fundamental value and characteristics of the underlying real estate,

creditworthiness of the tenant, and

transaction structure and pricing.

We believe we can achieve an appropriate risk-adjusted return through these pillars and conservatively project a property’s potential to generate targeted returns from current and future cash flows. We believe targeted returns are achieved through a combination of in-place income at the time of acquisition, rent growth, and a property’s potential for appreciation.

To achieve an appropriate risk-adjusted return, we maintain a diversified portfolio of real estate spread across multiple tenants, industries, and geographic locations. 25

Real Estate Portfolio Information

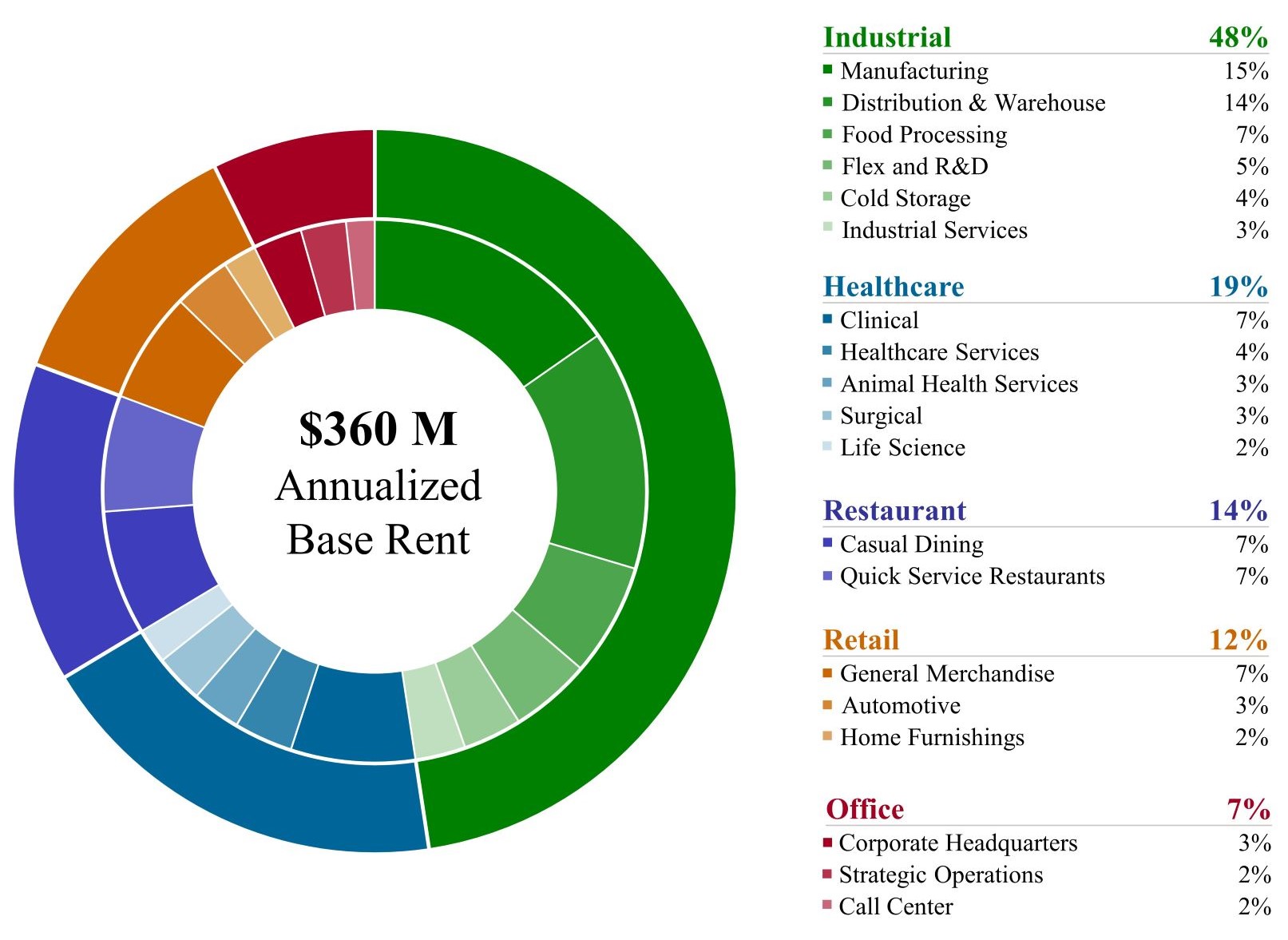

The following charts summarize our portfolio diversification by property type, tenant, brand, industry, and geographic location as of SeptemberJune 30, 2017.2022. The percentages below are calculated based on our contractual rental revenue over the next twelve months (“NTM Rent”), on a per property type basis divided by total NTM Rent. Late payments, non-payments or other unscheduled payments are not considered in the calculation. NTM Rent includes the impactABR of contractual rent escalations, excluding any potential variable rent increases that are based on consumer price index (“CPI”) and/or the tenants’ sales volume.$360.0 million as of June 30, 2022.

Industry

Diversification by % of NTM RentProperty Type

|

| |||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

| ||||

|

| |||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

Geographic

26

Property Type |

| # Properties |

|

| ABR |

|

| ABR as a % of |

|

| Square Feet |

|

| SF as a % of |

| |||||

Industrial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Manufacturing |

|

| 69 |

|

| $ | 55,116 |

|

|

| 15.3 | % |

|

| 10,046 |

|

|

| 29.2 | % |

Distribution & Warehouse |

|

| 47 |

|

|

| 51,375 |

|

|

| 14.3 | % |

|

| 9,526 |

|

|

| 27.7 | % |

Food Processing |

|

| 17 |

|

|

| 24,200 |

|

|

| 6.7 | % |

|

| 2,730 |

|

|

| 7.9 | % |

Flex and R&D |

|

| 7 |

|

|

| 17,296 |

|

|

| 4.8 | % |

|

| 1,457 |

|

|

| 4.3 | % |

Cold Storage |

|

| 4 |

|

|

| 12,724 |

|

|

| 3.5 | % |

|

| 933 |

|

|

| 2.7 | % |

Industrial Services |

|

| 22 |

|

|

| 10,765 |

|

|

| 3.0 | % |

|

| 587 |

|

|

| 1.7 | % |

Industrial Total |

|

| 166 |

|

|

| 171,476 |

|

|

| 47.6 | % |

|

| 25,279 |

|

|

| 73.5 | % |

Healthcare |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Clinical |

|

| 52 |

|

|

| 26,770 |

|

|

| 7.4 | % |

|

| 1,091 |

|

|

| 3.2 | % |

Healthcare Services |

|

| 28 |

|

|

| 12,528 |

|

|

| 3.5 | % |

|

| 463 |

|

|

| 1.3 | % |

Animal Health Services |

|

| 27 |

|

|

| 10,437 |

|

|

| 2.9 | % |

|

| 405 |

|

|

| 1.2 | % |

Surgical |

|

| 12 |

|

|

| 10,274 |

|

|

| 2.9 | % |

|

| 329 |

|

|

| 0.9 | % |

Life Science |

|

| 9 |

|

|

| 7,722 |

|

|

| 2.1 | % |

|

| 549 |

|

|

| 1.6 | % |

Untenanted |

|

| 1 |

|

|

| — |

|

|

| — |

|

|

| 18 |

|

|

| 0.1 | % |

Healthcare Total |

|

| 129 |

|

|

| 67,731 |

|

|

| 18.8 | % |

|

| 2,855 |

|

|

| 8.3 | % |

Restaurant |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Casual Dining |

|

| 101 |

|

|

| 26,738 |

|

|

| 7.4 | % |

|

| 675 |

|

|

| 2.0 | % |

Quick Service Restaurants |

|

| 146 |

|

|

| 24,787 |

|

|

| 6.9 | % |

|

| 499 |

|

|

| 1.4 | % |

Restaurant Total |

|

| 247 |

|

|

| 51,525 |

|

|

| 14.3 | % |

|

| 1,174 |

|

|

| 3.4 | % |

Retail |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

General Merchandise |

|

| 126 |

|

|

| 23,924 |

|

|

| 6.6 | % |

|

| 1,802 |

|

|

| 5.2 | % |

Automotive |

|

| 66 |

|

|

| 12,196 |

|

|

| 3.4 | % |

|

| 771 |

|

|

| 2.3 | % |

Home Furnishings |

|

| 13 |

|

|

| 7,030 |

|

|

| 2.0 | % |

|

| 797 |

|

|

| 2.3 | % |

Untenanted |

|

| 1 |

|

|

| — |

|

|

| — |

|

|

| 34 |

|

|

| 0.1 | % |

Retail Total |

|

| 206 |

|

|

| 43,150 |

|

|

| 12.0 | % |

|

| 3,404 |

|

|

| 9.9 | % |

Office |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Corporate Headquarters |

