Part I—Financial Information

Item 1. Financial Statements

MPLX LP

Consolidated Statements of Income (Unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| (In millions, except per unit data) | 2021 | 2020 | 2021 | 2020 | |||||||||||||||||||

| Revenues and other income: | |||||||||||||||||||||||

| Service revenue | $ | 600 | $ | 604 | $ | 1,767 | $ | 1,779 | |||||||||||||||

| Service revenue - related parties | 902 | 909 | 2,681 | 2,694 | |||||||||||||||||||

| Service revenue - product related | 82 | 41 | 235 | 102 | |||||||||||||||||||

| Rental income | 88 | 102 | 286 | 296 | |||||||||||||||||||

| Rental income - related parties | 164 | 241 | 574 | 712 | |||||||||||||||||||

| Product sales | 448 | 165 | 1,034 | 454 | |||||||||||||||||||

| Product sales - related parties | 26 | 37 | 99 | 100 | |||||||||||||||||||

| Sales-type lease revenue - related parties | 132 | 38 | 305 | 114 | |||||||||||||||||||

Income/(loss) from equity method investments(1) | 92 | 83 | 228 | (1,012) | |||||||||||||||||||

| Other income (loss) | (2) | 2 | 2 | 5 | |||||||||||||||||||

| Other income - related parties | 27 | 25 | 82 | 76 | |||||||||||||||||||

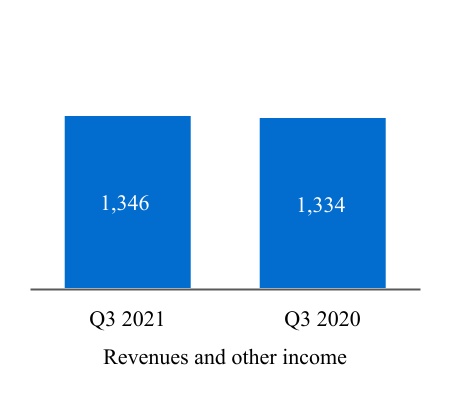

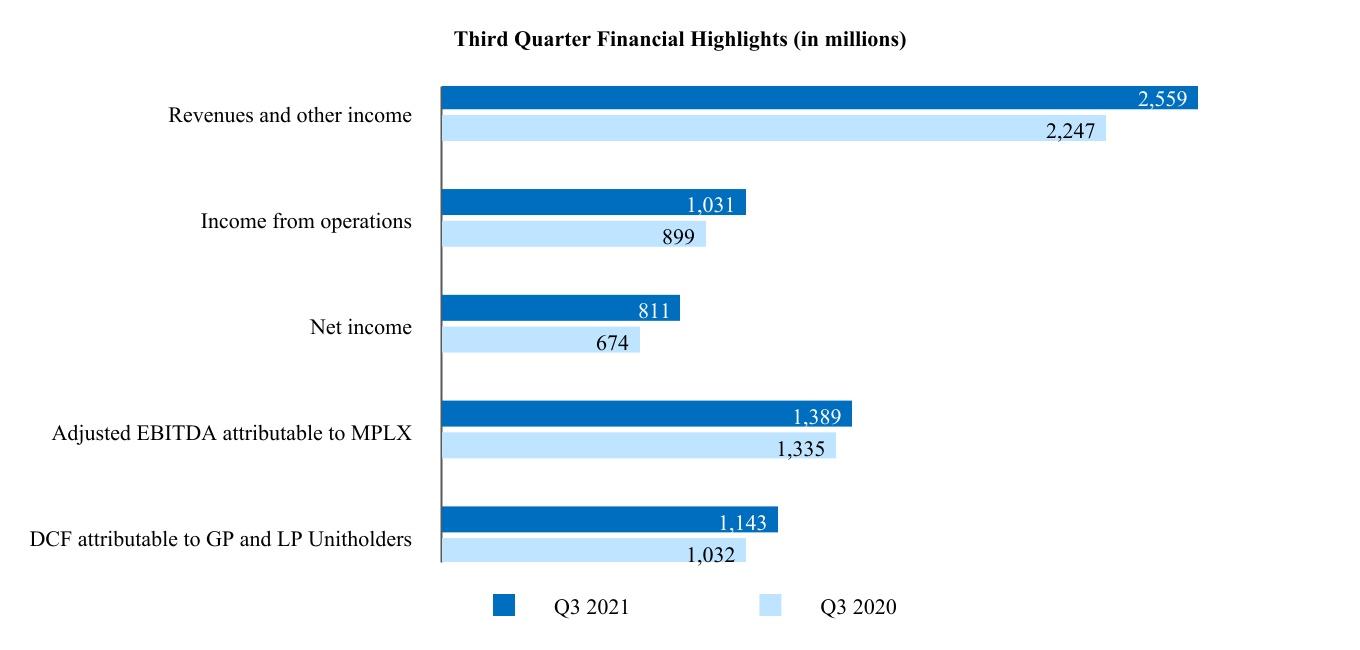

| Total revenues and other income | 2,559 | 2,247 | 7,293 | 5,320 | |||||||||||||||||||

| Costs and expenses: | |||||||||||||||||||||||

| Cost of revenues (excludes items below) | 298 | 323 | 864 | 1,006 | |||||||||||||||||||

| Purchased product costs | 421 | 152 | 1,035 | 374 | |||||||||||||||||||

| Rental cost of sales | 33 | 33 | 97 | 101 | |||||||||||||||||||

| Rental cost of sales - related parties | 24 | 32 | 86 | 119 | |||||||||||||||||||

| Purchases - related parties | 307 | 297 | 902 | 853 | |||||||||||||||||||

| Depreciation and amortization | 324 | 346 | 971 | 992 | |||||||||||||||||||

| Impairment expense | — | — | 42 | 2,165 | |||||||||||||||||||

| General and administrative expenses | 94 | 96 | 267 | 289 | |||||||||||||||||||

| Restructuring expenses | — | 36 | — | 36 | |||||||||||||||||||

| Other taxes | 27 | 33 | 93 | 94 | |||||||||||||||||||

| Total costs and expenses | 1,528 | 1,348 | 4,357 | 6,029 | |||||||||||||||||||

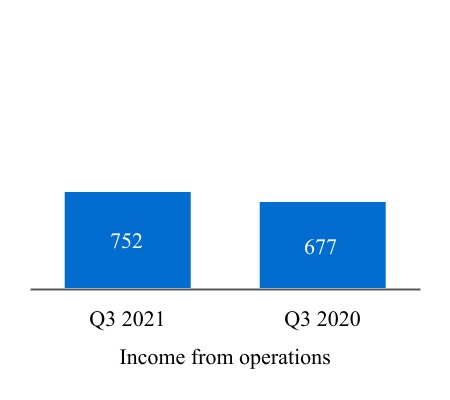

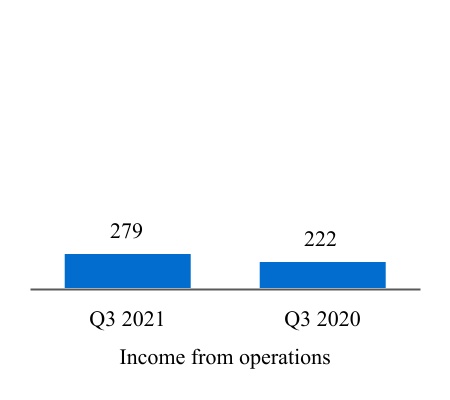

| Income/(loss) from operations | 1,031 | 899 | 2,936 | (709) | |||||||||||||||||||

| Related party interest and other financial costs | 2 | — | 4 | 4 | |||||||||||||||||||

| Interest expense (net of amounts capitalized of $2 million, $8 million, $12 million and $31 million respectively) | 197 | 207 | 590 | 624 | |||||||||||||||||||

| Other financial costs | 21 | 17 | 67 | 49 | |||||||||||||||||||

| Income/(loss) before income taxes | 811 | 675 | 2,275 | (1,386) | |||||||||||||||||||

| Provision for income taxes | — | 1 | 1 | 1 | |||||||||||||||||||

| Net income/(loss) | 811 | 674 | 2,274 | (1,387) | |||||||||||||||||||

| Less: Net income attributable to noncontrolling interests | 9 | 9 | 27 | 24 | |||||||||||||||||||

| Net income/(loss) attributable to MPLX LP | 802 | 665 | 2,247 | (1,411) | |||||||||||||||||||

| Less: Series A preferred unitholders interest in net income | 38 | 20 | 79 | 61 | |||||||||||||||||||

| Less: Series B preferred unitholders interest in net income | 10 | 10 | 31 | 31 | |||||||||||||||||||

| Limited partners’ interest in net income/(loss) attributable to MPLX LP | $ | 754 | $ | 635 | $ | 2,137 | $ | (1,503) | |||||||||||||||

| Per Unit Data (See Note 7) | |||||||||||||||||||||||

| Net income/(loss) attributable to MPLX LP per limited partner unit: | |||||||||||||||||||||||

| Common - basic | $ | 0.74 | $ | 0.61 | $ | 2.07 | $ | (1.43) | |||||||||||||||

| Common - diluted | $ | 0.74 | $ | 0.61 | $ | 2.07 | $ | (1.43) | |||||||||||||||

| Weighted average limited partner units outstanding: | |||||||||||||||||||||||

| Common - basic | 1,024 | 1,046 | 1,030 | 1,054 | |||||||||||||||||||

| Common - diluted | 1,025 | 1,047 | 1,030 | 1,054 | |||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In millions, except per unit data) | 2017 | 2016(1) | 2017 | 2016(1) | |||||||||||

| Revenues and other income: | |||||||||||||||

| Service revenue | $ | 299 | $ | 250 | $ | 845 | $ | 712 | |||||||

| Service revenue - related parties | 276 | 253 | 801 | 676 | |||||||||||

| Rental income | 69 | 77 | 208 | 218 | |||||||||||

| Rental income - related parties | 70 | 68 | 207 | 172 | |||||||||||

| Product sales | 217 | 157 | 611 | 394 | |||||||||||

| Product sales - related parties | 2 | 2 | 6 | 8 | |||||||||||

| Gain on sale of assets | — | 1 | 1 | 1 | |||||||||||

| Income (loss) from equity method investments | 23 | 6 | 29 | (72 | ) | ||||||||||

