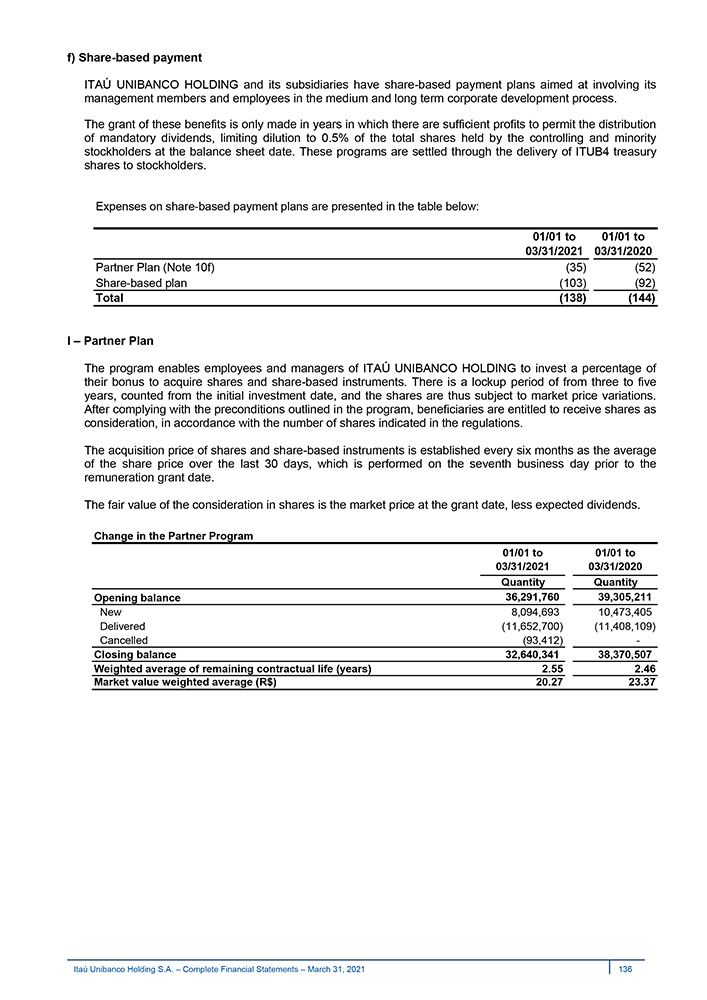

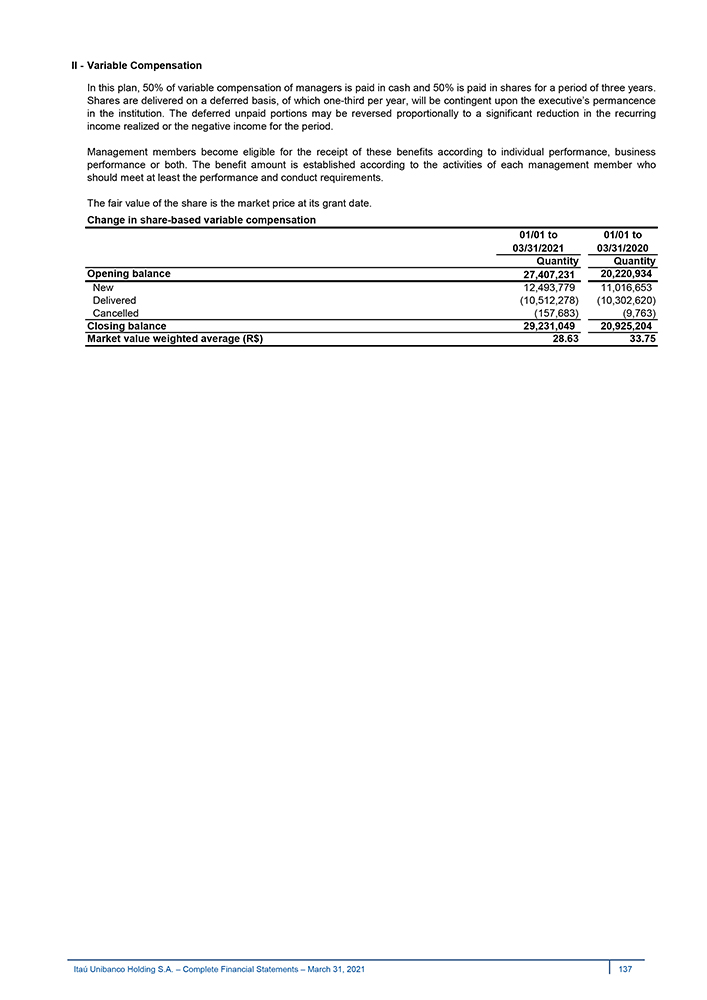

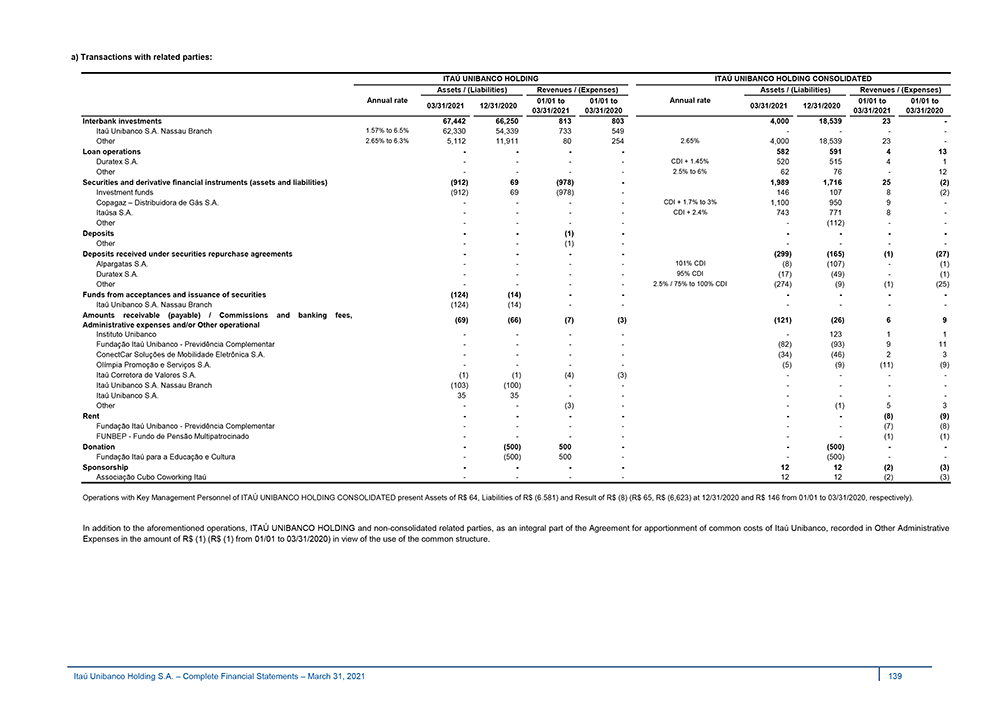

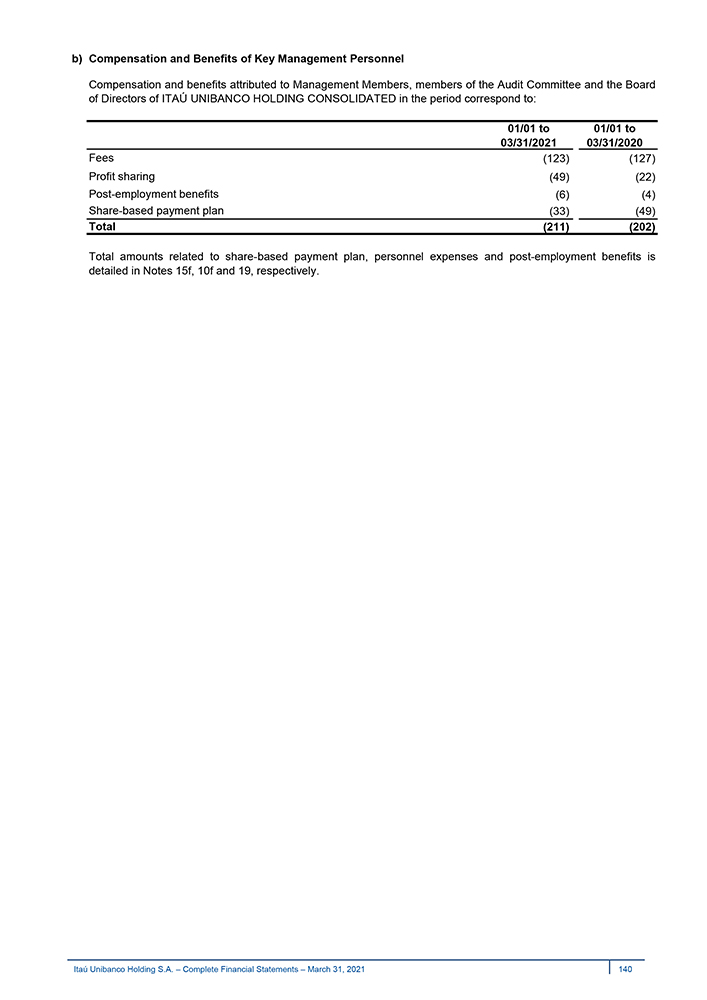

Exhibit 99.1

1Q 21 Management discussion & analysis and complete financial statements First quarter of 2021

Contents Management discussion & analysis Page 03 Executive Summary 03 Income Statement and Balance Sheet Analysis 11 Managerial Financial Margin 12 Cost of Credit 13 Credit Quality 15 Commissions and Fees & Result from Insurance 17 Result from Insurance, Pension Plan and Premium Bonds 19 Non-interest Expenses 20 Balance Sheet 22 Credit Portfolio 23 Funding 25 Capital, Liquidity and Market Ratios 26 Results by Business Segments 27 Results by Region—Brazil and Latin America 29 Activities Abroad 30 Additional Information 31 Itaú Unibanco Shares 32 Comparison between BRGAAP and IFRS 33 Glossary 35 Independent Auditor’s Report 37 Complete financial statements Page 39