|

| 7 |

|

|

| 10,429 |

|

|

| 2.9 | % |

|

| 679 |

|

|

| 2.0 | % |

Strategic Operations |

|

| 5 |

|

|

| 9,806 |

|

|

| 2.7 | % |

|

| 615 |

|

|

| 1.8 | % |

Call Center |

|

| 4 |

|

|

| 5,902 |

|

|

| 1.7 | % |

|

| 391 |

|

|

| 1.1 | % |

Office Total |

|

| 16 |

|

|

| 26,137 |

|

|

| 7.3 | % |

|

| 1,685 |

|

|

| 4.9 | % |

Total |

|

| 764 |

|

| $ | 360,019 |

|

|

| 100.0 | % |

|

| 34,397 |

|

|

| 100.0 | % |

27

Diversification by %Tenant

Tenant |

| Property Type |

| # Properties |

|

| ABR |

|

| ABR as a % |

|

| Square Feet |

|

| SF as a % |

| |||||

Jack's Family Restaurants LP* |

| Quick Service Restaurants |

|

| 43 |

|

| $ | 7,166 |

|

|

| 2.0 | % |

|

| 147 |

|

|

| 0.4 | % |

Joseph T. Ryerson & Son, Inc |

| Distribution & Warehouse |

|

| 11 |

|

|

| 6,395 |

|

|

| 1.8 | % |

|

| 1,537 |

|

|

| 4.5 | % |

Red Lobster Hospitality & Red Lobster |

| Casual Dining |

|

| 20 |

|

|

| 6,361 |

|

|

| 1.8 | % |

|

| 166 |

|

|

| 0.5 | % |

J. Alexander's, LLC* |

| Casual Dining |

|

| 16 |

|

|

| 6,025 |

|

|

| 1.7 | % |

|

| 131 |

|

|

| 0.4 | % |

Axcelis Technologies, Inc. |

| Flex and R&D |

|

| 1 |

|

|

| 5,991 |

|

|

| 1.6 | % |

|

| 417 |

|

|

| 1.2 | % |

Hensley & Company* |

| Distribution & Warehouse |

|

| 3 |

|

|

| 5,871 |

|

|

| 1.6 | % |

|

| 577 |

|

|

| 1.7 | % |

Dollar General Corporation |

| General Merchandise |

|

| 57 |

|

|

| 5,636 |

|

|

| 1.5 | % |

|

| 531 |

|

|

| 1.5 | % |

BluePearl Holdings, LLC** |

| Animal Health Services |

|

| 13 |

|

|

| 5,451 |

|

|

| 1.5 | % |

|

| 165 |

|

|

| 0.5 | % |

Tractor Supply Company |

| General Merchandise |

|

| 21 |

|

|

| 5,279 |

|

|

| 1.5 | % |

|

| 417 |

|

|

| 1.2 | % |

Outback Steakhouse of Florida LLC*1 |

| Casual Dining |

|

| 22 |

|

|

| 5,278 |

|

|

| 1.5 | % |

|

| 140 |

|

|

| 0.4 | % |

Total Top 10 Tenants |

|

|

|

| 207 |

|

|

| 59,453 |

|

|

| 16.5 | % |

|

| 4,228 |

|

|

| 12.3 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

AHF, LLC* |

| Distribution & Warehouse/ |

|

| 5 |

|

|

| 5,142 |

|

|

| 1.4 | % |

|

| 982 |

|

|

| 2.8 | % |

Krispy Kreme Doughnut Corporation |

| Quick Service Restaurants/ |

|

| 27 |

|

|

| 5,034 |

|

|

| 1.4 | % |

|

| 156 |

|

|

| 0.4 | % |

Big Tex Trailer Manufacturing, Inc.* |

| Automotive/Distribution & |

|

| 17 |

|

|

| 4,957 |

|

|

| 1.4 | % |

|

| 1,302 |

|

|

| 3.8 | % |

Siemens Medical Solutions USA, Inc. & |

| Manufacturing/Flex |

|

| 2 |

|

|

| 4,936 |

|

|

| 1.4 | % |

|

| 545 |

|

|

| 1.6 | % |

Carvana, LLC* |

| Industrial Services |

|

| 2 |

|

|

| 4,510 |

|

|

| 1.3 | % |

|

| 230 |

|

|

| 0.7 | % |

Santa Cruz Valley Hospital |

| Healthcare Facilities |

|

| 1 |

|

|

| 4,500 |

|

|

| 1.2 | % |

|

| 148 |

|

|

| 0.4 | % |

Nestle' Dreyer's Ice Cream Company |

| Cold Storage |

|

| 1 |

|

|

| 4,476 |

|

|

| 1.2 | % |

|

| 310 |

|

|

| 0.9 | % |

Arkansas Surgical Hospital |

| Surgical |

|

| 1 |

|

|

| 4,366 |

|

|

| 1.2 | % |

|

| 129 |

|

|

| 0.4 | % |

American Signature, Inc. |

| Home Furnishings |

|

| 6 |

|

|

| 4,224 |

|

|

| 1.2 | % |

|

| 474 |

|

|

| 1.4 | % |

Fresh Express Incorporated |

| Food Processing |

|

| 1 |

|

|

| 4,144 |

|

|

| 1.2 | % |

|

| 335 |

|

|

| 1.0 | % |

Total Top 20 Tenants |

|

|

|

| 270 |

|

| $ | 105,742 |

|

|

| 29.4 | % |

|

| 8,839 |

|

|

| 25.7 | % |

1Tenant's properties include 20 Outback Steakhouse restaurants and two Carrabba's Italian Grill restaurants.

*Subject to a master lease.

**Includes properties leased by multiple tenants, some, not all, of NTM Rentwhich are subject to master leases.

Diversification by Brand

Brand |

| Property Type |

| # Properties |

|

| ABR |

|

| ABR as a % |

|

| Square Feet |

|

| SF as a % |

| |||||

Jack's Family Restaurants* |

| Quick Service Restaurants |

|

| 43 |

|

| $ | 7,166 |

|

|

| 2.0 | % |

|

| 147 |

|

|

| 0.4 | % |

Ryerson |

| Distribution & Warehouse |

|

| 11 |

|

|

| 6,395 |

|

|

| 1.8 | % |

|

| 1,537 |

|

|

| 4.5 | % |

Red Lobster* |

| Casual Dining |

|

| 20 |

|

|

| 6,361 |

|

|

| 1.8 | % |

|

| 166 |

|

|

| 0.5 | % |

Axcelis |

| Flex and R&D |

|

| 1 |

|

|

| 5,991 |

|

|

| 1.6 | % |

|

| 417 |

|

|

| 1.2 | % |

Hensley* |

| Distribution & Warehouse |

|

| 3 |

|

|

| 5,871 |

|

|

| 1.6 | % |

|

| 577 |

|

|

| 1.7 | % |

Dollar General |

| General Merchandise |

|

| 57 |

|

|

| 5,636 |

|

|

| 1.5 | % |

|

| 531 |

|

|

| 1.5 | % |

BluePearl Veterinary Partners** |

| Animal Health Services |

|

| 13 |

|

|

| 5,451 |

|

|

| 1.5 | % |

|

| 165 |

|

|

| 0.5 | % |

Bob Evans Farms*1 |

| Casual Dining/Food Processing |

|

| 21 |

|

|

| 5,352 |

|

|

| 1.5 | % |

|

| 281 |

|

|

| 0.9 | % |

Tractor Supply Co. |

| General Merchandise |

|

| 21 |

|

|

| 5,279 |

|

|

| 1.5 | % |

|

| 417 |

|

|

| 1.2 | % |

AHF Products* |

| Distribution & Warehouse/ |

|

| 5 |

|

|

| 5,142 |

|

|

| 1.4 | % |

|

| 982 |

|

|

| 2.8 | % |

Total Top 10 Brands |

|

|

|

| 195 |

|

|

| 58,644 |

|

|

| 16.2 | % |

|

| 5,220 |

|

|

| 15.2 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Krispy Kreme |

| Quick Service Restaurants/ |

|

| 27 |

|

|

| 5,034 |

|

|

| 1.4 | % |

|

| 156 |

|

|

| 0.4 | % |

Big Tex Trailers* |

| Automotive/Distribution & |

|

| 17 |

|

|

| 4,957 |

|

|

| 1.4 | % |

|

| 1,302 |

|

|

| 3.8 | % |

Siemens |

| Manufacturing/Flex |

|

| 2 |

|

|

| 4,936 |

|

|

| 1.4 | % |

|

| 545 |

|

|

| 1.6 | % |

Outback Steakhouse* |

| Casual Dining |

|

| 20 |

|

|

| 4,566 |

|

|

| 1.3 | % |

|

| 126 |

|

|

| 0.4 | % |

Carvana* |

| Industrial Services |

|

| 2 |

|

|

| 4,510 |

|

|

| 1.3 | % |

|

| 230 |

|

|

| 0.7 | % |

Santa Cruz Valley Hospital |

| Healthcare Facilities |

|

| 1 |

|

|

| 4,500 |

|

|

| 1.2 | % |

|

| 148 |

|

|

| 0.4 | % |

Nestle' |

| Cold Storage |

|

| 1 |

|

|

| 4,476 |

|

|

| 1.2 | % |

|

| 310 |

|

|

| 0.9 | % |

Arkansas Surgical Hospital |

| Surgical |

|

| 1 |

|

|

| 4,366 |

|

|

| 1.2 | % |

|

| 129 |

|

|

| 0.4 | % |

Wendy's** |

| Quick Service Restaurants |

|

| 29 |

|

|

| 4,320 |

|

|

| 1.2 | % |

|

| 83 |

|

|

| 0.2 | % |

Value City Furniture |

| Home Furnishings |

|

| 6 |

|

|

| 4,224 |

|

|

| 1.2 | % |

|

| 474 |

|

|

| 1.4 | % |

Total Top 20 Brands |

|

|

|

| 301 |

|

| $ | 104,533 |

|

|

| 29.0 | % |

|

| 8,723 |

|

|

| 25.4 | % |

1Brand includes one BEF Foods, Inc. property and 20 Bob Evans Restaurants, LLC properties.