| Other income | 2 | 2 | 5 | 5 | |||||||||||

| Other income - related parties | 22 | 22 | 69 | 67 | |||||||||||

| Total revenues and other income | 980 | 838 | 2,782 | 2,181 | |||||||||||

| Costs and expenses: | |||||||||||||||

| Cost of revenues (excludes items below) | 129 | 122 | 381 | 329 | |||||||||||

| Purchased product costs | 170 | 117 | 441 | 310 | |||||||||||

| Rental cost of sales | 19 | 13 | 44 | 42 | |||||||||||

| Rental cost of sales - related parties | — | — | 1 | 1 | |||||||||||

| Purchases - related parties | 114 | 109 | 330 | 286 | |||||||||||

| Depreciation and amortization | 164 | 151 | 515 | 438 | |||||||||||

| Impairment expense | — | — | — | 130 | |||||||||||

| General and administrative expenses | 59 | 56 | 174 | 172 | |||||||||||

| Other taxes | 14 | 12 | 40 | 37 | |||||||||||

| Total costs and expenses | 669 | 580 | 1,926 | 1,745 | |||||||||||

| Income from operations | 311 | 258 | 856 | 436 | |||||||||||

| Related party interest and other financial costs | 1 | — | 1 | 1 | |||||||||||

| Interest expense (net of amounts capitalized of $6 million, $7 million, $24 million and $21 million, respectively) | 77 | 51 | 217 | 158 | |||||||||||

| Other financial costs | 15 | 13 | 40 | 37 | |||||||||||

| Income before income taxes | 218 | 194 | 598 | 240 | |||||||||||

| Provision (benefit) for income taxes | 1 | — | 3 | (12 | ) | ||||||||||

| Net income | 217 | 194 | 595 | 252 | |||||||||||

| Less: Net income attributable to noncontrolling interests | 1 | 2 | 3 | 3 | |||||||||||

| Less: Net income attributable to Predecessor | — | 51 | 36 | 149 | |||||||||||

| Net income attributable to MPLX LP | 216 | 141 | 556 | 100 | |||||||||||

| Less: Preferred unit distributions | 16 | 16 | 49 | 25 | |||||||||||

| Less: General partner’s interest in net income attributable to MPLX LP | 86 | 51 | 222 | 136 | |||||||||||

| Limited partners’ interest in net income (loss) attributable to MPLX LP | $ | 114 | $ | 74 | $ | 285 | $ | (61 | ) | ||||||

| Per Unit Data (See Note 6) | |||||||||||||||

| Net income (loss) attributable to MPLX LP per limited partner unit: | |||||||||||||||

| Common - basic | $ | 0.29 | $ | 0.22 | $ | 0.75 | $ | (0.19 | ) | ||||||

| Common - diluted | 0.29 | 0.21 | 0.75 | (0.19 | ) | ||||||||||

| Weighted average limited partner units outstanding: | |||||||||||||||

| Common - basic | 394 | 341 | 378 | 324 | |||||||||||

| Common - diluted | 395 | 346 | 381 | 324 | |||||||||||

| Cash distributions declared per limited partner common unit | $ | 0.5875 | $ | 0.5150 | $ | 1.6900 | $ | 1.5300 | |||||||

(1) The accompanying notes are an integral partnine months ended September 30, 2021 and September 30, 2020 include $6 million and $1,264 million of these consolidated financial statements.impairment expense, respectively.

| (In millions) | September 30, 2017 | December 31, 2016 | |||||

| Assets | |||||||

| Current assets: | |||||||

| Cash and cash equivalents | $ | 3 | $ | 234 | |||

| Receivables, net | 320 | 299 | |||||

| Receivables - related parties | 152 | 247 | |||||

| Inventories | 64 | 55 | |||||

| Other current assets | 32 | 33 | |||||

| Total current assets | 571 | 868 | |||||

| Equity method investments | 3,997 | 2,471 | |||||

| Property, plant and equipment, net | 11,922 | 11,408 | |||||

| Intangibles, net | 463 | 492 | |||||

| Goodwill | 2,245 | 2,245 | |||||

| Long-term receivables - related parties | 18 | 11 | |||||

| Other noncurrent assets | 22 | 14 | |||||

| Total assets | $ | 19,238 | $ | 17,509 | |||

| Liabilities | |||||||

| Current liabilities: | |||||||

| Accounts payable | $ | 152 | $ | 140 | |||

| Accrued liabilities | 202 | 232 | |||||

| Payables - related parties | 317 | 87 | |||||

| Deferred revenue | 3 | 2 | |||||

| Deferred revenue - related parties | 42 | 38 | |||||

| Accrued property, plant and equipment | 183 | 146 | |||||

| Accrued taxes | 44 | 38 | |||||

| Accrued interest payable | 64 | 53 | |||||

| Other current liabilities | 41 | 27 | |||||

| Total current liabilities | 1,048 | 763 | |||||

| Long-term deferred revenue | 34 | 12 | |||||

| Long-term deferred revenue - related parties | 40 | 19 | |||||

| Long-term debt | 6,848 | 4,422 | |||||

| Deferred income taxes | 7 | 6 | |||||

| Deferred credits and other liabilities | 175 | 177 | |||||

| Total liabilities | 8,152 | 5,399 | |||||

| Commitments and contingencies (see Note 17) | |||||||

| Redeemable preferred units | 1,000 | 1,000 | |||||

| Equity | |||||||

| Common unitholders - public (289 million and 271 million units issued and outstanding) | 8,457 | 8,086 | |||||

| Class B unitholders (0 million and 4 million units issued and outstanding) | — | 133 | |||||

| Common unitholder - MPC (95 million and 86 million units issued and outstanding) | 1,302 | 1,069 | |||||

| Common unitholder - GP (23 million and 0 units issued and outstanding) | 822 | — | |||||

| General partner - MPC (8 million and 7 million units issued and outstanding) | (626 | ) | 1,013 | ||||

| Equity of Predecessor | — | 791 | |||||

| Accumulated other comprehensive loss | (14 | ) | — | ||||

| Total MPLX LP partners’ capital | 9,941 | 11,092 | |||||

| Noncontrolling interests | 145 | 18 | |||||

| Total equity | 10,086 | 11,110 | |||||

| Total liabilities, preferred units and equity | $ | 19,238 | $ | 17,509 | |||

The accompanying notes are an integral part of these consolidated financial statements.

3

MPLX LP

Consolidated Statements of Cash FlowsComprehensive Income (Unaudited)

| Nine Months Ended September 30, | |||||||

| (In millions) | 2017 | 2016(1) | |||||

| (Decrease) increase in cash and cash equivalents | |||||||

| Operating activities: | |||||||

| Net income | $ | 595 | $ | 252 | |||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

| Amortization of deferred financing costs | 38 | 34 | |||||

| Depreciation and amortization | 515 | 438 | |||||

| Impairment expense | — | 130 | |||||

| Deferred income taxes | 2 | (16 | ) | ||||

| Asset retirement expenditures | (2 | ) | (4 | ) | |||

| Gain on disposal of assets | (1 | ) | (1 | ) | |||

| (Income) loss from equity method investments | (29 | ) | 72 | ||||

| Distributions from unconsolidated affiliates | 136 | 111 | |||||

| Changes in: | |||||||

| Current receivables | (20 | ) | (43 | ) | |||

| Inventories | (3 | ) | (4 | ) | |||

| Fair value of derivatives | (3 | ) | 28 | ||||

| Current accounts payable and accrued liabilities | 6 | 64 | |||||

| Receivables from / liabilities to related parties | 61 | (104 | ) | ||||

| All other, net | 43 | 18 | |||||

| Net cash provided by operating activities | 1,338 | 975 | |||||

| Investing activities: | |||||||

| Additions to property, plant and equipment | (1,004 | ) | (943 | ) | |||

| Acquisitions, net of cash acquired | (249 | ) | — | ||||

| Disposal of assets | 4 | — | |||||

| Investments - net related party loans | 80 | 103 | |||||

| Investments in unconsolidated affiliates | (690 | ) | (56 | ) | |||

| Distributions from unconsolidated affiliates - return of capital | 24 | — | |||||

| All other, net | (2 | ) | 4 | ||||

| Net cash used in investing activities | (1,837 | ) | (892 | ) | |||

| Financing activities: | |||||||

| Long-term debt - borrowings | 2,661 | 434 | |||||

| - repayments | (251 | ) | (1,312 | ) | |||

| Related party debt - borrowings | 829 | 2,215 | |||||

| - repayments | (627 | ) | (2,223 | ) | |||

| Debt issuance costs | (25 | ) | — | ||||

| Net proceeds from equity offerings | 483 | 510 | |||||

| Issuance of redeemable preferred units | — | 984 | |||||

| Distribution to MPC for acquisition | (1,931 | ) | — | ||||

| Distributions to preferred unitholders | (49 | ) | (9 | ) | |||

| Distributions to unitholders and general partner | (800 | ) | (612 | ) | |||

| Distributions to noncontrolling interests | (4 | ) | (3 | ) | |||

| Contributions from noncontrolling interests | 128 | 4 | |||||

| Consideration payment to Class B unitholders | (25 | ) | (25 | ) | |||

| All other, net | (8 | ) | (2 | ) | |||

| Contribution from MPC | — | 225 | |||||

| Distributions to MPC from Predecessor | (113 | ) | (104 | ) | |||

| Net cash provided by financing activities | 268 | 82 | |||||

| Net (decrease) increase in cash and cash equivalents | (231 | ) | 165 | ||||

| Cash and cash equivalents at beginning of period | 234 | 43 | |||||

| Cash and cash equivalents at end of period | $ | 3 | $ | 208 | |||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||||||||

| (In millions) | 2021 | 2020 | 2021 | 2020 | |||||||||||||||||||||||||

| Net income/(loss) | $ | 811 | $ | 674 | $ | 2,274 | $ | (1,387) | |||||||||||||||||||||

| Other comprehensive income/(loss), net of tax: | |||||||||||||||||||||||||||||

| Remeasurements of pension and other postretirement benefits related to equity method investments, net of tax | — | — | (2) | (1) | |||||||||||||||||||||||||

| Comprehensive income/(loss) | 811 | 674 | 2,272 | (1,388) | |||||||||||||||||||||||||

| Less comprehensive income attributable to: | |||||||||||||||||||||||||||||

| Noncontrolling interests | 9 | 9 | 27 | 24 | |||||||||||||||||||||||||

| Comprehensive income/(loss) attributable to MPLX LP | $ | 802 | $ | 665 | $ | 2,245 | $ | (1,412) | |||||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

