITED)

| | | (Millions of Dollars) | June 30,

2019 |

| December 31,

2018 |

| March 31,

2020 | December 31,

2019 |

| LIABILITIES AND SHAREHOLDERS’ EQUITY | | |

| CURRENT LIABILITIES | | |

| Long-term debt due within one year | $1,972 | $650 | $2,093 | $1,446 |

| Term loan | — |

| 825 | |

| Notes payable | 1,161 | 1,741 | 1,208 | 1,692 |

| Accounts payable | 994 | 1,187 | 1,015 | 1,164 |

| Customer deposits | 350 | 351 | 344 | 346 |

| Accrued taxes | 47 | 61 | 31 | 76 |

| Accrued interest | 154 | 129 | 238 | 153 |

| Accrued wages | 111 | 109 | 116 | 102 |

| Fair value of derivative liabilities | 68 | 50 | 153 | 123 |

| Regulatory liabilities | 104 | 114 | 123 | 102 |

| System benefit charge | 626 | 627 | 628 | 647 |

| Operating lease liabilities | 55 | — |

| 77 | 65 |

| Other current liabilities | 327 | 363 | 285 | 371 |

| TOTAL CURRENT LIABILITIES | 5,969 | 6,207 | 6,311 | 6,287 |

| NONCURRENT LIABILITIES | | |

| Provision for injuries and damages | 144 | 146 | 129 | 130 |

| Pensions and retiree benefits | 1,120 | 1,228 | 1,329 | 1,516 |

| Superfund and other environmental costs | 770 | 779 | 737 | 734 |

| Asset retirement obligations | 427 | 450 | 429 | 425 |

| Fair value of derivative liabilities | 130 | 16 | 228 | 105 |

| Deferred income taxes and unamortized investment tax credits | 6,011 | 5,820 | 6,348 | 6,227 |

| Operating lease liabilities | 821 | — |

| 799 | 809 |

| Regulatory liabilities | 4,604 | 4,641 | 4,689 | 4,827 |

| Other deferred credits and noncurrent liabilities | 245 | 299 | 270 | 279 |

| TOTAL NONCURRENT LIABILITIES | 14,272 | 13,379 | 14,958 | 15,052 |

| LONG-TERM DEBT | 17,496 | 17,495 | 19,423 | 18,527 |

| EQUITY | | |

| Common shareholders’ equity | 17,709 | 16,726 | 18,261 | 18,022 |

| Noncontrolling interest | 156 | 113 | 206 | 191 |

| TOTAL EQUITY (See Statement of Equity) | 17,865 | 16,839 | 18,467 | 18,213 |

| TOTAL LIABILITIES AND EQUITY | $55,602 | $53,920 | $59,159 | $58,079 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison, Inc.

CONSOLIDATED STATEMENT OF EQUITY (UNAUDITED)

|

| | | | | | | | | | |

| (In Millions, except for dividends per share) | Common Stock | Additional

Paid-In

Capital | Retained

Earnings | Treasury Stock | Capital

Stock

Expense | Accumulated

Other

Comprehensive

Income/(Loss) | Non- controlling

Interest | Total |

| Shares | Amount | Shares | Amount |

| BALANCE AS OF DECEMBER 31, 2018 | 321 | $34 | $7,117 | $10,728 | 23 | $(1,038) | $(99) | $(16) | $113 | $16,839 |

| Net income |

|

|

| 424 |

|

|

|

| 21 | 445 |

| Common stock dividends ($0.74 per share) |

|

|

| (237) |

|

|

|

|

| (237) |

| Issuance of common shares – public offering | 6 |

| 433 |

|

|

| (8) |

|

| 425 |

| Issuance of common shares for stock plans |

|

| 27 |

|

|

|

|

|

| 27 |

| Other comprehensive income |

|

|

|

|

|

|

| 4 |

| 4 |

| Distributions to noncontrolling interest |

|

|

|

|

|

|

|

| (2) | (2) |

| BALANCE AS OF MARCH 31, 2019 | 327 | $34 | $7,577 | $10,915 | 23 | $(1,038) | $(107) | $(12) | $132 | $17,501 |

| | | | | | | | | | | |

| BALANCE AS OF BALANCE AS OF DECEMBER 31, 2019 | 333 | $35 | $8,054 | $11,100 | 23 | $(1,038) | $(110) | $(19) | $191 | $18,213 |