**Includes properties leased by multiple tenants, some, not all, of which are subject to master leases.

28

Diversification by Industry

Industry |

| # Properties |

|

| ABR |

|

| ABR as a % |

|

| Square Feet ('000s) |

|

| SF as a % |

| |||||

Healthcare Facilities |

|

| 102 |

|

| $ | 53,633 |

|

|

| 14.9 | % |

|

| 2,029 |

|

|

| 5.9 | % |

Restaurant |

|

| 250 |

|

|

| 52,296 |

|

|

| 14.5 | % |

|

| 1,217 |

|

|

| 3.5 | % |

Packaged Foods & Meats |

|

| 11 |

|

|

| 17,698 |

|

|

| 4.9 | % |

|

| 1,914 |

|

|

| 5.6 | % |

Distributors |

|

| 27 |

|

|

| 15,699 |

|

|

| 4.4 | % |

|

| 2,695 |

|

|

| 7.8 | % |

Food Distributors |

|

| 8 |

|

|

| 14,678 |

|

|

| 4.1 | % |

|

| 1,786 |

|

|

| 5.2 | % |

Specialty Stores |

|

| 31 |

|

|

| 13,930 |

|

|

| 3.9 | % |

|

| 1,338 |

|

|

| 3.9 | % |

Auto Parts & Equipment |

|

| 39 |

|

|

| 12,672 |

|

|

| 3.5 | % |

|

| 2,387 |

|

|

| 6.9 | % |

Home Furnishings Retail |

|

| 18 |

|

|

| 12,459 |

|

|

| 3.5 | % |

|

| 1,858 |

|

|

| 5.4 | % |

Specialized Consumer Services |

|

| 47 |

|

|

| 12,218 |

|

|

| 3.4 | % |

|

| 722 |

|

|

| 2.1 | % |

Metal & Glass Containers |

|

| 8 |

|

|

| 9,898 |

|

|

| 2.7 | % |

|

| 2,206 |

|

|

| 6.4 | % |

Healthcare Services |

|

| 18 |

|

|

| 9,213 |

|

|

| 2.6 | % |

|

| 515 |

|

|

| 1.5 | % |

General Merchandise Stores |

|

| 90 |

|

|

| 9,011 |

|

|

| 2.5 | % |

|

| 817 |

|

|

| 2.4 | % |

Aerospace & Defense |

|

| 7 |

|

|

| 8,694 |

|

|

| 2.4 | % |

|

| 952 |

|

|

| 2.8 | % |

Internet & Direct Marketing Retail |

|

| 3 |

|

|

| 6,881 |

|

|

| 1.9 | % |

|

| 447 |

|

|

| 1.3 | % |

Electronic Components |

|

| 2 |

|

|

| 6,806 |

|

|

| 1.9 | % |

|

| 466 |

|

|

| 1.4 | % |

Other (42 industries) |

|

| 101 |

|

|

| 104,233 |

|

|

| 28.9 | % |

|

| 12,996 |

|

|

| 37.7 | % |

Untenanted properties |

|

| 2 |

|

|

| — |

|

|

| — |

|

|

| 52 |

|

|

| 0.2 | % |

Total |

|

| 764 |

|

| $ | 360,019 |

|

|

| 100.0 | % |

|

| 34,397 |

|

|

| 100.0 | % |

29

Diversification by Geographic Location

State / |

| # |

|

| ABR |

|

| ABR as a |

|

| Square Feet ('000s) |

|

| SF as a % |

|

|

| State / |

| # |

|

| ABR |

|

| ABR as a |

|

| Square Feet ('000s) |

|

| SF as a % |

| ||||||||||

TX |

|

| 70 |

|

| $ | 37,549 |

|

|

| 10.4 | % |

|

| 3,636 |

|

|

| 10.6 | % |

|

| LA |

|

| 4 |

|

|

| 3,401 |

|

|

| 0.9 | % |

|

| 194 |

|

|

| 0.6 | % |

IL |

|

| 27 |

|

|

| 21,566 |

|

|

| 6.0 | % |

|

| 2,002 |

|

|

| 5.8 | % |

|

| NE |

|

| 6 |

|

|

| 3,037 |

|

|

| 0.8 | % |

|

| 509 |

|

|

| 1.5 | % |

WI |

|

| 35 |

|

|

| 20,744 |

|

|

| 5.8 | % |

|

| 2,163 |

|

|

| 6.3 | % |

|

| MD |

|

| 4 |

|

|

| 2,987 |

|

|

| 0.8 | % |

|

| 293 |

|

|

| 0.9 | % |

MI |

|

| 49 |

|

|

| 17,130 |

|

|

| 4.8 | % |

|

| 1,633 |

|

|

| 4.7 | % |

|

| NM |

|

| 8 |

|

|

| 2,815 |

|

|

| 0.8 | % |

|

| 96 |

|

|

| 0.3 | % |

FL |

|

| 42 |

|

|

| 16,122 |

|

|

| 4.5 | % |

|

| 844 |

|

|

| 2.5 | % |

|

| MS |

|

| 8 |

|

|

| 2,774 |

|

|

| 0.8 | % |

|

| 334 |

|

|

| 1.0 | % |

OH |

|

| 38 |

|

|

| 15,786 |

|

|

| 4.4 | % |

|

| 1,416 |

|

|

| 4.1 | % |

|

| IA |

|

| 4 |

|

|

| 2,754 |

|

|

| 0.8 | % |

|

| 622 |

|

|

| 1.8 | % |

CA |

|

| 10 |

|

|

| 15,622 |

|

|

| 4.3 | % |

|

| 1,493 |

|

|

| 4.3 | % |

|

| SC |

|

| 13 |

|

|

| 2,494 |

|

|

| 0.7 | % |

|

| 308 |

|

|

| 0.9 | % |

IN |

|

| 30 |

|

|

| 15,035 |

|

|

| 4.2 | % |

|

| 1,858 |

|

|

| 5.4 | % |

|

| WV |

|

| 16 |

|

|

| 2,486 |

|

|

| 0.7 | % |

|

| 109 |

|

|

| 0.3 | % |

MN |

|

| 21 |

|

|

| 14,600 |

|

|

| 4.0 | % |

|

| 2,285 |

|

|

| 6.6 | % |

|

| CO |

|

| 4 |

|

|

| 2,459 |

|

|

| 0.7 | % |

|

| 126 |

|

|

| 0.4 | % |

TN |

|

| 49 |

|

|

| 13,995 |

|

|

| 3.9 | % |

|

| 866 |

|

|

| 2.5 | % |

|

| UT |

|

| 3 |

|

|

| 2,379 |

|

|

| 0.7 | % |

|

| 280 |

|

|

| 0.8 | % |

NC |

|

| 36 |

|

|

| 13,742 |

|

|

| 3.8 | % |

|

| 1,425 |

|

|

| 4.1 | % |

|

| CT |

|

| 2 |

|

|

| 1,758 |

|

|

| 0.5 | % |

|

| 55 |

|

|

| 0.2 | % |

AZ |

|

| 9 |

|

|

| 13,213 |

|

|

| 3.7 | % |

|

| 909 |

|

|

| 2.6 | % |

|

| MT |

|

| 7 |

|

|

| 1,563 |

|

|

| 0.4 | % |

|

| 43 |

|

|

| 0.1 | % |

AL |

|

| 53 |

|

|

| 11,950 |

|

|

| 3.3 | % |

|

| 873 |

|

|

| 2.5 | % |

|

| NV |

|

| 2 |

|

|

| 1,336 |

|

|

| 0.4 | % |

|

| 81 |

|

|

| 0.2 | % |

GA |

|

| 33 |

|

|

| 11,356 |

|

|

| 3.1 | % |

|

| 1,576 |

|

|

| 4.6 | % |