1Q 21 Management discussion & analysis First quarter of 2021

(This page was intentionally left blank) Itaú Unibanco Holding S.A. 04

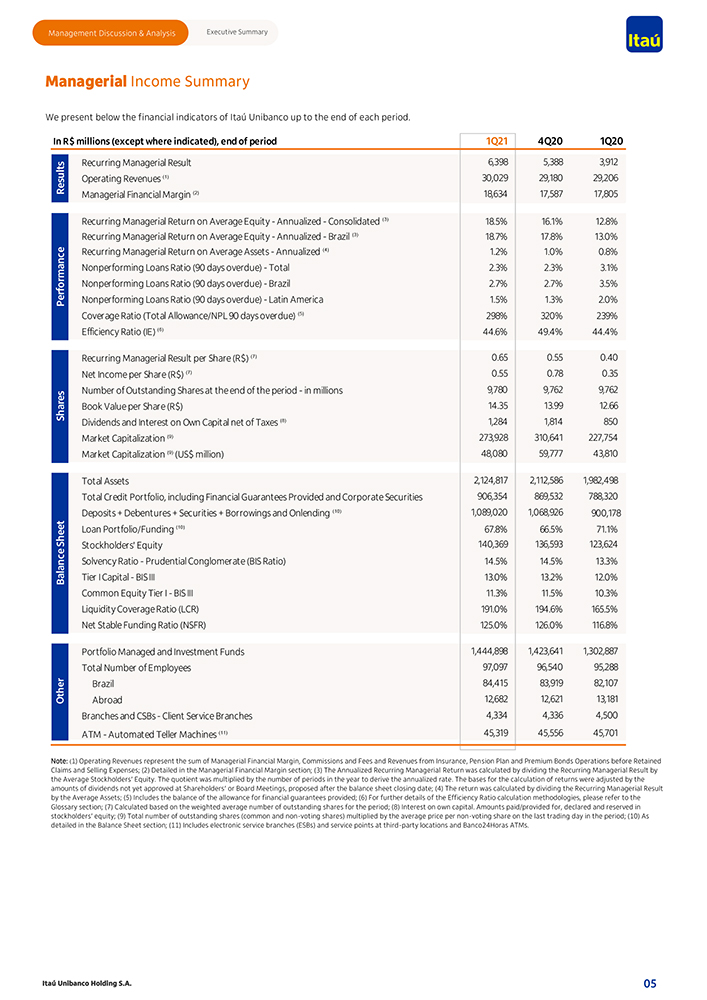

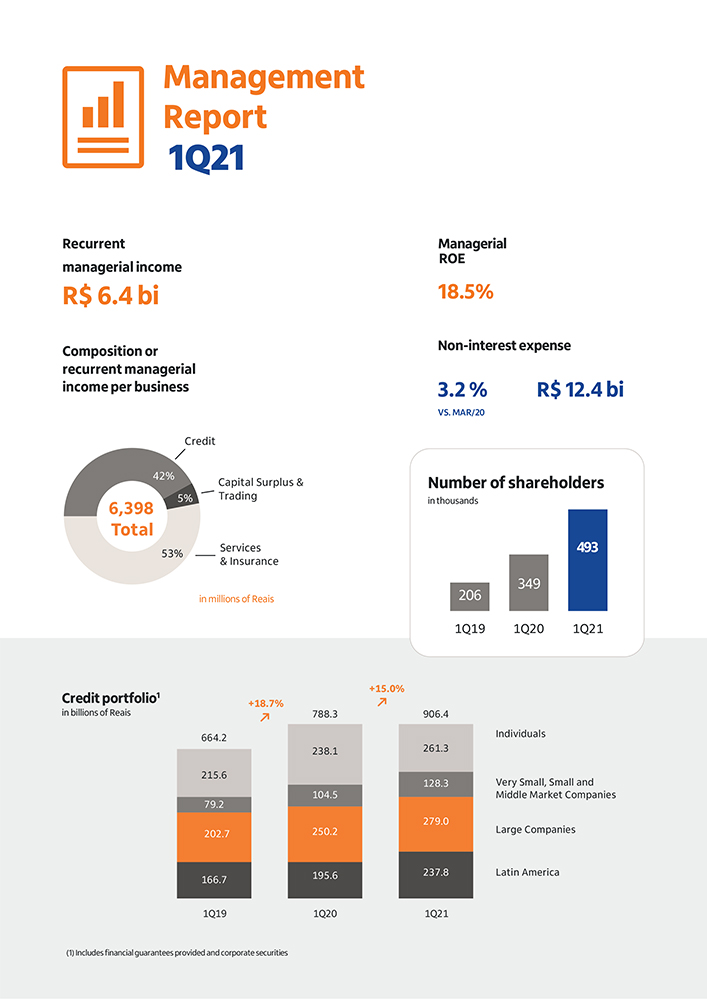

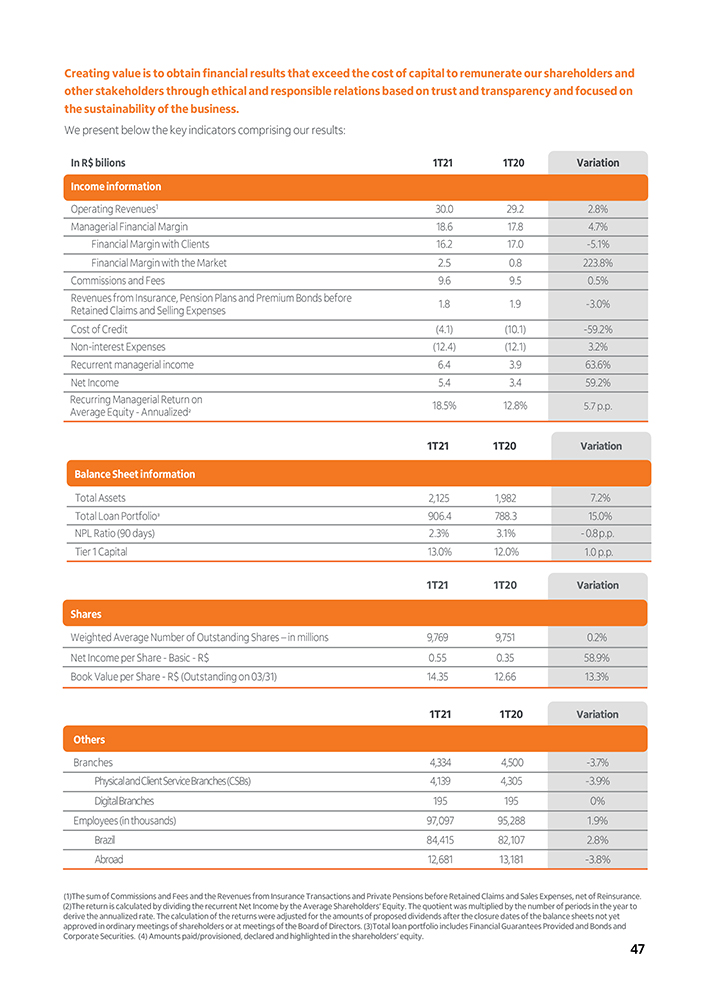

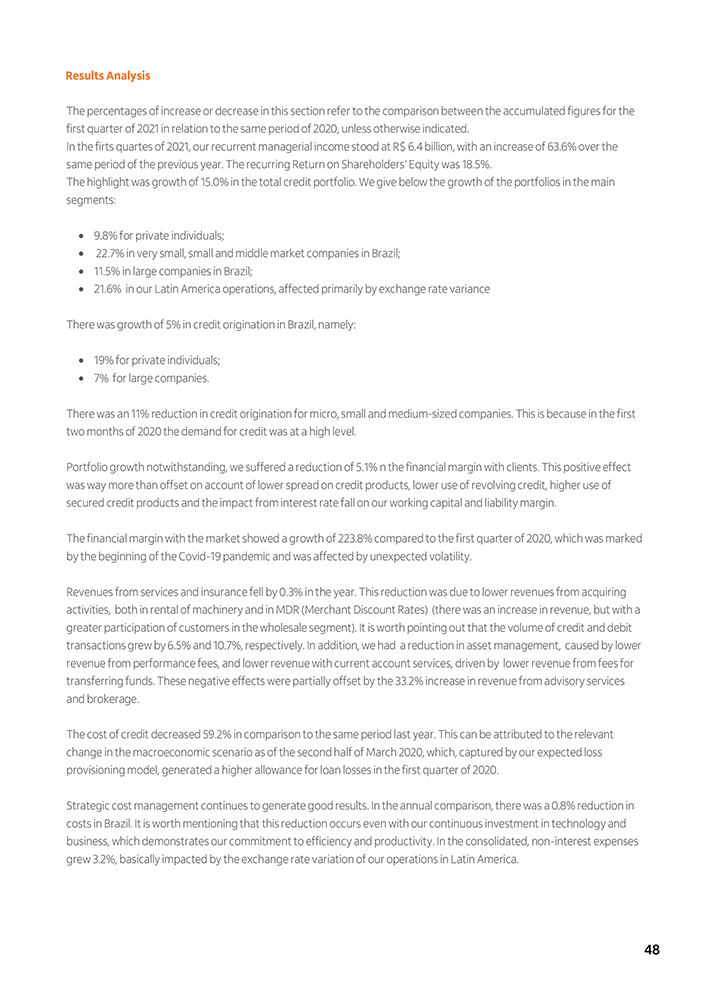

Management Discussion & Analysis Executive Summary Managerial Income Summary We present below the financial indicators of Itaú Unibanco up to the end of each period. In R$ millions (except where indicated), end of period 1Q21 4Q20 1Q20 Recurring Managerial Result 6,398 5,388 3,912 Res u lts Operating Revenues (1) 30,029 29,180 29,206 Managerial Financial Margin (2) 18,634 17,587 17,805 Recurring Managerial Return on Average Equity—Annualized—Consolidated (3) 18.5% 16.1% 12.8% Recurring Managerial Return on Average Equity—Annualized—Brazil (3) 18.7% 17.8% 13.0% Recurring Managerial Return on Average Assets—Annualized (4) 1.2% 1.0% 0.8% Nonperforming Loans Ratio (90 days overdue)—Total 2.3% 2.3% 3.1% Nonperforming Loans Ratio (90 days overdue)—Brazil 2.7% 2.7% 3.5% Per f orm a nce Nonperforming Loans Ratio (90 days overdue)—Latin America 1.5% 1.3% 2.0% Coverage Ratio (Total Allowance/NPL 90 days overdue) (5) 298% 320% 239% Efficiency Ratio (IE) (6) 44.6% 49.4% 44.4% Recurring Managerial Result per Share (R$) (7) 0.65 0.55 0.40 Net Income per Share (R$) (7) 0.55 0.78 0.35 Number of Outstanding Shares at the end of the period—in millions 9,780 9,762 9,762 S h ar e s Book Value per Share (R$) 14.35 13.99 12.66 Dividends and Interest on Own Capital net of Taxes (8) 1,284 1,814 850 Market Capitalization (9) 273,928 310,641 227,754 Market Capitalization (9) (US$ million) 48,080 59,777 43,810 Total Assets 2,124,817 2,112,586 1,982,498 Total Credit Portfolio, including Financial Guarantees Provided and Corporate Securities 906,354 869,532 788,320 Deposits + Debentures + Securities + Borrowings and Onlending (10) 1,089,020 1,068,926 900,178 Loan Portfolio/Funding (10) 67.8% 66.5% 71.1% Stockholders’ Equity 140,369 136,593 123,624 Solvency Ratio—Prudential Conglomerate (BIS Ratio) 14.5% 14.5% 13.3% Balanc e S hee t Tier I Capital—BIS III 13.0% 13.2% 12.0% Common Equity Tier I—BIS III 11.3% 11.5% 10.3% Liquidity Coverage Ratio (LCR) 191.0% 194.6% 165.5% Net Stable Funding Ratio (NSFR) 125.0% 126.0% 116.8% Portfolio Managed and Investment Funds 1,444,898 1,423,641 1,302,887 Total Number of Employees 97,097 96,540 95,288 Brazil 84,415 83,919 82,107 Abroad 12,682 12,621 13,181 Branches and CSBs—Client Service Branches 4,334 4,336 4,500 ATM—Automated Teller Machines (11) 45,319 45,556 45,701 Note: (1) Operating Revenues represent the sum of Managerial Financial Margin, Commissions and Fees and Revenues from Insurance, Pension Plan and Premium Bonds Operations before Retained Claims and Selling Expenses; (2) Detailed in the Managerial Financial Margin section; (3) The Annualized Recurring Managerial Return was calculated by dividing the Recurring Managerial Result by the Average Stockholders’ Equity. The quotient was multiplied by the number of periods in the year to derive the annualized rate. The bases for the calculation of returns were adjusted by the amounts of dividends not yet approved at Shareholders’ or Board Meetings, proposed after the balance sheet closing date; (4) The return was calculated by dividing the Recurring Managerial Result by the Average Assets; (5) Includes the balance of the allowance for financial guarantees provided; (6) For further details of the Efficiency Ratio calculation methodologies, please refer to the Glossary section; (7) Calculated based on the weighted average number of outstanding shares for the period; (8) Interest on own capital. Amounts paid/provided for, declared and reserved in stockholders’ equity; (9) Total number of outstanding shares (common and non-voting shares) multiplied by the average price per non-voting share on the last trading day in the period; (10) As detailed in the Balance Sheet section; (11) Includes electronic service branches (ESBs) and service points at third-party locations and Banco24Horas ATMs. Itaú Unibanco Holding S.A. 05

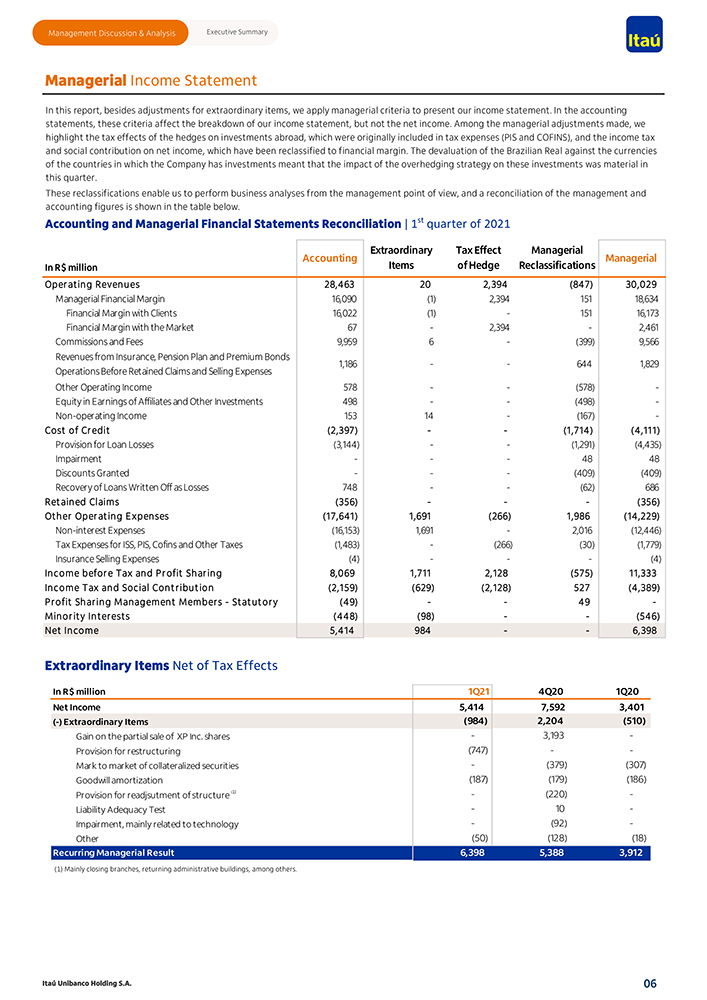

Management Discussion & Analysis Executive Summary Managerial Income Statement In this report, besides adjustments for extraordinary items, we apply managerial criteria to present our income statement. In the accounting statements, these criteria affect the breakdown of our income statement, but not the net income. Among the managerial adjustments made, we highlight the tax effects of the hedges on investments abroad, which were originally included in tax expenses (PIS and COFINS), and the income tax and social contribution on net income, which have been reclassified to financial margin. The devaluation of the Brazilian Real against the currencies of the countries in which the Company has investments meant that the impact of the overhedging strategy on these investments was material in this quarter. These reclassifications enable us to perform business analyses from the management point of view, and a reconciliation of the management and accounting figures is shown in the table below. Accounting and Managerial Financial Statements Reconciliation | 1st quarter of 2021 Extraordinary Tax Effect Managerial Accounting Managerial In R$ million Items of Hedge Reclassifications Oper ating Revenues 28,463 20 2,394 (847) 30,029 Managerial Financial Margin 16,090 (1) 2,394 151 18,634 Financial Margin with Clients 16,022 (1)—151 16,173 Financial Margin with the Market 67—2,394—2,461 Commissions and Fees 9,959 6—(399) 9,566 Revenues from Insurance, Pension Plan and Premium Bonds 1,186 — 644 1,829 Operations Before Retained Claims and Selling Expenses Other Operating Income 578 — (578)—Equity in Earnings of Affiliates and Other Investments 498 — (498)—Non-operating Income 153 14—(167)—Cost of Cr edit (2,397) — (1,714) (4,111) Provision for Loan Losses (3,144) — (1,291) (4,435) Impairment ——48 48 Discounts Granted ——(409) (409) Recovery of Loans Written Off as Losses 748 — (62) 686 Retained Claims (356) ——(356) Other Oper ating Expenses (17,641) 1,691 (266) 1,986 (14,229) Non-interest Expenses (16,153) 1,691—2,016 (12,446) Tax Expenses for ISS, PIS, Cofins and Other Taxes (1,483)—(266) (30) (1,779) Insurance Selling Expenses (4) ——(4) Income befor e Tax and Pr ofit Shar ing 8,069 1,711 2,128 (575) 11,333 Income Tax and Social Contr ibution (2,159) (629) (2,128) 527 (4,389) Pr ofit Shar ing Management Member s—Statutor y (49) — 49—Minor ity Inter ests (448) (98) — (546) Net Income 5,414 984 — 6,398 Extraordinary Items Net of Tax Effects In R$ million 1Q21 4Q20 1Q20 Net Income 5,414 7,592 3,401 (-) Extraordinary Items (984) 2,204 (510) Gain on the partial sale of XP Inc. shares—3,193—Provision for restructuring (747) — Mark to market of collateralized securities—(379) (307) Goodwill amortization (187) (179) (186) Provision for readjsutment of structure (1)—(220)—Liability Adequacy Test—10—Impairment, mainly related to technology—(92)—Other (50) (128) (18) Recurring Managerial Result 6,398 5,388 3,912 (1) Mainly closing branches, returning administrative buildings, among others. Itaú Unibanco Holding S.A. 06

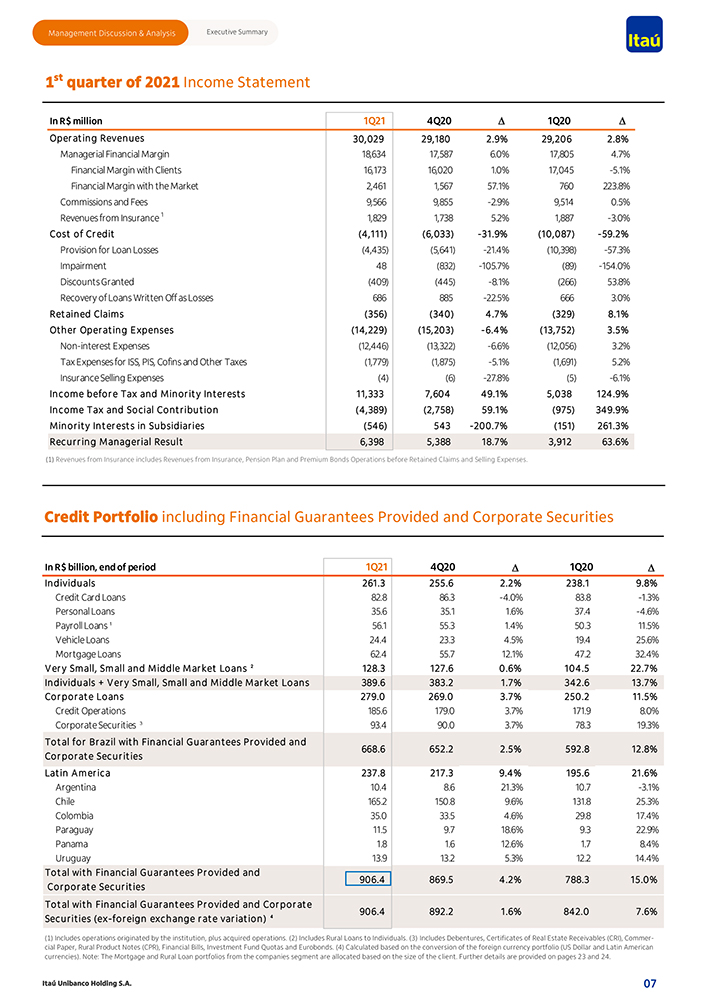

Management Discussion & Analysis Executive Summary 1st quarter of 2021 Income Statement In R$ million 1Q21 4Q20 D’ 1Q20 D’ Oper ating Revenues 30,029 29,180 2. 9% 29,206 2. 8% Managerial Financial Margin 18,634 17,587 6.0% 17,805 4.7% Financial Margin with Clients 16,173 16,020 1.0% 17,045 -5.1% Financial Margin with the Market 2,461 1,567 57.1% 760 223.8% Commissions and Fees 9,566 9,855 -2.9% 9,514 0.5% Revenues from Insurance 1 1,829 1,738 5.2% 1,887 -3.0% Cost of Cr edit (4,111) (6,033)—31 . 9% (10,087)—59. 2% Provision for Loan Losses (4,435) (5,641) -21.4% (10,398) -57.3% Impairment 48 (832) -105.7% (89) -154.0% Discounts Granted (409) (445) -8.1% (266) 53.8% Recovery of Loans Written Off as Losses 686 885 -22.5% 666 3.0% Retained Claims (356) (340) 4 . 7% (329) 8. 1% Other Oper ating Expenses (14,229) (15,203)—6. 4% (13,752) 3 . 5% Non-interest Expenses (12,446) (13,322) -6.6% (12,056) 3.2% Tax Expenses for ISS, PIS, Cofins and Other Taxes (1,779) (1,875) -5.1% (1,691) 5.2% Insurance Selling Expenses (4) (6) -27.8% (5) -6.1% Income befor e Tax and Minor ity Inter ests 11,333 7,604 49. 1% 5,038 124 . 9% Income Tax and Social Contr ibution (4,389) (2,758) 59. 1% (975) 349. 9% Minor ity Inter ests in Subsidiar ies (546) 543—200 . 7% (151) 261 . 3% Recur r ing Manager ial Result 6,398 5,388 18. 7% 3,912 63 . 6% (1) Revenues from Insurance includes Revenues from Insurance, Pension Plan and Premium Bonds Operations before Retained Claims and Selling Expenses. Credit Portfolio including Financial Guarantees Provided and Corporate Securities In R$ billion, end of period 1Q21 4Q20 D’ 1Q20 D’ Individuals 261 . 3 255. 6 2. 2% 238. 1 9. 8% Credit Card Loans 82.8 86.3 -4.0% 83.8 -1.3% Personal Loans 35.6 35.1 1.6% 37.4 -4.6% Payroll Loans 1 56.1 55.3 1.4% 50.3 11.5% Vehicle Loans 24.4 23.3 4.5% 19.4 25.6% Mortgage Loans 62.4 55.7 12.1% 47.2 32.4% V er y Small, Small and Middle Mar ket Loans 2 128. 3 127 . 6 0 . 6% 104 . 5 22. 7% Individuals + V er y Small, Small and Middle Mar ket Loans 389. 6 383 . 2 1 . 7% 342. 6 13 . 7% Cor por ate Loans 279. 0 269. 0 3 . 7% 250 . 2 11 . 5% Credit Operations 185.6 179.0 3.7% 171.9 8.0% Corporate Securities 3 93.4 90.0 3.7% 78.3 19.3% Total for Br azil with Financial Guar antees Pr ovided and 668. 6 652. 2 2. 5% 592. 8 12. 8% Cor por ate Secur ities Latin Amer ica 237 . 8 217 . 3 9. 4% 195. 6 21 . 6% Argentina 10.4 8.6 21.3% 10.7 -3.1% Chile 165.2 150.8 9.6% 131.8 25.3% Colombia 35.0 33.5 4.6% 29.8 17.4% Paraguay 11.5 9.7 18.6% 9.3 22.9% Panama 1.8 1.6 12.6% 1.7 8.4% Uruguay 13.9 13.2 5.3% 12.2 14.4% Total with Financial Guar antees Pr ovided and 906. 4 869. 5 4 . 2% 788. 3 15. 0% Cor por ate Secur ities Total with Financial Guar antees Pr ovided and Cor por ate 906. 4 892. 2 1 . 6% 842. 0 7 . 6% Secur ities (ex—for eign exchange r ate var iation) 4 (1) Includes operations originated by the institution, plus acquired operations. (2) Includes Rural Loans to Individuals. (3) Includes Debentures, Certificates of Real Estate Receivables (CRI), Commercial Paper, Rural Product Notes (CPR), Financial Bills, Investment Fund Quotas and Eurobonds. (4) Calculated based on the conversion of the foreign currency portfolio (US Dollar and Latin American currencies). Note: The Mortgage and Rural Loan portfolios from the companies segment are allocated based on the size of the client. Further details are provided on pages 23 and 24. Itaú Unibanco Holding S.A. 07

