Exhibit 5 Jesus González President CEMEX SCAC

This presentation contains forward-looking statements within the meaning of the U.S. federal securities laws. We intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements within the meaning of the U.S. federal securities laws. In some cases, these statements can be identified by the use of forward-looking words such as“may,”“assume,”“might,”“should,”“could,”“continue,”“would,”“can,”“consider,”“anticipate,”“estimate,”“expect,”“envision,”“plan,”“believe,”“foresee,”“predict,”“potential,” “target,”“strategy,”“intend,”“aimed” or other similar words. These forward-looking statements reflect, as of the date such forward-looking statements are made, or unless otherwise indicated, our current expectations and projections about future events based on our knowledge of present facts and circumstances and assumptions about future events. These statements necessarily involve risks and uncertainties that could cause actual results to differ materially from our expectations. Some of the risks, uncertainties and other important factors that could cause results to differ, or that otherwise could have an impact on us or our consolidated entities, include, but are not limited to: the impact of pandemics, epidemics or outbreaks of infectious diseases and the response of governments and other third parties, including with respect to the novel strain of the coronavirus identified in China in late 2019(“COVID-19”), which have affected and may continue to adversely affect, among other matters, the ability of our operating facilities to operate at full or any capacity, supply chains, international operations, availability of liquidity, investor confidence and consumer spending, as well as availability of, and demand for, our products and services; the cyclical activity of the construction sector; our exposure to other sectors that impact our and ourclients’ businesses, such as, but not limited to, the energy sector; availability of raw materials and related fluctuating prices; competition in the markets in which we offer our products and services; general political, social, health, economic and business conditions in the markets in which we operate or that affect our operations and any significant economic, health, political or social developments in those markets, as well as any inherent risks to international operations; the regulatory environment, including environmental, energy, tax, antitrust, and acquisition-related rules and regulations; our ability to satisfy our obligations under our material debt agreements, the indentures that govern our outstanding senior secured notes and our other debt instruments and financial obligations, including our subordinated notes with no fixed maturity; the availability of short-term credit lines or working capital facilities, which can assist us in connection with market cycles; the impact of our below investment grade debt rating on our cost of capital and on the cost of the products and services we purchase; loss of reputation of our brands; our ability to consummate asset sales, fully integrate newly acquired businesses, achieve cost-savings from our cost-reduction initiatives, implement our pricing initiatives for our products and generally meet our“OperationResilience”strategy’s goals; the increasing reliance on information technology infrastructure for our sales, invoicing, procurement, financial statements and other processes that can adversely affect our sales and operations in the event that the infrastructure does not work as intended, experiences technical difficulties or is subjected to cyber-attacks; changes in the economy that affect demand for consumer goods, consequently affecting demand for our products and services; weather conditions, including but not limited to, excessive rain and snow, and disasters such as earthquakes and floods; trade barriers, including tariffs or import taxes and changes in existing trade policies or changes to, or withdrawals from, free trade agreements, including the United States-Mexico-Canada Agreement; terrorist and organized criminal activities as well as geopolitical events; declarations of insolvency or bankruptcy, or becoming subject to similar proceedings; natural disasters and other unforeseen events (including global health hazards such as COVID-19); and the other risks and uncertainties described in the our public filings. Readers are urged to read this presentation and carefully consider the risks, uncertainties and other factors that affect our business and operations. The information contained in this presentation is subject to change without notice, and we are not obligated to publicly update or revise forward-looking statements after the date hereof or to reflect the occurrence of anticipated or unanticipated events or circumstances. Readers should review future reports filed by us with the U.S. Securities and Exchange Commission and the Mexican Stock Exchange (Bolsa Mexicana de Valores). This presentation also includes statistical data regarding the production, distribution, marketing and sale of cement, ready mix concrete, clinker and aggregates We generated some of this data internally, and some was obtained from independent industry publications and reports that we believe to be reliable sources We have not independently verified this data nor sought the consent of any organizations to refer to their reports in this presentation. UNLESS OTHERWISE NOTED, ALL FIGURES ARE PRESENTED IN DOLLARS, BASED ON INTERNATIONAL FINANCIAL REPORTING STANDARDS, AS APPLICABLE Copyright CEMEX, S.A.B. de