MPLX LP

Consolidated Statements of EquityBalance Sheets (Unaudited)

| (In millions) | September 30, 2021 | December 31, 2020 | |||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | 39 | $ | 15 | |||||||

| Receivables, net | 617 | 452 | |||||||||

| Current assets - related parties | 645 | 677 | |||||||||

| Inventories | 141 | 118 | |||||||||

| Assets held for sale | 20 | 188 | |||||||||

| Other current assets | 54 | 65 | |||||||||

| Total current assets | 1,516 | 1,515 | |||||||||

| Equity method investments | 4,001 | 4,036 | |||||||||

| Property, plant and equipment, net | 20,158 | 21,218 | |||||||||

| Intangibles, net | 864 | 959 | |||||||||

| Goodwill | 7,657 | 7,657 | |||||||||

| Right of use assets, net | 282 | 309 | |||||||||

| Noncurrent assets - related parties | 1,160 | 672 | |||||||||

| Other noncurrent assets | 61 | 48 | |||||||||

| Total assets | 35,699 | 36,414 | |||||||||

| Liabilities | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | 177 | 152 | |||||||||

| Accrued liabilities | 332 | 194 | |||||||||

| Current liabilities - related parties | 1,706 | 356 | |||||||||

| Accrued property, plant and equipment | 66 | 84 | |||||||||

| Long-term debt due within one year | 1 | 764 | |||||||||

| Accrued interest payable | 188 | 222 | |||||||||

| Operating lease liabilities | 61 | 63 | |||||||||

| Liabilities held for sale | — | 101 | |||||||||

| Other current liabilities | 190 | 150 | |||||||||

| Total current liabilities | 2,721 | 2,086 | |||||||||

| Long-term deferred revenue | 366 | 314 | |||||||||

| Long-term liabilities - related parties | 297 | 283 | |||||||||

| Long-term debt | 18,253 | 19,375 | |||||||||

| Deferred income taxes | 11 | 12 | |||||||||

| Long-term operating lease liabilities | 220 | 244 | |||||||||

| Deferred credits and other liabilities | 155 | 115 | |||||||||

| Total liabilities | 22,023 | 22,429 | |||||||||

| Commitments and contingencies (see Note 19) | 0 | 0 | |||||||||

| Series A preferred units | 986 | 968 | |||||||||

| Equity | |||||||||||

| Common unitholders - public (374 million and 391 million units issued and outstanding) | 8,919 | 9,384 | |||||||||

| Common unitholders - MPC (647 million and 647 million units issued and outstanding) | 2,944 | 2,792 | |||||||||

| Series B preferred units (.6 million and .6 million units issued and outstanding) | 601 | 611 | |||||||||

| Accumulated other comprehensive loss | (17) | (15) | |||||||||

| Total MPLX LP partners’ capital | 12,447 | 12,772 | |||||||||

| Noncontrolling interests | 243 | 245 | |||||||||

| Total equity | 12,690 | 13,017 | |||||||||

| Total liabilities, preferred units and equity | $ | 35,699 | $ | 36,414 | |||||||

| Partnership | |||||||||||||||||||||||||||||||||||

| (In millions) | Common Unit-holders Public | Class B Unit-holders Public | Common Unit-holder MPC | Common Unit-holder GP | General Partner MPC | Accumulated Other Comprehensive Loss | Non-controlling Interests | Equity of Predecessor(1) | Total | ||||||||||||||||||||||||||

| Balance at December 31, 2015 | $ | 7,691 | $ | 266 | $ | 465 | $ | — | $ | 819 | $ | — | $ | 13 | $ | 692 | $ | 9,946 | |||||||||||||||||

| Distributions to MPC from Predecessor | — | — | — | — | — | — | — | (104 | ) | (104 | ) | ||||||||||||||||||||||||

| Contribution from MPC | — | — | 84 | — | 141 | — | — | — | 225 | ||||||||||||||||||||||||||

| Contribution of MarkWest Hydrocarbon from MPC | — | — | — | — | (188 | ) | — | — | — | (188 | ) | ||||||||||||||||||||||||

| Distribution of MarkWest Hydrocarbon to MPC | — | — | — | — | 565 | — | — | — | 565 | ||||||||||||||||||||||||||

| Issuance of units under ATM Program | 499 | — | — | — | 11 | — | — | — | 510 | ||||||||||||||||||||||||||

| Net (loss) income | (51 | ) | — | (10 | ) | — | 136 | — | 3 | 149 | 227 | ||||||||||||||||||||||||

| Allocation of MPC's net investment at acquisition | — | — | 669 | — | (337 | ) | — | — | (332 | ) | — | ||||||||||||||||||||||||

| Distributions to unitholders and general partner | (378 | ) | — | (98 | ) | — | (136 | ) | — | — | — | (612 | ) | ||||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | (3 | ) | — | (3 | ) | ||||||||||||||||||||||||

| Contributions from noncontrolling interests | — | — | — | — | — | — | 4 | — | 4 | ||||||||||||||||||||||||||

| Class B unit conversion | 133 | (133 | ) | — | — | — | — | — | — | — | |||||||||||||||||||||||||

| Non-cash contribution from MPC | — | — | — | — | — | — | — | 334 | 334 | ||||||||||||||||||||||||||

| Equity-based compensation | 6 | — | — | — | — | — | — | — | 6 | ||||||||||||||||||||||||||

| Deferred income tax impact from changes in equity | (2 | ) | — | (13 | ) | — | (2 | ) | — | — | — | (17 | ) | ||||||||||||||||||||||

| Balance at September 30, 2016 | $ | 7,898 | $ | 133 | $ | 1,097 | $ | — | $ | 1,009 | $ | — | $ | 17 | $ | 739 | $ | 10,893 | |||||||||||||||||

| Balance at December 31, 2016 | $ | 8,086 | $ | 133 | $ | 1,069 | $ | — | $ | 1,013 | $ | — | $ | 18 | $ | 791 | $ | 11,110 | |||||||||||||||||

| Distributions to MPC from Predecessor | — | — | — | — | — | — | — | (113 | ) | (113 | ) | ||||||||||||||||||||||||

| Distributions of cash received from Joint-Interest Acquisition entities to MPC | — | — | — | — | (13 | ) | — | — | — | (13 | ) | ||||||||||||||||||||||||

| Issuance of units under ATM Program | 473 | — | — | — | 10 | — | — | — | 483 | ||||||||||||||||||||||||||

| Net income | 212 | — | 68 | 5 | 222 | — | 3 | 36 | 546 | ||||||||||||||||||||||||||

| Contribution from MPC | — | — | — | — | — | (14 | ) | — | 689 | 675 | |||||||||||||||||||||||||

| Allocation of MPC's net investment at acquisition | — | — | 845 | 824 | (266 | ) | — | — | (1,403 | ) | — | ||||||||||||||||||||||||

| Distribution to MPC for acquisitions | — | — | (537 | ) | — | (1,394 | ) | — | — | — | (1,931 | ) | |||||||||||||||||||||||

| Distributions to unitholders and general partner | (452 | ) | — | (143 | ) | (7 | ) | (198 | ) | — | — | — | (800 | ) | |||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | (4 | ) | — | (4 | ) | ||||||||||||||||||||||||

| Contributions from noncontrolling interests | — | — | — | — | — | — | 128 | — | 128 | ||||||||||||||||||||||||||

| Class B unit conversion | 133 | (133 | ) | — | — | — | — | — | — | — | |||||||||||||||||||||||||

| Equity-based compensation | 5 | — | — | — | — | — | — | — | 5 | ||||||||||||||||||||||||||

| Balance at September 30, 2017 | $ | 8,457 | $ | — | $ | 1,302 | $ | 822 | $ | (626 | ) | $ | (14 | ) | $ | 145 | $ | — | $ | 10,086 | |||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

5

MPLX LP

Consolidated Statements of Cash Flows (Unaudited)

| Nine Months Ended September 30, | |||||||||||

| (In millions) | 2021 | 2020 | |||||||||

| Increase/(decrease) in cash, cash equivalents and restricted cash | |||||||||||

| Operating activities: | |||||||||||

| Net income/(loss) | $ | 2,274 | $ | (1,387) | |||||||

| Adjustments to reconcile net income/(loss) to net cash provided by operating activities: | |||||||||||

| Amortization of deferred financing costs | 53 | 44 | |||||||||

| Depreciation and amortization | 971 | 992 | |||||||||

| Impairment expense | 42 | 2,165 | |||||||||

| Deferred income taxes | (1) | (1) | |||||||||

| Loss on disposal of assets | 4 | 1 | |||||||||

(Income)/loss from equity method investments(1) | (228) | 1,012 | |||||||||

| Distributions from unconsolidated affiliates | 361 | 350 | |||||||||

| Changes in: | |||||||||||

| Current receivables | (162) | 69 | |||||||||

| Inventories | (22) | (8) | |||||||||

| Fair value of derivatives | 41 | 1 | |||||||||

| Current accounts payable and accrued liabilities | 166 | (27) | |||||||||

| Current assets/current liabilities - related parties | 94 | 36 | |||||||||

| Right of use assets/operating lease liabilities | 2 | (2) | |||||||||

| Deferred revenue | 65 | 85 | |||||||||

| All other, net | 11 | 6 | |||||||||

| Net cash provided by operating activities | 3,671 | 3,336 | |||||||||

| Investing activities: | |||||||||||

| Additions to property, plant and equipment | (374) | (982) | |||||||||

| Disposal of assets | 77 | 54 | |||||||||

| Investments in unconsolidated affiliates | (116) | (244) | |||||||||

| Distributions from unconsolidated affiliates - return of capital | 36 | 112 | |||||||||

| Net cash used in investing activities | (377) | (1,060) | |||||||||

| Financing activities: | |||||||||||

| Long-term debt - borrowings | 3,000 | 5,990 | |||||||||

| - repayments | (4,946) | (5,372) | |||||||||

| Related party debt - borrowings | 6,571 | 4,870 | |||||||||

| - repayments | (5,201) | (5,464) | |||||||||

| Debt issuance costs | — | (23) | |||||||||

| Unit repurchases | (465) | — | |||||||||

| Distributions to noncontrolling interests | (29) | (26) | |||||||||

| Distributions to Series A preferred unitholders | (61) | (61) | |||||||||

| Distributions to Series B preferred unitholders | (41) | (41) | |||||||||

| Distributions to unitholders and general partner | (2,126) | (2,162) | |||||||||

| Contributions from MPC | 31 | 34 | |||||||||

| All other, net | (3) | (8) | |||||||||

| Net cash used in financing activities | (3,270) | (2,263) | |||||||||

| Net increase in cash, cash equivalents and restricted cash | 24 | 13 | |||||||||

| Cash, cash equivalents and restricted cash at beginning of period | 15 | 15 | |||||||||

| Cash, cash equivalents and restricted cash at end of period | $ | 39 | $ | 28 | |||||||

(1) The nine months ended September 30, 2021 and September 30, 2020 include $6 million and $1,264 million of impairment expense, respectively.

The accompanying notes are an integral part of these consolidated financial statements.