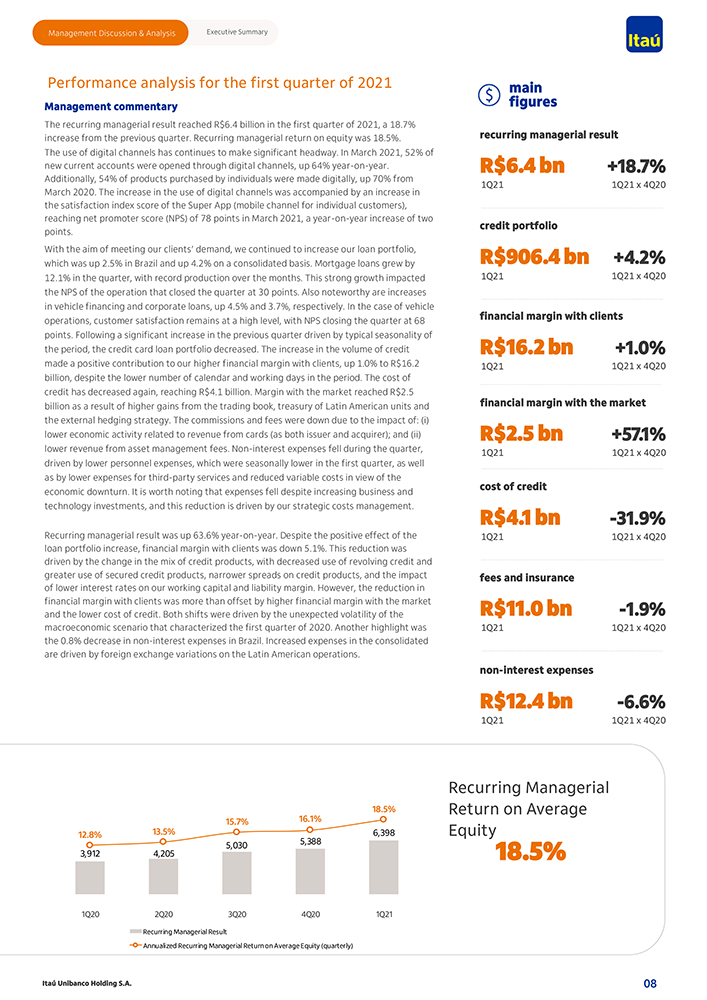

Management Discussion & Analysis Executive Summary Performance analysis for the first quarter of 2021 Management commentary The recurring managerial result reached R$6.4 billion in the first quarter of 2021, a 18.7% increase from the previous quarter. Recurring managerial return on equity was 18.5% . The use of digital channels has continues to make significant headway. In March 2021, 52% of new current accounts were opened through digital channels, up 64% year-on-year. Additionally, 54% of products purchased by individuals were made digitally, up 70% from March 2020. The increase in the use of digital channels was accompanied by an increase in the satisfaction index score of the Super App (mobile channel for individual customers), reaching net promoter score (NPS) of 78 points in March 2021, a year-on-year increase of two points. With the aim of meeting our clients’ demand, we continued to increase our loan portfolio, which was up 2.5% in Brazil and up 4.2% on a consolidated basis. Mortgage loans grew by 12.1% in the quarter, with record production over the months. This strong growth impacted the NPS of the operation that closed the quarter at 30 points. Also noteworthy are increases in vehicle financing and corporate loans, up 4.5% and 3.7%, respectively. In the case of vehicle operations, customer satisfaction remains at a high level, with NPS closing the quarter at 68 points. Following a significant increase in the previous quarter driven by typical seasonality of the period, the credit card loan portfolio decreased. The increase in the volume of credit made a positive contribution to our higher financial margin with clients, up 1.0% to R$16.2 billion, despite the lower number of calendar and working days in the period. The cost of credit has decreased again, reaching R$4.1 billion. Margin with the market reached R$2.5 billion as a result of higher gains from the trading book, treasury of Latin American units and the external hedging strategy. The commissions and fees were down due to the impact of: (i) lower economic activity related to revenue from cards (as both issuer and acquirer); and (ii) lower revenue from asset management fees. Non-interest expenses fell during the quarter, driven by lower personnel expenses, which were seasonally lower in the first quarter, as well as by lower expenses for third-party services and reduced variable costs in view of the economic downturn. It is worth noting that expenses fell despite increasing business and technology investments, and this reduction is driven by our strategic costs management. Recurring managerial result was up 63.6% year-on-year. Despite the positive effect of the loan portfolio increase, financial margin with clients was down 5.1% . This reduction was driven by the change in the mix of credit products, with decreased use of revolving credit and greater use of secured credit products, narrower spreads on credit products, and the impact of lower interest rates on our working capital and liability margin. However, the reduction in financial margin with clients was more than offset by higher financial margin with the market and the lower cost of credit. Both shifts were driven by the unexpected volatility of the macroeconomic scenario that characterized the first quarter of 2020. Another highlight was the 0.8% decrease in non-interest expenses in Brazil. Increased expenses in the consolidated are driven by foreign exchange variations on the Latin American operations. 16.1% 18.5% 13.5% 15.7% 12.8% 6,398 5,030 5,388 3,912 4,205 1Q20 2Q20 3Q20 4Q20 1Q21 Recurring Managerial Result Annualized Recurring Managerial Return on Average Equity (quarterly) Itaú Unibanco Holding S.A. main figures recurring managerial result R$6.4 bn +18.7% 1Q21 1Q21 x 4Q20 credit portfolio R$906.4 bn +4.2% 1Q21 1Q21 x 4Q20 financial margin with clients R$16.2 bn +1.0% 1Q21 1Q21 x 4Q20 financial margin with the market R$2.5 bn +57.1% 1Q21 1Q21 x 4Q20 cost of credit R$4.1 bn -31.9% 1Q21 1Q21 x 4Q20 fees and insurance R$11.0 bn -1.9% 1Q21 1Q21 x 4Q20 non-interest expenses R$12.4 bn -6.6% 1Q21 1Q21 x 4Q20 Recurring Managerial Return on Average Equity 18.5% 08

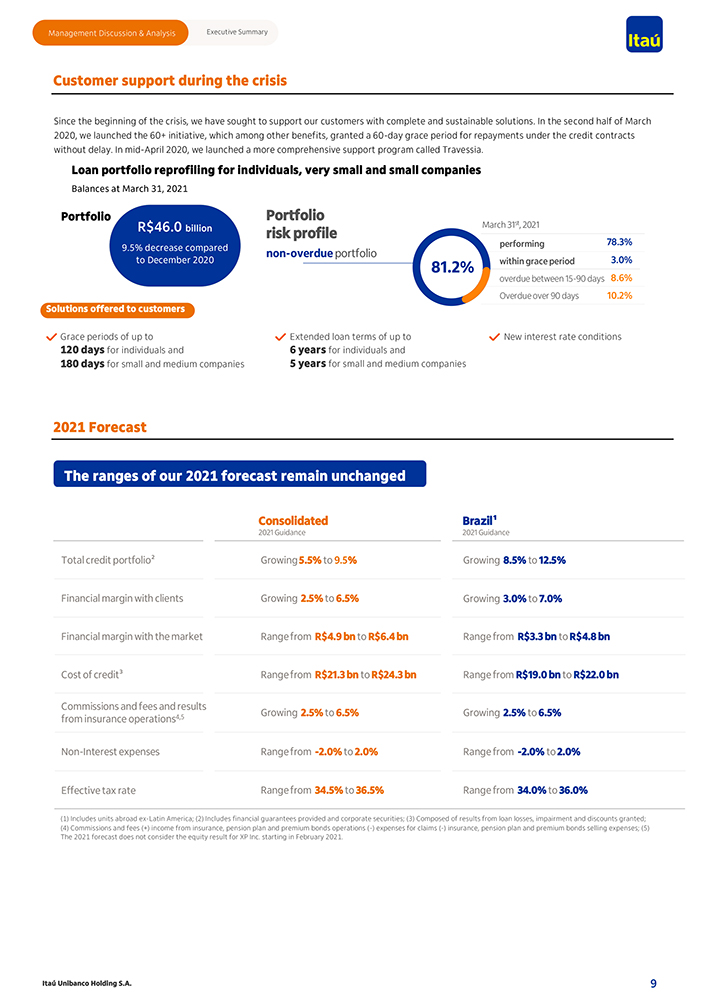

Management Discussion & Analysis Executive Summary Customer support during the crisis Since the beginning of the crisis, we have sought to support our customers with complete and sustainable solutions. In the second half of March 2020, we launched the 60+ initiative, which among other benefits, granted a 60-day grace period for repayments under the credit contracts without delay. In mid-April 2020, we launched a more comprehensive support program called Travessia. Loan portfolio reprofiling for individuals, very small and small companies Balances at March 31, 2021 Portfolio Portfolio R$46.0 billion riskprofile March31st, 2021 performing 78.3% 9.5% decrease compared non-overdue portfolio to December 2020 81.2% withingraceperiod 3.0% overduebetween15-90 days 8.6% Overdueover 90 days 10.2% Solutions offered to customers Grace periods of up to Extended loan terms of up to New interest rate conditions 120 days for individuals and 6 years for individuals and 180 days for small and medium companies 5 years for small and medium companies 2021 Forecast The ranges of our 2021 forecast remain unchanged Consolidated Brazil¹ 2021 Guidance 2021 Guidance Total credit portfolio² Growing 5.5% to 9.5% Growing 8.5% to 12.5% Financial margin with clients Growing 2.5% to 6.5% Growing 3.0% to 7.0% Financial margin with the market Range from R$4.9 bn to R$6.4 bn Range from R$3.3 bn to R$4.8 bn Cost of credit³ Range from R$21.3 bn to R$24.3 bn Range from R$19.0 bn to R$22.0 bn Commissions and fees and results from insurance operations4,5 Growing 2.5% to 6.5% Growing 2.5% to 6.5% Non-Interest expenses Range from -2.0% to 2.0% Range from -2.0% to 2.0% Effective tax rate Range from 34.5% to 36.5% Range from 34.0% to 36.0% (1) Includes units abroad ex-Latin America; (2) Includes financial guarantees provided and corporate securities; (3) Composed of results from loan losses, impairment and discounts granted; (4) Commissions and fees (+) income from insurance, pension plan and premium bonds operations (-) expenses for claims (-) insurance, pension plan and premium bonds selling expenses; (5) The 2021 forecast does not consider the equity result for XP Inc. starting in February 2021. Itaú Unibanco Holding S.A. 9

Management Discussion & Analysis Executive Summary Itaú Unibanco Holding S.A. 10

Income Statement and Balance Sheet Analysis Management Discussion and Analysis and Complete Financial Statements

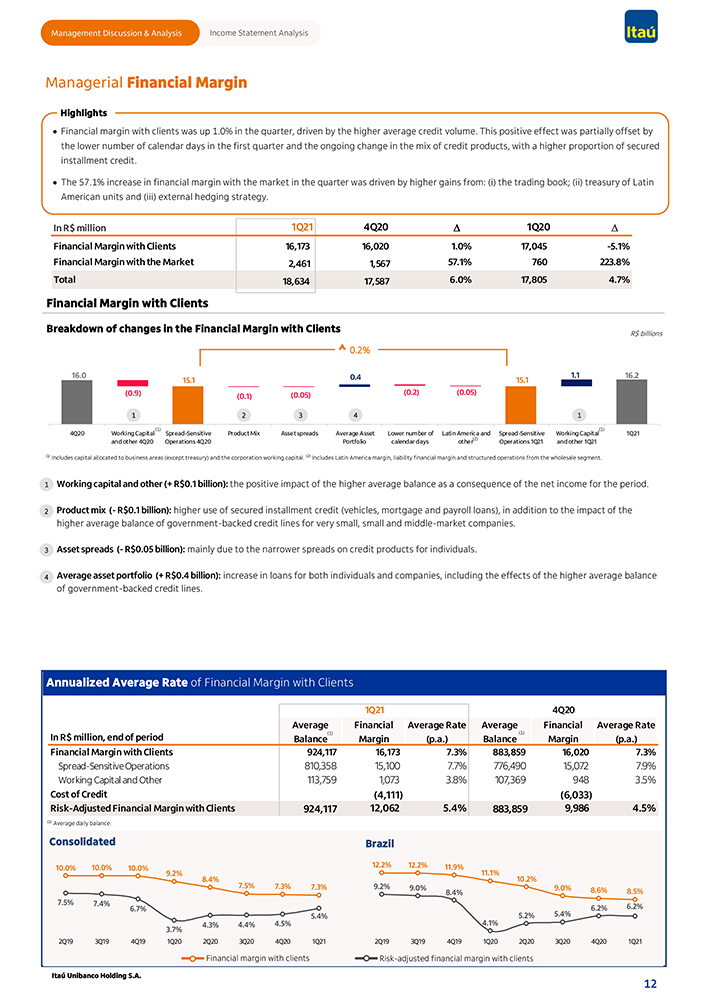

Management Discussion & Analysis Income Statement Analysis Managerial Financial Margin Highlights • Financial margin with clients was up 1.0% in the quarter, driven by the higher average credit volume. This positive effect was partially offset by the lower number of calendar days in the first quarter and the ongoing change in the mix of credit products, with a higher proportion of secured installment credit. • The 57.1% increase in financial margin with the market in the quarter was driven by higher gains from: (i) the trading book; (ii) treasury of Latin American units and (iii) external hedging strategy. In R$ million 1Q21 4Q20ï„ 1Q20ï„ Financial Margin with Clients 16,173 16,020 1.0% 17,045 -5.1% Financial Margin with the Market2,461 1,567 57.1% 760 223.8% Total 18,63417,587 6.0% 17,805 4.7% Financial Margin with Clients Breakdown of changes in the Financial Margin with Clients R$ billions 0.2% 16.0 0.4 1.1 16.2 15.1 15.1 (0.9) (0.1) (0.05) (0.2) (0.05) 1 2 3 4 1 (1) (1) 4Q20 Working Capital Spread-Sensitive Product Mix Asset spreads Average Asset Lower number of Latin America and (2) Spread-Sensitive Working Capital 1Q21 and other 4Q20 Operations 4Q20 Portfolio calendar days other Operations 1Q21 and other 1Q21 1) Includes capital allocated to business areas (except treasury) and the corporation working capital. (2) Includes Latin America margin, liability financial margin and structured operations from the wholesale segment. 1 Working capital and other (+ R$0.1 billion): the positive impact of the higher average balance as a consequence of the net income for the period. 2 Product mix (- R$0.1 billion): higher use of secured installment credit (vehicles, mortgage and payroll loans), in addition to the impact of the higher average balance of government-backed credit lines for very small, small and middle-market companies. 3 Asset spreads (- R$0.05 billion): mainly due to the narrower spreads on credit products for individuals. 4 Average asset portfolio (+ R$0.4 billion): increase in loans for both individuals and companies, including the effects of the higher average balance of government-backed credit lines. Annualized Average Rate of Financial Margin with Clients 1Q21 4Q20 Average Financial Average Rate Average Financial Average Rate In R$ million, end of period (1) (1) Balance Margin (p.a.) Balance Margin (p.a.) Financial Margin with Clients 924,117 16,173 7.3% 883,859 16,020 7.3% Spread-Sensitive Operations 810,358 15,100 7.7% 776,490 15,072 7.9% Working Capital and Other 113,759 1,073 3.8% 107,369 948 3.5% Cost of Credit (4,111) (6,033) Risk-Adjusted Financial Margin with Clients924,117 12,062 5.4% 883,859 9,986 4.5% (1) Average daily balance. Consolidated Brazil 10.0% 10.0% 10.0% 9.2% 12.2% 12.2% 11.9% 11.1% 8.4% 10.2% 7.5% 7.3% 7.3% 9.2% 9.0% 9.0% 8.4% 8.6% 8.5% 7.5% 7.4% 6.2% 6.7% 6.2% 5.4% 5.2% 5.4% 4.3% 4.4% 4.5% 4.1% 3.7% 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 Financial margin with clients Risk-adjusted financial margin with clients Itaú Unibanco Holding S.A. 12

Management Discussion & Analysis Income Statement Analysis Cost of Credit Highlights • The decrease in the cost of credit during the quarter was driven by the lower provision for loan losses in Latin America and in the Retail business segment in Brazil. Additionally, impairment charges on corporate securities in the Wholesale business segment were down during this quarter. • Compared to the first quarter of 2020, the decrease in the cost of credit was due to the requirement to make provision in March 2020, due to changes in the macroeconomic scenario and in the financial prospects of individuals and companies due to the pandemic, as captured by our expected loss provisioning model. In R$ millions 1Q21 4Q20 ï„ 1Q20 ï„ Provision for Loan Losses (4,435) (5,641) -21.4% (10,398) -57.3% Recovery of Loans Written Off as Losses 686 885 -22.5% 666 3.0% Result from Loan Losses (3,750) (4,756) -21.2% (9,732) -61.5% Impairment 48 (832) -105.7% (89) -154.0% Discounts Granted (409) (445) -8.1% (266) 53.8% Cost of Credit (4,111) (6,033) -31.9% (10,087) -59.2% The cost of credit decreased by R$1,922 million compared to the Provision for Loan Losses by Segment previous quarter. This reduction is driven by the lower provision for 6.8 R$ millions loan losses in Latin America and in the Retail business segment in 4.7 3.8 10,398 3.2 2.4 Brazil, due to the lower provisioning requirement for expected losses. 808 In addition, impairment charges on corporate securities decreased by 7,561 6,337 R$880 million due to the reversal of the balance of one client, whose 2,441 795 5,641 1,076 4,435 debt was restructured, and the impairment of another client during 1,845 99 2,335 522 the previous quarter within the Wholesale business in Brazil. 7,149 4,922 5,162 4,645 4,219 The cost of credit decreased by R$5,976 million compared to the first -1,339 -306 quarter of 2020. This variation is driven by the changes in the 1Q20 2Q20 3Q20 4Q20 1Q21 Latin America ex-Brazil macroeconomic scenario and the financial prospects of individuals and Wholesale—Brazil companies occurred in March 2020, captured by our expected loss Retail—Brazil provisioning model, which led to an increase in the provision for loan Provision for Loan Losses / Loan portfolio (*) – Annualized (%) losses during the period. (*) Average loan portfolio balance, considering the last two quarters. Note: Retail business includes loan loss provision expenses in the Corporation segment. In the business segment, Latin America is a part of the Wholesale business. Cost of Credit R$ millions 5.3% 3.9% 3.0% 2.8% 1.9% 10,087 266 7,770 89 750 6,319 6,033 196 617 445 4,111 9,732 346 832 409 ‘ 6,823 ‘ 5,356 4,756 3,750 -48 1Q20 2Q20 3Q20 4Q20 1Q21 Discounts Granted Impairment Result from Loan Losses Cost of Credit Cost of Credit / Total Risk (*) – Annualized (%) (*) The average loan portfolio balance, including financial guarantees provided and corporate securities, for the last two quarters. Itaú Unibanco Holding S.A. Decreases in the provisions for loan losses occurred in Latin America and in the Retail business segment in Brazil, due to the lower requirements for provisions during the quarter. In the Wholesale business segment in Brazil, the reversal during the previous quarter of the provision for a specific client which was subject to impairment during that quarter, led to a lower reversal of provisions during the first quarter of 2021. Also in Wholesale business segment, there were risk rating upgrades for other clients. Recovery of Loans Written off as Losses R$ millions ‘ 981 885 666 738 686 1Q20 2Q20 3Q20 4Q20 1Q21 The reduction compared to the previous quarter was due to the typical seasonality effects during the first quarter. In the same quarter, the sales of portfolios that had already been written off as losses in the amount of R$196 million, generated a positive impact of R$24 million on the recovery of loans written off as losses and of R$13 million in the recurring managerial result. 13