| Net income |

|

|

| 375 |

|

|

|

| 17 | 392 |

| Common stock dividends ($0.76 per share) |

|

|

| (255) |

|

|

|

|

| (255) |

| Issuance of common shares - public offering | 1 |

| $88 |

|

|

|

|

|

| 88 |

| Issuance of common shares for stock plans |

|

| 26 |

|

|

|

|

|

| 26 |

| Other comprehensive income |

|

|

|

|

|

|

| 5 |

| 5 |

| Distributions to noncontrolling interest |

|

|

|

|

|

|

|

| (2) | (2) |

| BALANCE AS OF MARCH 31, 2020 | 334 | $35 | $8,168 | $11,220 | 23 | $(1,038) | $(110) | $(14) | $206 | $18,467 |

|

| | | | | | | | | | | | |

| (In Millions, except for dividends per share) | Common Stock | Additional

Paid-In

Capital | Retained

Earnings | Treasury Stock | Capital

Stock

Expense | Accumulated

Other

Comprehensive

Income/(Loss) | Non- controlling

Interest | Total |

| Shares | Amount | Shares | Amount |

| BALANCE AS OF DECEMBER 31, 2017 | 310 | $34 | $6,298 | $10,235 | 23 | $(1,038) | $(85) | $(26) | $7 | $15,425 |

| Net income |

|

|

| 428 |

|

|

|

|

| 428 |

| Common stock dividends ($0.715 per share) |

|

|

| (221) |

|

|

|

|

| (221) |

| Issuance of common shares for stock plans | 1 |

| 25 |

|

|

|

|

|

| 25 |

| Other comprehensive income |

|

|

|

|

|

|

| 4 |

| 4 |

| Noncontrolling interest |

|

|

|

|

|

|

|

|

| — |

|

| BALANCE AS OF MARCH 31, 2018 | 311 | $34 | $6,323 | $10,442 | 23 | $(1,038) | $(85) | $(22) | $7 | $15,661 |

| Net income |

|

|

| 188 |

|

|

|

|

| 188 |

| Common stock dividends ($0.715 per share) |

|

|

| (223) |

|

|

|

|

| (223) |

| Issuance of common shares for stock plans |

|

| 27 |

|

|

|

|

|

| 27 |

| Other comprehensive income |

|

|

|

|

|

|

| 2 |

| 2 |

| Noncontrolling interest |

|

|

|

|

|

|

|

|

| — |

|

| BALANCE AS OF JUNE 30, 2018 | 311 | $34 | $6,350 | $10,407 | 23 | $(1,038) | $(85) | $(20) | $7 | $15,655 |

| | | | | | | | | | | |

| BALANCE AS OF DECEMBER 31, 2018 | 321 | $34 | $7,117 | $10,728 | 23 | $(1,038) | $(99) | $(16) | $113 | $16,839 |

| Net income |

|

|

| 424 |

|

|

|

| 21 | 445 |

| Common stock dividends ($0.74 per share) |

|

|

| (237) |

|

|

|

|

| (237) |

| Issuance of common shares – public offering | 6 |

| 433 |

|

|

| (8) |

|

| 425 |

| Issuance of common shares for stock plans |

|

| 27 |

|

|

|

|

|

| 27 |

| Other comprehensive income |

|

|

|

|

|

|

| 4 |

| 4 |

| Distributions to noncontrolling interest |

|

|

|

|

|

|

|

| (2) | (2) |

| BALANCE AS OF MARCH 31, 2019 | 327 | $34 | $7,577 | $10,915 | 23 | $(1,038) | $(107) | $(12) | $132 | $17,501 |

| Net income |

|

|

| 152 |

|

|

|

| 27 | 179 |

| Common stock dividends ($0.74 per share) |

|

|

| (242) |

|

|

|

|

| (242) |

| Issuance of common shares – public offering | 5 | 1 | 402 |

|

|

| (3) |

|

| 400 |

| Issuance of common shares for stock plans |

|

| 29 |

|

|

|

|

|

| 29 |

| Other comprehensive income |

|

|

|

|

|

|

| 1 |

|

| 1 |

| Distributions to noncontrolling interest |

|

|

|

|

|

|

|

| (3) | (3) |

| BALANCE AS OF JUNE 30, 2019 | 332 | $35 | $8,008 | $10,825 | 23 | $(1,038) | $(110) | $(11) | $156 | $17,865 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison Company of New York, Inc.

CONSOLIDATED INCOME STATEMENT (UNAUDITED)

| | | | For the Three Months Ended June 30, | For the Six Months Ended June 30, | For the Three Months Ended March 31, |

| (Millions of Dollars) | 2019 | 2018 | 2019 | 2018 | 2020 | 2019 |

| OPERATING REVENUES | | |

| Electric | $1,833 | $1,807 | $3,630 | $3,536 | $1,770 | $1,797 |

| Gas | 408 | 435 | 1,330 | 1,276 | 834 | 921 |

| Steam | 90 | 96 | 411 | 410 | 250 | 321 |

| TOTAL OPERATING REVENUES | 2,331 | 2,338 | 5,371 | 5,222 | 2,854 | 3,039 |

| OPERATING EXPENSES | | |

| Purchased power | 313 | 343 | 635 | 645 | 273 | 322 |

| Fuel | 26 | 38 | 133 | 162 | 78 | 106 |

| Gas purchased for resale | 76 | 118 | 393 | 391 | 195 | 317 |

| Other operations and maintenance | 651 | 629 | 1,311 | 1,260 | 569 | 659 |

| Depreciation and amortization | 339 | 316 | 673 | 626 | 390 | 334 |

| Taxes, other than income taxes | 550 | 512 | 1,125 | 1,051 | 607 | 575 |

| TOTAL OPERATING EXPENSES | 1,955 | 1,956 | 4,270 | 4,135 | 2,112 | 2,313 |

| OPERATING INCOME | 376 | 382 | 1,101 | 1,087 | 742 | 726 |

| OTHER INCOME (DEDUCTIONS) | | |

| Investment and other income | 4 | 13 | 8 | 2 | 9 |

| Allowance for equity funds used during construction | 3 | 6 | 4 | 3 |

| Other deductions | (22) | (42) | (41) | (81) | (67) | (19) |

| TOTAL OTHER INCOME (DEDUCTIONS) | (15) | (35) | (22) | (67) | (61) | (7) |

| INCOME BEFORE INTEREST AND INCOME TAX EXPENSE | 361 | 347 | 1,079 | 1,020 | 681 | 719 |

| INTEREST EXPENSE | | |

| Interest on long-term debt | 165 | 162 | 334 | 324 | 172 | 169 |

| Other interest | 19 | 7 | 36 | 12 | 11 | 17 |

| Allowance for borrowed funds used during construction | (2) | (6) | (4) | (3) |

| NET INTEREST EXPENSE | 182 | 167 | 364 | 332 | 180 | 183 |

| INCOME BEFORE INCOME TAX EXPENSE | 179 | 180 | 715 | 688 | 501 | 536 |

| INCOME TAX EXPENSE | 27 | 31 | 151 | 150 | 95 | 124 |

| NET INCOME | $152 | $149 | $564 | $538 | $406 | $412 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison Company of New York, Inc.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME (UNAUDITED)

| | | | Three Months Ended June 30, | Six Months Ended June 30, | Three Months Ended March 31, |

| (Millions of Dollars) | 2019 |

| 2018 | 2019 |

| 2018 | 2020 | 2019 |

|

| NET INCOME | $152 | $149 | $564 | $538 | $406 | $412 |

| Pension and other postretirement benefit plan liability adjustments, net of taxes | — |

| 1 | — |

| 1 | 1 | — |

|

| TOTAL OTHER COMPREHENSIVE INCOME, NET OF TAXES | — |

| 1 | — |

| 1 | 1 | — |

|

| COMPREHENSIVE INCOME | $152 | $150 | $564 | $539 | $407 | $412 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison Company of New York, Inc.

CONSOLIDATED STATEMENT OF CASH FLOWS (UNAUDITED)

| | | For the Six Months Ended June 30, | | For the Three Months Ended March 31, | |

| (Millions of Dollars) | 2019 |

| 2018 |

| 2020 |

| 2019 |

|

| OPERATING ACTIVITIES | | |

| Net income | $564 | $538 | $406 | $412 |

| PRINCIPAL NON-CASH CHARGES/(CREDITS) TO INCOME | | |

| Depreciation and amortization | 673 | 626 | 390 | 334 |

| Deferred income taxes | 90 | 149 | 94 | 122 |

| Rate case amortization and accruals | (58) | (65) | (11) | (29) |

| Common equity component of allowance for funds used during construction | (6) | (4) | (3) |

| Unbilled revenue and net unbilled revenue deferrals | 21 | 36 | 41 | 19 |

| Gain on sale of assets | (5) | — |

| — |

| (5) |

| Other non-cash items, net | (10) | (13) | 35 | (11) |

| CHANGES IN ASSETS AND LIABILITIES | | |

| Accounts receivable – customers | 143 | 14 | (78) | (36) |

| Materials and supplies, including fuel oil and gas in storage | 17 | 10 | 20 | 24 |