|

| DE |

|

| 4 |

|

|

| 1,154 |

|

|

| 0.3 | % |

|

| 133 |

|

|

| 0.4 | % |

NY |

|

| 26 |

|

|

| 10,718 |

|

|

| 3.0 | % |

|

| 680 |

|

|

| 2.0 | % |

|

| ND |

|

| 2 |

|

|

| 943 |

|

|

| 0.3 | % |

|

| 28 |

|

|

| 0.1 | % |

MA |

|

| 5 |

|

|

| 10,456 |

|

|

| 2.9 | % |

|

| 1,026 |

|

|

| 3.0 | % |

|

| VT |

|

| 2 |

|

|

| 420 |

|

|

| 0.1 | % |

|

| 24 |

|

|

| 0.1 | % |

AR |

|

| 12 |

|

|

| 8,767 |

|

|

| 2.4 | % |

|

| 544 |

|

|

| 1.6 | % |

|

| WY |

|

| 1 |

|

|

| 307 |

|

|

| 0.1 | % |

|

| 21 |

|

|

| 0.1 | % |

OK |

|

| 21 |

|

|

| 7,597 |

|

|

| 2.1 | % |

|

| 977 |

|

|

| 2.8 | % |

|

| OR |

|

| 1 |

|

|

| 136 |

|

|

| 0.0 | % |

|

| 9 |

|

|

| 0.1 | % |

KY |

|

| 24 |

|

|

| 7,486 |

|

|

| 2.1 | % |

|

| 946 |

|

|

| 2.7 | % |

|

| SD |

|

| 1 |

|

|

| 81 |

|

|

| 0.0 | % |

|

| 9 |

|

|

| 0.0 | % |

PA |

|

| 17 |

|

|

| 7,080 |

|

|

| 2.0 | % |

|

| 1,037 |

|

|

| 3.0 | % |

|

| Total US |

|

| 757 |

|

| $ | 351,970 |

|

|

| 97.8 | % |

|

| 33,967 |

|

|

| 98.8 | % |

MO |

|

| 12 |

|

|

| 6,064 |

|

|

| 1.7 | % |

|

| 1,136 |

|

|

| 3.3 | % |

|

| BC |

|

| 2 |

|

| $ | 4,633 |

|

|

| 1.3 | % |

|

| 253 |

|

|

| 0.7 | % |

KS |

|

| 11 |

|

|

| 5,489 |

|

|

| 1.5 | % |

|

| 648 |

|

|

| 1.9 | % |

|

| ON |

|

| 3 |

|

|

| 2,085 |

|

|

| 0.6 | % |

|

| 101 |

|

|

| 0.3 | % |

VA |

|

| 17 |

|

|

| 5,451 |

|

|

| 1.5 | % |

|

| 204 |

|

|

| 0.6 | % |

|

| AB |

|

| 1 |

|

|

| 981 |

|

|

| 0.2 | % |

|

| 51 |

|

|

| 0.1 | % |

NJ |

|

| 3 |

|

|

| 4,904 |

|

|

| 1.4 | % |

|

| 366 |

|

|

| 1.1 | % |

|

| MB |

|

| 1 |

|

|

| 350 |

|

|

| 0.1 | % |

|

| 25 |

|

|

| 0.1 | % |

WA |

|

| 15 |

|

|

| 4,264 |

|

|

| 1.2 | % |

|

| 150 |

|

|

| 0.4 | % |

|

| Total Canada |

|

| 7 |

|

| $ | 8,049 |

|

|

| 2.2 | % |

|

| 430 |

|

|

| 1.2 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Grand Total |

|

| 764 |

|

| $ | 360,019 |

|

|

| 100.0 | % |

|

| 34,397 |

|

|

| 100.0 | % | |||||

30

Our Leases

We typically lease our properties pursuant to long-term net leases that often have renewal options. Substantially all of our leases are triple-net,net, meaning that our tenants are responsible for the maintenance, insurance, and property taxesgenerally obligated to pay all expenses associated with the leased property (such as real estate taxes, insurance, maintenance, repairs, and capital costs).

As of June 30, 2022, approximately 99.8% of our portfolio, representing all but two of our properties, they lease from us. Since inception and at September 30, 2017,was subject to a lease. Because substantially all of our properties are subject to leases. We do not currently engage in the development of real estate, which could cause a delay in timing between the funds used to invest in properties and the corresponding cash inflows from rental receipts. Our cash flows from operations are primarily generated through our real estate investment portfolio and the monthly lease payments under our long-term leases with our tenants.

Due to the fact that all of our properties are leased to single tenants under long-term leases, we are not currently required to perform significant ongoing leasing activities on our properties. The leases for only two of our properties, representing less than 1% of our annual rental streams (calculated based on NTM Rent), will expire before 2020.

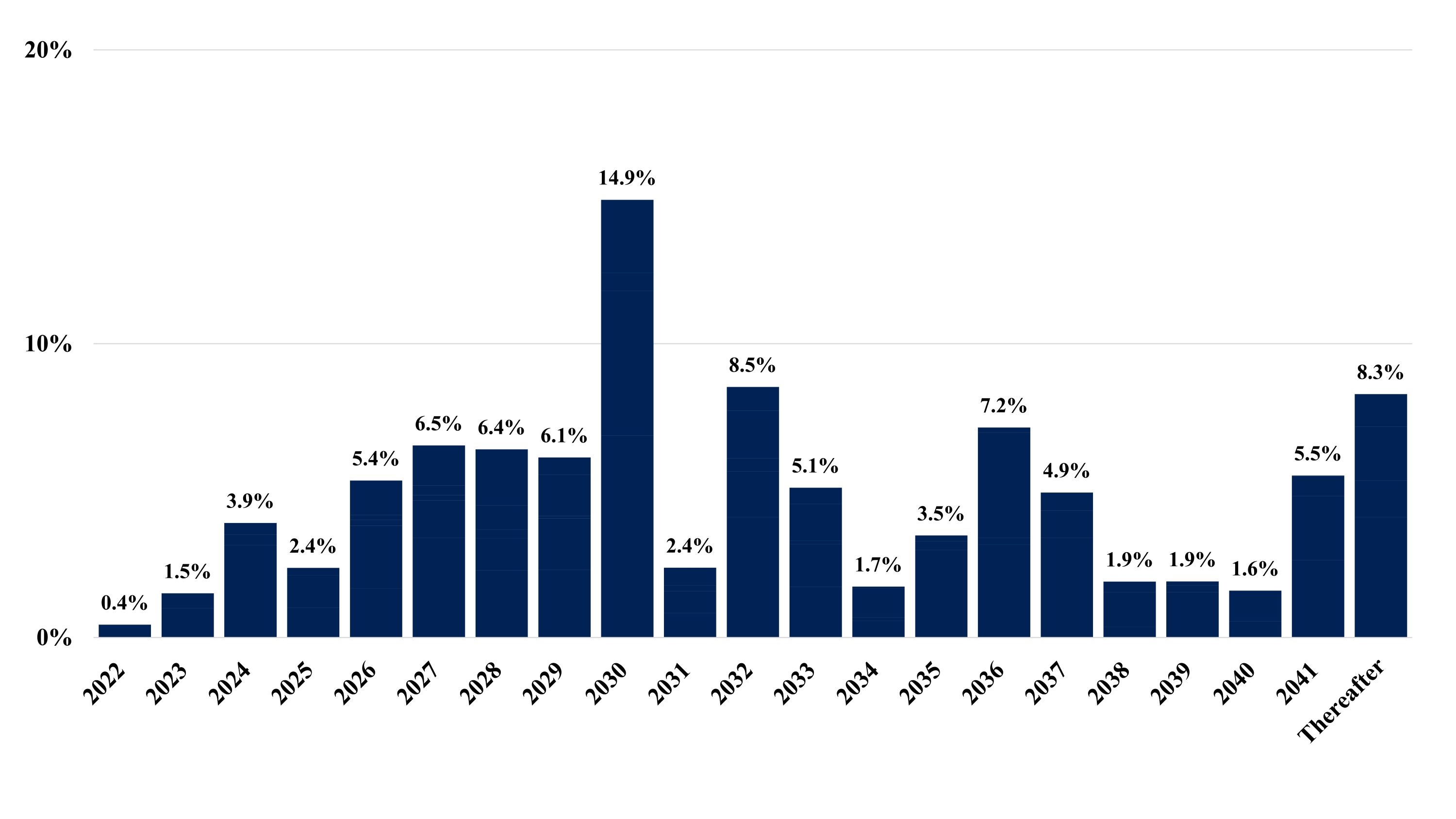

As of SeptemberJune 30, 2017,2022, the ABR weighted average remaining term of our leases (calculated based on NTM Rent) was approximately 13.2 years, excluding renewal options, which are exercisable at the option of our tenants upon expiration of their base lease term.10.6 years. Less than 5% of the properties in our portfolio are subject to leases without at least one renewal option. Furthermore, the weighted average lease term on the $159.2 million in properties acquired during the three months ended September 30, 2017, was 13.0 years. Over 50%Approximately 67.4% of our rental revenue isABR was derived from leases that will expire duringin 2030 and thereafter. As of September 30, 2017, notafter, and no more than 10%6.5% of our rental revenue isABR was derived from leases that expire in any single year in the decade between 2020 andprior to 2030. The following chart sets forth our lease expirations based upon the terms of ourthe leases in place as of SeptemberJune 30, 2017.2022.

31

The following table presents certain information based on lease expirations by year. Amounts are in thousands, except for number of properties.