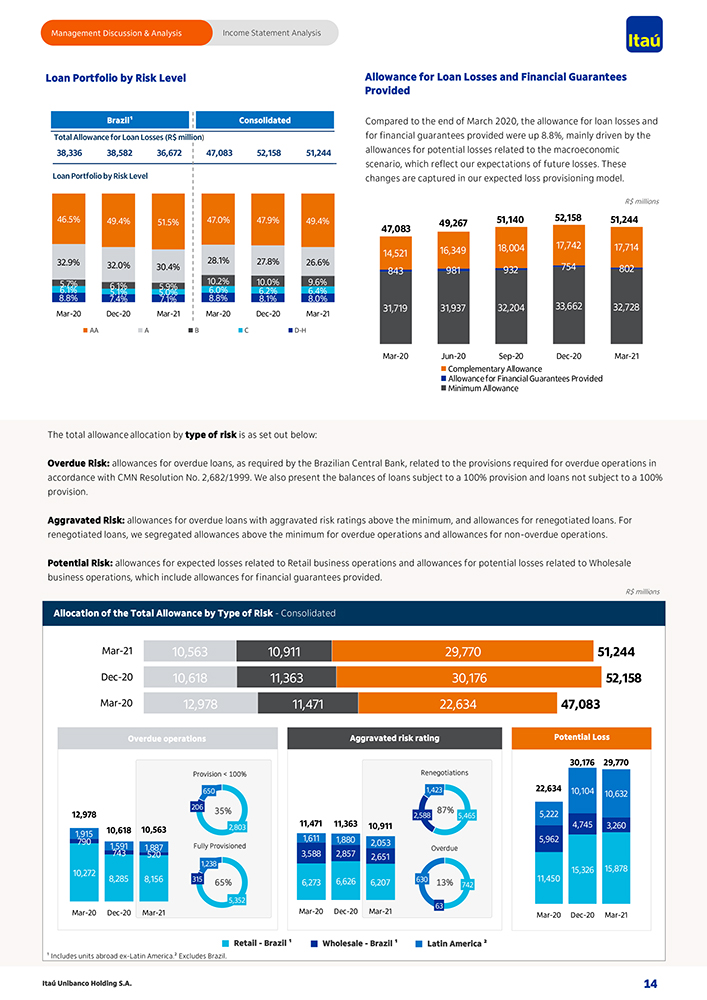

Management Discussion & Analysis Income Statement Analysis Loan Portfolio by Risk Level Allowance for Loan Losses and Financial Guarantees Provided Brazil¹ Consolidated Compared to the end of March 2020, the allowance for loan losses and Total Allowance for Loan Losses (R$ million) for financial guarantees provided were up 8.8%, mainly driven by the 38,336 38,582 36,672 47,083 52,158 51,244 allowances for potential losses related to the macroeconomic scenario, which reflect our expectations of future losses. These Loan Portfolio by Risk Level changes are captured in our expected loss provisioning model. R$ millions 46.5% 49.4% 51.5% 47.0% 47.9% 49.4% 51,140 52,158 51,244 49,267 47,083 16,349 18,004 17,742 17,714 14,521 32.9% 32.0% 28.1% 27.8% 26.6% 30.4% 843 981 932 754 802 5.7% 6.1% 10.2% 10.0% 9.6% 6.1% 5.9% 6.0% 6.2% 6.4% 5.1% 5.0% 8.8% 7.4% 7.1% 8.8% 8.1% 8.0% 31,719 31,937 32,204 33,662 32,728 Mar-20 Dec-20 Mar-21 Mar-20 Dec-20 Mar-21 AA A B C D-H Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Complementary Allowance Allowance for Financial Guarantees Provided Minimum Allowance The total allowance allocation by type of risk is as set out below Overdue Risk: allowances for overdue loans, as required by the Brazilian Central Bank, related to the provisions required for overdue operations in accordance with CMN Resolution No. 2,682/1999. We also present the balances of loans subject to a 100% provision and loans not subject to a 100% provision. Aggravated Risk: allowances for overdue loans with aggravated risk ratings above the minimum, and allowances for renegotiated loans. For renegotiated loans, we segregated allowances above the minimum for overdue operations and allowances for non-overdue operations. Potential Risk: allowances for expected losses related to Retail business operations and allowances for potential losses related to Wholesale business operations, which include allowances for financial guarantees provided. R$ millions Allocation of the Total Allowance by Type of Risk—Consolidated Mar-21 10,563 10,911 29,770 51,244 Dec-20 10,618 11,363 30,176 52,158 Mar-20 12,978 11,471 22,634 47,083 Overdue operations Aggravated risk rating Potential Loss 30,176 29,770 Provision < 100% Renegotiations 650 1,423 22,634 10,104 10,632 206 35% 87% 12,978 11,471 11,363 2,588 5,465 5,222 2,803 10,911 4,745 3,260 1,915 10,618 10,563 790 Fully Provisioned 1,611 1,880 2,053 5,962 1,591 1,887 Overdue 743 520 3,588 2,857 2,651 1,238 15,878 10,272 8,285 11,450 15,326 8,156 315 65% 6,273 6,626 6,207 630 13% 742 5,352 63 Mar-20 Dec-20 Mar-21 Mar-20 Dec-20 Mar-21 Mar-20 Dec-20 Mar-21 Retail—Brazil ¹ Wholesale—Brazil ¹ Latin America ² ¹ Includes units abroad ex-Latin America.² Excludes Brazil. Itaú Unibanco Holding S.A. 14

Management Discussion & Analysis Income Statement Analysis Credit Quality Highlights • The NPL 90 days overdue ratio (NPL 90) remained stable compared the previous quarter. The decline in the individuals segment in Brazil, which reached the lowest level since the merger between Itaú and Unibanco, was offset by increases in Latin America and in the very small, small and middle-market companies segment in Brazil, the latter due to the ends of grace periods of loans reprofiled in previous periods. • The NPL 15 to 90 days overdue ratio (NPL 15-90) increased during the quarter, mainly impacted by the typical seasonality of individuals segment in Brazil during the period. Nonperforming Loans NPL Ratio (%) | 15 to 90 days R$ billions 2.6 19.7 17.5 17.2 2.4 1.7 2.0 1.8 2.0 16.1 14.7 15.1 16.3 1.7 1.9 1.8 2.0 13.7 13.9 12.7 3.5 3.0 2.8 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 3.0 2.4 2.4 Nonperforming Loans over 90 days—Total Nonperforming Loans over 90 days—Brazil¹ 1.9 1.9 1.7 1.9 2.0 1.0 1.1 1.8 1.6 • Nonperforming loans—90 days—Total: the 5.5% increase compared to the previous quarter occurred mainly in Latin America 0.7 0.9 0.7 0.6 0.5 and was driven by a specific client in Chile and by the foreign exchange Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 variations during the period. Total Brazil¹ Latin America² Individuals Very Small, Small and Middle Market Companies Corporate NPL Ratio (%) | over 90 days The total ratio of NPL 15-90 days for both Brazil and Latin America increased compared to the previous quarter. In Brazil, the increase in the ratio for the individuals segment was mainly due to the typical seasonality effects during the first quarter, when family expenses are 5.1 5.0 most concentrated, and due to the effects of the COVID-19 pandemic. This ratio decreased for very small, small and middle-market 4.3 4.2 3.9 companies, driven by the rollover of clients with loans reprofiled in 2.3 2.5 2.0 1.7 previous periods to NPL 90, reflecting the ends of the grace periods on 2.0 1.4 these loans. The ratio for the corporate segment decreased compared 1.1 1.4 1.2 1.3 1.5 to the previous quarter, reaching its lowest level since the fourth 0.7 0.5 0.4 0.4 quarter of 2013. In both segments, the number of new clients with Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 loans overdue between 15 and 90 days was lower than the number Total Brazil¹ Individuals Corporate with loans that migrated to NPL 90-day portfolios. In Latin America, Very Small, Small and Middle Market Companies Latin America² the increase in NPL 15-90 ratio was mainly driven by the individuals segment in Chile and the individuals and companies segments in Colombia. Both the total ratio of NPL 90 days and that for Brazil remained stable compared to the previous quarter. In Brazil, this ratio increased for very small, small and middle-market companies, mainly driven by the ends of the grace periods of loans reprofiled in previous periods. This growth was offset by the reduction in credit card payments overdue in the individuals segment, with the NPL ratio reaching its lowest level since the merger between Itaú and Unibanco. The ratio for the corporate segment remained stable compared to the previous quarter, remaining at its lowest level since 2012. The increase in Latin America was mainly driven by a specific client in Chile. ¹ Includes units abroad ex-Latin America.² Excludes Brazil. Itaú Unibanco Holding S.A. 15

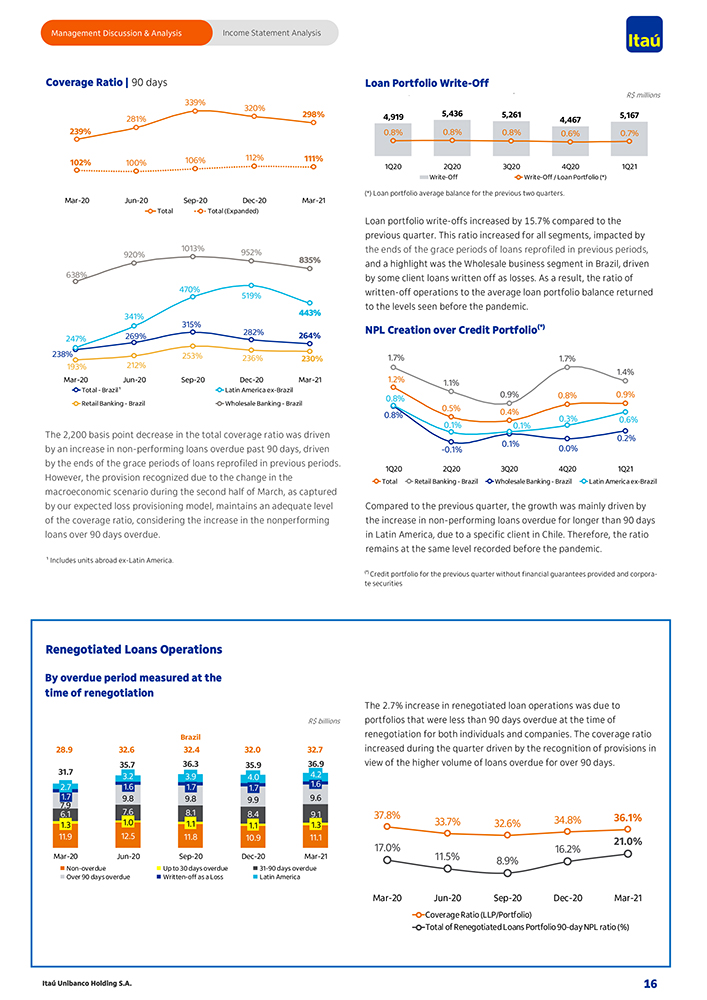

Management Discussion & Analysis Income Statement Analysis Coverage Ratio | 90 days 339% 320% 298% 281% 239% 106% 112% 111% 102% 100% Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Total Total (Expanded) 1013% 952% 920% 835% 638% 470% 519% 341% 443% 315% 269% 282% 264% 247% 238% 253% 236% 230% 193% 212% Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Total—Brazil¹ Latin America ex-Brazil Retail Banking—Brazil Wholesale Banking—Brazil The 2,200 basis point decrease in the total coverage ratio was driven by an increase in non-performing loans overdue past 90 days, driven by the ends of the grace periods of loans reprofiled in previous periods. However, the provision recognized due to the change in the macroeconomic scenario during the second half of March, as captured by our expected loss provisioning model, maintains an adequate level of the coverage ratio, considering the increase in the nonperforming loans over 90 days overdue. ¹ Includes units abroad ex-Latin America. Loan Portfolio Write-Off ‘ ‘ R$ millions 4,919 5,436 5,261 5,167 4,467 0.8% 0.8% 0.8% 0.6% 0.7% 1Q20 2Q20 3Q20 4Q20 1Q21 Write-Off Write-Off / Loan Portfolio (*) (*) Loan portfolio average balance for the previous two quarters. Loan portfolio write-offs increased by 15.7% compared to the previous quarter. This ratio increased for all segments, impacted by the ends of the grace periods of loans reprofiled in previous periods, and a highlight was the Wholesale business segment in Brazil, driven by some client loans written off as losses. As a result, the ratio of written-off operations to the average loan portfolio balance returned to the levels seen before the pandemic. NPL Creation over Credit Portfolio(*) 1.7% 1.7% 1.4% 1.2% 1.1% 0.8% 0.9% 0.8% 0.9% 0.5% 0.4% 0.8% 0.3% 0.6% 0.1% 0.1% 0.2% 0.1% 0.0% -0.1% 1Q20 2Q20 3Q20 4Q20 1Q21 Total Retail Banking—Brazil Wholesale Banking—Brazil Latin America ex-Brazil Compared to the previous quarter, the growth was mainly driven by the increase in non-performing loans overdue for longer than 90 days in Latin America, due to a specific client in Chile. Therefore, the ratio remains at the same level recorded before the pandemic. (*) Credit portfolio for the previous quarter without financial guarantees provided and corporate securities Renegotiated Loans Operations By overdue period measured at the time of renegotiation The 2.7% increase in renegotiated loan operations was due to R$ billions portfolios that were less than 90 days overdue at the time of Brazil renegotiation for both individuals and companies. The coverage ratio 28.9 32.6 32.4 32.0 32.7 increased during the quarter driven by the recognition of provisions in 35.7 36.3 35.9 36.9 view of the higher volume of loans overdue for over 90 days. 31.7 3.2 3.9 4.0 4.2 2.7 1.6 1.7 1.7 1.6 1.7 9.8 9.8 9.9 9.6 7.9 6.1 1.3 7.6 1.0 8.1 1.1 8.4 1.1 9.1 1.3 37.8% 33.7% 32.6% 34.8% 36.1% 11.9 12.5 11.8 10.9 11.1 21.0% 17.0% 16.2% Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 11.5% 8.9% Non-overdue Up to 30 days overdue 31-90 days overdue Over 90 days overdue Written-off as a Loss Latin America Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Coverage Ratio (LLP/Portfolio) Total of Renegotiated Loans Portfolio 90-day NPL ratio (%) Itaú Unibanco Holding S.A. 16