| Revenue decoupling mechanism | (126) | — |

| (22) | (55) |

| Other receivables and other current assets | 115 | (74) | 25 | 31 |

| Accounts receivable from affiliated companies | 83 | (149) | (8) | (6) |

| Prepayments | (33) | (17) | (473) | (438) |

| Accounts payable | (140) | (71) | (115) | (75) |

| Accounts payable to affiliated companies | (2) | 9 | |

| Pensions and retiree benefits obligations, net | 157 | 3 | 87 |

| Pensions and retiree benefits contributions | (77) | (367) | (4) | (3) |

| Superfund and environmental remediation costs, net | (8) | (9) | (5) | (2) |

| Accrued taxes | (18) | (66) | (42) | (18) |

| Accrued taxes to affiliated companies | — |

| (72) | |

| Accrued interest | (2) | (1) | 75 | 72 |

| System benefit charge | — |

| 86 | (20) | 7 |

| Deferred charges, noncurrent assets and other regulatory assets | (216) | (164) | (39) | (47) |

| Deferred credits and other regulatory liabilities | 146 | 229 | 122 | 92 |

| Other current and noncurrent liabilities | (17) | (125) | (50) | (77) |

| NET CASH FLOWS FROM OPERATING ACTIVITIES | 1,291 | 655 | 340 | 395 |

| INVESTING ACTIVITIES | | |

| Utility construction expenditures | (1,501) | (1,509) | (719) | (728) |

| Cost of removal less salvage | (138) | (118) | (67) | (70) |

| Proceeds from sale of assets | 48 | — |

| — |

| 48 |

| NET CASH FLOWS USED IN INVESTING ACTIVITIES | (1,591) | (1,627) | (786) | (750) |

| FINANCING ACTIVITIES | | |

| Net issuance/(payment) of short-term debt | (343) | 400 | |

| Net payment of short-term debt | | (540) | (107) |

| Issuance of long-term debt | 700 | 1,640 | 1,600 | — |

|

| Retirement of long-term debt | (475) | (600) | |

| Debt issuance costs | (8) | (16) | (23) | (1) |

| Capital contribution by parent | 850 | 70 | 25 | 225 |

| Dividend to parent | (456) | (423) | (246) | (228) |

| NET CASH FLOWS FROM FINANCING ACTIVITIES | 268 | 1,071 | |

| CASH, TEMPORARY CASH INVESTMENTS, AND RESTRICTED CASH: | | |

| NET CASH FLOWS FROM (USED) FINANCING ACTIVITIES | | 816 | (111) |

| CASH AND TEMPORARY CASH INVESTMENTS | | |

| NET CHANGE FOR THE PERIOD | (32) | 99 | 370 | (466) |

| BALANCE AT BEGINNING OF PERIOD | 818 | 730 | 933 | 818 |

| BALANCE AT END OF PERIOD | $786 | $829 | $1,303 | $352 |

| SUPPLEMENTAL DISCLOSURE OF CASH INFORMATION | | |

| Cash paid/(received) during the period for: | | |

| Cash paid during the period for: | | |

| Interest | $340 | $324 | $97 | $101 |

| Income taxes | $(20) | $227 | $12 | $8 |

| SUPPLEMENTAL DISCLOSURE OF NON-CASH INFORMATION | | |

| Construction expenditures in accounts payable | $297 | $284 | $292 | $267 |

| Software licenses acquired but unpaid as of end of period | $76 | $89 | $76 | $95 |

| Equipment acquired but unpaid as of end of period | | $33 | — |

|

The accompanying notes are an integral part of these financial statements.

Consolidated Edison Company of New York, Inc.

CONSOLIDATED BALANCE SHEET (UNAUDITED)

| | | (Millions of Dollars) | June 30,

2019 | December 31,

2018 |

| March 31,

2020 | December 31,

2019 |

| ASSETS | | | |

| CURRENT ASSETS | | | |

| Cash and temporary cash investments | $786 | $818 | $1,303 | $933 |

| Accounts receivable – customers, less allowance for uncollectible accounts of $60 and $57 in 2019 and 2018, respectively | 1,016 | 1,163 | |

| Other receivables, less allowance for uncollectible accounts of $3 in 2019 and 2018 | 89 | 211 | |

| Taxes receivable | 5 | 5 | |

| Accounts receivable – customers, less allowance for uncollectible accounts of $70 and $65 in 2020 and 2019, respectively | | 1,226 | 1,153 |

| Other receivables, less allowance for uncollectible accounts of $3 in 2020 and 2019 | | 118 | 120 |

| Accrued unbilled revenue | 403 | 392 | 331 | 477 |

| Accounts receivable from affiliated companies | 131 | 214 | 81 | 73 |

| Fuel oil, gas in storage, materials and supplies, at average cost | 287 | 304 | 273 | 293 |

| Prepayments | 150 | 117 | 651 | 178 |

| Regulatory assets | 82 | 64 | 125 | 113 |

| Revenue decoupling mechanism receivable | 127 | — |

| 98 | 76 |

| Other current assets | 67 | 69 | 100 | 127 |

| TOTAL CURRENT ASSETS | 3,143 | 3,357 | 4,306 | 3,543 |

| INVESTMENTS | 422 | 385 | 417 | 461 |

| UTILITY PLANT, AT ORIGINAL COST | | | |

| Electric | 29,416 | 28,595 | 30,292 | 29,989 |

| Gas | 8,762 | 8,295 | 9,411 | 9,229 |

| Steam | 2,580 | 2,562 | 2,625 | 2,601 |

| General | 3,140 | 3,056 | 3,314 | 3,271 |

| TOTAL | 43,898 | 42,508 | 45,642 | 45,090 |

| Less: Accumulated depreciation | 9,333 | 8,988 | 9,682 | 9,490 |

| Net | 34,565 | 33,520 | 35,960 | 35,600 |

| Construction work in progress | 1,780 | 1,850 | 1,874 | 1,812 |

| NET UTILITY PLANT | 36,345 | 35,370 | 37,834 | 37,412 |

| NON-UTILITY PROPERTY | | | |

| Non-utility property, less accumulated depreciation of $25 in 2019 and 2018 | 3 | 4 | |

| Non-utility property, less accumulated depreciation of $25 in 2020 and 2019 | | 2 |

| NET PLANT | 36,348 | 35,374 | 37,836 | 37,414 |

| OTHER NONCURRENT ASSETS | | | |

| Regulatory assets | 3,894 | 3,923 | 4,365 | 4,487 |

| Operating lease right-of-use asset | 617 | — |

| 591 | 601 |

| Other deferred charges and noncurrent assets | 51 | 69 | 53 | 51 |

| TOTAL OTHER NONCURRENT ASSETS | 4,562 | 3,992 | 5,009 | 5,139 |

| TOTAL ASSETS | $44,475 | $43,108 | $47,568 | $46,557 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison Company of New York, Inc.