6

MPLX LP

Consolidated Statements of Equity (Unaudited)

| Partnership | |||||||||||||||||||||||||||||||||||||||||

| (In millions) | Common Unit-holders Public | Common Unit-holder MPC | Series B Preferred Unit-holders | Accumulated Other Comprehensive Loss | Non-controlling Interests | Total | |||||||||||||||||||||||||||||||||||

| Balance at December 31, 2019 | $ | 10,800 | $ | 4,968 | $ | 611 | $ | (15) | $ | 249 | $ | 16,613 | |||||||||||||||||||||||||||||

| Net (loss)/income (excludes amounts attributable to Series A preferred units) | (1,022) | (1,733) | 11 | — | 8 | (2,736) | |||||||||||||||||||||||||||||||||||

| Distributions to: | |||||||||||||||||||||||||||||||||||||||||

| Unitholders | (271) | (446) | (21) | — | — | (738) | |||||||||||||||||||||||||||||||||||

| Noncontrolling interests | — | — | — | — | (9) | (9) | |||||||||||||||||||||||||||||||||||

| Contributions from: | |||||||||||||||||||||||||||||||||||||||||

| MPC | — | 225 | — | — | — | 225 | |||||||||||||||||||||||||||||||||||

| Other | 2 | — | — | (1) | — | 1 | |||||||||||||||||||||||||||||||||||

| Balance at March 31, 2020 | 9,509 | 3,014 | 601 | (16) | 248 | 13,356 | |||||||||||||||||||||||||||||||||||

| Net income (excludes amounts attributable to Series A preferred units) | 229 | 388 | 10 | — | 7 | 634 | |||||||||||||||||||||||||||||||||||

| Distributions to: | |||||||||||||||||||||||||||||||||||||||||

| Unitholders | (270) | (458) | — | — | — | (728) | |||||||||||||||||||||||||||||||||||

| Noncontrolling interests | — | — | — | — | (8) | (8) | |||||||||||||||||||||||||||||||||||

| Contributions from: | |||||||||||||||||||||||||||||||||||||||||

| MPC | — | 6 | — | — | — | 6 | |||||||||||||||||||||||||||||||||||

| Other | 1 | 1 | — | — | — | 2 | |||||||||||||||||||||||||||||||||||

| Balance at June 30, 2020 | 9,469 | 2,951 | 611 | (16) | 247 | 13,262 | |||||||||||||||||||||||||||||||||||

| Net income (excludes amounts attributable to Series A preferred units) | 236 | 399 | 10 | — | 9 | 654 | |||||||||||||||||||||||||||||||||||

| Distributions to: | |||||||||||||||||||||||||||||||||||||||||

| Unitholders | (271) | (445) | (20) | — | — | (736) | |||||||||||||||||||||||||||||||||||

| Noncontrolling interests | — | — | — | — | (9) | (9) | |||||||||||||||||||||||||||||||||||

| Contributions from: | |||||||||||||||||||||||||||||||||||||||||

| MPC | — | 13 | — | — | — | 13 | |||||||||||||||||||||||||||||||||||

| Wholesale Exchange | — | (90) | — | — | — | (90) | |||||||||||||||||||||||||||||||||||

| Other | 2 | (1) | — | — | — | 1 | |||||||||||||||||||||||||||||||||||

| Balance at September 30, 2020 | $ | 9,436 | $ | 2,827 | $ | 601 | $ | (16) | $ | 247 | $ | 13,095 | |||||||||||||||||||||||||||||

| The accompanying notes are an integral part of these consolidated financial statements. | |||||||||||||||||||||||||||||||||||||||||

7

| Partnership | |||||||||||||||||||||||||||||||||||||||||

| (In millions) | Common Unit-holders Public | Common Unit-holder MPC | Series B Preferred Unit-holders | Accumulated Other Comprehensive Loss | Non-controlling Interests | Total | |||||||||||||||||||||||||||||||||||

| Balance at December 31, 2020 | $ | 9,384 | $ | 2,792 | $ | 611 | $ | (15) | $ | 245 | $ | 13,017 | |||||||||||||||||||||||||||||

| Net income (excludes amounts attributable to Series A preferred units) | 266 | 443 | 11 | — | 9 | 729 | |||||||||||||||||||||||||||||||||||

| Unit Repurchases | (155) | — | — | — | — | (155) | |||||||||||||||||||||||||||||||||||

| Distributions to: | |||||||||||||||||||||||||||||||||||||||||

| Unitholders | (269) | (445) | (21) | — | — | (735) | |||||||||||||||||||||||||||||||||||

| Noncontrolling interests | — | — | — | — | (10) | (10) | |||||||||||||||||||||||||||||||||||

| Contributions from: | |||||||||||||||||||||||||||||||||||||||||

| MPC | — | 7 | — | — | — | 7 | |||||||||||||||||||||||||||||||||||

| Other | — | (1) | — | (2) | — | (3) | |||||||||||||||||||||||||||||||||||

| Balance at March 31, 2021 | 9,226 | 2,796 | 601 | (17) | 244 | 12,850 | |||||||||||||||||||||||||||||||||||

| Net income (excludes amounts attributable to Series A preferred units) | 251 | 423 | 10 | — | 9 | 693 | |||||||||||||||||||||||||||||||||||

| Unit Repurchases | (155) | — | — | — | — | (155) | |||||||||||||||||||||||||||||||||||

| Distributions to: | |||||||||||||||||||||||||||||||||||||||||

| Unitholders | (262) | (445) | — | — | — | (707) | |||||||||||||||||||||||||||||||||||

| Noncontrolling interests | — | — | — | — | (10) | (10) | |||||||||||||||||||||||||||||||||||

| Contributions from: | |||||||||||||||||||||||||||||||||||||||||

| MPC | — | 122 | — | — | — | 122 | |||||||||||||||||||||||||||||||||||

| Other | 1 | 1 | — | — | — | 2 | |||||||||||||||||||||||||||||||||||

| Balance at June 30, 2021 | 9,061 | 2,897 | 611 | (17) | 243 | 12,795 | |||||||||||||||||||||||||||||||||||

| Net income (excludes amounts attributable to Series A preferred units) | 278 | 476 | 10 | — | 9 | 773 | |||||||||||||||||||||||||||||||||||

| Unit Repurchases | (160) | — | — | — | — | (160) | |||||||||||||||||||||||||||||||||||

| Distributions to: | |||||||||||||||||||||||||||||||||||||||||

| Unitholders | (261) | (445) | (20) | — | — | (726) | |||||||||||||||||||||||||||||||||||

| Noncontrolling interests | — | — | — | — | (9) | (9) | |||||||||||||||||||||||||||||||||||

| Contributions from: | |||||||||||||||||||||||||||||||||||||||||

| MPC | — | 16 | — | — | — | 16 | |||||||||||||||||||||||||||||||||||

| Other | 1 | — | — | — | — | 1 | |||||||||||||||||||||||||||||||||||

| Balance at September 30, 2021 | $ | 8,919 | $ | 2,944 | $ | 601 | $ | (17) | $ | 243 | $ | 12,690 | |||||||||||||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

8

Notes to Consolidated Financial Statements (Unaudited)

1. Description of the Business and Basis of Presentation

Description of the Business – MPLX LP is a diversified, growth-orientedlarge-cap master limited partnership formed by Marathon Petroleum Corporation.Corporation that owns and operates midstream energy infrastructure and logistics assets, and provides fuels distribution services. References in this report to “MPLX LP,” “MPLX,” “the Partnership,” “we,” “ours,” “us,” or like terms refer to MPLX LP and its subsidiaries (collectively, the “Partnership”) are engaged in the gathering, processing and transportation of natural gas; the gathering, transportation, fractionation, storage and marketing of NGLs; and the transportation, storage and distribution of crude oil and refined petroleum products, principally for our sponsor.subsidiaries. References to “MPC” refer collectively to Marathon Petroleum Corporation as our sponsor and its subsidiaries, other than the Partnership. We are engaged in the transportation, storage, marketing and distribution of crude oil, asphalt and refined petroleum products; the gathering, processing and transportation of natural gas; and the gathering, transportation, fractionation, storage and marketing of NGLs. MPLX’s principal executive office is located in Findlay, Ohio.

In the equity method. The Partnership’s investmentssecond quarter of 2021, we recognized impairment expense of $42 million within our G&P segment related to our continued emphasis on portfolio optimization with the anticipated divestiture of several non-core assets and the closure of other non-core assets.

During the first quarter of 2020, the overall deterioration in a VIEthe economy and the environment in which the Partnership exercises significant influence but does not controlMPLX and is not the primary beneficiary are also accounted for using the equity method.

| (In millions) | Impairment | Footnote Reference | ||||||||||||

| Goodwill | $ | 1,814 | 12 | |||||||||||

| Equity method investments | 1,264 | 4 | ||||||||||||

| Intangibles, net | 177 | 12 | ||||||||||||

| Property, plant and equipment, net | 174 | 11 | ||||||||||||

| Total impairments | $ | 3,429 | ||||||||||||

Basis of net income attributable to MPLX LP for purposes of calculating net income per limited partner unit is described in Note 6.

Presentation – The accompanying interim consolidated financial statements are unaudited; however, in the opinion of the Partnership’sMPLX’s management, these statements reflect all adjustments necessary for a fair statement of the results for the periods reported. All such adjustments are of a normal, recurring nature unless otherwise disclosed. These interim consolidated financial statements, including the notes, have been prepared in accordance with the rules and regulations of the SEC applicable to interim period financial statements and do not include all of the information and disclosures required by GAAP for complete financial statements. Certain amounts in prior years have been reclassified to conform to current year presentation.

These interim consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto included in theour Annual Report on Form 10-K for the year ended December 31, 2016, as updated by our Current Report on Form 8-K filed on May 1, 2017.2020. The results of operations for the three and nine months ended September 30, 20172021 are not necessarily indicative of the results to be expected for the full year.

MPLX’s consolidated financial statements include all majority-owned and controlled subsidiaries. For non-wholly owned consolidated subsidiaries, the interests owned by third parties have been recorded as “Noncontrolling interests” on the accompanying Consolidated Balance Sheets. Intercompany investments, accounts and transactions have been eliminated.

9

MPLX’s investments in which MPLX exercises significant influence but does not control and does not have a controlling financial interest are accounted for using the equity method. MPLX’s investments in VIEs in which MPLX exercises significant influence but does not control and is not the primary beneficiary are also accounted for using the equity method.

2. Accounting Standards

Recently Adopted

3. Acquisitions and Dispositions

Sale of Javelina Assets and Liabilities

On February 12, 2021, MarkWest Energy Operating Company, L.L.C., (“MarkWest Energy”) a wholly owned subsidiary of MPLX, completed the consolidated financial statements.