C.V. and its subsidiariesThis presentation contains forward-looking statements within the meaning of the U.S. federal securities laws. We intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements within the meaning of the U.S. federal securities laws. In some cases, these statements can be identified by the use of forward-looking words such as“may,”“assume,”“might,”“should,”“could,”“continue,”“would,”“can,”“consider,”“anticipate,”“estimate,”“expect,”“envision,”“plan,”“believe,”“foresee,”“predict,”“potential,” “target,”“strategy,”“intend,”“aimed” or other similar words. These forward-looking statements reflect, as of the date such forward-looking statements are made, or unless otherwise indicated, our current expectations and projections about future events based on our knowledge of present facts and circumstances and assumptions about future events. These statements necessarily involve risks and uncertainties that could cause actual results to differ materially from our expectations. Some of the risks, uncertainties and other important factors that could cause results to differ, or that otherwise could have an impact on us or our consolidated entities, include, but are not limited to: the impact of pandemics, epidemics or outbreaks of infectious diseases and the response of governments and other third parties, including with respect to the novel strain of the coronavirus identified in China in late 2019(“COVID-19”), which have affected and may continue to adversely affect, among other matters, the ability of our operating facilities to operate at full or any capacity, supply chains, international operations, availability of liquidity, investor confidence and consumer spending, as well as availability of, and demand for, our products and services; the cyclical activity of the construction sector; our exposure to other sectors that impact our and ourclients’ businesses, such as, but not limited to, the energy sector; availability of raw materials and related fluctuating prices; competition in the markets in which we offer our products and services; general political, social, health, economic and business conditions in the markets in which we operate or that affect our operations and any significant economic, health, political or social developments in those markets, as well as any inherent risks to international operations; the regulatory environment, including environmental, energy, tax, antitrust, and acquisition-related rules and regulations; our ability to satisfy our obligations under our material debt agreements, the indentures that govern our outstanding senior secured notes and our other debt instruments and financial obligations, including our subordinated notes with no fixed maturity; the availability of short-term credit lines or working capital facilities, which can assist us in connection with market cycles; the impact of our below investment grade debt rating on our cost of capital and on the cost of the products and services we purchase; loss of reputation of our brands; our ability to consummate asset sales, fully integrate newly acquired businesses, achieve cost-savings from our cost-reduction initiatives, implement our pricing initiatives for our products and generally meet our“OperationResilience”strategy’s goals; the increasing reliance on information technology infrastructure for our sales, invoicing, procurement, financial statements and other processes that can adversely affect our sales and operations in the event that the infrastructure does not work as intended, experiences technical difficulties or is subjected to cyber-attacks; changes in the economy that affect demand for consumer goods, consequently affecting demand for our products and services; weather conditions, including but not limited to, excessive rain and snow, and disasters such as earthquakes and floods; trade barriers, including tariffs or import taxes and changes in existing trade policies or changes to, or withdrawals from, free trade agreements, including the United States-Mexico-Canada Agreement; terrorist and organized criminal activities as well as geopolitical events; declarations of insolvency or bankruptcy, or becoming subject to similar proceedings; natural disasters and other unforeseen events (including global health hazards such as COVID-19); and the other risks and uncertainties described in the our public filings. Readers are urged to read this presentation and carefully consider the risks, uncertainties and other factors that affect our business and operations. The information contained in this presentation is subject to change without notice, and we are not obligated to publicly update or revise forward-looking statements after the date hereof or to reflect the occurrence of anticipated or unanticipated events or circumstances. Readers should review future reports filed by us with the U.S. Securities and Exchange Commission and the Mexican Stock Exchange (Bolsa Mexicana de Valores). This presentation also includes statistical data regarding the production, distribution, marketing and sale of cement, ready mix concrete, clinker and aggregates We generated some of this data internally, and some was obtained from independent industry publications and reports that we believe to be reliable sources We have not independently verified this data nor sought the consent of any organizations to refer to their reports in this presentation. UNLESS OTHERWISE NOTED, ALL FIGURES ARE PRESENTED IN DOLLARS, BASED ON INTERNATIONAL FINANCIAL REPORTING STANDARDS, AS APPLICABLE Copyright CEMEX, S.A.B. de C.V. and its subsidiaries