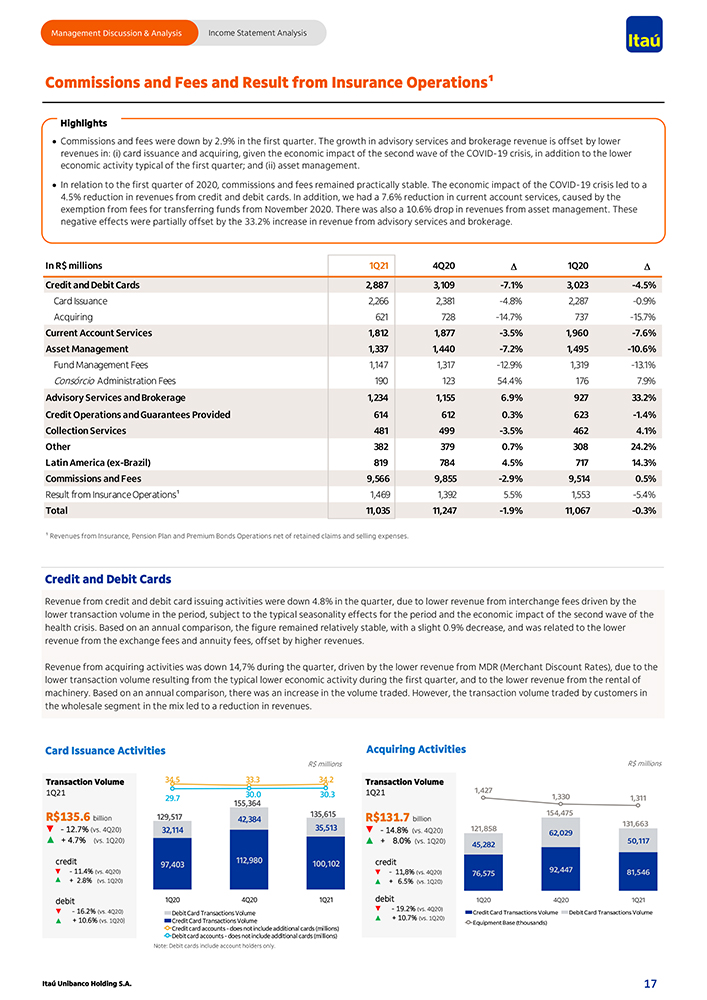

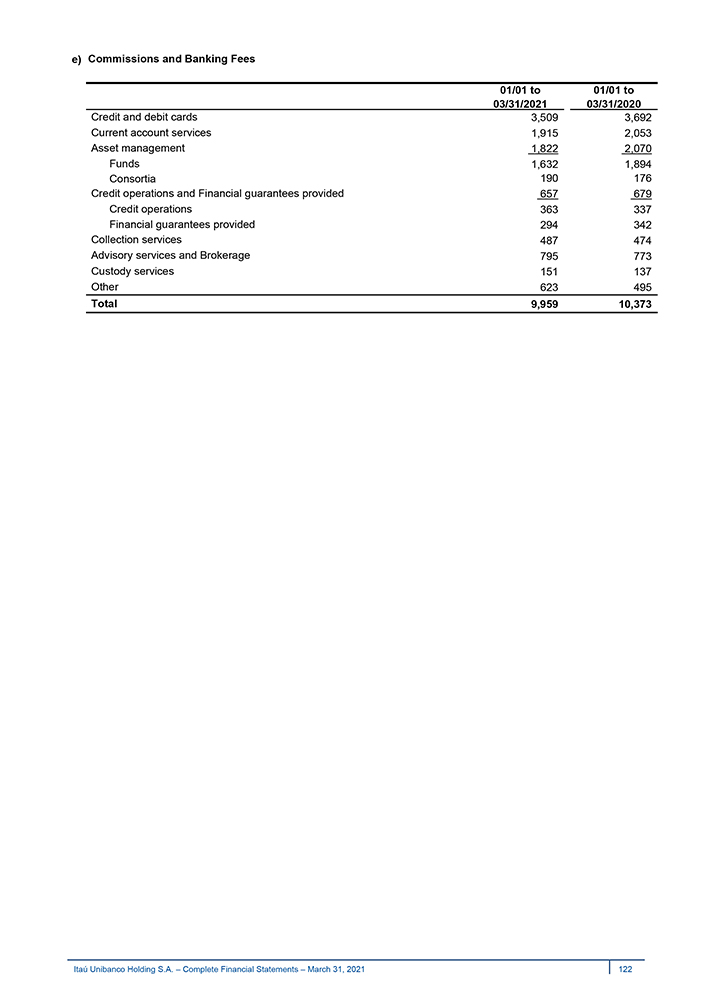

Management Discussion & Analysis Income Statement Analysis Commissions and Fees and Result from Insurance Operations¹ Highlights • Commissions and fees were down by 2.9% in the first quarter. The growth in advisory services and brokerage revenue is offset by lower revenues in: (i) card issuance and acquiring, given the economic impact of the second wave of the COVID-19 crisis, in addition to the lower economic activity typical of the first quarter; and (ii) asset management. • In relation to the first quarter of 2020, commissions and fees remained practically stable. The economic impact of the COVID-19 crisis led to a 4.5% reduction in revenues from credit and debit cards. In addition, we had a 7.6% reduction in current account services, caused by the exemption from fees for transferring funds from November 2020. There was also a 10.6% drop in revenues from asset management. These negative effects were partially offset by the 33.2% increase in revenue from advisory services and brokerage. In R$ millions 1Q21 4Q20 D 1Q20 D Credit and Debit Cards 2,887 3,109 -7.1% 3,023 -4.5% Card Issuance 2,266 2,381 -4.8% 2,287 -0.9% Acquiring 621 728 -14.7% 737 -15.7% Current Account Services 1,812 1,877 -3.5% 1,960 -7.6% Asset Management 1,337 1,440 -7.2% 1,495 -10.6% Fund Management Fees 1,147 1,317 -12.9% 1,319 -13.1% Consórcio Administration Fees 190 123 54.4% 176 7.9% Advisory Services and Brokerage 1,234 1,155 6.9% 927 33.2% Credit Operations and Guarantees Provided 614 612 0.3% 623 -1.4% Collection Services 481 499 -3.5% 462 4.1% Other 382 379 0.7% 308 24.2% Latin America (ex-Brazil) 819 784 4.5% 717 14.3% Commissions and Fees 9,566 9,855 -2.9% 9,514 0.5% Result from Insurance Operations¹ 1,469 1,392 5.5% 1,553 -5.4% Total 11,035 11,247 -1.9% 11,067 -0.3% ¹ Revenues from Insurance, Pension Plan and Premium Bonds Operations net of retained claims and selling expenses. Credit and Debit Cards Revenue from credit and debit card issuing activities were down 4.8% in the quarter, due to lower revenue from interchange fees driven by the lower transaction volume in the period, subject to the typical seasonality effects for the period and the economic impact of the second wave of the health crisis. Based on an annual comparison, the figure remained relatively stable, with a slight 0.9% decrease, and was related to the lower revenue from the exchange fees and annuity fees, offset by higher revenues. Revenue from acquiring activities was down 14,7% during the quarter, driven by the lower revenue from MDR (Merchant Discount Rates), due to the lower transaction volume resulting from the typical lower economic activity during the first quarter, and to the lower revenue from the rental of machinery. Based on an annual comparison, there was an increase in the volume traded. However, the transaction volume traded by customers in the wholesale segment in the mix led to a reduction in revenues. Card Issuance Activities Acquiring Activities R$ millions R$ millions Transaction Volume 34.5 33.3 34.2 Transaction Volume 1Q21 30.0 30.3 1Q21 1,427 29.7 1,330 1,311 155,364 129,517 135,615 154,475 R$135.6 billion 42,384 R$131.7 billion 35,513 131,663—12.7% (vs. 4Q20) 32,114—14.8% (vs. 4Q20) 121,858 62,029 + 4.7% (vs. 1Q20) +8.0% (vs. 1Q20) 50,117 45,282 credit 97,403 112,980 100,102 credit—11.4% (vs. 4Q20)—11,8% (vs. 4Q20) 76,575 92,447 81,546 + 2.8% (vs. 1Q20) + 6.5% (vs. 1Q20) debit 1Q20 4Q20 1Q21 debit 1Q20 4Q20 1Q21—16.2% (vs. 4Q20)—19.2% (vs. 4Q20) Debit Card Transactions Volume 1Q20) Credit Card Transactions Volume Debit Card Transactions Volume + 10.6% (vs. 1Q20 Credit Card Transactions Volume + 10.7% (vs. Equipment Base (thousands) Credit card accounts—does not include additional cards (millions) Debit card accounts—does not include additional cards (millions) Note: Debit cards include account holders only. Itaú Unibanco Holding S.A. 17

Management Discussion & Analysis Income Statement Analysis Current Account Services Revenue from current account services was down 3.5% on the previous quarter driven by lower gains from funds transfers, due to resource transfer fees exemption beginning in November 2020, with the launch of PIX. In the year-to-date, revenues from current account services decreased by 7.6%, driven by lower revenue from the transfer of funds and to the current-account service packages, due to the optimization of the portfolio based on the customers usage profiles. Asset Management • Fund Management Funds management fees were down 12.9% in comparison to the previous quarter and 13,1% lower on a year-on-year basis. In both cases the reduction is due to lower revenue from performance fees. Managed Portfolio and Investment Funds R$ billions +1.4% +10.3% 1,343 1,387 1,407 1,276 1,299 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Note: Does not include Latin America (ex-Brazil). • Consórcio Administration Fees Consórcio management revenue was 54.4% higher during the quarter, due to higher production and the negative effect of changes in provisions on reseller’s commissions occurring in December 2020, which were not repeated in the first quarter; based on an annual comparison, growth is related to higher production. . [Graphic Appears Here] Loan Operations and Financial Guarantees Provided Revenue from loan operations and financial guarantees provided remained broadly stable, with a 0.3% increase on the previous quarter and a 1.4% decrease year-on-year, mainly due to the decrease in the volume of financial guarantees provided. Collection Services Revenue from collection services was down 3.5% from the previous quarter, as a result of the lower transaction volume caused by the economic downturn in the period. Compared to the first quarter of 2020, this revenue was up 4.1% driven by the higher volume. Advisory Services and Brokerage Revenue from advisory and brokerage services increased by R$79 million on the previous quarter. This revenue was up 33.2%, a R$307 million increase on a year-on-year basis, due to the higher levels of capital markets activity. Fixed Income: we took part in local operations involving debentures, promissory notes and securitization, which totaled R$2,313 million in 2021, and were ranked second in the ANBIMA (Brazilian Financial and Capital Markets Association) ranking. Equities: we entered into 17 transactions (including Block Trade) in South America in the first quarter of 2021, which totaled R$6,160 million, and were ranked second in the Dealogic ranking. Mergers and Acquisitions: in 2021, we provided financial advisory services on 9 transactions in Brazil, with a total value of R$130,600 million and we were once again ranked first in the Dealogic ranking. Itaú Unibanco Holding S.A. 18

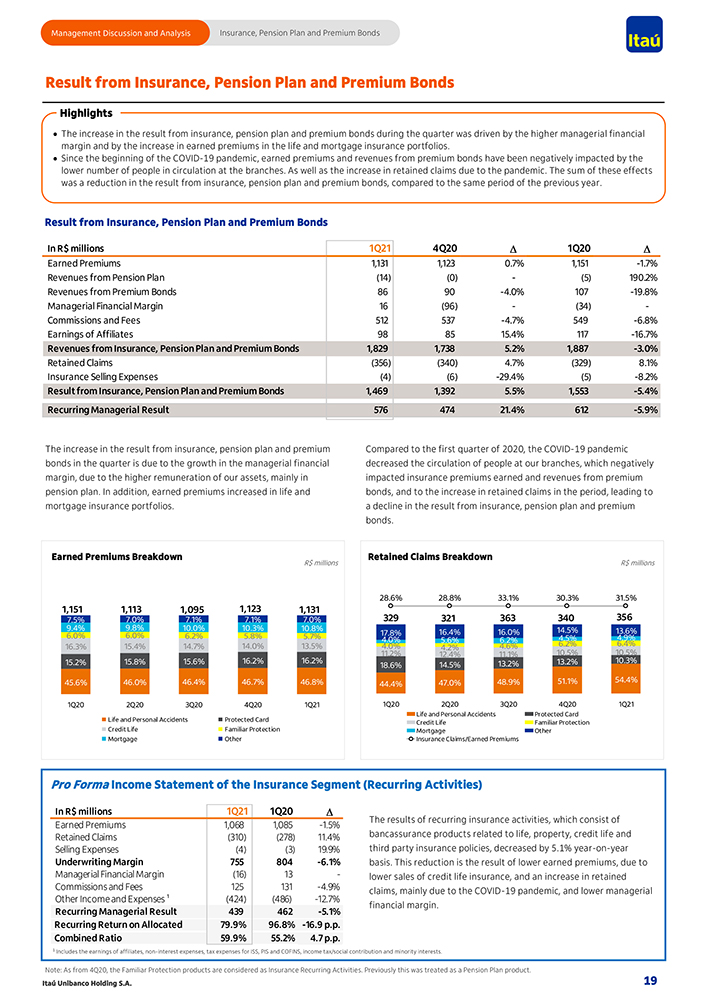

Management Discussion and Analysis Insurance, Pension Plan and Premium Bonds Result from Insurance, Pension Plan and Premium Bonds Highlights • The increase in the result from insurance, pension plan and premium bonds during the quarter was driven by the higher managerial financial margin and by the increase in earned premiums in the life and mortgage insurance portfolios. • Since the beginning of the COVID-19 pandemic, earned premiums and revenues from premium bonds have been negatively impacted by the lower number of people in circulation at the branches. As well as the increase in retained claims due to the pandemic. The sum of these effects was a reduction in the result from insurance, pension plan and premium bonds, compared to the same period of the previous year. Result from Insurance, Pension Plan and Premium Bonds In R$ millions 1Q21 4Q20 D 1Q20 D Earned Premiums 1,131 1,123 0.7% 1,151 -1.7% Revenues from Pension Plan (14) (0)—(5) 190.2% Revenues from Premium Bonds 86 90 -4.0% 107 -19.8% Managerial Financial Margin 16 (96)—(34)—Commissions and Fees 512 537 -4.7% 549 -6.8% Earnings of Affiliates 98 85 15.4% 117 -16.7% Revenues from Insurance, Pension Plan and Premium Bonds 1,829 1,738 5.2% 1,887 -3.0% Retained Claims (356) (340) 4.7% (329) 8.1% Insurance Selling Expenses (4) (6) -29.4% (5) -8.2% Result from Insurance, Pension Plan and Premium Bonds 1,469 1,392 5.5% 1,553 -5.4% Recurring Managerial Result 576 474 21.4% 612 -5.9% The increase in the result from insurance, pension plan and premium bonds in the quarter is due to the growth in the managerial financial margin, due to the higher remuneration of our assets, mainly in pension plan. In addition, earned premiums increased in life and mortgage insurance portfolios. Compared to the first quarter of 2020, the COVID-19 pandemic decreased the circulation of people at our branches, which negatively impacted insurance premiums earned and revenues from premium bonds, and to the increase in retained claims in the period, leading to a decline in the result from insurance, pension plan and premium bonds. Earned Premiums Breakdown Retained Claims Breakdown R$ millions R$ millions 28.6% 28.8% 33.1% 30.3% 31.5% 1,151 1,113 1,095 1,123 1,131 7.5% 7.0% 7.1% 7.1% 7.0% 329 321 363 340 356 9.4% 9.8% 10.0% 10.3% 10.8% 17.8% 16.4% 16.0% 14.5% 13.6% 6.0% 6.0% 6.2% 5.8% 5.7% 4.0% 5.6% 6.2% 4.5% 4.9% 16.3% 15.4% 14.7% 14.0% 13.5% 4.0% 4.2% 4.6% 6.2% 6.4% 11.2% 12.4% 11.1% 10.5% 10.5% 15.2% 15.8% 15.6% 16.2% 16.2% 18.6% 14.5% 13.2% 13.2% 10.3% 45.6% 46.0% 46.4% 46.7% 46.8% 44.4% 47.0% 48.9% 51.1% 54.4% 1Q20 2Q20 3Q20 4Q20 1Q21 1Q20 2Q20 3Q20 4Q20 1Q21 Life and Personal Accidents Protected Card Life and Personal Accidents Protected Card Credit Life Familiar Protection Credit Life Familiar Protection Mortgage Other Mortgage Other Insurance Claims/Earned Premiums Pro Forma Income Statement of the Insurance Segment (Recurring Activities) In R$ millions 1Q21 1Q20 D Earned Premiums 1,068 1,085 -1.5% The results of recurring insurance activities, which consist of Retained Claims (310) (278) 11.4% bancassurance products related to life, property, credit life and Selling Expenses (4) (3) 19.9% third party insurance policies, decreased by 5.1% year-on-year Underwriting Margin 755 804 -6.1% basis. This reduction is the result of lower earned premiums, due to Managerial Financial Margin (16) 13—lower sales of credit life insurance, and an increase in retained Commissions and Fees 125 131 -4.9% claims, mainly due to the COVID-19 pandemic, and lower managerial Other Income and Expenses ¹ (424) (486) -12.7% financial margin. Recurring Managerial Result 439 462 -5.1% Recurring Return on Allocated 79.9% 96.8% -16.9 p.p. Combined Ratio 59.9% 55.2% 4.7 p.p. 1 Includes the earnings of affiliates, non-interest expenses, tax expenses for ISS, PIS and COFINS, income tax/social contribution and minority interests. Note: As from 4Q20, the Familiar Protection products are considered as Insurance Recurring Activities. Previously this was treated as a Pension Plan product. Itaú Unibanco Holding S.A. 19