On September 1, 2017, the PartnershipJuly 31, 2020, MPLX entered into a Membership Interests and Shares ContributionsRedemption Agreement (the “September 2017 Contributions“Redemption Agreement”) with MPLX GP LLCWestern Refining Southwest, Inc. (now known as Western Refining Southwest LLC) (“MPLX GP”WRSW”), MPLX Logistics Holdings LLC (“MPLX Logistics”), MPLX Holdings Inc. (“MPLX Holdings”) and MPC Investment LLC (“MPC Investment”), each a wholly-ownedwholly owned subsidiary of MPC, whereby the Partnershippursuant to which MPLX agreed to acquire certain ownership interests in joint venture entities indirectly held by MPC. Pursuanttransfer to the September 2017 Contributions Agreement, MPC Investment agreed to contribute:WRSW all of the outstanding membership interests in Western Refining Wholesale, LLC (“WRW”) in exchange for the redemption of Lincoln Pipeline LLC, which holds a 35 percent interest in Illinois Extension Pipeline Company, L.L.C. (“Illinois Extension”); allMPLX common units held by WRSW. The transaction effected the transfer to MPC of the membership interestsWestern wholesale distribution business that MPLX acquired as a result of MPL Louisiana Holdings LLC, which holds a 40.7 percent interest in LOOP LLCits acquisition of Andeavor Logistics LP (“LOOP”ANDX”); a 58.52 percent interest in LOCAP LLC (“LOCAP”); and a 24.51 percent interest in Explorer Pipeline Company (“Explorer”), through a series. Per the terms of intercompany contributions to the Partnership for an agreed upon purchase price of approximately $420 million in cash and equity consideration valued at approximately $630 million for total consideration of $1.05 billion (collectively, the “Joint-Interest Acquisition”Redemption Agreement, MPLX redeemed 18,582,088 common units (the “Redeemed Units”). held by WRSW on July 31, 2020. The number of common units representing the equity considerationRedeemed Units was then determinedcalculated by dividing the contribution amountWRW’s aggregate valuation of $340 million by the simple average of the ten day trading volume weighted average NYSE priceprices of aan MPLX common unit for the ten trading days ending at market close on August 31, 2017.July 27, 2020. MPLX canceled the Redeemed Units immediately following the Wholesale Exchange. The faircarrying value of the common and general partner units issuednet assets of WRW transferred to MPC was approximately $653$90 million based on the closing common unit price as of September 1, 2017, asJuly 31, 2020, resulting in $250 million being recorded onto “Common Unit-holder MPC” within the Consolidated Statements of Equity, for a total purchase price of $1.07 billion. The equity issued consisted of: (i) 13,719,017 common units to MPLX GP, (ii) 3,350,893 common units to MPLX Logistics and (iii) 1,441,224 common units to MPLX Holdings. The Partnership also issued 377,778 general partner units to MPLX GP in order to maintain its two percent general partner interest (“GP Interest”) innetted against the Partnership.

10

4. Investments and consisted of (i) 9,197,900 common units to MPLX GP, (ii) 2,630,427 common units to MPLX Logistics and (iii) 1,132,049 common units to MPLX Holdings. The Partnership also issued 264,497 general partner units to MPLX GP in order to maintain its two percent GP Interest in the Partnership. MPC agreed to waive two-thirds of the first quarter 2017 distributions on the common units issued in connection with the Transaction. As a result of this waiver, MPC did not receive two-thirds of the general partner distributions or IDRs that would have otherwise accrued on such common units with respect to the first quarter 2017 distributions. The value of these waived distributions was $6 million.Noncontrolling Interests

| Three Months Ended September 30, 2016 | |||||||||||||||||||

| (In millions, except per unit data) | MPLX LP (Previously Reported) | HST/WHC | MPLXT | Eliminations(1) | MPLX LP (Currently Reported) | ||||||||||||||

| Revenues and other income: | |||||||||||||||||||

| Service revenue | $ | 250 | $ | — | $ | — | $ | — | $ | 250 | |||||||||

| Service revenue - related parties | 153 | 28 | 72 | — | 253 | ||||||||||||||

| Rental income | 77 | — | — | — | 77 | ||||||||||||||

| Rental income - related parties | 29 | 13 | 26 | — | 68 | ||||||||||||||

| Product sales | 157 | — | — | — | 157 | ||||||||||||||

| Product sales - related parties | 2 | — | — | — | 2 | ||||||||||||||

| Income from equity method investments | 6 | — | — | — | 6 | ||||||||||||||

| Gain on sale of assets | 1 | — | — | — | 1 | ||||||||||||||

| Other income | 2 | — | — | — | 2 | ||||||||||||||

| Other income - related parties | 26 | — | — | (4 | ) | 22 | |||||||||||||

| Total revenues and other income | 703 | 41 | 98 | (4 | ) | 838 | |||||||||||||

| Costs and expenses: | |||||||||||||||||||

| Cost of revenues (excludes items below) | 90 | 10 | 22 | — | 122 | ||||||||||||||

| Purchased product costs | 117 | — | — | — | 117 | ||||||||||||||

| Rental cost of sales | 11 | 2 | — | — | 13 | ||||||||||||||

| Rental cost of sales - related parties | — | 1 | — | (1 | ) | — | |||||||||||||

| Purchases - related parties | 84 | 4 | 24 | (3 | ) | 109 | |||||||||||||

| Depreciation and amortization | 138 | 4 | 9 | — | 151 | ||||||||||||||

| General and administrative expenses | 46 | 2 | 8 | — | 56 | ||||||||||||||

| Other taxes | 10 | — | 2 | — | 12 | ||||||||||||||

| Total costs and expenses | 496 | 23 | 65 | (4 | ) | 580 | |||||||||||||

| Income from operations | 207 | 18 | 33 | — | 258 | ||||||||||||||

| Interest expense (net of amounts capitalized) | 51 | — | — | — | 51 | ||||||||||||||

| Other financial costs | 13 | — | — | — | 13 | ||||||||||||||

| Income before income taxes | 143 | 18 | 33 | — | 194 | ||||||||||||||

| Net income | 143 | 18 | 33 | — | 194 | ||||||||||||||

| Less: Net income attributable to noncontrolling interests | 2 | — | — | — | 2 | ||||||||||||||

| Less: Net income attributable to Predecessor | — | 18 | 33 | — | 51 | ||||||||||||||

| Net income attributable to MPLX LP | 141 | — | — | — | 141 | ||||||||||||||

| Less: Preferred unit distributions | 16 | — | — | — | 16 | ||||||||||||||

| Less: General partner’s interest in net income attributable to MPLX LP | 51 | — | — | — | 51 | ||||||||||||||

| Limited partners’ interest in net income attributable to MPLX LP | $ | 74 | $ | — | $ | — | $ | — | $ | 74 | |||||||||

| Nine Months Ended September 30, 2016 | |||||||||||||||||||

| (In millions, except per unit data) | MPLX LP (Previously Reported) | HST/WHC | MPLXT | Eliminations(1) | MPLX LP (Currently Reported) | ||||||||||||||

| Revenues and other income: | |||||||||||||||||||

| Service revenue | $ | 712 | $ | — | $ | — | $ | — | $ | 712 | |||||||||

| Service revenue - related parties | 448 | 82 | 146 | — | 676 | ||||||||||||||

| Rental income | 218 | — | — | — | 218 | ||||||||||||||

| Rental income - related parties | 84 | 36 | 52 | — | 172 | ||||||||||||||

| Product sales | 394 | — | — | — | 394 | ||||||||||||||

| Product sales - related parties | 8 | — | — | — | 8 | ||||||||||||||

| Loss from equity method investments | (72 | ) | — | — | — | (72 | ) | ||||||||||||

| Gain on sale of assets | 1 | — | — | — | 1 | ||||||||||||||

| Other income | 5 | — | — | — | 5 | ||||||||||||||

| Other income - related parties | 78 | — | — | (11 | ) | 67 | |||||||||||||

| Total revenues and other income | 1,876 | 118 | 198 | (11 | ) | 2,181 | |||||||||||||

| Costs and expenses: | |||||||||||||||||||

| Cost of revenues (excludes items below) | 263 | 24 | 42 | — | 329 | ||||||||||||||

| Purchased product costs | 310 | — | — | — | 310 | ||||||||||||||

| Rental cost of sales | 39 | 3 | — | — | 42 | ||||||||||||||

| Rental cost of sales - related parties | — | 2 | — | (1 | ) | 1 | |||||||||||||

| Purchases - related parties | 238 | 13 | 45 | (10 | ) | 286 | |||||||||||||

| Depreciation and amortization | 407 | 12 | 19 | — | 438 | ||||||||||||||

| Impairment expense | 130 | — | — | — | 130 | ||||||||||||||

| General and administrative expenses | 147 | 5 | 20 | — | 172 | ||||||||||||||

| Other taxes | 32 | 2 | 3 | — | 37 | ||||||||||||||

| Total costs and expenses | 1,566 | 61 | 129 | (11 | ) | 1,745 | |||||||||||||

| Income from operations | 310 | 57 | 69 | — | 436 | ||||||||||||||

| Related party interest and other financial income | 1 | — | — | — | 1 | ||||||||||||||

| Interest expense (net of amounts capitalized) | 158 | — | — | — | 158 | ||||||||||||||

| Other financial costs | 37 | — | — | — | 37 | ||||||||||||||

| Income before income taxes | 114 | 57 | 69 | — | 240 | ||||||||||||||

| Benefit for income taxes | (12 | ) | — | — | — | (12 | ) | ||||||||||||

| Net income | 126 | 57 | 69 | — | 252 | ||||||||||||||

| Less: Net income attributable to noncontrolling interests | 3 | — | — | — | 3 | ||||||||||||||

| Less: Net income attributable to Predecessor | 23 | 57 | 69 | — | 149 | ||||||||||||||

| Net income attributable to MPLX LP | 100 | — | — | — | 100 | ||||||||||||||

| Less: Preferred unit distributions | 25 | — | — | — | 25 | ||||||||||||||

| Less: General partner’s interest in net income attributable to MPLX LP | 136 | — | — | — | 136 | ||||||||||||||

| Limited partners’ interest in net loss attributable to MPLX LP | $ | (61 | ) | $ | — | $ | — | $ | — | $ | (61 | ) | |||||||