Expiration Year |

| # Properties |

|

| # Leases |

|

| ABR |

|

| ABR as a % of |

|

| Square Feet |

|

| SF as a % of |

| ||||||

2022 |

|

| 1 |

|

|

| 2 |

|

| $ | 1,566 |

|

|

| 0.4 | % |

|

| 46 |

|

|

| 0.1 | % |

2023 |

|

| 7 |

|

|

| 8 |

|

|

| 5,412 |

|

|

| 1.5 | % |

|

| 538 |

|

|

| 1.6 | % |

2024 |

|

| 11 |

|

|

| 11 |

|

|

| 14,036 |

|

|

| 3.9 | % |

|

| 1,689 |

|

|

| 4.9 | % |

2025 |

|

| 20 |

|

|

| 23 |

|

|

| 8,527 |

|

|

| 2.4 | % |

|

| 698 |

|

|

| 2.0 | % |

2026 |

|

| 35 |

|

|

| 32 |

|

|

| 19,235 |

|

|

| 5.4 | % |

|

| 1,413 |

|

|

| 4.1 | % |

2027 |

|

| 29 |

|

|

| 28 |

|

|

| 23,531 |

|

|

| 6.5 | % |

|

| 2,019 |

|

|

| 5.9 | % |

2028 |

|

| 33 |

|

|

| 31 |

|

|

| 23,061 |

|

|

| 6.4 | % |

|

| 2,291 |

|

|

| 6.7 | % |

2029 |

|

| 71 |

|

|

| 39 |

|

|

| 22,061 |

|

|

| 6.1 | % |

|

| 2,711 |

|

|

| 7.9 | % |

2030 |

|

| 101 |

|

|

| 57 |

|

|

| 53,636 |

|

|

| 14.9 | % |

|

| 5,110 |

|

|

| 14.8 | % |

2031 |

|

| 33 |

|

|

| 28 |

|

|

| 8,547 |

|

|

| 2.4 | % |

|

| 805 |

|

|

| 2.3 | % |

2032 |

|

| 59 |

|

|

| 44 |

|

|

| 30,701 |

|

|

| 8.5 | % |

|

| 3,437 |

|

|

| 10.0 | % |

2033 |

|

| 49 |

|

|

| 23 |

|

|

| 18,360 |

|

|

| 5.1 | % |

|

| 1,575 |

|

|

| 4.6 | % |

2034 |

|

| 33 |

|

|

| 22 |

|

|

| 6,240 |

|

|

| 1.7 | % |

|

| 409 |

|

|

| 1.2 | % |

2035 |

|

| 17 |

|

|

| 13 |

|

|

| 12,494 |

|

|

| 3.5 | % |

|

| 1,927 |

|

|

| 5.6 | % |

2036 |

|

| 86 |

|

|

| 21 |

|

|

| 25,732 |

|

|

| 7.2 | % |

|

| 2,854 |

|

|

| 8.3 | % |

2037 |

|

| 24 |

|

|

| 9 |

|

|

| 17,762 |

|

|

| 4.9 | % |

|

| 1,369 |

|

|

| 4.0 | % |

2038 |

|

| 33 |

|

|

| 29 |

|

|

| 6,842 |

|

|

| 1.9 | % |

|

| 306 |

|

|

| 0.9 | % |

2039 |

|

| 11 |

|

|

| 6 |

|

|

| 6,860 |

|

|

| 1.9 | % |

|

| 803 |

|

|

| 2.3 | % |

2040 |

|

| 31 |

|

|

| 5 |

|

|

| 5,744 |

|

|

| 1.6 | % |

|

| 312 |

|

|

| 0.9 | % |

2041 |

|

| 40 |

|

|

| 8 |

|

|

| 19,850 |

|

|

| 5.5 | % |

|

| 1,731 |

|

|

| 5.0 | % |

Thereafter |

|

| 38 |

|

|

| 9 |

|

|

| 29,822 |

|

|

| 8.3 | % |

|

| 2,302 |

|

|

| 6.7 | % |

Untenanted properties |

|

| 2 |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| 52 |

|

|

| 0.2 | % |

Total |

|

| 764 |

|

|

| 448 |

|

| $ | 360,019 |

|

|

| 100.0 | % |

|

| 34,397 |

|

|

| 100.0 | % |

32

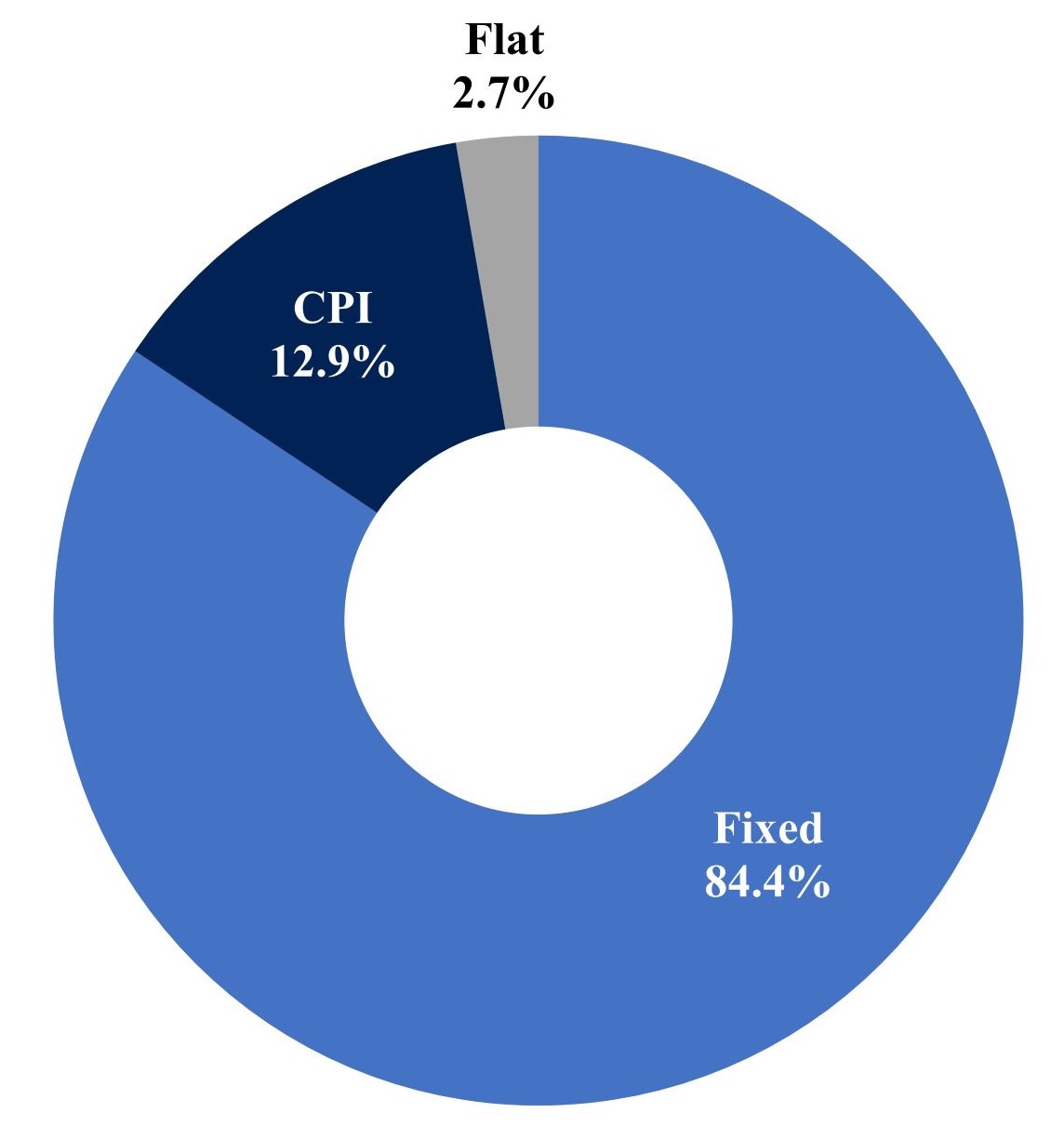

Substantially all of our leases provide for periodic contractual rent escalations. As of June 30, 2022, leases contributing 97.3% of our ABR provided for increases in future ABR, generally ranging from 1.5% to 2.5% annually, with an ABR weighted average annual minimum increase equal to 2.0% of base rent. Generally, our rent escalators increase rent on specified dates by a fixed percentage. Our escalations provide us with a source of organic revenue growth and a measure of inflation protection. Additional information on lease escalation frequency and weighted average annual escalation rates as of June 30, 2022 is displayed below:

Lease Escalation Frequency |

| % of ABR |

|

| Weighted Average Annual Minimum Increase (a) |

| ||

Annually |

|

| 78.2 | % |

|

| 2.3 | % |

Every 2 years |

|

| 0.1 | % |

|

| 1.8 | % |

Every 3 years |

|

| 2.9 | % |

|

| 3.0 | % |

Every 4 years |

|

| 1.1 | % |

|

| 2.4 | % |

Every 5 years |

|

| 8.0 | % |

|

| 1.8 | % |

Other escalation frequencies |

|

| 7.0 | % |

|

| 1.6 | % |

Flat |

|

| 2.7 | % |

|

| — |

|

Total/Weighted Average (b) |

|

| 100.0 | % |

|

| 2.0 | % |

(a)

The escalation provisions of our leases (by percentage of ABR) as of June 30, 2022, are displayed in the following chart:

33

Results of Operations

The following discussion includes the results of our operations for the periods presented.

Three Months Ended June 30, 2022 Compared to Three Months Ended March 31, 2022

Lease Maturity Schedule, by %Revenues, net

|

| For the Three Months Ended | |||||||||||||

|

| June 30, |

| March 31, |

| Increase/(Decrease) | |||||||||

(in thousands) |

| 2022 |

| 2022 |

| $ |

| % | |||||||

Contractual rental amounts billed for operating leases |

| $ | 87,505 |

|

| $ | 84,396 |

|

| $ | 3,109 |

|

| 3.7 | % |

Adjustment to recognize contractual operating lease |

|

| 5,090 |

|

|

| 5,021 |

|

|

| 69 |

|

| 1.4 | % |

Net write-offs of accrued rental income |

|

| — |

|

|

| (1,326 | ) |

|

| 1,326 |

|

| (100.0 | )% |

Variable rental amounts earned |

|

| 291 |

|

|

| 186 |

|

|

| 105 |

|

| 56.5 | % |

Earned income from direct financing leases |

|

| 721 |

|

|

| 723 |

|

|

| (2 | ) |

| (0.3 | )% |

Interest income from sales-type leases |

|

| 15 |

|

|

| 14 |

|

|

| 1 |

|

| 7.1 | % |

Operating expenses billed to tenants |

|

| 4,263 |

|

|

| 4,735 |

|

|

| (472 | ) |

| (10.0 | )% |

Other income from real estate transactions |

|

| 134 |

|

|

| 42 |

|

|

| 92 |

|

| >100.0 | % |

Adjustment to revenue recognized for uncollectible |

|

| (6 | ) |

|

| 50 |

|

|

| (56 | ) |

| <(100.0 | )% |

Total Lease revenues, net |

| $ | 98,013 |

|

| $ | 93,841 |

|

| $ | 4,172 |

|

| 4.4 | % |

The increase in Lease revenues, net was primarily attributable to growth in our real estate portfolio through property acquisitions. As we acquire properties throughout the period, the full benefit of NTM Rentlease revenues from newly acquired properties will not be realized in the quarter of acquisition. During the first quarter of 2022, we invested $210.0 million, excluding capitalized acquisition costs, in 27 properties at a weighted average initial cash capitalization rate of 5.7%. Most of these acquisitions closed during the month of March 2022, and therefore did not materially contribute to Lease revenues, net for the three months ended March 31, 2022. The increase was also partially attributable to our $182.4 million of acquisitions during the second quarter of 2022 at a 6.4% weighted average initial cash capitalization rate, the full benefit of which we anticipate will be realized during the third quarter of 2022. Additionally, we did not record any write-offs of accrued rental income during the three months ended June 30, 2022.