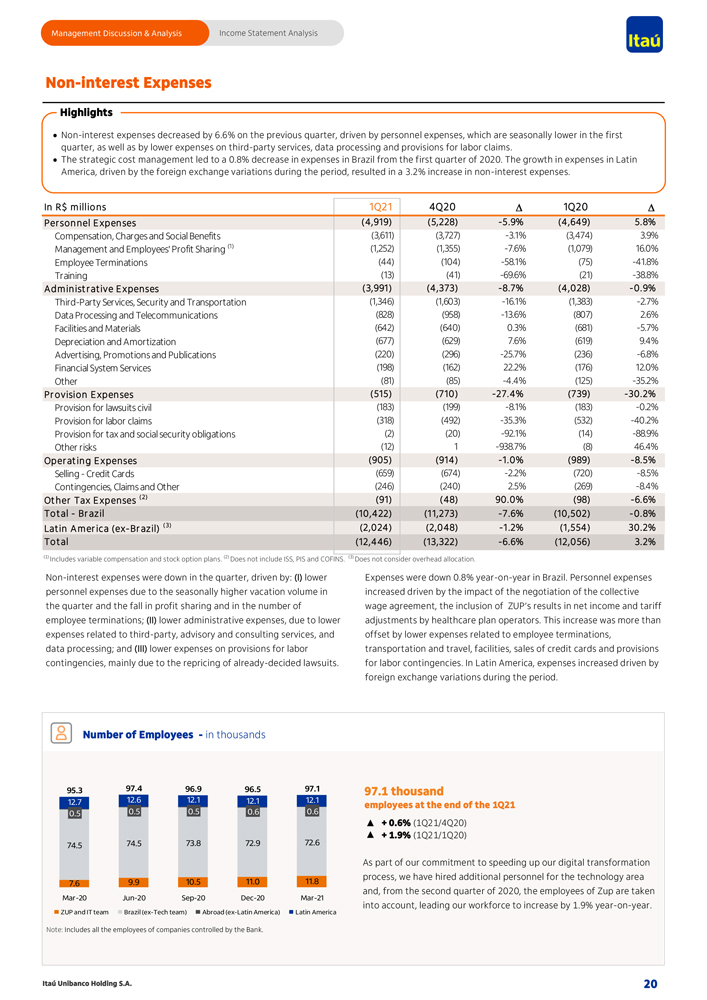

Management Discussion & Analysis Income Statement Analysis Non-interest Expenses Highlights • Non-interest expenses decreased by 6.6% on the previous quarter, driven by personnel expenses, which are seasonally lower in the first quarter, as well as by lower expenses on third-party services, data processing and provisions for labor claims. • The strategic cost management led to a 0.8% decrease in expenses in Brazil from the first quarter of 2020. The growth in expenses in Latin America, driven by the foreign exchange variations during the period, resulted in a 3.2% increase in non-interest expenses. In R$ millions Per sonnel Expenses Compensation, Charges and Social Benefits Management and Employees’ Profit Sharing (1) Employee Terminations Training Administrative Expenses Third-Party Services, Security and Transportation Data Processing and Telecommunications Facilities and Materials Depreciation and Amortization Advertising, Promotions and Publications Financial System Services Other Provision Expenses Provision for lawsuits civil Provision for labor claims Provision for tax and social security obligations Other risks Operating Expenses Selling—Credit Cards Contingencies, Claims and Other Other Tax Expenses ( 2) Total—Brazil Latin America (ex-Brazil) ( 3) Total 1Q21 (4,919) (3,611) (1,252) (44) (13) (3,991) (1,346) (828) (642) (677) (220) (198) (81) (515) (183) (318) (2) (12) (905) (659) (246) (91) (10,422) (2,024) (12,446) 4Q20 (5,228) (3,727) (1,355) (104) (41) (4,373) (1,603) (958) (640) (629) (296) (162) (85) (710) (199) (492) (20) 1 (914) (674) (240) (48) (11,273) (2,048) (13,322) D -5.9% -3.1% -7.6% -58.1% -69.6% -8.7% -16.1% -13.6% 0.3% 7.6% -25.7% 22.2% -4.4% -27.4% -8.1% -35.3% -92.1% -938.7% -1.0% -2.2% 2.5% 90.0% -7.6% -1.2% -6.6% 1Q20 (4,649) (3,474) (1,079) (75) (21) (4,028) (1,383) (807) (681) (619) (236) (176) (125) (739) (183) (532) (14) (8) (989) (720) (269) (98) (10,502) (1,554) (12,056) D 5.8% 3.9% 16.0% -41.8% -38.8% -0.9% -2.7% 2.6% -5.7% 9.4% -6.8% 12.0% -35.2% -30.2% -0.2% -40.2% -88.9% 46.4% -8.5% -8.5% -8.4% -6.6% -0.8% 30.2% 3.2% (1) Includes variable compensation and stock option plans. (2) Does not include ISS, PIS and COFINS. (3) Does not consider overhead allocation. Non-interest expenses were down in the quarter, driven by: (I) lower personnel expenses due to the seasonally higher vacation volume in the quarter and the fall in profit sharing and in the number of employee terminations; (II) lower administrative expenses, due to lower expenses related to third-party, advisory and consulting services, and data processing; and (III) lower expenses on provisions for labor contingencies, mainly due to the repricing of already-decided lawsuits. Expenses were down 0.8% year-on-year in Brazil. Personnel expenses increased driven by the impact of the negotiation of the collective wage agreement, the inclusion of ZUP’s results in net income and tariff adjustments by healthcare plan operators. This increase was more than offset by lower expenses related to employee terminations, transportation and travel, facilities, sales of credit cards and provisions for labor contingencies. In Latin America, expenses increased driven by foreign exchange variations during the period. Number of Employees - in thousands 95.3 97.4 96.9 96.5 97.1 12.7 12.6 12.1 12.1 12.1 0.5 0.5 0.5 0.6 0.6 74.5 74.5 73.8 72.9 72.6 7.6 9.9 10.5 11.0 11.8 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 ZUP and IT team Brazil (ex-Tech team) Abroad (ex-Latin America) Latin America Note: Includes all the employees of companies controlled by the Bank. 97.1 thousand employees at the end of the 1Q21 + 0.6% (1Q21/4Q20) + 1.9% (1Q21/1Q20) As part of our commitment to speeding up our digital transformation process, we have hired additional personnel for the technology area and, from the second quarter of 2020, the employees of Zup are taken into account, leading our workforce to increase by 1.9% year-on-year. Itaú Unibanco Holding S.A.

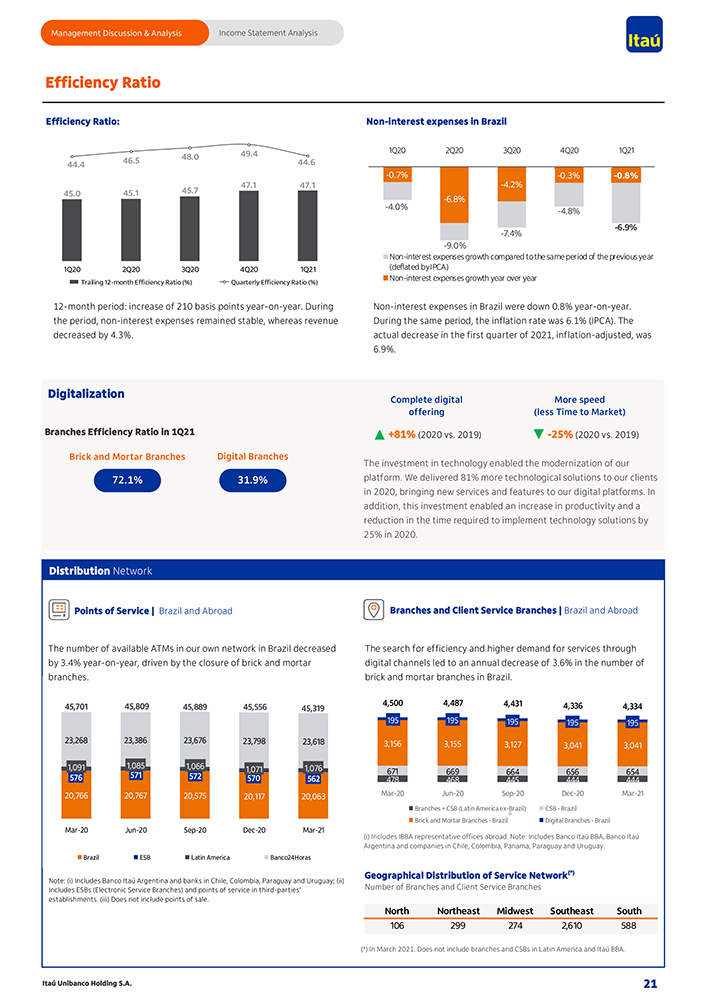

Management Discussion & Analysis Income Statement Analysis Efficiency Ratio Efficiency Ratio: Non-interest expenses in Brazil 1Q20 2Q20 3Q20 4Q20 1Q21 46.5 48.0 49.4 44.4 44.6 -0.7% -0.3% -0.8% 47.1 47.1 -4.2% 45.0 45.1 45.7 -6.8% -4.0% -4.8% -7.4% -6.9% -9.0% Non-interest expenses growth compared to the same period of the previous year 1Q20 2Q20 3Q20 4Q20 1Q21 (deflated byIPCA) Trailing 12-month Efficiency Ratio (%) Quarterly Efficiency Ratio (%) Non-interest expenses growth year over year 12-month period: increase of 210 basis points year-on-year. During the period, non-interest expenses remained stable, whereas revenue decreased by 4.3% . Non-interest expenses in Brazil were down 0.8% year-on-year. During the same period, the inflation rate was 6.1% (IPCA). The actual decrease in the first quarter of 2021, inflation-adjusted, was 6.9% . Digitalization Complete digital More speed offering (less Time to Market) Branches Efficiency Ratio in 1Q21 +81% (2020 vs. 2019) -25% (2020 vs. 2019) Brick and Mortar Branches Digital Branches The investment in technology enabled the modernization of our 72.1% 31.9% platform. We delivered 81% more technological solutions to our clients in 2020, bringing new services and features to our digital platforms. In addition, this investment enabled an increase in productivity and a reduction in the time required to implement technology solutions by 25% in 2020. Distribution Network Points of Service | Brazil and Abroad Branches and Client Service Branches | Brazil and Abroad The number of available ATMs in our own network in Brazil decreased The search for efficiency and higher demand for services through by 3.4% year-on-year, driven by the closure of brick and mortar digital channels led to an annual decrease of 3.6% in the number of branches. brick and mortar branches in Brazil. 45,701 45,809 45,889 45,556 45,319 4,500 4,487 4,431 4,336 4,334 195 195 195 195 195 23,268 23,386 23,676 23,798 23,618 3,156 3,155 3,127 3,041 3,041 1,091 576 1,085 571 1,066 572 1,071 570 1,076 562 478 671 468 669 445 664 444 656 444 654 20,766 20,767 20,575 20,117 20,063 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Branches + CSB (Latin America ex-Brazil) CSB—Brazil Brick and Mortar Branches—Brazil Digital Branches—Brazil Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 (i) Includes IBBA representative offices abroad. Note: Includes Banco Itaú BBA, Banco Itaú Argentina and companies in Chile, Colombia, Panama, Paraguay and Uruguay. Brazil ESB Latin America Banco24Horas Note: (i) Includes Banco Itaú Argentina and banks in Chile, Colombia, Paraguay and Uruguay; (ii) Geographical Distribution of Service Network(*) Includes ESBs (Electronic Service Branches) and points of service in third-parties’ Number of Branches and Client Service Branches establishments. (iii) Does not include points of sale. North Northeast Midwest Southeast South 106 299 274 2,610 588 (*) In March 2021. Does not include branches and CSBs in Latin America and Itaú BBA. Itaú Unibanco Holding S.A. 21

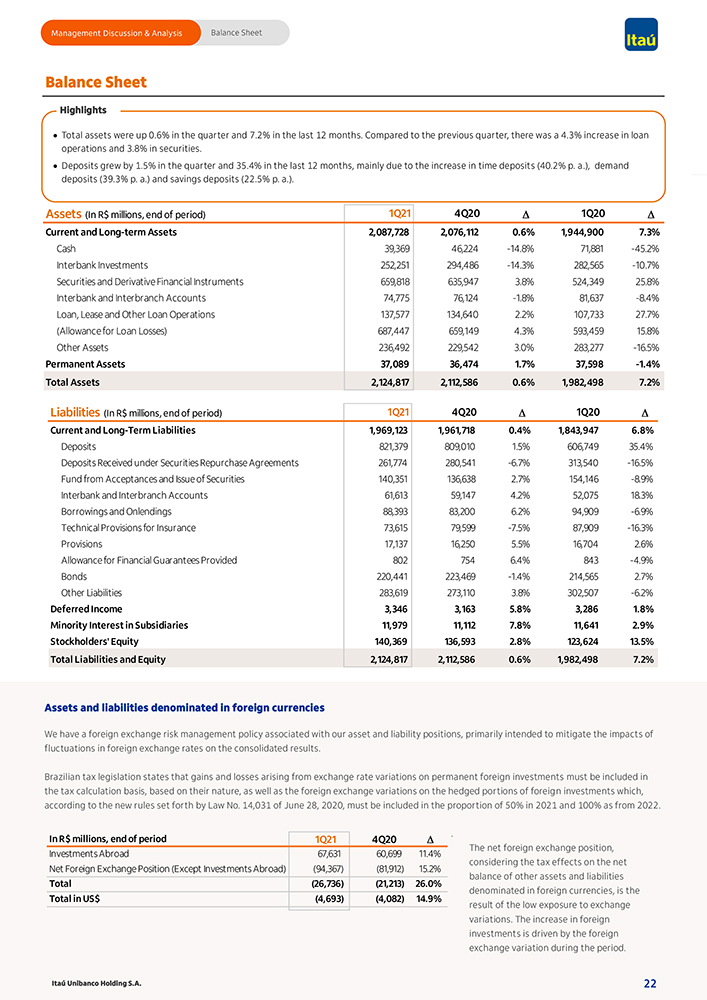

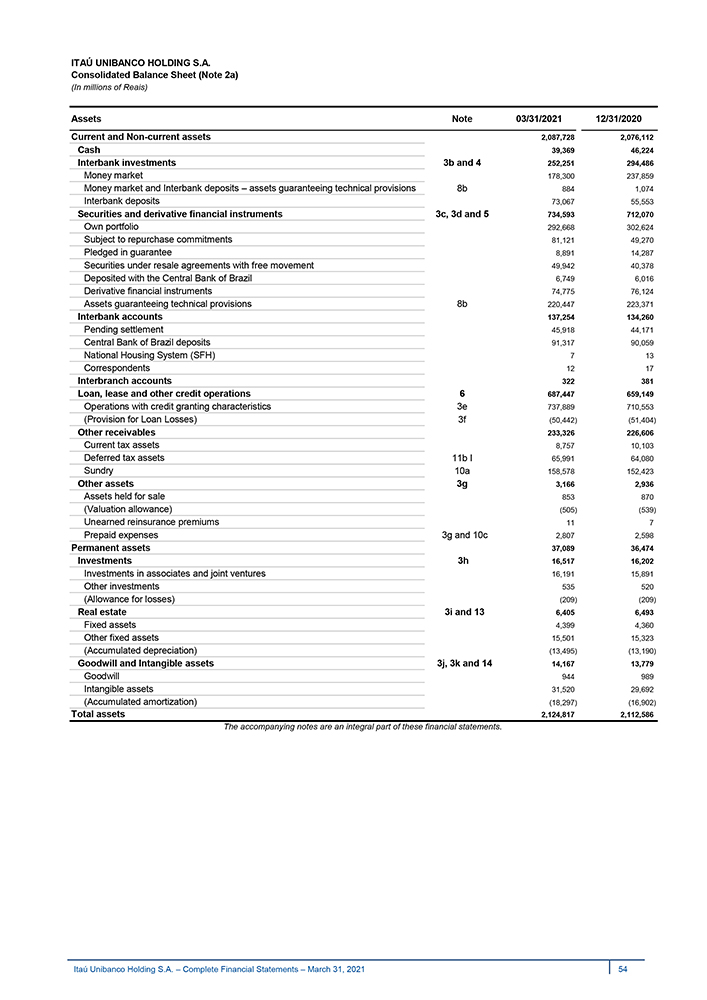

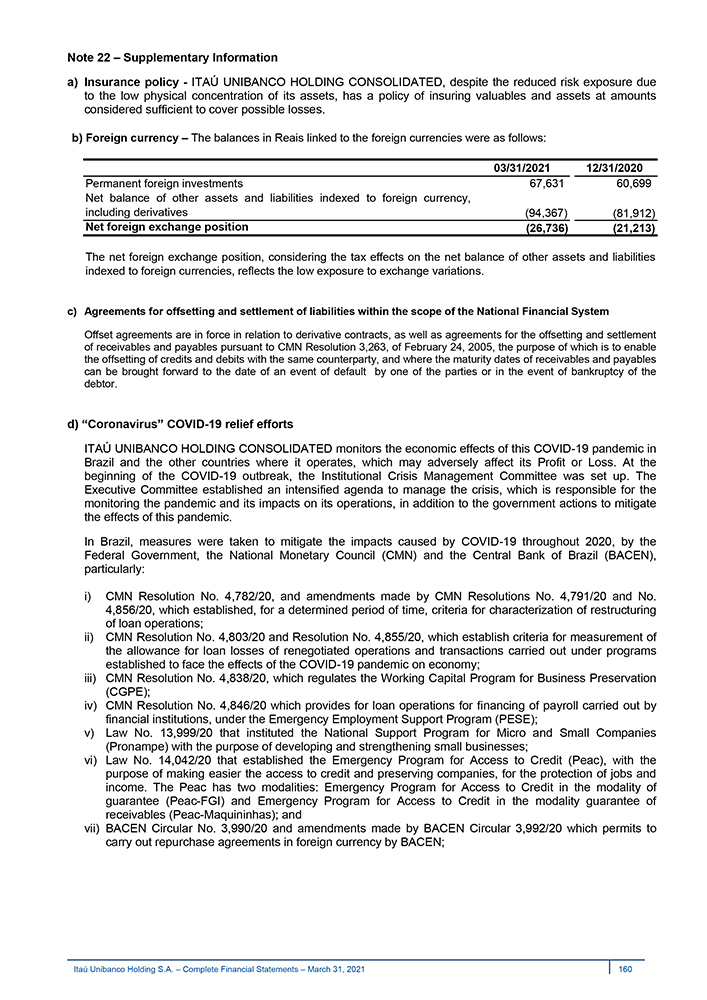

Management Discussion & Analysis Balance Sheet Balance Sheet Highlights • Deposits grew by 1.5% in the quarter and 35.4% in the last 12 months, mainly due to the increase in time deposits (40.2% p. a.), demand deposits (39.3% p. a.) and savings deposits (22.5% p. a.). Assets (In R$ millions, end of period) 1Q21 4Q20 D’ 1Q20 D’ Current and Long-term Assets 2,087,728 2,076,112 0.6% 1,944,900 7.3% Cash 39,369 46,224 -14.8% 71,881 -45.2% Interbank Investments 252,251 294,486 -14.3% 282,565 -10.7% Securities and Derivative Financial Instruments 659,818 635,947 3.8% 524,349 25.8% Interbank and Interbranch Accounts 74,775 76,124 -1.8% 81,637 -8.4% Loan, Lease and Other Loan Operations 137,577 134,640 2.2% 107,733 27.7% (Allowance for Loan Losses) 687,447 659,149 4.3% 593,459 15.8% Other Assets 236,492 229,542 3.0% 283,277 -16.5% Permanent Assets 37,089 36,474 1.7% 37,598 -1.4% Total Assets 2,124,817 2,112,586 0.6% 1,982,498 7.2% Liabilities (In R$ millions, end of period) 1Q21 4Q20 D’ 1Q20 D’ Current and Long-Term Liabilities 1,969,123 1,961,718 0.4% 1,843,947 6.8% Deposits 821,379 809,010 1.5% 606,749 35.4% Deposits Received under Securities Repurchase Agreements 261,774 280,541 -6.7% 313,540 -16.5% Fund from Acceptances and Issue of Securities 140,351 136,638 2.7% 154,146 -8.9% Interbank and Interbranch Accounts 61,613 59,147 4.2% 52,075 18.3% Borrowings and Onlendings 88,393 83,200 6.2% 94,909 -6.9% Technical Provisions for Insurance 73,615 79,599 -7.5% 87,909 -16.3% Provisions 17,137 16,250 5.5% 16,704 2.6% Allowance for Financial Guarantees Provided 802 754 6.4% 843 -4.9% Bonds 220,441 223,469 -1.4% 214,565 2.7% Other Liabilities 283,619 273,110 3.8% 302,507 -6.2% Deferred Income 3,346 3,163 5.8% 3,286 1.8% Minority Interest in Subsidiaries 11,979 11,112 7.8% 11,641 2.9% Stockholders’ Equity 140,369 136,593 2.8% 123,624 13.5% Total Liabilities and Equity 2,124,817 2,112,586 0.6% 1,982,498 7.2% Assets and liabilities denominated in foreign currencies We have a foreign exchange risk management policy associated with our asset and liability positions, primarily intended to mitigate the impacts of fluctuations in foreign exchange rates on the consolidated results. Brazilian tax legislation states that gains and losses arising from exchange rate variations on permanent foreign investments must be included in the tax calculation basis, based on their nature, as well as the foreign exchange variations on the hedged portions of foreign investments which, according to the new rules set forth by Law No. 14,031 of June 28, 2020, must be included in the proportion of 50% in 2021 and 100% as from 2022. In R$ millions, end of period 1Q21 4Q20 D . Investments Abroad 67,631 60,699 11.4% The net foreign exchange position, Net Foreign Exchange Position (Except Investments Abroad) (94,367) (81,912) 15.2% considering the tax effects on the net balance of other assets and liabilities Total (26,736) (21,213) 26.0% denominated in foreign currencies, is the Total in US$ (4,693) (4,082) 14.9% result of the low exposure to exchange variations. The increase in foreign investments is driven by the foreign exchange variation during the period. Itaú Unibanco Holding S.A. 22