The following table presents the Partnership’s previously reported unaudited Consolidated Statements of Cash Flows, retrospectively adjusted for the acquisition of HST, WHC and MPLXT:

| Nine Months Ended September 30, 2016 | |||||||||||||||

| (In millions) | MPLX LP (Previously Reported) | HST/WHC | MPLXT | MPLX LP (Currently Reported) | |||||||||||

| Increase (decrease) in cash and cash equivalents | |||||||||||||||

| Operating activities: | |||||||||||||||

| Net income | $ | 126 | $ | 57 | $ | 69 | $ | 252 | |||||||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | |||||||||||||||

| Amortization of deferred financing costs | 34 | — | — | 34 | |||||||||||

| Depreciation and amortization | 407 | 12 | 19 | 438 | |||||||||||

| Impairment expense | 130 | — | — | 130 | |||||||||||

| Deferred income taxes | (16 | ) | — | — | (16 | ) | |||||||||

| Asset retirement expenditures | (3 | ) | (1 | ) | — | (4 | ) | ||||||||

| Gain on disposal of assets | (1 | ) | — | — | (1 | ) | |||||||||

| Loss from equity method investments | 72 | — | — | 72 | |||||||||||

| Distributions from unconsolidated affiliates | 111 | — | — | 111 | |||||||||||

| Changes in: | |||||||||||||||

| Current receivables | (44 | ) | 1 | — | (43 | ) | |||||||||

| Inventories | (4 | ) | — | — | (4 | ) | |||||||||

| Fair value of derivatives | 28 | — | — | 28 | |||||||||||

| Current accounts payable and accrued liabilities | 59 | (1 | ) | 6 | 64 | ||||||||||

| Receivables from / liabilities to related parties | 15 | 3 | (122 | ) | (104 | ) | |||||||||

| All other, net | 18 | 2 | (2 | ) | 18 | ||||||||||

| Net cash provided by (used in) operating activities | 932 | 73 | (30 | ) | 975 | ||||||||||

| Investing activities: | |||||||||||||||

| Additions to property, plant and equipment | (874 | ) | (36 | ) | (33 | ) | (943 | ) | |||||||

| Investments - net related party loans | 77 | (37 | ) | 63 | 103 | ||||||||||

| Investments in unconsolidated affiliates | (56 | ) | — | — | (56 | ) | |||||||||

| All other, net | 4 | — | — | 4 | |||||||||||

| Net cash (used in) provided by investing activities | (849 | ) | (73 | ) | 30 | (892 | ) | ||||||||

| Financing activities: | |||||||||||||||

| Long-term debt - borrowings | 434 | — | — | 434 | |||||||||||

| - repayments | (1,312 | ) | — | — | (1,312 | ) | |||||||||

| Related party debt - borrowings | 2,215 | — | — | 2,215 | |||||||||||

| - repayments | (2,223 | ) | — | — | (2,223 | ) | |||||||||

| Net proceeds from equity offerings | 510 | — | — | 510 | |||||||||||

| Issuance of redeemable preferred units | 984 | — | — | 984 | |||||||||||

| Distributions to preferred unitholders | (9 | ) | — | — | (9 | ) | |||||||||

| Distributions to unitholders and general partner | (612 | ) | — | — | (612 | ) | |||||||||

| Distributions to noncontrolling interests | (3 | ) | — | — | (3 | ) | |||||||||

| Contributions from noncontrolling interests | 4 | — | — | 4 | |||||||||||

| Consideration payment to Class B unitholders | (25 | ) | — | — | (25 | ) | |||||||||

| All other, net | (2 | ) | — | — | (2 | ) | |||||||||

| Contribution from MPC | 225 | — | — | 225 | |||||||||||

| Distributions to MPC from Predecessor | (104 | ) | — | — | (104 | ) | |||||||||

| Net cash provided by financing activities | 82 | — | — | 82 | |||||||||||

| Net increase in cash and cash equivalents | 165 | — | — | 165 | |||||||||||

| Cash and cash equivalents at beginning of period | 43 | — | — | 43 | |||||||||||

| Cash and cash equivalents at end of period | $ | 208 | $ | — | $ | — | $ | 208 | |||||||

| Ownership as of | Carrying value at | ||||||||||||||||

| September 30, | September 30, | December 31, | |||||||||||||||

| (In millions, except ownership percentages) | 2021 | 2021 | 2020 | ||||||||||||||

| L&S | |||||||||||||||||

MarEn Bakken Company LLC(1) | 25% | $ | 457 | $ | 465 | ||||||||||||

| Illinois Extension Pipeline Company, L.L.C. | 35% | 253 | 254 | ||||||||||||||

| LOOP LLC | 41% | 268 | 252 | ||||||||||||||

Andeavor Logistics Rio Pipeline LLC(2) | 67% | 188 | 194 | ||||||||||||||

| Minnesota Pipe Line Company, LLC | 17% | 184 | 188 | ||||||||||||||

Whistler Pipeline LLC(2) | 38% | 146 | 185 | ||||||||||||||

| Explorer Pipeline Company | 25% | 68 | 72 | ||||||||||||||

W2W Holdings LLC(2)(3) | 50% | 66 | 72 | ||||||||||||||

Other(2) | 115 | 103 | |||||||||||||||

| Total L&S | 1,745 | 1,785 | |||||||||||||||

| G&P | |||||||||||||||||

MarkWest Utica EMG, L.L.C.(2) | 57% | 682 | 698 | ||||||||||||||

Sherwood Midstream LLC(2) | 50% | 548 | 557 | ||||||||||||||

MarkWest EMG Jefferson Dry Gas Gathering Company, L.L.C.(2) | 67% | 335 | 307 | ||||||||||||||

MarkWest Torñado GP, L.L.C.(2) | 60% | 223 | 188 | ||||||||||||||

Rendezvous Gas Services, L.L.C.(2) | 78% | 151 | 159 | ||||||||||||||

Sherwood Midstream Holdings LLC(2) | 51% | 138 | 148 | ||||||||||||||

| Centrahoma Processing LLC | 40% | 132 | 145 | ||||||||||||||

Other(2) | 47 | 49 | |||||||||||||||

| Total G&P | 2,256 | 2,251 | |||||||||||||||

| Total | $ | 4,001 | $ | 4,036 | |||||||||||||

(1) The Ozark pipeline is a 433-mile, 22-inch crude oil pipeline originatinginvestment in Cushing, Oklahoma, and terminating in Wood River, Illinois, capable of transporting approximately 230 mbpd. The Partnership accounts for the Ozark pipeline within its L&S segment.

| (In millions) | Three Months Ended September 30, 2017 | Seven Months Ended September 30, 2017 | |||||

| Revenues and other income | $ | 19 | $ | 45 | |||

| Income from operations | 6 | 17 | |||||

(2) Investments deemed to acquire a 36.75 percent indirectbe VIEs. Some investments included within “Other” have also been deemed to be VIEs.

(3) Through our ownership interest in the Bakken Pipeline system. The Partnership holds, throughW2W Holdings LLC, we have a subsidiary, a 2515 percent interest in MarEn Bakken, which equates to a 9.1875 percent indirect interest in the Bakken Pipeline system.

| Nine Months Ended September 30, 2017 | |||||||||||||||

| (In millions) | MarkWest Utica EMG | Other VIEs | Non-VIEs | Total | |||||||||||

| Revenues and other income | $ | 137 | $ | 49 | $ | 178 | $ | 364 | |||||||

| Costs and expenses | 72 | 29 | 115 | 216 | |||||||||||

| Income from operations | 65 | 20 | 63 | 148 | |||||||||||

| Net income | 65 | 19 | 28 | 112 | |||||||||||

Income from equity method investments(1) | 6 | 7 | 16 | 29 | |||||||||||

| Nine Months Ended September 30, 2016 | |||||||||||||||

| (In millions) | MarkWest Utica EMG | Other VIEs(2) | Non-VIEs | Total | |||||||||||

| Revenues and other income | $ | 165 | $ | 13 | $ | 108 | $ | 286 | |||||||

| Costs and expenses | 70 | 107 | 80 | 257 | |||||||||||

| Income (loss) from operations | 95 | (94 | ) | 28 | 29 | ||||||||||

| Net income (loss) | 94 | (94 | ) | 28 | 28 | ||||||||||

Income (loss) from equity method investments(1) | 10 | (88 | ) | 6 | (72 | ) | |||||||||

| September 30, 2017 | |||||||||||||||

| (In millions) | MarkWest Utica EMG(1) | Other VIEs | Non-VIEs | Total | |||||||||||

| Current assets | $ | 72 | $ | 47 | $ | 379 | $ | 498 | |||||||

| Noncurrent assets | 2,092 | 878 | 4,614 | 7,584 | |||||||||||

| Current liabilities | 37 | 55 | 492 | 584 | |||||||||||

| Noncurrent liabilities | 2 | 12 | 562 | 576 | |||||||||||

| December 31, 2016 | |||||||||||||||

| (In millions) | MarkWest Utica EMG(1) | Other VIEs | Non-VIEs | Total | |||||||||||

| Current assets | $ | 45 | $ | 2 | $ | 40 | $ | 87 | |||||||

| Noncurrent assets | 2,173 | 132 | 390 | 2,695 | |||||||||||

| Current liabilities | 30 | 4 | 26 | 60 | |||||||||||

| Noncurrent liabilities | 2 | 13 | — | 15 | |||||||||||

Sherwood Midstream LLC (“Sherwood Midstream”) has been deemed the primary beneficiary of Sherwood Midstream Holdings LLC (Sherwood Midstream Holdings”) due to its controlling financial interest through its authority to manage the joint venture. As a result, Sherwood Midstream consolidates Sherwood Midstream Holdings. Therefore, MPLX also reports its portion of Sherwood Midstream Holdings’ net assets as a component of its investment in MarkWest Utica EMG’s, which was $2.2 billion atSherwood Midstream. As of September 30, 2017 and December 31, 2016, is reported under the caption Equity method investments on the Consolidated Balance Sheets. The Partnership’s2021, MPLX has a 24.55 percent indirect ownership interest in Sherwood Midstream Holdings through Sherwood Midstream.

MPLX’s maximum exposure to loss as a result of its involvement with MarkWest Utica EMGequity method investments includes its equity investment, any additional capital contribution commitments and any operating expenses incurred by the subsidiary operator in excess of its compensation received for the performance of the operating services. The PartnershipMPLX did not provide any financial support to MarkWest Utica EMG that it was not contractually obligated to provide during the three and nine months ended September 30, 2017 and 2016, respectively. The Partnership receives management fee revenue for engineering and construction and administrative services for operating MarkWest Utica EMG, and is also reimbursed for personnel services (“Operational Service revenue”). Operational Service revenue is reported as Other income-related parties in the Consolidated Statements of Income. The amount of Operational Service revenue related to MarkWest Utica EMG for the three and nine months ended September 30, 2017, totaled $5 million and $13 million, respectively. The amount of Operational Service revenue related to MarkWest Utica EMG for the three and nine months ended September 30, 2016, totaled approximately $5 million and $12 million, respectively.