CONSOLIDATED BALANCE SHEET (UNAUDITED)

| | | (Millions of Dollars) | June 30,

2019 | December 31,

2018 |

| March 31,

2020 | December 31,

2019 |

| LIABILITIES AND SHAREHOLDER’S EQUITY | | | |

| CURRENT LIABILITIES | | | |

| Long-term debt due within one year | $350 | $475 | $350 |

| Notes payable | 849 | 1,192 | 597 | 1,137 |

| Accounts payable | 835 | 977 | 848 | 956 |

| Accounts payable to affiliated companies | 15 | 17 | 13 |

| Customer deposits | 337 | 339 | 331 | 334 |

| Accrued taxes | 38 | 55 | 29 | 71 |

| Accrued interest | 110 | 112 | 188 | 113 |

| Accrued wages | 101 | 99 | 105 | 92 |

| Fair value of derivative liabilities | 41 | 25 | 99 | 81 |

| Regulatory liabilities | 61 | 73 | 93 | 63 |

| System benefit charge | 569 | 569 | 567 | 587 |

| Operating lease liabilities | 46 | — |

| 59 | 54 |

| Other current liabilities | 256 | 267 | 224 | 280 |

| TOTAL CURRENT LIABILITIES | 3,608 | 4,200 | 3,503 | 4,131 |

| NONCURRENT LIABILITIES | | | |

| Provision for injuries and damages | 140 | 141 | 124 | 125 |

| Pensions and retiree benefits | 858 | 952 | 1,080 | 1,241 |

| Superfund and other environmental costs | 686 | 693 | 657 | 654 |

| Asset retirement obligations | 298 | 292 | 366 | 362 |

| Fair value of derivative liabilities | 86 | 6 | 113 | 65 |

| Deferred income taxes and unamortized investment tax credits | 5,893 | 5,739 | 6,155 | 6,000 |

| Operating lease liabilities | 595 | — |

| 548 | 551 |

| Regulatory liabilities | 4,214 | 4,258 | 4,262 | 4,427 |

| Other deferred credits and noncurrent liabilities | 206 | 241 | 233 | 240 |

| TOTAL NONCURRENT LIABILITIES | 12,976 | 12,322 | 13,538 | 13,665 |

| LONG-TERM DEBT | 14,023 | 13,676 | 16,194 | 14,614 |

| SHAREHOLDER’S EQUITY (See Statement of Shareholder’s Equity) | 13,868 | 12,910 | 14,333 | 14,147 |

| TOTAL LIABILITIES AND SHAREHOLDER’S EQUITY | $44,475 | $43,108 | $47,568 | $46,557 |

The accompanying notes are an integral part of these financial statements.

Consolidated Edison Company of New York, Inc.

CONSOLIDATED STATEMENT OF SHAREHOLDER’S EQUITY (UNAUDITED) | | | | Common Stock | Additional

Paid-In

Capital | Retained

Earnings | Repurchased

Con Edison

Stock | Capital

Stock

Expense | Accumulated

Other

Comprehensive

Income/(Loss) | Total | Common Stock | Additional

Paid-In

Capital | Retained

Earnings | Repurchased

Con Edison

Stock | Capital

Stock

Expense | Accumulated

Other

Comprehensive

Income/(Loss) | Total |

| (In Millions, except for dividends per share) | Shares | Amount | |

| BALANCE AS OF DECEMBER 31, 2017 | 235 | $589 | $4,649 | $8,231 | $(962) | $(62) | $(6) | $12,439 | |

| (In Millions | | Shares | Amount | Additional

Paid-In

Capital | Retained

Earnings | Repurchased

Con Edison

Stock | Capital

Stock

Expense | Accumulated

Other

Comprehensive

Income/(Loss) | Total |

| BALANCE AS OF DECEMBER 31, 2018 | | 235 | $589 |

| Net income | | | 412 | | 412 |

| Common stock dividend to parent | | | (228) | | (228) |

| Capital contribution by parent | | | 225 | | 225 |

| BALANCE AS OF MARCH 31, 2019 | | 235 | $589 | $4,994 | $8,765 | $(962) | $(62) | $(5) | $13,319 |

| | | |

| BALANCE AS OF DECEMBER 31, 2019 | | 235 | $589 | $5,669 | $8,919 | $(962) | $(62) | $(6) | $14,147 |

| Net income |

|

| 389 |

|

| 389 |

| 406 |

| 406 |

| Common stock dividend to parent |

|

| (211) |

|

| (211) |

| (246) |

| (246) |

| Capital contribution by parent |

| 45 |

|

|

| 45 |

| 25 |

| 25 |

| Other comprehensive income |

|

|

|

|

| — |

|

| 1 |

| BALANCE AS OF MARCH 31, 2018 | 235 | $589 | $4,694 | $8,409 | $(962) | $(62) | $(6) | $12,662 | |

| Net income |

|

| 149 |

|

|

| 149 | |

| Common stock dividend to parent |

|

| (212 | ) |

|

| (212) | |

| Capital contribution by parent |

| 25 |

|

|

|

| 25 | |

| Other comprehensive income |

|

|

| 1 |

| 1 | |

| BALANCE AS OF JUNE 30, 2018 | 235 | $589 | $4,719 | $8,346 | $(962) | $(62) | $(5) | $12,625 | |

| | | | | | |

| BALANCE AS OF DECEMBER 31, 2018 | 235 | $589 | $4,769 | $8,581 | $(962) | $(62) | $(5) | $12,910 | |

| Net income | | | 412 | | | 412 | |

| Common stock dividend to parent | | | (228) | | | (228) | |

| Capital contribution by parent | | 225 | | | | 225 | |

| Other comprehensive income | | | | | — |

| |

| BALANCE AS OF MARCH 31, 2019 | 235 | $589 | $4,994 | $8,765 | $(962) | $(62) | $(5) | $13,319 | |

| Net income |

|

| 152 |

|

| 152 | |

| Common stock dividend to parent |

|

| (228) |

|

| (228) | |

| Capital contribution by parent |

| 625 |

|

|

| 625 | |

| Other comprehensive income |

|

|

|

|

| — |

| |

| BALANCE AS OF JUNE 30, 2019 | 235 | $589 | $5,619 | $8,689 | $(962) | $(62) | $(5) | $13,868 | |

| BALANCE AS OF MARCH 31, 2020 | | 235 | $589 | $5,694 | $9,079 | $(962) | $(62) | $(5) | $14,333 |

The accompanying notes are an integral part of these financial statements.