Operating Expenses

|

| For the Three Months Ended |

| |||||||||||||

|

| June 30, |

|

| March 31, |

|

| Increase/(Decrease) |

| |||||||

(in thousands) |

| 2022 |

|

| 2022 |

|

| $ |

|

| % |

| ||||

Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Depreciation and amortization |

| $ | 35,511 |

|

| $ | 34,290 |

|

| $ | 1,221 |

|

|

| 3.6 | % |

Property and operating expense |

|

| 4,696 |

|

|

| 5,044 |

|

|

| (348 | ) |

|

| (6.9 | )% |

General and administrative |

|

| 9,288 |

|

|

| 8,828 |

|

|

| 460 |

|

|

| 5.2 | % |

Provision for impairment of investment in rental properties |

|

| 1,380 |

|

|

| — |

|

|

| 1,380 |

|

|

| 100.0 | % |

Total operating expenses |

| $ | 50,875 |

|

| $ | 48,162 |

|

| $ | 2,713 |

|

|

| 5.6 | % |

Depreciation and amortization

The increase in depreciation and amortization for the three months ended June 30, 2022 was primarily due to growth in our real estate portfolio.

Provision for impairment of investment in rental properties

During the three months ended June 30, 2022 we recognized $1.4 million of impairment on our investments in rental properties due to change in our long-term hold strategy for a single property, compared to no impairment recognized during the three months ended March 31, 2022. The following table presents the lease expirations by year, including the number of tenants and properties with leases expiring, the square footage covered by the leases expiring, the NTM Rent, and the percentage of NTM Rentimpairment charges for the leases expiring. Late payments, non-paymentsrespective periods:

|

| For the Three Months Ended |

| |||||

|

| June 30, |

|

| March 31, |

| ||

(in thousands, except number of properties) |

| 2022 |

|

| 2022 |

| ||

Number of properties |

|

| 1 |

|

|

| — |

|

Carrying value prior to impairment charge |

| $ | 3,674 |

|

| $ | — |

|

Fair value |

|

| 2,294 |

|

|

| — |

|

Impairment charge |

| $ | 1,380 |

|

| $ | — |

|

The timing and amount of impairment fluctuates from period to period depending on the specific facts and circumstances.

35

Other income (expenses)

|

| For the Three Months Ended | |||||||||||||||||||

| �� | June 30, |

| March 31, |

| Increase/(Decrease) | |||||||||||||||

(in thousands) |

| 2022 |

| 2022 |

| $ |

| % | |||||||||||||

Other income (expenses) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

Interest expense |

| $ | (17,888 |

| ) |

| $ | (16,896 |

| ) |

| $ | 992 |

|

|

| 5.9 | % | |||

Gain on sale of real estate |

|

|

| 4,071 |

|

|

|

|

| 1,196 |

|

|

|

|

| 2,875 |

|

|

| >100.0 | % |

Income taxes |

|

| (401 |

| ) |

|

| (412 |

| ) |

|

| (11 |

| ) |

| (2.7 | )% | |||

Other income (expenses) |

|

|

| 2,632 |

|

|

|

| (1,126 |

| ) |

|

| (3,758 |

| ) |

| >100.0 | % | ||

Interest expense

The increase in interest expense reflects an increase in our weighted average cost of borrowings combined with increased average outstanding borrowings during the three months ended June 30, 2022 compared to during the three months ended March 31, 2022. During the second quarter we increased total outstanding borrowings by $53.8 million to partially fund our acquisitions. Of our $1.9 billion of total outstanding indebtedness, approximately $200.5 million, or other unscheduled payments are not considered in the NTM Rent amounts. NTM Rent includes10.8% is variable, and therefore subject to the impact of contractual rent escalations, excluding any potential variable rent increases that arefluctuations in interest rates.

Gain on sale of real estate

Our recognition of a gain or loss on the sale of real estate varies from transaction to transaction based on CPI and/or the tenants’ sales volume. Amounts arefluctuations in thousands, except the number of tenantsasset prices and properties.

Year |

| Number of Tenants |

|

| Number of Properties |

|

| Square Footage |

|

| NTM Rent |

|

| Percentage of NTM Rent |

| |||||

2017 |

|

| — |

|

|

| — |

|

|

| — |

|

| $ | — |

|

|

| — | % |

2018 |

|

| 1 |

|

|

| 1 |

|

|

| 2 |

|

|

| 131 |

|

|

| <0.1 | % |

2019 |

|

| 1 |

|

|

| 1 |

|

|

| 2 |

|

|

| 117 |

|

|

| <0.1 | % |

2020 |

|

| 3 |

|

|

| 4 |

|

|

| 116 |

|

|

| 1,376 |

|

|

| 0.8 | % |

2021 |

|

| 2 |

|

|

| 4 |

|

|

| 9 |

|

|

| 576 |

|

|

| 0.3 | % |

2022 |

|

| 3 |

|

|

| 3 |

|

|

| 87 |

|

|

| 2,393 |

|

|

| 1.4 | % |

2023 |

|

| 9 |

|

|

| 13 |

|

|

| 724 |

|

|

| 6,786 |

|

|

| 4.0 | % |

2024 |

|

| 12 |

|

|

| 15 |

|

|

| 1,741 |

|

|

| 13,933 |

|

|

| 8.2 | % |

2025 |

|

| 2 |

|

|

| 8 |

|

|

| 28 |

|

|

| 1,034 |

|

|

| 0.6 | % |

2026 |

|

| 17 |

|

|

| 27 |

|

|

| 620 |

|

|

| 9,964 |

|

|

| 5.9 | % |

2027 |

|

| 16 |

|

|

| 30 |

|

|

| 1,210 |

|

|

| 14,785 |

|

|

| 8.8 | % |

2028 |

|

| 12 |

|

|

| 22 |

|

|

| 1,025 |

|

|

| 11,184 |

|

|

| 6.6 | % |

2029 |

|

| 12 |

|

|

| 54 |

|

|

| 2,483 |

|

|

| 15,623 |

|

|

| 9.2 | % |

2030 and thereafter |

|

| 61 |

|

|

| 295 |

|

|

| 6,015 |

|

|

| 91,023 |

|

|

| 53.9 | % |

Our top tenants and brands at September 30, 2017, are listeddemand in the tables below. real estate market. During the three months ended June 30, 2022, we recognized a gain of $4.1 million on the sale of three properties, compared to a gain of $1.2 million on the sale of one property during the three months ended March 31, 2022. Our proactive asset management strategy includes determining to sell any of our properties where we believe the risk profile has changed and become misaligned with our then current risk-adjusted return objectives.

Other income (expenses)

The percentages are calculated basedchange in other income (expenses) during the three months ended June 30, 2022 was primarily due to $2.6 million of an unrealized foreign exchange gain recognized on the quarterly remeasurement of our $100 million CAD revolver borrowings, compared to a $1.1 million unrealized foreign exchange loss recognized during the three months ended March 31, 2022.

Net income and Net earnings per diluted share

|

| For the Three Months Ended |

| |||||||||||||

|

| June 30, |

|

| March 31, |

|

| Increase/(Decrease) |

| |||||||

(in thousands, except per share data) |

| 2022 |

|

| 2022 |

|

| $ |

|

| % |

| ||||

Net income |

| $ | 35,552 |

|

| $ | 28,441 |

|

| $ | 7,111 |

|

|

| 25.0 | % |

Net earnings per diluted share |

|

| 0.20 |

|

|

| 0.16 |

|

|

| 0.04 |

|

|

| 25.0 | % |

The increase in net income is primarily attributable to a $4.2 million increase in lease revenue associated with growth in our real estate portfolio, a $3.8 million increase in unrealized foreign exchange gains, and a $2.9 million increase in gain on sale of real estate, partially offset by a $1.4 million increase in impairment of investment in rental properties, a $1.2 million increase in depreciation and amortization, and a $1.0 million increase in interest expense.

GAAP net income includes items such as gain or loss on sale of real estate and provisions for impairment, among others, which can vary from quarter to quarter and impact period-over-period comparisons.

36

Six Months Ended June 30, 2022 Compared to Six Months Ended June 30, 2021

Lease Revenues, net

|

| For the Six Months Ended | |||||||||||||

|

| June 30, |

| Increase/(Decrease) | |||||||||||

(in thousands) |

| 2022 |

| 2021 |

| $ |

| % | |||||||

Contractual rental amounts billed for operating leases |

| $ | 171,901 |

|

| $ | 148,256 |

|

| $ | 23,645 |

|

| 15.9 | % |

Adjustment to recognize contractual operating lease |

|

| 10,111 |

|

|

| 9,533 |

|

|

| 578 |

|

| 6.1 | % |

Net write-offs of accrued rental income |

|

| (1,326 | ) |

|

| (442 | ) |

|

| (884 | ) |

| >100.0 | % |

Variable rental amounts earned |

|

| 477 |

|

|

| 205 |

|

|

| 272 |

|

| >100.0 | % |

Earned income from direct financing leases |

|

| 1,444 |

|

|

| 1,458 |

|

|

| (14 | ) |

| (1.0 | )% |

Interest income from sales-type leases |

|

| 29 |

|

|

| 29 |

|

|

| — |

|

| — | % |

Operating expenses billed to tenants |

|

| 8,998 |

|

|

| 8,584 |

|

|

| 414 |

|

| 4.8 | % |

Other income from real estate transactions |

|

| 176 |

|

|

| 33 |

|

|

| 143 |

|

| >100.0 | % |

Adjustment to revenue recognized for uncollectible |

|

| 44 |

|

|

| (199 | ) |

|

| 243 |

|

| >100.0 | % |

Total Lease revenues, net |

| $ | 191,854 |

|

| $ | 167,457 |

|

| $ | 24,397 |

|

| 14.6 | % |

The increase in Lease revenues, net was primarily attributable to growth in our real estate portfolio through property acquisitions closed since June 30, 2021. During the twelve months ended June 30, 2022, we invested $765.8 million, excluding capitalized acquisition costs, in 96 properties at a weighted average initial cash capitalization rate of 6.2%.