11

During the first quarter of 2020, we recorded an other than temporary impairment for operating Sherwood Midstream. The amountthree joint ventures in which we have an interest as discussed in Note 1. Impairment of Operational Service revenuethese investments was $1,264 million, of which $1,251 million was related to Sherwood Midstream for the threeMarkWest Utica EMG, L.L.C. and nine months ended September 30, 2017, totaled approximately $2 million and $6 million, respectively, and is reported as Other income-related parties in the Consolidated Statements of Income.

| Nine Months Ended September 30, 2021 | |||||||||||||||||

| (In millions) | VIEs | Non-VIEs | Total | ||||||||||||||

| Revenues and other income | $ | 565 | $ | 940 | $ | 1,505 | |||||||||||

| Costs and expenses | 350 | 427 | 777 | ||||||||||||||

| Income from operations | 215 | 513 | 728 | ||||||||||||||

| Net income | 172 | 449 | 621 | ||||||||||||||

Income from equity method investments(1) | $ | 120 | $ | 108 | $ | 228 | |||||||||||

| Nine Months Ended September 30, 2020 | |||||||||||||||||

| (In millions) | VIEs | Non-VIEs | Total | ||||||||||||||

| Revenues and other income | $ | 132 | $ | 933 | $ | 1,065 | |||||||||||

| Costs and expenses | 308 | 405 | 713 | ||||||||||||||

| (Loss)/income from operations | (176) | 528 | 352 | ||||||||||||||

| Net (loss)/income | (230) | 477 | 247 | ||||||||||||||

(Loss)/income from equity method investments(1) | $ | (1,138) | $ | 126 | $ | (1,012) | |||||||||||

(1) Includes impairment expense of Sherwood Midstream Holdings’ net assets$1,264 million.

Summarized balance sheet information for MPLX’s equity method investments as a component of its investment in Sherwood Midstream. As of September 30, 2017, the Partnership has a 14.7 percent indirect ownership interest in Sherwood Midstream Holdings through Sherwood Midstream.2021 and December 31, 2020 is as follows:

| September 30, 2021 | |||||||||||||||||

| (In millions) | VIEs | Non-VIEs | Total | ||||||||||||||

| Current assets | $ | 328 | $ | 444 | $ | 772 | |||||||||||

| Noncurrent assets | 7,426 | 4,907 | 12,333 | ||||||||||||||

| Current liabilities | 216 | 254 | 470 | ||||||||||||||

| Noncurrent liabilities | $ | 2,448 | $ | 873 | $ | 3,321 | |||||||||||

| December 31, 2020 | |||||||||||||||||

| (In millions) | VIEs | Non-VIEs | Total | ||||||||||||||

| Current assets | $ | 530 | $ | 318 | $ | 848 | |||||||||||

| Noncurrent assets | 6,889 | 4,997 | 11,886 | ||||||||||||||

| Current liabilities | 323 | 187 | 510 | ||||||||||||||

| Noncurrent liabilities | $ | 1,904 | $ | 830 | $ | 2,734 | |||||||||||

5. Related Party Agreements and Transactions

12

storage volumescapacity; operating and management fees; as well as reimbursements for certain direct and indirect costs. MPC has also committed to provide a fixed fee for 100 percent of crude oil, refined productsavailable capacity for boats, barges and butane.third-party chartered equipment under the marine transportation service agreement. MPLX also has a keep-whole commodity agreement with MPC under which MPC pays us a processing fee for NGLs related to keep-whole agreements and delivers shrink gas to the producers on our behalf. We pay MPC a marketing fee in exchange for assuming the commodity risk. Additionally, MPLX has obligations to MPC for services provided to MPLX by MPC under omnibus and employee services-type agreements as well as other various agreements.

MPLX is party to a loan agreement with MPC Investment a wholly-owned subsidiary of MPC.LLC (“MPC Investment”) (the “MPC Loan Agreement”). Under the terms of the agreement, MPC Investment will make a loan orextends loans to the PartnershipMPLX on a revolving basis as requested by the PartnershipMPLX and as agreed to by MPC Investment, in an amount or amounts that do not result inInvestment. The borrowing capacity of the MPC Loan Agreement is $1.5 billion aggregate principal amount of all loans outstanding exceeding $500 million at any one time. The entire unpaid principal amount ofloan agreement is scheduled to expire, and borrowings under the loan together with all accruedagreement are scheduled to mature and unpaid interest and other amounts (if any), shall become due and payable, on December 4, 2020.July 31, 2024, provided that MPC Investment may demand payment of all or any portion of the outstanding principal amount of the loan, together with all accrued and unpaid interest and other amounts (if any), at any time prior to December 4, 2020.maturity. Borrowings under the loan willMPC Loan Agreement bear interest at LIBOR plus 1.50 percent. During1.25 percent or such lower rate as would be applicable to such loans under the nine months ended September 30, 2017,MPLX Credit Agreement as discussed in Note 15. Activity on the Partnership borrowed $829 million and repaid $627 million, resultingMPC Loan Agreement was as follows:

| (In millions) | Nine Months Ended September 30, 2021 | Year Ended December 31, 2020 | |||||||||

| Borrowings | $ | 6,571 | $ | 6,264 | |||||||

| Average interest rate of borrowings | 1.345 | % | 2.278 | % | |||||||

| Repayments | $ | 5,201 | $ | 6,858 | |||||||

Outstanding balance at end of period(1) | $ | 1,370 | $ | — | |||||||

(1) Included in $202 million outstanding balance at September 30, 2017, which is included in Payables-related parties“Current liabilities - related parties” on the Consolidated Balance Sheets. Borrowings were at an average interest rate of 2.721 percent, per annum, for the nine months ended September 30, 2017. During the year ended December 31, 2016, the Partnership borrowed $2.5 billion and repaid $2.5 billion, resulting in no outstanding balance at December 31, 2016. Borrowings were at an average interest rate of 1.939 percent, per annum, for the year ended December 31, 2016. For additional information regarding the Partnership’s commercial and other agreements with MPC, see Item 1. Business in the Annual Report on Form 10-K for the year ended December 31, 2016.

Related Party TransactionsRevenue

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Service revenues | |||||||||||||||

| MPC | $ | 276 | $ | 253 | $ | 801 | $ | 676 | |||||||

| Rental income | |||||||||||||||

| MPC | $ | 70 | $ | 68 | $ | 207 | $ | 172 | |||||||

Product sales(1) | |||||||||||||||

| MPC | $ | 2 | $ | 2 | $ | 6 | $ | 8 | |||||||

Related party sales to MPC consist of crude oil and refined products pipeline and trucking transportation services based on regulated tariff rates,tariff/contracted rates; storage, terminal and fuels distribution services based on contracted ratesrates; and marine transportation services. Related party sales to MPC also includes revenue related to volume deficiency credits.

Certain product sales to MPC net to zero within the consolidated financial statements as the transactions are recorded net due to the terms of the agreements under which such product was sold. For the three and nine months ended September 30, 2021, these sales totaled $203 million and $548 million, respectively. For the three and nine months ended September 30, 2020, these sales totaled $107 million and $332 million, respectively.

MPLX also has operating agreements with MPC under which it receives a fee for operating MPC’s retained pipeline assets and a fixed annual fee for providing oversight and management services provided by HSM. Underrequired to run the Partnership’s pipeline transportationmarine business. MPLX also receives management fee revenue for engineering, construction and administrative services for operating certain of its equity method investments. These agreements are classified as “Other income - related parties” on the Consolidated Statements of Income.

Related Party Expenses

MPC charges MPLX for executive management services and certain general and administrative services that MPC provides to MPLX under the terms of our omnibus agreements (“Omnibus charges”). Omnibus charges included in “Rental cost of sales - related parties” primarily relate to services that support MPLX’s rental operations and maintenance of assets available for rent, as well as compensation expenses. Omnibus charges included in “Purchases - related parties” primarily relate to services that support MPLX’s operations and maintenance activities, as well as compensation expenses. Omnibus charges included in “General and administrative expenses” primarily relate to services that support MPLX’s executive management, accounting and human resources activities. MPLX also obtains employee services from MPC under employee services agreements if(“ESA charges”). ESA charges for personnel directly involved in or supporting operations and maintenance activities related to rental services are classified as “Rental cost of sales - related parties.” ESA charges for personnel directly involved in or supporting operations and maintenance activities related to other services are classified as “Purchases - related parties.” ESA charges for personnel involved in executive management, accounting and human resources activities are classified as “General and

13

administrative expenses.” In addition to these agreements, MPLX purchases products from MPC, makes payments to MPC in its capacity as general contractor to MPLX, and has certain lease agreements with MPC.

For the three and nine months ended September 30, 2021, “General and administrative expenses” incurred from MPC totaled $70 million and $190 million, respectively. For the three and nine months ended September 30, 2020, “General and administrative expenses” incurred from MPC totaled $63 million and $195 million, respectively.

Some charges incurred under the omnibus and ESA agreements are related to engineering services and are associated with assets under construction. These charges are added to “Property, plant and equipment, net” on the Consolidated Balance Sheets. For the three and nine months ended September 30, 2021, these charges totaled $13 million and $40 million, respectively. For the three and nine months ended September 30, 2020, these charges totaled $29 million and $80 million, respectively.

MPC has also been advancing certain strategic priorities to lay a foundation for long-term success, including plans to optimize its assets and structurally lower costs in 2021 and beyond. In 2020, MPC approved and executed an involuntary workforce reduction plan, which together with employee reductions resulting from MPC’s indefinite idling of its Martinez, California and Gallup, New Mexico refineries, affected approximately 2,050 employees. All of the employees that conduct MPLX’s business are directly employed by affiliates of MPC, and certain of those employees were affected by MPC’s workforce reductions. During the third quarter of 2020, MPLX reimbursed MPC for $36 million related to severance and employee benefits related expenses that MPC recorded in connection with its workforce reductions. There were no such costs in the first nine months of 2021.

Related Party Assets and Liabilities

Assets and liabilities with related parties appearing on the Consolidated Balance Sheets are detailed in the table below. This table identifies the various components of related party assets and liabilities, including those associated with leases (see Note 18 for additional information) and deferred revenue on minimum volume commitments. If MPC fails to transportmeet its minimum throughputcommitted volumes, during any quarter, then MPC will pay the PartnershipMPLX a deficiency payment equal tobased on the volumeterms of the deficiency multiplied by the tariff rate then in effect.agreement. The deficiency amounts received under these agreements (excluding payments received under agreements classified as sales-type leases) are recorded as Deferred revenue-related parties.“Current liabilities - related parties.” In many cases, MPC may then apply the amount of any such deficiency payments as a credit for volumes transported on the applicable pipeline system in excess of its minimum volume commitment during the following four or eight quartersin future periods under the terms of the applicable transportation services agreement. The Partnershipagreements. MPLX recognizes related party revenues for the deficiency payments when credits are used for volumes transported in excess of minimum quarterly volume commitments, whenwhere it becomes impossible to physically transport volumes necessary to utilizeis probable the creditscustomer will not use the credit in future periods or upon the expiration of the credits. The use or expiration of the credits is a decrease in Deferred revenue-related parties.