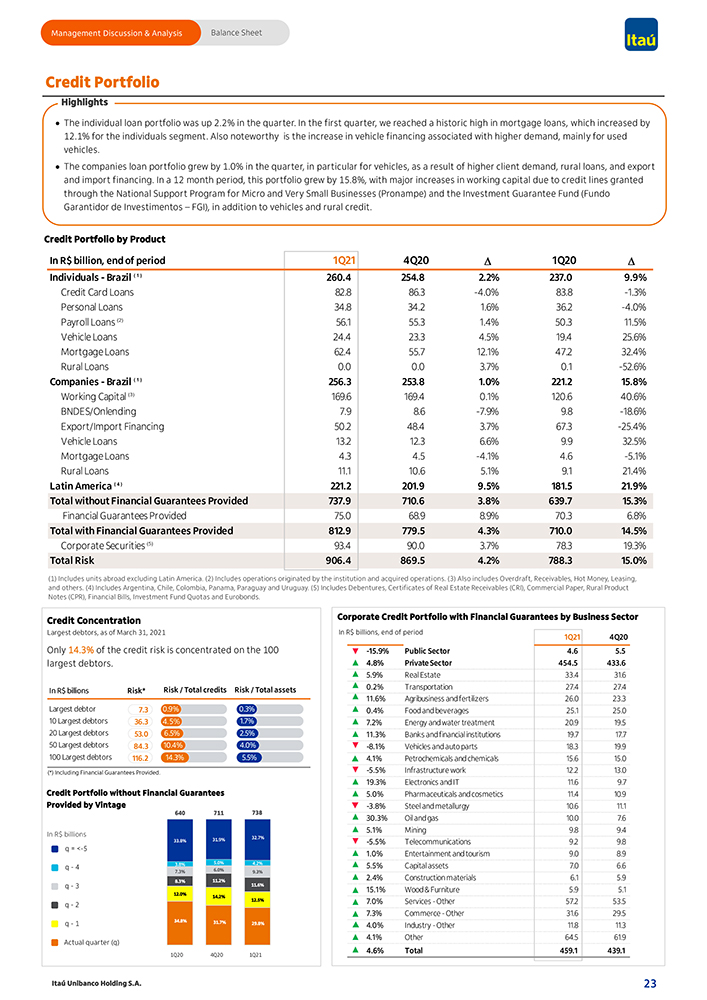

Management Discussion & Analysis Balance Sheet Credit Portfolio Highlights • The individual loan portfolio was up 2.2% in the quarter. In the first quarter, we reached a historic high in mortgage loans, which increased by 12.1% for the individuals segment. Also noteworthy is the increase in vehicle financing associated with higher demand, mainly for used vehicles. • The companies loan portfolio grew by 1.0% in the quarter, in particular for vehicles, as a result of higher client demand, rural loans, and export and import financing. In a 12 month period, this portfolio grew by 15.8%, with major increases in working capital due to credit lines granted through the National Support Program for Micro and Very Small Businesses (Pronampe) and the Investment Guarantee Fund (Fundo Garantidor de Investimentos – FGI), in addition to vehicles and rural credit. Credit Portfolio by Product In R$ billion, end of period 1Q21 4Q20 D 1Q20 D Individuals—Brazil ( 1 ) 260.4 254.8 2.2% 237.0 9.9% Credit Card Loans 82.8 86.3 -4.0% 83.8 -1.3% Personal Loans 34.8 34.2 1.6% 36.2 -4.0% Payroll Loans (2) 56.1 55.3 1.4% 50.3 11.5% Vehicle Loans 24.4 23.3 4.5% 19.4 25.6% Mortgage Loans 62.4 55.7 12.1% 47.2 32.4% Rural Loans 0.0 0.0 3.7% 0.1 -52.6% Companies—Brazil ( 1 ) 256.3 253.8 1.0% 221.2 15.8% Working Capital (3) 169.6 169.4 0.1% 120.6 40.6% BNDES/Onlending 7.9 8.6 -7.9% 9.8 -18.6% Export/Import Financing 50.2 48.4 3.7% 67.3 -25.4% Vehicle Loans 13.2 12.3 6.6% 9.9 32.5% Mortgage Loans 4.3 4.5 -4.1% 4.6 -5.1% Rural Loans 11.1 10.6 5.1% 9.1 21.4% Latin America ( 4 ) 221.2 201.9 9.5% 181.5 21.9% Total without Financial Guarantees Provided 737.9 710.6 3.8% 639.7 15.3% Financial Guarantees Provided 75.0 68.9 8.9% 70.3 6.8% Total with Financial Guarantees Provided 812.9 779.5 4.3% 710.0 14.5% Corporate Securities (5) 93.4 90.0 3.7% 78.3 19.3% Total Risk 906.4 869.5 4.2% 788.3 15.0% (1) Includes units abroad excluding Latin America. (2) Includes operations originated by the institution and acquired operations. (3) Also includes Overdraft, Receivables, Hot Money, Leasing, and others. (4) Includes Argentina, Chile, Colombia, Panama, Paraguay and Uruguay. (5) Includes Debentures, Certificates of Real Estate Receivables (CRI), Commercial Paper, Rural Product Notes (CPR), Financial Bills, Investment Fund Quotas and Eurobonds. Credit Concentration Corporate Credit Portfolio with Financial Guarantees by Business Sector Largest debtors, as of March 31, 2021 In R$ billions, end of period 1Q21 4Q20 Only 14.3% of the credit risk is concentrated on the 100 -15.9% Public Sector 4.6 5.5 largest debtors. 4.8% Private Sector 454.5 433.6 5.9% Real Estate 33.4 31.6 In R$ billions Risk* Risk / Total credits Risk / Total assets 0.2% Transportation 27.4 27.4 11.6% Agribusiness and fertilizers 26.0 23.3 Largest debtor 7.3 0.9% 0.3% 0.4% Food and beverages 25.1 25.0 10 Largest debtors 36.3 4.5% 1.7% 7.2% Energy and water treatment 20.9 19.5 20 Largest debtors 53.0 6.5% 2.5% 11.3% Banks and financial institutions 19.7 17.7 50 Largest debtors 84.3 10.4% 4.0% -8.1% Vehicles and auto parts 18.3 19.9 100 Largest debtors 116.2 14.3% 5.5% 4.1% Petrochemicals and chemicals 15.6 15.0 (*) Including Financial Guarantees Provided. -5.5% Infrastructure work 12.2 13.0 19.3% Electronics and IT 11.6 9.7 Credit Portfolio without Financial Guarantees 5.0% Pharmaceuticals and cosmetics 11.4 10.9 Provided by Vintage -3.8% Steel and metallurgy 10.6 11.1 640 711 738 30.3% Oil and gas 10.0 7.6 In R$ billions 5.1% Mining 9.8 9.4 33.8% 31.9% 32.7% -5.5% Telecommunications 9.2 9.8 q = <-5 1.0% Entertainment and tourism 9.0 8.9 q—4 3.8% 5.0% 4.2% 5.5% Capital assets 7.0 6.6 7.3% 6.0% 9.3% 8.3% 11.2% 2.4% Construction materials 6.1 5.9 q—3 11.6% 15.1% Wood & Furniture 5.9 5.1 12.0% q—2 14.2% 12.5% 7.0% Services—Other 57.2 53.5 7.3% Commerce—Other 31.6 29.5 q—1 34.8% 31.7% 29.8% 4.0% Industry—Other 11.8 11.3 Actual quarter (q) 4.1% Other 64.5 61.9 1T20 4T20 1T21 4.6% Total 459.1 439.1 1Q20 4Q20 1Q21 Itaú Unibanco Holding S.A. 23

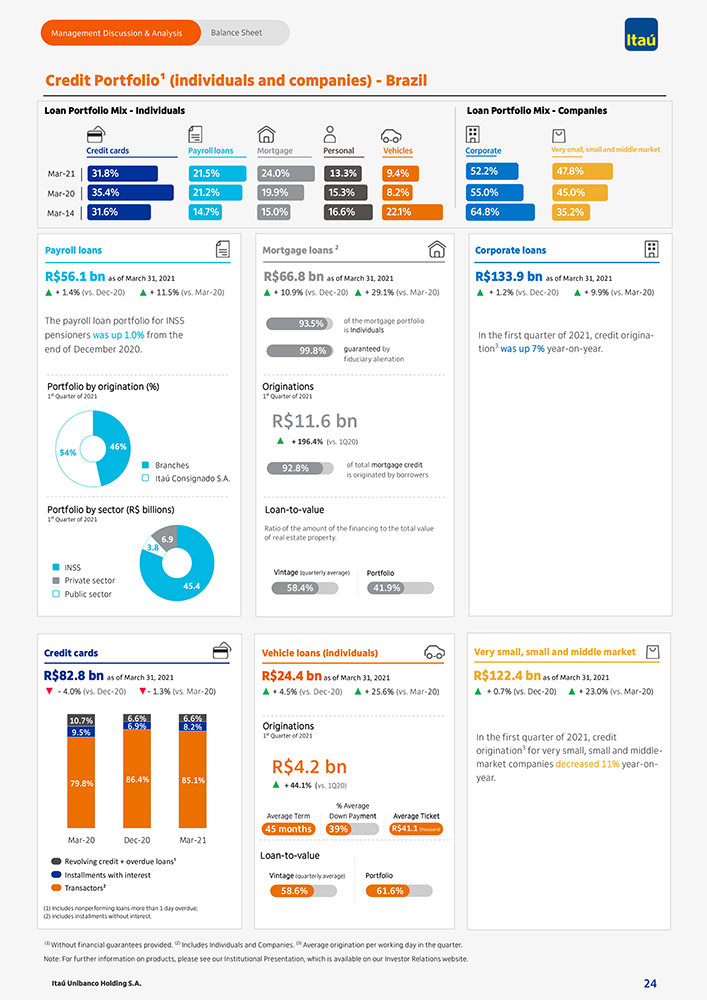

Management Discussion & Analysis Balance Sheet Credit Portfolio¹ (individuals and companies)—Brazil Loan Portfolio Mix—Individuals Loan Portfolio Mix—Companies Credit cards Payroll loans Mortgage Personal Vehicles Corporate Very small, small and middle market Mar-21 31.8% 21.5% 24.0% 13.3% 9.4% 52.2% 47.8% Mar-20 35.4% 21.2% 19.9% 15.3% 8.2% 55.0% 45.0% Mar-14 31.6% 14.7% 15.0% 16.6% 22.1% 64.8% 35.2% Payroll loans Mortgage loans 2 R$56.1 bn as of March 31, 2021 R$66.8 bn as of March 31, 2021 + 1.4% (vs. Dec-20) + 11.5% (vs. Mar-20) + 10.9% (vs. Dec-20) + 29.1% (vs. Mar-20) The payroll loan portfolio for INSS 93.5% of the mortgage portfolio pensioners was up 1.0% from the is Individuals end of December 2020. 99.8% guaranteed by fiduciary alienation Portfolio by origination (%) Originations 1st Quarter of 2021 1st Quarter of 2021 R$11.6 bn 46% + 196.4% (vs. 1Q20) 54% Branches 92.8% of total mortgage credit Itaú Consignado S.A. is originated by borrowers Portfolio by sector (R$ billions) Loan-to-value 1st Quarter of 2021 Ratio of the amount of the financing to the total value 6.9 of real estate property. 3.8 INSS Vintage (quarterly average) Portfolio Private sector 45.4 58.4% 41.9% Public sector Credit cards R$82.8 bn as of March 31, 2021—4.0% (vs. Dec-20)—1.3% (vs. Mar-20) 10.7% 6.6% 6.6% 6.9% 8.2% 9.5% 79.8% 86.4% 85.1% Mar-20 Dec-20 Mar-21 Revolving credit + overdue loans¹ Installments with interest Transactors² (1) Includes nonperforming loans more than 1 day overdue; (2) includes installments without interest. Vehicle loans (individuals) R$24.4 bn as of March 31, 2021 + 4.5% (vs. Dec-20)+ 25.6% (vs. Mar-20) Originations 1st Quarter of 2021 R$4.2 bn + 44.1% (vs. 1Q20) % Average Average Term Down Payment Average Ticket 45 months R$41.1 thousand 39% Loan-to-value Vintage (quarterly average) Portfolio 58.6% 61.6% Corporate loans R$133.9 bn as of March 31, 2021 + 1.2% (vs. Dec-20) + 9.9% (vs. Mar-20) In the first quarter of 2021, credit origination3 was up 7% year-on-year. Very small, small and middle market R$122.4 bn as of March 31, 2021 + 0.7% (vs. Dec-20) + 23.0% (vs. Mar-20) In the first quarter of 2021, credit origination3 for very small, small and middle-market companies decreased 11% year-on-year. (1) Without financial guarantees provided. (2) Includes Individuals and Companies. (3) Average origination per working day in the quarter. Note: For further information on products, please see our Institutional Presentation, which is available on our Investor Relations website. Itaú Unibanco Holding S.A. 24

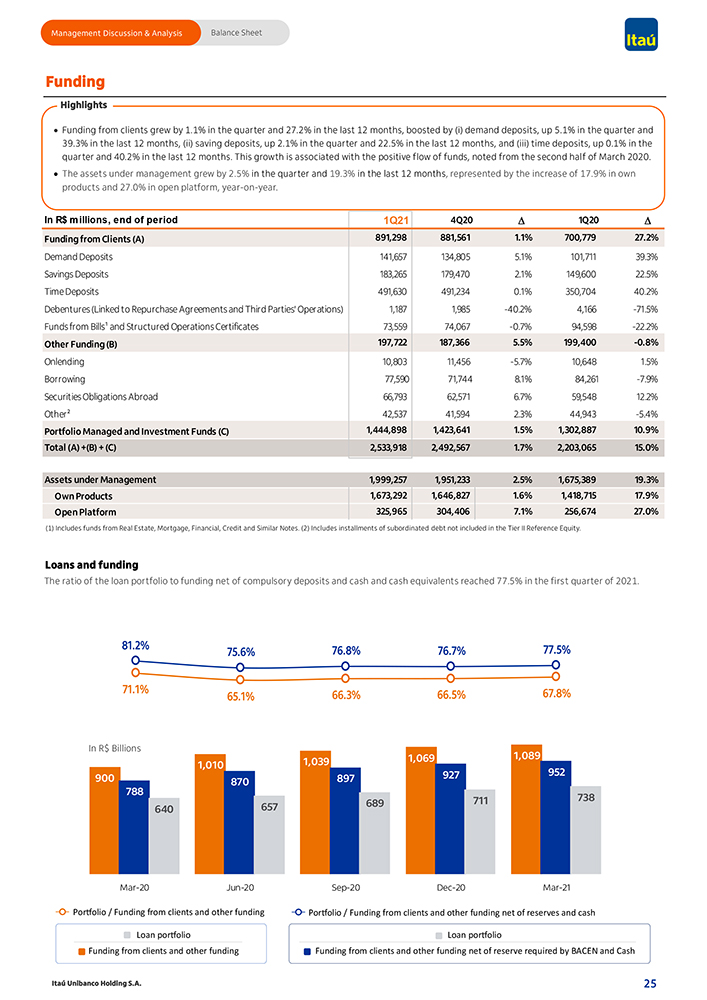

Management Discussion & Analysis Balance Sheet Funding Highlights • Funding from clients grew by 1.1% in the quarter and 27.2% in the last 12 months, boosted by (i) demand deposits, up 5.1% in the quarter and 39.3% in the last 12 months, (ii) saving deposits, up 2.1% in the quarter and 22.5% in the last 12 months, and (iii) time deposits, up 0.1% in the quarter and 40.2% in the last 12 months. This growth is associated with the positive flow of funds, noted from the second half of March 2020. • The assets under management grew by 2.5% in the quarter and 19.3% in the last 12 months, represented by the increase of 17.9% in own products and 27.0% in open platform, year-on-year. In R$ millions, end of period 1Q21 4Q20 D 1Q20 D Funding from Clients (A) 891,298 881,561 1.1% 700,779 27.2% Demand Deposits 141,657 134,805 5.1% 101,711 39.3% Savings Deposits 183,265 179,470 2.1% 149,600 22.5% Time Deposits 491,630 491,234 0.1% 350,704 40.2% Debentures (Linked to Repurchase Agreements and Third Parties’ Operations) 1,187 1,985 -40.2% 4,166 -71.5% Funds from Bills¹ and Structured Operations Certificates 73,559 74,067 -0.7% 94,598 -22.2% Other Funding (B) 197,722 187,366 5.5% 199,400 -0.8% Onlending 10,803 11,456 -5.7% 10,648 1.5% Borrowing 77,590 71,744 8.1% 84,261 -7.9% Securities Obligations Abroad 66,793 62,571 6.7% 59,548 12.2% Other² 42,537 41,594 2.3% 44,943 -5.4% Portfolio Managed and Investment Funds (C) 1,444,898 1,423,641 1.5% 1,302,887 10.9% Total (A) +(B) + (C) 2,533,918 2,492,567 1.7% 2,203,065 15.0% Assets under Management 1,999,257 1,951,233 2.5% 1,675,389 19.3% Own Products 1,673,292 1,646,827 1.6% 1,418,715 17.9% Open Platform 325,965 304,406 7.1% 256,674 27.0% (1) Includes funds from Real Estate, Mortgage, Financial, Credit and Similar Notes. (2) Includes installments of subordinated debt not included in the Tier II Reference Equity. Loans and funding The ratio of the loan portfolio to funding net of compulsory deposits and cash and cash equivalents reached 77.5% in the first quarter of 2021. 81.2% 76.8% 76.7% 77.5% 75.6% 71.1% 66.3% 66.5% 67.8% 65.1% In R$ Billions 1,069 1,089 1,010 1,039 927 952 900 870 897 788 711 738 657 689 640 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Portfolio / Funding from clients and other funding Portfolio / Funding from clients and other funding net of reserves and cash Loan portfolio Loan portfolio Funding from clients and other funding Funding from clients and other funding net of reserve required by BACEN and Cash Itaú Unibanco Holding S.A. 25