Operating Expenses

|

| For the Six Months Ended |

| |||||||||||||

|

| June 30, |

|

| Increase/(Decrease) |

| ||||||||||

(in thousands) |

| 2022 |

|

| 2021 | �� |

| $ |

|

| % |

| ||||

Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Depreciation and amortization |

| $ | 69,801 |

|

| $ | 61,938 |

|

| $ | 7,863 |

|

|

| 12.7 | % |

Property and operating expense |

|

| 9,740 |

|

|

| 9,177 |

|

|

| 563 |

|

|

| 6.1 | % |

General and administrative |

|

| 18,116 |

|

|

| 19,288 |

|

|

| (1,172 | ) |

|

| (6.1 | )% |

Provision for impairment of investment in rental properties |

|

| 1,380 |

|

|

| 2,012 |

|

|

| (632 | ) |

|

| (31.4 | )% |

Total operating expenses |

| $ | 99,037 |

|

| $ | 92,415 |

|

| $ | 6,622 |

|

|

| 7.2 | % |

Depreciation and amortization

The increase in depreciation and amortization for the six months ended June 30, 2022 was primarily due to growth in our real estate portfolio.

General and administrative

The decrease in general and administrative expenses mainly reflects decreased severance expense. During the six months ended June 30, 2021, we recognized severance associated with the departure of a named executive officer.

Provision for impairment of investment in rental properties

During the six months ended June 30, 2022, we recognized $1.4 million of impairment on our NTM Rent on a per property type basis divided by total NTM Rent. Late payments, non-payments or other unscheduled payments are not considered in the calculation. NTM Rent includes the impact of contractual rent escalations, excluding any potential variable rent increases that are based on CPI and/or the tenants’ sales volume.

Top Ten Tenants, by % of NTM Rent

Tenant |

| Property Type |

| % NTM Rent |

|

| Properties |

| ||

Red Lobster Hospitality LLC & Red Lobster Restaurants LLC |

| Retail |

|

| 4.3 | % |

|

| 25 |

|

Art Van Furniture, LLC |

| Retail |

|

| 3.9 | % |

|

| 9 |

|

Jack’s Family Restaurants LP |

| Retail |

|

| 3.4 | % |

|

| 36 |

|

Outback Steakhouse of Florida, LLC(1) |

| Retail |

|

| 3.1 | % |

|

| 24 |

|

Big Tex Trailer Manufacturing Inc. |

| Industrial/Retail |

|

| 2.7 | % |

|

| 17 |

|

Siemens Medical Solutions USA, Inc. & Siemens Corporation |

| Industrial |

|

| 2.6 | % |

|

| 2 |

|

Nestle' Dreyer's Ice Cream Company |

| Industrial |

|

| 2.5 | % |

|

| 1 |

|

Nationwide Mutual Insurance Company |

| Other |

|

| 2.3 | % |

|

| 2 |

|

Arkansas Surgical Hospital LLC |

| Healthcare |

|

| 2.3 | % |

|

| 1 |

|

Bob Evans Restaurants, LLC |

| Retail |

|

| 2.2 | % |

|

| 25 |

|

Total |

|

|

|

| 29.3 | % |

|

| 142 |

|

All Other |

|

|

|

| 70.7 | % |

|

| 335 |

|

|

|

Top Ten Brands, by % of NTM Rent

Brand |

| Property Type |

| % NTM Rent |

|

| Properties |

| ||

Bob Evans Farms(1) |

| Industrial/Retail |

|

| 4.3 | % |

|

| 27 |

|

Red Lobster |

| Retail |

|

| 4.3 | % |

|

| 25 |

|

Art Van Furniture |

| Retail |

|

| 3.9 | % |

|

| 9 |

|

Jack's Family Restaurants |

| Retail |

|

| 3.4 | % |

|

| 36 |

|

Taco Bell |

| Retail |

|

| 3.1 | % |

|

| 41 |

|

Wendy's |

| Retail |

|

| 2.9 | % |

|

| 35 |

|

Outback Steakhouse |

| Retail |

|

| 2.8 | % |

|

| 22 |

|

Big Tex Trailers |

| Industrial/Retail |

|

| 2.7 | % |

|

| 17 |

|

Siemens |

| Industrial |

|

| 2.6 | % |

|

| 2 |

|

Nestle' |

| Retail |

|

| 2.5 | % |

|

| 1 |

|

Total |

|

|

|

| 32.5 | % |

|

| 215 |

|

All Other |

|

|

|

| 67.5 | % |

|

| 262 |

|

|

|

As previously mentioned, the IDC approved certain updates to our Investment Policy following the regular annual review of the policy at the November 2017 meeting of our board of directors. As updated, our Investment Policy generally requires us to seek diversification of our investments. Based on the aggregate NTM rent of the properties in the portfolio, determined as of the date of the prior quarter end, new investments may not cause us to exceed:

5% in any single property,

8% leased to any single tenant or brand,

10% located in any single metropolitan statistical area, or

20% located in any single state.

We may exceed these diversification targets from time to time with the approval of the IDC. To avoid undue risk concentrations in any single asset class or category, long-term asset allocation will be set with the following target percentages and within the following ranges, although these ranges may be temporarily waived by the IDC:

|

|

| ||||

|

|

|

| |||

|

|

|

| |||

|

|

|

| |||

|

|

|

| |||

|

|

|

| |||

Our Investment Policy provides the Asset Manager with the authority to make any acquisition or sale of any property or group of related properties involving up to $50 million for any single or portfolio transaction, $75 million per cumulative tenant concentration, or $100 million per cumulative brand concentration on our behalf, without approval of the IDC, provided that any properties so acquired otherwise meet our Investment Policy and Property Selection Criteria, and any financing related to any such acquisitions does not violate our Leverage Policy (as defined below), as such are established by the IDC from time to time. Our Investment Policy permits investments in rental properties, that do not otherwise meet our Investment Policy or Property Selection Criteria withcompared to $2.0 million during the approval of the IDC.

Leverage Policy

In March of 2016, Moody’s Investors Service (“Moody’s”) assigned the Operating Company an investment grade credit rating of Baa3 with a stable outlook. Moody’s re-affirmed the investment grade credit rating in March 2017. The investment grade credit rating allowed us to take advantage of preferential borrowing margins on our outstanding debt, including the $800 million credit facility we entered into on June 23, 2017. The investment grade credit ratings will also allow us more attractive access to the debt private placement markets. The rating is based on a number of factors, including an assessment of our financial strength, portfolio size and diversification, credit and operating metrics, corporate governance policies, and sustainability of cash flow and earnings. We are strongly committed to maintaining modest leverage, commensurate with our investment grade rating. While Moody’s utilizes other factors outside of our leverage ratio, our leverage policy (“Leverage Policy”) is to maintain a leverage ratio in the 35% to 45% range based on the market value of assets, recognizing that the actual leverage ratio will vary over time and there may be opportunistic reasons to exceed a 45% leverage ratio; provided, however, that we cannot exceed a 50% leverage ratio without the approval of the IDC.

To reduce its exposure to variable rate debt, the Operating Company enters into interest rate swap agreements to fix the rate of interest as a hedge against interest rate fluctuations. These interest rate hedges have staggered maturities to reduce the exposure to interest rate fluctuations in any one year, and generally extend up to 10 years. The interest rate swaps are applied against a pool of debt, which offers flexibility in maintaining our hedge designation concurrent with our ongoing capital market activity. We limit our total exposure to floating rate debt to no more than 5% of the market value of total assets, measured at quarter end.

During the ninesix months ended SeptemberJune 30, 2017, we added $150 million of unsecured Senior Notes (as defined below) to our capital structure. The Senior Notes bear interest at a fixed of 4.84% per annum, with a 10 year maturity. We strategically used this channel of long-term, fixed rate debt capital to help mitigate interest rate risk, lengthen our maturity profile, and diversify our sources of debt capital.

The IDC reviews our Leverage Policy at least annually, however, depending on market conditions and other factors, they may change our Leverage Policy from time to time.

As of September 30, 2017, our total outstanding indebtedness was $910.1 million, and the ratio of our total indebtedness to the market value of our assets was approximately 36.5%.

Determined Share Value

Our shares of common stock are sold by us in our ongoing private offering at a price equal to a determined share value (the “Determined Share Value”), which is established quarterly by the IDC based on the net asset value (“NAV”) of our portfolio, input from management, and such other factors as the IDC may determine. Shares of our common stock are also sold pursuant to our DRIP, and repurchased by us pursuant to our share redemption program, at a price based upon the Determined Share Value. For additional information regarding our valuation policy and procedures, please see the section titled “Determined Share Value” in Item 1 of our Form 10.2021. The following table presents our Determined Share Value for each period indicated below, together with the corresponding NAV as of the preceding quarter-end:

Period |

| NAV as of |

| Determined Share Value |

|

| NAV per share |

| ||

November 1, 2017 - January 31, 2018 |

| September 30, 2017 |

| $ | 81.00 |

|

| $ | 80.55 |

|

August 1, 2017 - October 31, 2017 |

| June 30, 2017 |

| $ | 80.00 |

|

| $ | 79.90 |

|

The adjustments to NAV per share in arriving at the Determined Share Valueimpairment charges for the periods presented above account forrespective periods:

|

| For the Six Months Ended |

| |||||

|

| June 30, |

| |||||

(in thousands, except number of properties) |

| 2022 |

|

| 2021 |

| ||

Number of properties |

|

| 1 |

|

|

| 1 |

|

Carrying value prior to impairment charge |

| $ | 3,674 |

|

| $ | 2,818 |

|

Fair value |

|

| 2,294 |

|

|

| 806 |

|

Impairment charge |

| $ | 1,380 |

|

| $ | 2,012 |

|

The timing and amount of impairment fluctuates from period to period depending on the inherent imprecisionspecific facts and circumstances.