NOTES TO THE FINANCIAL STATEMENTS (UNAUDITED)

General

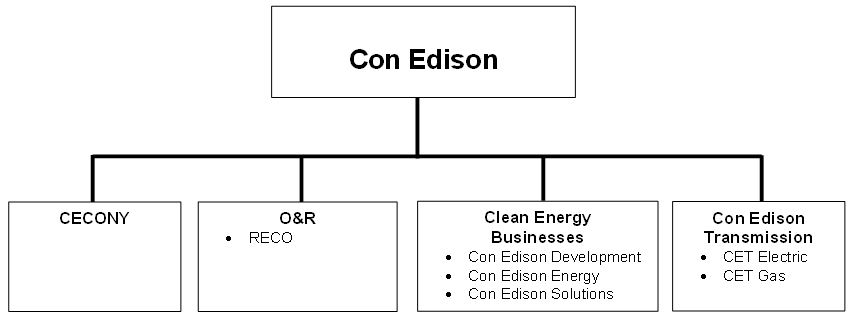

These combined notes accompany and form an integral part of the separate consolidated financial statements of each of the two2 separate registrants: Consolidated Edison, Inc. and its subsidiaries (Con Edison) and Consolidated Edison Company of New York, Inc. and its subsidiaries (CECONY). CECONY is a subsidiary of Con Edison and as such its financial condition and results of operations and cash flows, which are presented separately in the CECONY consolidated financial statements, are also consolidated, along with those of Orange and Rockland Utilities, Inc. (O&R), Con Edison Clean Energy Businesses, Inc. (together with its subsidiaries, the Clean Energy Businesses) and Con Edison Transmission, Inc. (together with its subsidiaries, Con Edison Transmission) in Con Edison’s consolidated financial statements. The term “Utilities” is used in these notes to refer to CECONY and O&R.

As used in these notes, the term “Companies” refers to Con Edison and CECONY and, except as otherwise noted, the information in these combined notes relates to each of the Companies. However, CECONY makes no representation as to information relating to Con Edison or the subsidiaries of Con Edison other than itself.

The separate interim consolidated financial statements of each of the Companies are unaudited but, in the opinion of their respective managements, reflect all adjustments (which include only normally recurring adjustments) necessary for a fair presentationstatement of the results for the interim periods presented. The Companies’ separate interim consolidated financial statements should be read together with their separate audited financial statements (including the combined notes thereto) included in Item 8 of their combined Annual Report on Form 10-K for the year ended December 31, 2018 and their separate unaudited financial statements (including the combined notes thereto) included in Part 1, Item 1 of their combined Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2019. Certain prior period amounts have been reclassified to conform to the current period presentation.

Con Edison has two2 regulated utility subsidiaries: CECONY and O&R. CECONY provides electric service and gas service in New York City and Westchester County. The company also provides steam service in parts of Manhattan. O&R, along with its regulated utility subsidiary, provides electric service in southeastern New York and northern New Jersey and gas service in southeastern New York. Con Edison Clean Energy Businesses, Inc. has three subsidiaries: Consolidated Edison Development, Inc. (Con Edison Development), a company thatthrough its subsidiaries, develops, owns and operates renewable and energy infrastructure projects; Consolidated Edison Energy, Inc. (Con Edison Energy), a company thatprojects and provides energy-related products and services to wholesale customers; and Consolidated Edison Solutions, Inc. (Con Edison Solutions), a company that provides energy-related products and services to retail customers. Con Edison Transmission, Inc. invests in electric transmission facilities through its subsidiary, Consolidated Edison Transmission, LLC (CET Electric), and invests in gas pipeline and storage facilities through its subsidiary Con Edison Gas Pipeline and Storage, LLC (CET Gas).

Note A – Summary of Significant Accounting Policies and Other Matters

Revenue RecognitionFinancial Instruments – Credit Losses

Adoption of New Standard

In January 2020, the Companies adopted ASU 2016-13, “Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments” (CECL). The following table presents, foramendments replace the threeincurred loss impairment methodology which involved delayed recognition of credit losses. The amendments introduce an expected credit loss impairment model which requires immediate recognition of anticipated losses over the instrument’s life. A broader range of reasonable and six months ended June 30, 2019supportable information must be considered in developing the credit loss estimates. The Companies' financial instruments subject to the amendments are included in the lines “Accounts receivable – customers” and 2018, revenue from contracts with customers as defined in Accounting Standards Codification (ASC) Topic 606, "Revenue from Contracts with Customers," as well as additional revenue from sources other than contracts with customers, disaggregated by major source.“Other receivables.” Substantially all of these in-scope financial instruments are expected to be collected within one year of billing.

The Companies adopted the amendments using the modified retrospective method for all financial instruments measured at amortized costs. Results for reporting periods beginning after January 1, 2020 are presented under ASC 326 while prior period amounts continue to be reported in accordance with previously applicable GAAP. No prior period adjustment or charge to retained earnings for cumulative impact was required as a result of the Companies’ adoption of the amendments.

The Utilities’ “Account receivable – customers” balance consists of utility bills due (bills are generally due the month following billing) from customers who have energy delivered, generated, or services provided by the Utilities. The balance also reflects the Utilities’ purchase of receivables from energy service companies to support the retail choice programs.

“Other receivables” balance generally reflects costs billed by the Utilities for goods and services provided to external parties, such as accommodation work for private parties and certain governmental entities, real estate rental and pole attachments.

|

| | | | | | | | | | | | | | |

| | For the Three Months Ended June 30, 2019 | For the Three Months Ended June 30, 2018 |

| (Millions of Dollars) | Revenues from contracts with customers | | Other revenues (a) | Total operating revenues | Revenues from contracts with customers | | Other revenues (a) | Total operating revenues |

| CECONY | | | | | | | | |

| Electric | $1,751 | | $82 | $1,833 | $1,771 | | $36 | $1,807 |

| Gas | 400 | | 8 | 408 | 428 | | 7 | 435 |

| Steam | 86 | | 4 | 90 | 93 | | 3 | 96 |

| Total CECONY | $2,237 | | $94 | $2,331 | $2,292 | | $46 | $2,338 |

| O&R | | | | | | | | |

| Electric | 140 | | (2) | 138 | 146 | | (2) | 144 |

| Gas | 39 | | 2 | 41 | 47 | | 7 | 54 |

| Total O&R | $179 | |

| $— |

| $179 | $193 | | $5 | $198 |

| Clean Energy Businesses | | | | | | | | |

| Renewables | 171 | (b) | — |

| 171 | 73 | (b) | — |

| 73 |

| Energy services | 16 | | — |

| 16 | 23 | | — |

| 23 |

| Other | — |

| | 46 | 46 | — |

| | 62 | 62 |

| Total Clean Energy Businesses | $187 | | $46 | $233 | $96 | | $62 | $158 |

| Con Edison Transmission | 1 | | — |

| 1 | 1 | | — |

| 1 |

| Other (c) | — |

|

| — |

| — |

| — |

|

| 1 | 1 |

| Total Con Edison | $2,604 | | $140 | $2,744 | $2,582 | | $114 | $2,696 |

(a) ForThe Clean Energy Businesses’ accounts receivable balance generally reflects bills related to the Utilities, this includes revenuesale of energy from alternative revenue programs, such asrenewable electric production projects, the revenue decoupling mechanisms under their New York electricmanagement of energy supply assets, energy-efficiency services to government and gas rate plans.Forcommercial customers, and the engineering, procurement, and construction services of renewable energy projects. The Clean Energy Businesses this includes revenue from wholesale services.calculate an allowance for uncollectible accounts related to their energy services customers based on an aging and customer-specific analysis. The amount of such reserves was not material at March 31, 2020.