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| MPC | $ | 9 | $ | 10 | $ | 30 | $ | 36 | |||||||

| MarkWest Utica EMG | 5 | 5 | 13 | 12 | |||||||||||

| Ohio Gathering | 4 | 5 | 12 | 12 | |||||||||||

| Other | 4 | 2 | 14 | 7 | |||||||||||

| Total | $ | 22 | $ | 22 | $ | 69 | $ | 67 | |||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Purchases - related parties | $ | 17 | $ | 11 | $ | 50 | $ | 29 | |||||||

| General and administrative expenses | 9 | 11 | 28 | 33 | |||||||||||

| Total | $ | 26 | $ | 22 | $ | 78 | $ | 62 | |||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| MPC | $ | 11 | $ | 14 | $ | 33 | $ | 36 | |||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Purchases - related parties | $ | 97 | $ | 98 | $ | 280 | $ | 257 | |||||||

| General and administrative expenses | 25 | 27 | 74 | 75 | |||||||||||

| Total | $ | 122 | $ | 125 | $ | 354 | $ | 332 | |||||||

| (In millions) | September 30, 2017 | December 31, 2016 | |||||

| MPC | $ | 144 | $ | 242 | |||

| MarkWest Utica EMG | 2 | 2 | |||||

| Ohio Gathering | 2 | 2 | |||||

| Other | 4 | 1 | |||||

| Total | $ | 152 | $ | 247 | |||

| (In millions) | September 30, 2017 | December 31, 2016 | |||||

| MPC | $ | 18 | $ | 11 | |||

| (In millions) | September 30, 2017 | December 31, 2016 | |||||

MPC(1) | $ | 277 | $ | 63 | |||

| MarkWest Utica EMG | 30 | 24 | |||||

| Other | 10 | — | |||||

| Total | $ | 317 | $ | 87 | |||

14

| (In millions) | (In millions) | September 30, 2021 | December 31, 2020 | |||||||||||||||

| Current assets - related parties | Current assets - related parties | |||||||||||||||||

| Receivables - MPC | Receivables - MPC | $ | 547 | $ | 615 | |||||||||||||

| (In millions) | September 30, 2017 | December 31, 2016 | ||||||||||||||||

| Minimum volume deficiencies - MPC | $ | 55 | $ | 48 | ||||||||||||||

| Project reimbursements - MPC | 27 | 9 | ||||||||||||||||

| Receivables - Other | Receivables - Other | 7 | 27 | |||||||||||||||

| Prepaid - MPC | Prepaid - MPC | 13 | 4 | |||||||||||||||

| Other - MPC | Other - MPC | 2 | 1 | |||||||||||||||

| Lease Receivables - MPC | Lease Receivables - MPC | 76 | 30 | |||||||||||||||

| Total | $ | 82 | $ | 57 | Total | 645 | 677 | |||||||||||

| Noncurrent assets - related parties | Noncurrent assets - related parties | |||||||||||||||||

| Long-term receivables - MPC | Long-term receivables - MPC | 32 | 32 | |||||||||||||||

| Right of use assets - MPC | Right of use assets - MPC | 230 | 231 | |||||||||||||||

| Long-term lease receivables - MPC | Long-term lease receivables - MPC | 857 | 386 | |||||||||||||||

| Unguaranteed residual asset - MPC | Unguaranteed residual asset - MPC | 41 | 23 | |||||||||||||||

| Total | Total | 1,160 | 672 | |||||||||||||||

| Current liabilities - related parties | Current liabilities - related parties | |||||||||||||||||

| Payables - MPC | Payables - MPC | 1,577 | 215 | |||||||||||||||

| Payables - Other | Payables - Other | 36 | 43 | |||||||||||||||

| Operating lease liabilities - MPC | Operating lease liabilities - MPC | 1 | 1 | |||||||||||||||

| Deferred revenue - Minimum volume deficiencies - MPC | Deferred revenue - Minimum volume deficiencies - MPC | 43 | 66 | |||||||||||||||

| Deferred revenue - Project reimbursements - MPC | Deferred revenue - Project reimbursements - MPC | 48 | 30 | |||||||||||||||

| Deferred revenue - Project reimbursements - Other | Deferred revenue - Project reimbursements - Other | 1 | 1 | |||||||||||||||

| Total | Total | 1,706 | 356 | |||||||||||||||

| Long-term liabilities - related parties | Long-term liabilities - related parties | |||||||||||||||||

| Long-term operating lease liabilities - MPC | Long-term operating lease liabilities - MPC | 228 | 229 | |||||||||||||||

| Long-term deferred revenue - Project reimbursements - MPC | Long-term deferred revenue - Project reimbursements - MPC | 62 | 47 | |||||||||||||||

| Long-term deferred revenue - Project reimbursements - Other | Long-term deferred revenue - Project reimbursements - Other | 7 | 7 | |||||||||||||||

| Total | Total | $ | 297 | $ | 283 | |||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In millions) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Net income attributable to MPLX LP | $ | 216 | $ | 141 | $ | 556 | $ | 100 | |||||||

Less: Limited partners’ distributions declared on Preferred units(1) | 16 | 16 | 49 | 25 | |||||||||||

General partner’s distributions declared (including IDRs)(1) | 88 | 54 | 229 | 148 | |||||||||||

Limited partners’ distributions declared on common units(1) | 232 | 179 | 648 | 507 | |||||||||||

| Undistributed net loss attributable to MPLX LP | $ | (120 | ) | $ | (108 | ) | $ | (370 | ) | $ | (580 | ) | |||

| Three Months Ended September 30, 2017 | |||||||||||||||

| (In millions, except per unit data) | General Partner | Limited Partners’ Common Units | Redeemable Preferred Units | Total | |||||||||||

| Basic and diluted net income attributable to MPLX LP per unit: | |||||||||||||||

| Net income attributable to MPLX LP: | |||||||||||||||

| Distributions declared (including IDRs) | $ | 88 | $ | 232 | $ | 16 | $ | 336 | |||||||

| Undistributed net loss attributable to MPLX LP | (2 | ) | (118 | ) | — | (120 | ) | ||||||||

Net income attributable to MPLX LP(1) | $ | 86 | $ | 114 | $ | 16 | $ | 216 | |||||||

| Weighted average units outstanding: | |||||||||||||||

| Basic | 8 | 394 | 31 | 433 | |||||||||||

| Diluted | 8 | 395 | 31 | 434 | |||||||||||

| Net income attributable to MPLX LP per limited partner unit: | |||||||||||||||

| Basic | $ | 0.29 | |||||||||||||

| Diluted | $ | 0.29 | |||||||||||||

| Three Months Ended September 30, 2016 | |||||||||||||||

| (In millions, except per unit data) | General Partner | Limited Partners’ Common Units | Redeemable Preferred Units | Total | |||||||||||

| Basic and diluted net income attributable to MPLX LP per unit: | |||||||||||||||

| Net income attributable to MPLX LP: | |||||||||||||||

| Distributions declared (including IDRs) | $ | 54 | $ | 179 | $ | 16 | $ | 249 | |||||||

| Undistributed net loss attributable to MPLX LP | (3 | ) | (105 | ) | — | (108 | ) | ||||||||

Net income attributable to MPLX LP(1) | $ | 51 | $ | 74 | $ | 16 | $ | 141 | |||||||

| Weighted average units outstanding: | |||||||||||||||

| Basic | 7 | 341 | 31 | 379 | |||||||||||

| Diluted | 7 | 346 | 31 | 384 | |||||||||||

| Net income attributable to MPLX LP per limited partner unit: | |||||||||||||||

| Basic | $ | 0.22 | |||||||||||||

| Diluted | $ | 0.21 | |||||||||||||

| Nine Months Ended September 30, 2017 | |||||||||||||||

| (In millions, except per unit data) | General Partner | Limited Partners’ Common Units | Redeemable Preferred Units | Total | |||||||||||

| Basic and diluted net income attributable to MPLX LP per unit: | |||||||||||||||

| Net income attributable to MPLX LP: | |||||||||||||||

| Distributions declared (including IDRs) | $ | 229 | $ | 648 | $ | 49 | $ | 926 | |||||||

| Undistributed net loss attributable to MPLX LP | (7 | ) | (363 | ) | — | (370 | ) | ||||||||

Net income attributable to MPLX LP(1) | $ | 222 | $ | 285 | $ | 49 | $ | 556 | |||||||

| Weighted average units outstanding: | |||||||||||||||

| Basic | 8 | 378 | 31 | 417 | |||||||||||

| Diluted | 8 | 381 | 31 | 420 | |||||||||||

| Net income attributable to MPLX LP per limited partner unit: | |||||||||||||||

| Basic | $ | 0.75 | |||||||||||||

| Diluted | $ | 0.75 | |||||||||||||

| Nine Months Ended September 30, 2016 | |||||||||||||||

| (In millions, except per unit data) | General Partner | Limited Partners’ Common Units | Redeemable Preferred Units | Total | |||||||||||

| Basic and diluted net loss attributable to MPLX LP per unit: | |||||||||||||||

| Net income (loss) attributable to MPLX LP: | |||||||||||||||

| Distributions declared (including IDRs) | $ | 148 | $ | 507 | $ | 25 | $ | 680 | |||||||

| Undistributed net loss attributable to MPLX LP | (12 | ) | (568 | ) | — | (580 | ) | ||||||||

Net income (loss) attributable to MPLX LP(1) | $ | 136 | $ | (61 | ) | $ | 25 | $ | 100 | ||||||

| Weighted average units outstanding: | |||||||||||||||

| Basic | 7 | 324 | 16 | 347 | |||||||||||

| Diluted | 7 | 324 | 16 | 347 | |||||||||||

| Net loss attributable to MPLX LP per limited partner unit: | |||||||||||||||

| Basic | $ | (0.19 | ) | ||||||||||||

| Diluted | $ | (0.19 | ) | ||||||||||||

The changes in the number of common units outstanding during the nine months ended September 30, 20172021 are summarized below:

| (In units) | Common | Class B | General Partner | Total | |||||||

| Balance at December 31, 2016 | 357,193,288 | 3,990,878 | 7,371,105 | 368,555,271 | |||||||

Unit-based compensation awards(1) | 183,509 | — | 3,745 | 187,254 | |||||||

Issuance of units under the ATM Program(2) | 13,846,998 | — | 282,591 | 14,129,589 | |||||||

Contribution of HST/WHC/MPLXT(3) | 12,960,376 | — | 264,497 | 13,224,873 | |||||||

Contribution of the Joint-Interest Acquisition(3) | 18,511,134 | — | 377,778 | 18,888,912 | |||||||

Class B conversion(4) | 4,350,057 | (3,990,878 | ) | 7,330 | 366,509 | ||||||

| Balance at September 30, 2017 | 407,045,362 | — | 8,307,046 | 415,352,408 | |||||||