37

Other income (expenses)

|

| For the Six Months Ended | |||||||||||||||||||

|

| June 30, |

| Increase/(Decrease) | |||||||||||||||||

(in thousands) |

| 2022 |

| 2021 |

| $ |

| % | |||||||||||||

Other income (expenses) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

Interest income |

| $ |

| — |

|

|

| $ | 11 |

|

|

| $ | (11 |

| ) |

| <(100.0 | )% | ||

Interest expense |

|

| (34,784 |

| ) |

|

| (31,538 |

| ) |

|

|

| 3,246 |

|

|

| 10.3 | % | ||

Cost of debt extinguishment |

|

|

| — |

|

|

|

| (126 |

| ) |

|

| (126 |

| ) |

| <(100.0 | )% | ||

Gain on sale of real estate |

|

|

| 5,267 |

|

|

|

|

| 8,571 |

|

|

|

| (3,304 |

| ) |

| (38.5 | )% | |

Income taxes |

|

| (813 |

| ) |

|

| (714 |

| ) |

|

| 99 |

|

|

| 13.9 | % | |||

Change in fair value of earnout liability |

|

|

| — |

|

|

|

| (4,480 |

| ) |

|

|

| 4,480 |

|

|

| <(100.0 | )% | |

Other income |

|

|

| 1,506 |

|

|

|

| 14 |

|

|

|

|

| 1,492 |

|

|

| >100.0 | % | |

Interest expense

The increase in the valuation estimates. In February 2018, the IDC will review the NAV calculations as of December 31, 2017, and will assess whether adjustments to the current Determined Share Value of $81.00 are appropriate.

The following table provides a breakdown of the major components of our estimated NAV and NAV per share amounts as of September 30, 2017 and June 30, 2017 (in thousands, except per share amounts):

NAV as of: |

| September 30, 2017 |

|

| June 30, 2017 |

| ||

Investment in rental property |

| $ | 2,502,140 |

|

| $ | 2,351,989 |

|

Debt |

|

| (909,416 | ) |

|

| (883,112 | ) |

Other assets and liabilities, net |

|

| 1,348 |

|

|

| 34,790 |

|

NAV |

| $ | 1,594,072 |

|

| $ | 1,503,667 |

|

Number of outstanding shares, including noncontrolling interests |

| $ | 19,790 |

|

| $ | 18,820 |

|

NAV per share |

| $ | 80.55 |

|

| $ | 79.90 |

|

The following table details the implied market capitalization rates (shown on a weighted average basis) used to value the investment in rental property, by property type, as of September 30, 2017 and June 30, 2017, supporting the Determined Share Value in effect for the periods of November 1, 2017 through January 31, 2018, and August 1, 2017 through October 31, 2017, respectively:

Market capitalization rates, as of: |

| Retail |

|

| Industrial |

|

| Healthcare |

|

| Other |

|

| Portfolio Total |

| |||||

September 30, 2017 |

|

| 6.38 | % |

|

| 6.96 | % |

|

| 6.95 | % |

|

| 7.11 | % |

|

| 6.75 | % |

June 30, 2017 |

|

| 6.40 | % |

|

| 6.96 | % |

|

| 6.87 | % |

|

| 7.05 | % |

|

| 6.73 | % |

While we believe our assumptions are reasonable, a change in these assumptions would impact the calculation of the value of our real estate investments. For example, assuming all other factors remain unchanged,interest expense reflects an increase in theour weighted average implied market capitalization rate usedcost of borrowings combined with increased average outstanding borrowings during the six months ended June 30, 2022 compared to during the six months ended June 30, 2021. Since June 30, 2021 we increased total outstanding borrowings by $360.4 million to partially fund our acquisitions. Of our $1.9 billion of total outstanding indebtedness, approximately $200.5 million, or 10.8% is variable, and therefore subject to the impact of fluctuations in interest rates.

Gain on sale of real estate

Our recognition of a gain or loss on the sale of real estate varies from transaction to transaction based on fluctuations in asset prices and demand in the real estate market. During the six months ended June 30, 2022, we recognized a gain of $5.3 million on the sale of four properties, compared to a gain of $8.6 million on the sale of 19 properties during the six months ended June 30, 2021. Our proactive asset management strategy includes determining to sell any of our properties where we believe the risk profile has changed and become misaligned with our then current risk-adjusted return objectives.

Change in fair value of earnout liability

The fair value of the earnout liability was remeasured each reporting period, with changes recorded as Change in fair value of September 30, 2017,earnout liability in the Condensed Consolidated Statements of 0.25%, would result in a decreaseIncome and Comprehensive Income. All earnout milestones were achieved during the year ended December 31, 2021, therefore there is no change in the fair value of the earnout liability during the six months ended June 30, 2022. The change in the fair value of the earnout liability during the six months ended June 30, 2021 reflected an increase in our investmentshare price as compared to December 31, 2020.

Other income

The increase in rental property of 3.6%, and our NAV per share would have been $76.03.

Distributions and Distribution Reinvestment

At its November 7, 2017, meeting, our board of directors declared monthly distributions of $0.415 per shareother income during the six months ended June 30, 2022 was primarily due to a $1.5 million unrealized foreign exchange gain recognized on the quarterly remeasurement of our common stock and unit$100 million CAD revolver borrowings. The specific CAD revolver borrowings were drawn during the first quarter of membership interest in2022, with no similar activity during the Operating Company to be paid by us to our stockholders and members of the Operating Company (other than us) of record prior to the end of November 2017, December 2017, and January 2018:

Dividend Per Share/Unit |

|

| Record Date |

| Payment Date (on or before) | |

$ | 0.415 |

|

| November 29, 2017 |

| December 15, 2017 |

$ | 0.415 |

|

| December 28, 2017 |

| January 15, 2018 |

$ | 0.415 |

|

| January 30, 2018 |

| February 15, 2018 |

Investors may purchase additional shares of our common stock by electing to reinvest their distributions through our DRIP. The purchase price for shares of our common stock acquired through our DRIP will be 98% of the then-current Determined Share Value. Please refer to Item 11. “Description of Registrant’s Securities to Be Registered” of our Form 10 for additional discussion of our DRIP.

The following table summarizes distributions paid in cash and pursuant to our DRIP for the ninesix months ended SeptemberJune 30, 2017 (in thousands).2021.

Net income and Net earnings per diluted share

Month |

| Year |

| Cash Distribution - Common Stockholders |

|

| Cash Distribution - Membership Units |

|

| Distribution Paid Pursuant to DRIP on Common Stock (1) |

|

| Distribution Paid Pursuant to DRIP on Membership Units (1) |

|

| Total Amount of Distribution |

| |||||

January |

| 2017 |

| $ | 3,319 |

|

| $ | 488 |

|

| $ | 2,738 |

|

| $ | 98 |

|

| $ | 6,643 |

|

February |

| 2017 |

|

| 3,394 |

|

|

| 488 |

|

|

| 2,836 |

|

|

| 98 |

|

|

| 6,816 |

|

March |

| 2017 |

|

| 3,522 |

|

|

| 493 |

|

|

| 2,972 |

|

|

| 99 |

|

|

| 7,086 |

|

April |

| 2017 |

|

| 3,555 |

|

|

| 493 |

|

|

| 3,068 |

|

|

| 99 |

|

|

| 7,215 |

|

May |

| 2017 |

|

| 3,618 |

|

|

| 493 |

|

|

| 3,167 |

|

|

| 99 |

|

|

| 7,377 |

|

June |

| 2017 |

|

| 3,680 |

|

|

| 493 |

|

|

| 3,220 |

|

|

| 99 |

|

|

| 7,492 |

|

July |

| 2017 |

|

| 3,742 |

|

|

| 493 |

|

|

| 3,296 |

|

|

| 99 |

|

|

| 7,630 |

|

August |

| 2017 |

|

| 3,815 |

|

|

| 512 |

|

|

| 3,378 |

|

|

| 122 |

|

|

| 7,827 |

|

September |

| 2017 |

|

| 3,883 |

|

|

| 512 |

|

|

| 3,420 |

|

|

| 123 |

|

|

| 7,938 |

|

TOTAL |

|

|

| $ | 32,528 |

|

| $ | 4,465 |

|

| $ | 28,095 |

|

| $ | 936 |

|

| $ | 66,024 |

|

|

| For the Six Months Ended |

| |||||||||||||

|

| June 30, |

|

| Increase/(Decrease) |

| ||||||||||

(in thousands, except per share data) |

| 2022 |

|

| 2021 |

|

| $ |

|

| % |

| ||||

Net income |

| $ | 63,993 |

|

| $ | 46,780 |

|

| $ | 17,213 |

|

|

| 36.8 | % |

Net earnings per diluted share |

|

| 0.36 |

|

|

| 0.30 |

|

|

| 0.06 |

|

|

| 20.0 | % |

|

|

The following table summarizes our distributions paid during the nine months ended September 30, 2017 and 2016, including the sourceincrease in net income is primarily due to revenue growth of distributions$24.4 million, a $4.5 million increase in change in fair value of earnout liability, a $1.5 million increase in unrealized foreign exchange gain, and a comparison against FFO (in thousands).

|

| For the nine months ended |

| |||||

|

| September 30, |

| |||||

|

| 2017 |

|

| 2016 |

| ||

Distributions: |

|

|

|

|

|

|

|

|

Paid in cash |

| $ | 37,929 |

|

| $ | 31,229 |

|

Reinvested in shares |

|

| 28,095 |