YTD EBITDA growth driven by volume and pricing strategy EBITDA Variation +58% +54% 18 0 0 247 241 83 -10 -6 156 1H20 Volume Price Variable costs Cement & Fixed costs 1H21 FX 1H21 & freight Clinker imports & others l-t-l 24.0% +4.6pp 28.6% EBITDA marginYTD EBITDA growth driven by volume and pricing strategy EBITDA Variation +58% +54% 18 0 0 247 241 83 -10 -6 156 1H20 Volume Price Variable costs Cement & Fixed costs 1H21 FX 1H21 & freight Clinker imports & others l-t-l 24.0% +4.6pp 28.6% EBITDA margin

Region is growing again with more geographic diversification EBITDA Quarterly EBITDA EBITDA by country 1H21: COL -33% 17% 575 +18% 78% Dom. 27% TCL Republic 15% 455 8% 385 PAN COVID 36% 12% 21% lockdowns GUA OTHER 23% 6% 2013: 5% COL 53% -12% -29% 9% Dom. 18% L12M 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 2019 Avg. Republic PAN 16% 4% 2Q21 2010-2018 OTHER GUA 4

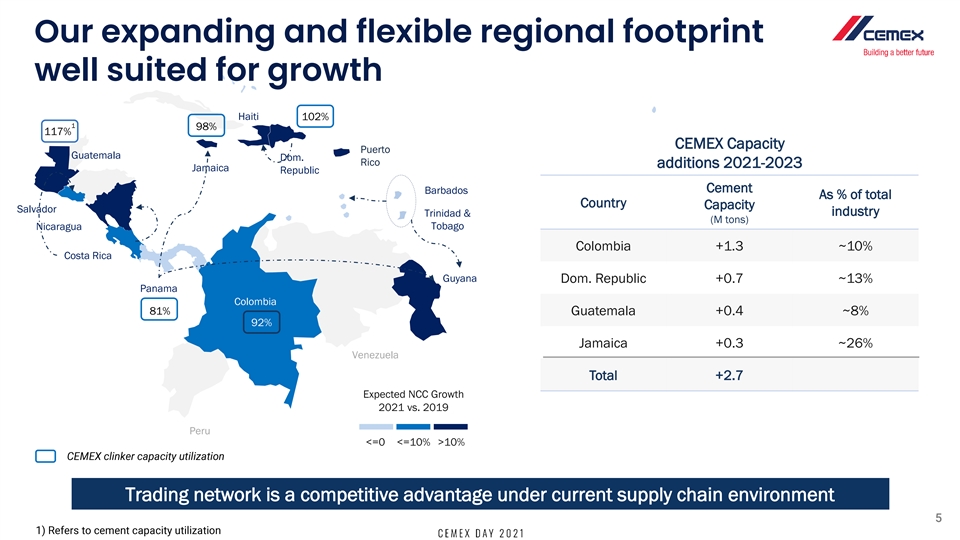

Our expanding and flexible regional footprint well suited for growth Haiti 102% 1 98% 117% CEMEX Capacity Puerto Guatemala Dom. Rico additions 2021-2023 Jamaica Republic Cement Barbados As % of total Country Capacity Salvador industry Trinidad & (M tons) Nicaragua Tobago Colombia +1.3 ~10% Costa Rica Guyana Dom. Republic +0.7 ~13% Panama Colombia 81% Guatemala +0.4 ~8% 92% Jamaica +0.3 ~26% Venezuela Total +2.7 Expected NCC Growth 2021 vs. 2019 Peru <=0 <=10% >10% Trading network is a competitive advantage under current supply chain environment 5Our expanding and flexible regional footprint well suited for growth Haiti 102% 1 98% 117% CEMEX Capacity Puerto Guatemala Dom. Rico additions 2021-2023 Jamaica Republic Cement Barbados As % of total Country Capacity Salvador industry Trinidad & (M tons) Nicaragua Tobago Colombia +1.3 ~10% Costa Rica Guyana Dom. Republic +0.7 ~13% Panama Colombia 81% Guatemala +0.4 ~8% 92% Jamaica +0.3 ~26% Venezuela Total +2.7 Expected NCC Growth 2021 vs. 2019 Peru <=0 <=10% >10% Trading network is a competitive advantage under current supply chain environment 5

Introducing Dominican Republic: now largest market in region EBITDA ▪ Remittances growing ~40% YTD Aug supporting Millions of USD +92% self construction 117 ▪ Strong construction projects pipeline for ~$7 B 61 for the next 5 years ▪ Formal housing backed by growth in mortgages 2018 L12M (+11% YTD Aug) 2Q21 28.1% +13.4pp 4 4 4 41.5 1.5 1.5 1.5% % % % 41.5% ▪ Acceleration in tourism-related projects EBITDA Margin Clinker demand CAGR ▪ Exports flexibility to serve Caribbean markets Million tons per year +9% 5.1 3.9 ▪ Assets include: 1 cement plant, 3 ready-mix 3.6 DR 2.9 plants, 1 aggregates quarry, and 2 cement 1 1.5 terminals HAI 1.0 2018 L12M Clinker 2Q21 demand As % of industry 98% 128% capacity 6Introducing Dominican Republic: now largest market in region EBITDA ▪ Remittances growing ~40% YTD Aug supporting Millions of USD +92% self construction 117 ▪ Strong construction projects pipeline for ~$7 B 61 for the next 5 years ▪ Formal housing backed by growth in mortgages 2018 L12M (+11% YTD Aug) 2Q21 28.1% +13.4pp 4 4 4 41.5 1.5 1.5 1.5% % % % 41.5% ▪ Acceleration in tourism-related projects EBITDA Margin Clinker demand CAGR ▪ Exports flexibility to serve Caribbean markets Million tons per year +9% 5.1 3.9 ▪ Assets include: 1 cement plant, 3 ready-mix 3.6 DR 2.9 plants, 1 aggregates quarry, and 2 cement 1 1.5 terminals HAI 1.0 2018 L12M Clinker 2Q21 demand As % of industry 98% 128% capacity 6

Jesus González President CEMEX SCAC 7Jesus González President CEMEX SCAC 7