(b) Included withinThe Companies develop expected loss estimates using past events data and consider current conditions and future reasonable and supportable forecasts. Changes to the totalsUtilities’ reserve balances which result in write-offs of customer accounts receivable balances above existing rate allowances are not reflected in rates during the term of the current rate plans and are considered in a future rate proceeding. For the Utilities’ customer accounts receivable allowance for Renewables revenue atuncollectible accounts, past events considered include write-offs relative to total customer accounts receivable; current conditions include macro-and micro-economic conditions related to trends in the Clean Energy Businesseslocal economy and bankruptcy rates, among other factors; and forecasts about the future include assumptions related to the level of write-offs and recoveries.

Other receivables allowance for uncollectible accounts is $4calculated based on a historical average of collections relative to total other receivables, including current receivables. Current macro- and micro-economic conditions are also considered when calculating the current reserve. Probable outcomes of pending litigation, whether favorable or unfavorable to the Companies, are also included in the consideration.

During the first quarter of 2020, the potential economic impact of the COVID-19 pandemic was also considered in forward looking projections related to write-off and recovery rates, and resulted in increases to the allowance for uncollectible accounts of $5 million for Con Edison, substantially all of which related to CECONY.

Customer accounts receivable and $9 millionthe associated allowance for uncollectible accounts are included in the line “Accounts receivable – customers” on the Companies’ consolidated balance sheets. Other receivables and the associated allowance for uncollectible accounts are included in “Other receivables” on the consolidated balance sheets.

The table below presents a rollforward by major portfolio segment type for the three months ended June 30, 2019 and 2018, respectively, of revenue related to engineering, procurement and construction services.

| |

(c) | Parent company and consolidation adjustments. |

|

| | | | | | | | | | | | | |

| | For the Six Months Ended June 30, 2019 | For the Six Months Ended June 30, 2018 |

| | Revenues from contracts with customers | | Other revenues (a) | Total operating revenues | Revenues from contracts with customers | | Other revenues (a) | Total operating revenues |

| CECONY | | | | | | | | |

| Electric | $3,465 | | $165 | $3,630 | $3,474 | | $62 | $3,536 |

| Gas | 1,310 | | 20 | 1,330 | 1,252 | | 24 | 1,276 |

| Steam | 402 | | 9 | 411 | 404 | | 6 | 410 |

| Total CECONY | $5,177 | | $194 | $5,371 | $5,130 | | $92 | $5,222 |

| O&R | | | | | | | | |

| Electric | 283 | | — |

| 283 | 293 | | — |

| 293 |

| Gas | 153 | | 1 | 154 | 148 | | 4 | 152 |

| Total O&R | $436 | | $1 | $437 | $441 | | $4 | $445 |

| Clean Energy Businesses | | | | | | | | |

| Renewables | 278 | (b) | — |

| 278 | 205 | (b) | — |

| 205 |

| Energy services | 39 | | — |

| 39 | 41 | | — |

| 41 |

| Other | — |

| | 133 | 133 | — |

| | 145 | 145 |

| Total Clean Energy Businesses | $317 | | $133 | $450 | $246 | | $145 | $391 |

| Con Edison Transmission | 2 | | — |

| 2 | 2 | | — |

| 2 |

| Other (c) | — |

| | (2) | (2) | — |

| | — |

| — |

|

| Total Con Edison | $5,932 | | $326 | $6,258 | $5,819 | | $241 | $6,060 |

(a) For the Utilities, this includes revenue from alternative revenue programs, such as the revenue decoupling mechanisms under their New York electric and gas rate plans.For the Clean Energy Businesses, this includes revenue from wholesale services.

(b) Included within the totals for Renewables revenue at the Clean Energy Businesses is $6 millionand $97 millionfor the six months ended June 30, 2019 and 2018, respectively, of revenue related to engineering, procurement and construction services.

| |

(c) | Parent company and consolidation adjustments. |

|

| | | | | | |

| | For the Three Months Ended March 31, 2020 |

| | Con Edison | CECONY |

| (Millions of Dollars) | Accounts receivable - customers | Other receivables | Accounts receivable - customers | Other receivables |

| Allowance for credit losses | | | | |

| Beginning Balance at January 1, 2020 | $70 | $4 | $65 | $3 |

| Recoveries | 2 | — |

| 2 | — |

|

| Write-offs | (18) | — |

| (18) | — |

|

| Reserve adjustments | 21 | 1 | 21 | — |

|

| Ending Balance March 31, 2020 | $75 | $5 | $70 | $3 |

20

|

| | | | | | | |

| | 2019 | 2018 |

| (Millions of Dollars) | Unbilled contract revenue (a) | Unearned revenue (b) |

| | Unbilled contract revenue (a) | Unearned revenue (b) | |

| Beginning balance as of January 1, | $29 | $20 | | $58 | $87 | |

| Additions (c) | 44 | — |

| | 73 | 31 | |

| Subtractions (c) | 38 | 2 | (d) | 88 | 105 | (d) |

| Ending balance as of June 30, | $35 | $18 | | $43 | $13 | |

| |

(a) | Unbilled contract revenue represents accumulated incurred costs and earned profits on contracts (revenue arrangements), which have been recorded as revenue, but have not yet been billed to customers, and which represent contract assets as defined in Topic 606. Substantially all accrued unbilled contract revenue is expected to be collected within one year. Unbilled contract revenue arises from the cost-to-cost method of revenue recognition. Unbilled contract revenue from fixed-price type contracts is converted to billed receivables when amounts are invoiced to customers according to contractual billing terms, which generally occur when deliveries or other performance milestones are completed. |

| |

(b) | Unearned revenue represents a liability for billings to customers in excess of earned revenue, which are contract liabilities as defined in Topic 606. |

| |

(c) | Additions for unbilled contract revenue and subtractions for unearned revenue represent additional revenue earned. Additions for unearned revenue and subtractions for unbilled contract revenue represent billings. Activity also includes appropriate balance sheet classification for the period. |

| |

(d) | Of the subtractions from unearned revenue, $2 million and $50 million were included in the balance as of January 1, 2019 and 2018, respectively. |

As of June 30, 2019, the aggregate amount of the remaining fixed performance obligations of the Clean Energy Businesses under contracts with customers for energy services is $67 million, of which $31 million will be recognized within the next two years, and the remaining $36 million will be recognized pursuant to long-term service and maintenance agreements.

General Utility Plant

General utility plant of Con Edison and CECONY included $97$91 million and $92$87 million, respectively, at June 30, 2019March 31, 2020 and $100$93 million and $95$88 million, respectively, at December 31, 2018,2019, related to a May 2018 acquisition of software licenses. The estimated aggregate annual amortization expense related to the software licenses for Con Edison and CECONY is $7 million. The accumulated amortization for Con Edison and CECONY was $7$12 million and $6$11 million, respectively at June 30, 2019March 31, 2020 and was $3$10 million at December 31, 2018.2019.

Goodwill

The Companies test goodwill for impairment at least annually or whenever there is a triggering event, and test long-lived and intangible assets for recoverability when events or changes in circumstances indicate that the carrying value of long-lived or intangible assets may not be recoverable. The Companies identified no triggering events or changes in circumstances related to the COVID-19 pandemic that would indicate that the carrying value of long-lived or intangible assets may not be recoverable at March 31, 2020.

Long-Lived and Intangible Assets

In January 2019, Pacific Gas and Electric Company (PG&E) filed in the United States Bankruptcy Court for the Northern District of California for reorganization under Chapter 11 of the U.S. Bankruptcy Code. The output of Con Edison Developmentcertain of the Clean Energy Businesses' renewable electric production projects with an aggregate generating capacity of 680 MW (AC) of generating capacity (PG&E Projects) is sold to PG&E under long-term power purchase agreements (PG&E PPAs). Most of the PG&E PPAs have contract prices that are higher than estimated market prices. PG&E, as a debtor in possession, may assume or reject the PG&E PPAs, subject to review by the bankruptcy court.

In March 2020, PG&E and certain PG&E shareholders submitted a joint plan of reorganization to the bankruptcy court. The plan includes the assumption by PG&E of all of its power purchase agreements. The plan is subject to, among other things: confirmation by the bankruptcy court by June 30, 2020 (or any extension of the date by which PG&E’s bankruptcy must be resolved for PG&E to participate in the insurance fund described below); approval by the California Public Utilities Commission (CPUC) of PG&E’s implementation of the plan and participation in the insurance fund; PG&E obtaining funding for distributions under the plan; and the continuation in full force and effect of the September 2019 subrogation claims restructuring support agreement, the December 2019 tort claimants restructuring support agreement and the January 2020 noteholder restructuring support agreement. The plan is supported by the parties to these restructuring support agreements, subject to their terms, and includes the assumption by PG&E of all of its power purchase agreements. A plan of reorganization can be revoked, amended, withdrawn or pursuantdelayed prior to aits confirmation by the bankruptcy court. The bankruptcy court has authorized PG&E to send the plan to creditors for consideration, and the current deadline for creditors to return ballots is May 15, 2020. The hearing to consider confirmation of the plan is scheduled to commence later in May 2020.

In January and May 2019, FERC orderissued orders (which PG&E is challenging), the bankruptcy court and FERC. In a May 2019 order, FERC denied PG&E’s request for a rehearing of the January 2019 order and reaffirmed affirming its jurisdiction to review and approve the modification or abrogation of wholesale power contracts that are the subject of rejection in bankruptcy. In June 2019, the bankruptcy court ruled that FERC does not have concurrent jurisdiction with it and that FERC’s January and May 2019 orders are of no force and effect in the bankruptcy proceeding. FERC and additional parties, including Con Edison Development,the Clean Energy Businesses, are challenging the bankruptcy court’s June 2019 ruling. ruling in appeals that are pending in the United States Court of Appeals for the Ninth Circuit.

In July 2019, California enacted a law addressing future California wildfires. The law includes provisions for the establishment of wildfire liquidity and insurance funds and possible limitation of future wildfire liabilities for California utilities. PG&E, Southern California Edison Company and San Diego Gas & Electric Company have agreed to participate in the insurance fund. PG&E’s participation will require bankruptcy court approval and is conditioned on, among other things, resolution of PG&E’s bankruptcy by June 30, 2020, and a determination by the California Public Utilities CommissionCPUC that PG&E’s bankruptcy reorganization plan is consistent with the state’s climate goals as required under the California Renewables Portfolio Standard Program and related procurement requirements of the state.

The PG&E bankruptcy is an event of default under the PG&E PPAs. Unless the lenders for the related project debt otherwise agree, distributions from the related projects to Con Edison Developmentthe Clean Energy Businesses will not be made during the pendency of the bankruptcy. See “Reconciliation of Cash, Temporary Cash Investments and Restricted Cash,” below.

At June 30,March 31, 2020 and December 31, 2019, Con Edison’s consolidated balance sheet included $853$802 million and $819 million of net non-utility plant relating to the PG&E Projects, $1,090$1,039 million and $1,057 million of intangible assets relating to the PG&E PPAs, $288$274 million and $282 million of net non-utility plant of additional projects that secure the related project debt and $1,032$980 million of

non-recourse related project debt.debt, respectively. See "Long-term Debt" in Note C. Con Edison has tested whether its net non-utility plant relating to the PG&E Projects and intangible assets relating to the PG&E PPAs have been impaired. The projected future cash flows used in the test reflected Con Edison’s expectation that the PG&E PPAs are not likely to be rejected. Based on the test, Con Edison has determined that there was no impairment. If, in the future, one or more of the PG&E PPAs is rejected or any such rejection becomes likely, there will be an impairment of the related intangible assets and could be an impairment of the related non-utility plant. The amount of any such impairment could be material.

Earnings Per Common Share

Con Edison presents basic and diluted earnings per share (EPS) on the face of its consolidated income statement. Basic EPS is calculated by dividing earnings available to common shareholders (“Net income for common stock” on Con Edison’s consolidated income statement) by the weighted average number of Con Edison common shares outstanding during the period. In the calculation of diluted EPS, weighted average shares outstanding are increased for additional shares that would be outstanding if potentially dilutive securities were converted to common stock.

Potentially dilutive securities for Con Edison consist of restricted stock units and deferred stock units for which the average market price of the common shares for the period was greater than the exercise price and its common shares that are subject to a May 2019 forward sale agreement (see Note C). Before the issuance of common shares upon settlement of the forward sale agreement, the shares will be reflected in the company’s diluted earnings per share calculations using the treasury stock method. Under this method, the number of common shares used in calculating diluted earnings per share is deemed to be increased by the excess, if any, of the number of shares that would be issued upon physical settlement of the forward sale agreement over the number of shares that could be purchased by the company in the market (based on the average market price during the period) using the proceeds due upon physical settlement (based on the adjusted forward sale price at the end of the reporting period).price.

For the three and six months ended June 30,March 31, 2020 and 2019, and 2018, basic and diluted EPS for Con Edison are calculated as follows:

|

| | | | |

| | For the Three Months Ended June 30, | For the Six Months Ended June 30, |

| (Millions of Dollars, except per share amounts/Shares in Millions) | 2019 | 2018 | 2019 | 2018 |

| Net income for common stock | $152 | $188 | $576 | $616 |

| Weighted average common shares outstanding – basic | 328.3 | 310.8 | 325.2 | 310.6 |

| Add: Incremental shares attributable to effect of potentially dilutive securities | 0.9 | 1.1 | 0.9 | 1.1 |

| Adjusted weighted average common shares outstanding – diluted | 329.2 | 311.9 | 326.1 | 311.7 |

| Net Income per common share – basic | $0.46 | $0.60 | $1.77 | $1.98 |

| Net Income per common share – diluted | $0.46 | $0.60 | $1.77 | $1.98 |

|

| | |

| | For the Three Months Ended March 31, |

| (Millions of Dollars, except per share amounts/Shares in Millions) | 2020 | 2019 |

| Net income for common stock | $375 | $424 |

| Weighted average common shares outstanding – basic | 333.6 | 322.5 |

| Add: Incremental shares attributable to effect of potentially dilutive securities | 1.0 | 0.9 |

| Adjusted weighted average common shares outstanding – diluted | 334.6 | 323.4 |

| Net Income per common share – basic | $1.13 | $1.31 |

| Net Income per common share – diluted | $1.12 | $1.31 |

The computation of diluted EPS for the three and six months ended June 30,March 31, 2020 and 2019 and 2018 excludes immaterial amounts of performance share awards that were not included because of their anti-dilutive effect.

Changes in Accumulated Other Comprehensive Income/(Loss) by Component

For the three and six months ended June 30,March 31, 2020 and 2019, and 2018, changes to accumulated other comprehensive income/(loss) (OCI) for Con Edison and CECONY are as follows:

|

| | | | | |

| | For the Three Months Ended June 30, |

| | Con Edison | CECONY |

| (Millions of Dollars) | 2019 | 2018 | 2019 |

| 2018 |

| Beginning balance, accumulated OCI, net of taxes (a) | $(12) | $(22) | $(5) | $(6) |

| Amounts reclassified from accumulated OCI related to pension plan liabilities, net of tax of $(1) for Con Edison in 2018 (a)(b) | 1 | 2 | — |

| 1 |

| Current period OCI, net of taxes | 1 | 2 | — |

| 1 |

| Ending balance, accumulated OCI, net of taxes | $(11) | $(20) | $(5) | $(5) |

| | | | For the Six Months Ended June 30, | For the Three Months Ended March 31, |

| | Con Edison | CECONY | Con Edison | CECONY |

| (Millions of Dollars) | 2019 | 2018 | 2019 |

| 2018 |

| 2020 | 2019 | 2020 |

| 2019 |

|

| Beginning balance, accumulated OCI, net of taxes (a) | $(16) | $(26) | $(5) | $(6) | $(19) | $(16) | $(6) | $(5) |

| OCI before reclassifications, net of tax of $(1) for Con Edison in 2019 and 2018 | 2 | 3 | — |

| — |

| |

| Amounts reclassified from accumulated OCI related to pension plan liabilities, net of tax of $(1) for Con Edison in 2019 and 2018 (a)(b) | 3 | 3 | — |

| 1 | |

| OCI before reclassifications, net of tax of $(1) for Con Edison in 2020 and 2019 | | 4 | 2 | — |

| — |

|

| Amounts reclassified from accumulated OCI related to pension plan liabilities, net of tax of $(1) for Con Edison in 2020 (a)(b) | | 1 | 2 | 1 | — |

|

| Current period OCI, net of taxes | 5 | 6 | — |

| 1 | 5 | 4 | 1 | — |

|

| Ending balance, accumulated OCI, net of taxes | $(11) | $(20) | $(5) | $(5) | $(14) | $(12) | $(5) | $(5) |

| |

| (a) | Tax reclassified from accumulated OCI is reported in the income tax expense line item of the consolidated income statement. |

| |

| (b) | For the portion of unrecognized pension and other postretirement benefit costs relating to the Utilities, costs are recorded into, and amortized out of, regulatory assets and liabilities instead of OCI. The net actuarial losses and prior service costs recognized during the period are included in the computation of total periodic pension and other postretirement benefit cost. See Notes E and F. |

Reconciliation of Cash, Temporary Cash Investments and Restricted Cash

Cash, temporary cash investments and restricted cash are presented on a combined basis in the Companies’ consolidated statements of cash flows. At June 30,March 31, 2020 and 2019, and 2018, cash, temporary cash investments and restricted cash for Con Edison and CECONY arewere as follows:

| | | | At June 30, | At March 31, |

| | Con Edison | CECONY | Con Edison | CECONY |

| (Millions of Dollars) | 2019 | 2018 | 2019 |

| 2018 |

| 2020 | 2019 | 2020 |

| 2019 |

|

| Cash and temporary cash investments | $831 | $866 | $786 | $829 | $1,395 | $406 | $1,303 | $352 |

| Restricted cash (a) | 139 | 55 | — |

| — |

| 179 | 68 | — |

| — |

|

| Total cash, temporary cash investments and restricted cash | $970 | $921 | $786 | $829 | $1,574 | $474 | $1,303 | $352 |

| |

| (a) | Restricted cash included cash of Con Edison Developmentthe Clean Energy Businesses' renewable electric production project subsidiaries ($138179 million and $54$67 million at June 30,March 31, 2020 and 2019, and 2018, respectively) that, under the related project debt agreements, is either restricted until the various maturity dates of the project debt to being used for normal operating expenses and capital expenditures, debt service, and required reserves.reserves or restricted as a result of the PG&E bankruptcy. During the pendency of the PG&E bankruptcy, unless the lenders for the related project debt otherwise agree, cash may not be distributed from the related projects to Con Edison Development.the Clean Energy Businesses. See “Long-Lived and Intangible Assets,” above, and Note C. In addition, restricted cash included O&R's New Jersey utility subsidiary, Rockland Electric Company transition bond charge collections, net of principal, interest, trustee and service fees ($1 million at June 30, 2019 and 2018)March 31, 2019). |

Note B – Regulatory Matters

Rate PlansCOVID-19 Regulatory Matters

CECONY – ElectricGovernors, public utility commissions, federal authorities and other regulatory agencies in the states in which the Utilities operate have issued orders related to the COVID-19 pandemic that impact the Utilities as described below.

In May 2019, the

New York State Public Service Commission (NYSPSC) staff submitted testimonyRegulation

In March 2020, New York State Governor Cuomo declared a State disaster emergency for the State of New York. Since that declaration, the NYSPSC and the Utilities have taken actions to mitigate the impact of the COVID-19 pandemic on the Utilities, their customers and other stakeholders. New York State has designated utilities, including CECONY and O&R, as essential businesses that may continue their work. The Utilities have modified or suspended certain work in the state.

In March 2020, the Utilities began suspending service disconnections, certain collection notices, final bill collection agency activity, new late payment charges and certain other fees for all customers. Historically, these fees have amounted to approximately $6 million and $0.4 million per month for CECONY and O&R, respectively. The suspension of these fees is expected to result in a reduction in revenues during the suspension period, the length of which has not yet been determined. The Utilities also began providing payment extensions for all customers that were scheduled to be disconnected prior to the start of the COVID-19 pandemic. All customer walk-in centers have been closed to the public and in-person investigations of billing issues at customer residences and businesses have been suspended. In April 2020, the NYSPSC proceedingalso suspended certain interconnection payment deadlines to mitigate the impact of the COVID-19 pandemic on developers of distributed renewable generation and energy storage. See Note K to the First Quarter Financial Statements.