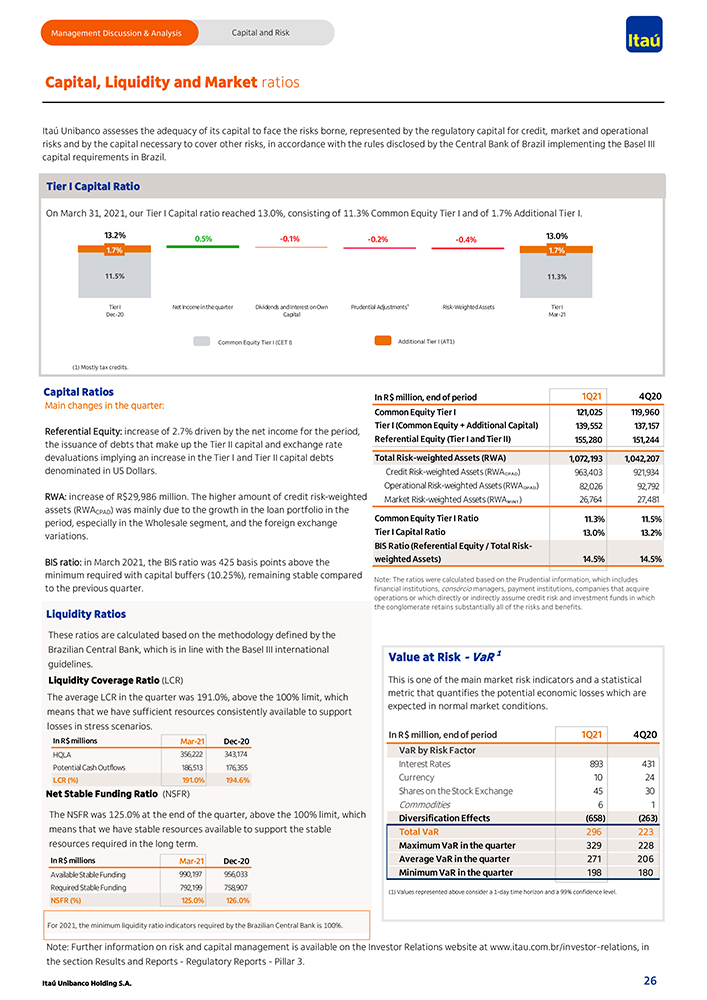

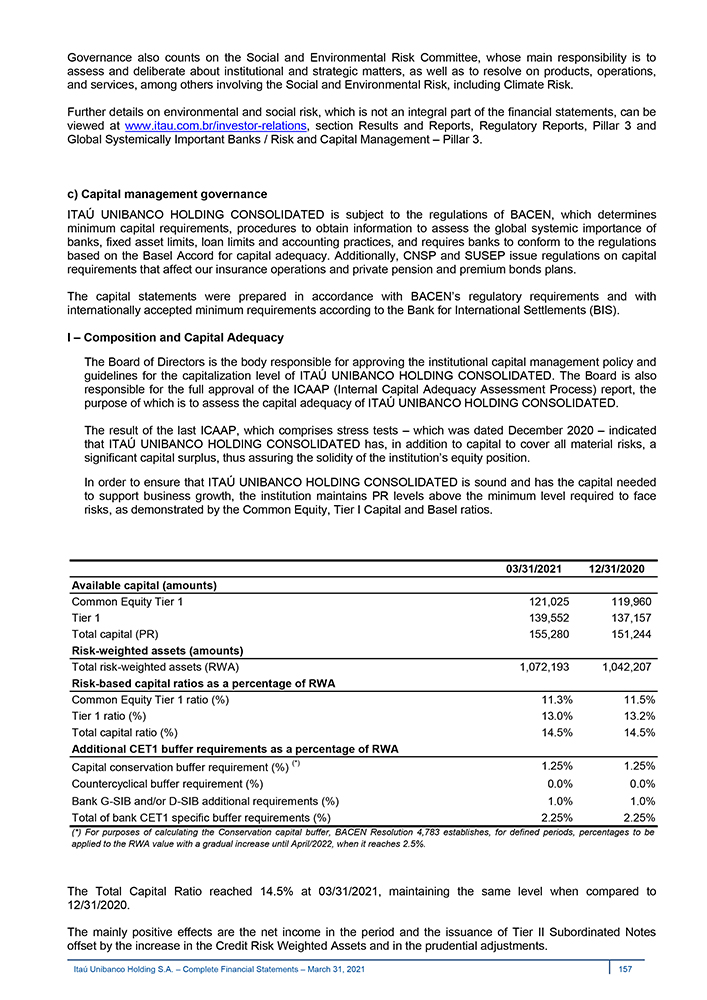

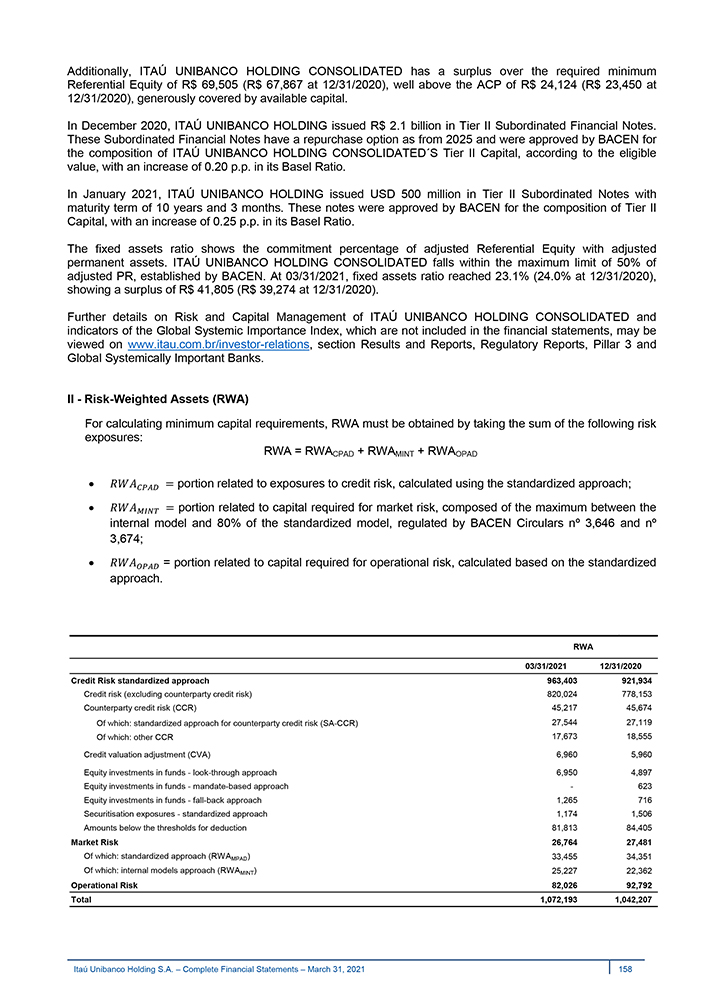

Management Discussion & Analysis Capital and Risk Capital, Liquidity and Market ratios Itaú Unibanco assesses the adequacy of its capital to face the risks borne, represented by the regulatory capital for credit, market and operational risks and by the capital necessary to cover other risks, in accordance with the rules disclosed by the Central Bank of Brazil implementing the Basel III capital requirements in Brazil. Tier I Capital Ratio On March 31, 2021, our Tier I Capital ratio reached 13.0%, consisting of 11.3% Common Equity Tier I and of 1.7% Additional Tier I. 13.2% 0.5% -0.1% -0.2% -0.4% 13.0% 1.7% 1.7% 11.5% 11.3% Tier I Net Income in the quarter Dividends and Interest on Own Prudential Adjustments¹ Risk-Weighted Assets Tier I Dec-20 Capital Mar-21 Common Equity Tier I (CET I) Additional Tier I (AT1) (1) Mostly tax credits. Capital Ratios Main changes in the quarter: Referential Equity: increase of 2.7% driven by the net income for the period, the issuance of debts that make up the Tier II capital and exchange rate devaluations implying an increase in the Tier I and Tier II capital debts denominated in US Dollars. RWA: increase of R$29,986 million. The higher amount of credit risk-weighted assets (RWACPAD) was mainly due to the growth in the loan portfolio in the period, especially in the Wholesale segment, and the foreign exchange variations. BIS ratio: in March 2021, the BIS ratio was 425 basis points above the minimum required with capital buffers (10.25%), remaining stable compared to the previous quarter. Liquidity Ratios These ratios are calculated based on the methodology defined by the Brazilian Central Bank, which is in line with the Basel III international guidelines. Liquidity Coverage Ratio (LCR) The average LCR in the quarter was 191.0%, above the 100% limit, which means that we have sufficient resources consistently available to support losses in stress scenarios. In R$ millions Mar-21 Dec-20 HQLA 356,222 343,174 Potential Cash Outflows 186,513 176,355 LCR (%) 191.0% 194.6% Net Stable Funding Ratio (NSFR) The NSFR was 125.0% at the end of the quarter, above the 100% limit, which means that we have stable resources available to support the stable resources required in the long term. In R$ millions Mar-21 Dec-20 Available Stable Funding 990,197 956,033 Required Stable Funding 792,199 758,907 NSFR (%) 125.0% 126.0% In R$ million, end of period 1Q21 4Q20 Common Equity Tier I 121,025 119,960 Tier I (Common Equity + Additional Capital) 139,552 137,157 Referential Equity (Tier I and Tier II) 155,280 151,244 Total Risk-weighted Assets (RWA) 1,072,193 1,042,207 Credit Risk-weighted Assets (RWACPAD) 963,403 921,934 Operational Risk-weighted Assets (RWAOPAD) 82,026 92,792 Market Risk-weighted Assets (RWAMINT ) 26,764 27,481 Common Equity Tier I Ratio 11.3% 11.5% Tier I Capital Ratio 13.0% 13.2% BIS Ratio (Referential Equity / Total Risk- weighted Assets) 14.5% 14.5% Note: The ratios were calculated based on the Prudential information, which includes financial institutions, consórcio managers, payment institutions, companies that acquire operations or which directly or indirectly assume credit risk and investment funds in which the conglomerate retains substantially all of the risks and benefits. Value at Risk—VaR 1 This is one of the main market risk indicators and a statistical metric that quantifies the potential economic losses which are expected in normal market conditions. In R$ million, end of period 1Q21 4Q20 VaR by Risk Factor Interest Rates 893 431 Currency 10 24 Shares on the Stock Exchange 45 30 Commodities 6 1 Diversification Effects (658) (263) Total VaR 296 223 Maximum VaR in the quarter 329 228 Average VaR in the quarter 271 206 Minimum VaR in the quarter 198 180 (1) Values represented above consider a 1-day time horizon and a 99% confidence level. For 2021, the minimum liquidity ratio indicators required by the Brazilian Central Bank is 100%. Note: Further information on risk and capital management is available on the Investor Relations website at www.itau.com.br/investor-relations, in the section Results and Reports—Regulatory Reports—Pillar 3. Itaú Unibanco Holding S.A. 26

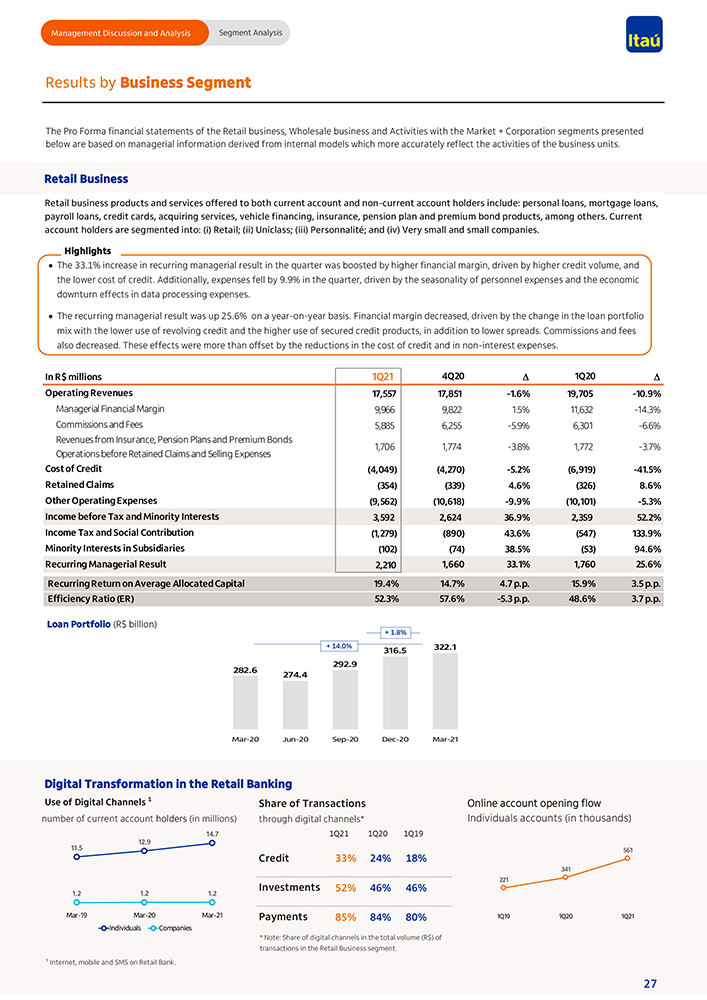

Management Discussion and Analysis Segment Analysis [Graphic Appears Here] Results by Business Segment The Pro Forma financial statements of the Retail business, Wholesale business and Activities with the Market + Corporation segments presented below are based on managerial information derived from internal models which more accurately reflect the activities of the business units. Retail Business Retail business products and services offered to both current account and non-current account holders include: personal loans, mortgage loans, payroll loans, credit cards, acquiring services, vehicle financing, insurance, pension plan and premium bond products, among others. Current account holders are segmented into: (i) Retail; (ii) Uniclass; (iii) Personnalité; and (iv) Very small and small companies. Highlights • The 33.1% increase in recurring managerial result in the quarter was boosted by higher financial margin, driven by higher credit volume, and the lower cost of credit. Additionally, expenses fell by 9.9% in the quarter, driven by the seasonality of personnel expenses and the economic downturn effects in data processing expenses. • The recurring managerial result was up 25.6% on a year-on-year basis. Financial margin decreased, driven by the change in the loan portfolio mix with the lower use of revolving credit and the higher use of secured credit products, in addition to lower spreads. Commissions and fees also decreased. These effects were more than offset by the reductions in the cost of credit and in non-interest expenses. In R$ millions 1Q21 4Q20 D 1Q20 D Operating Revenues 17,557 17,851 -1.6% 19,705 -10.9% Managerial Financial Margin 9,966 9,822 1.5% 11,632 -14.3% Commissions and Fees 5,885 6,255 -5.9% 6,301 -6.6% Revenues from Insurance, Pension Plans and Premium Bonds Operations before Retained Claims and Selling Expenses 1,706 1,774 -3.8% 1,772 -3.7% Cost of Credit (4,049) (4,270) -5.2% (6,919) -41.5% Retained Claims (354) (339) 4.6% (326) 8.6% Other Operating Expenses (9,562) (10,618) -9.9% (10,101) -5.3% Income before Tax and Minority Interests 3,592 2,624 36.9% 2,359 52.2% Income Tax and Social Contribution (1,279) (890) 43.6% (547) 133.9% Minority Interests in Subsidiaries (102) (74) 38.5% (53) 94.6% Recurring Managerial Result 2,210 1,660 33.1% 1,760 25.6% Recurring Return on Average Allocated Capital 19.4% 14.7% 4.7 p.p. 15.9% 3.5 p.p. Efficiency Ratio (ER) 52.3% 57.6% -5.3 p.p. 48.6% 3.7 p.p. Loan Portfolio (R$ billion) + 1.8% + 14.0% 316.5 322.1 292.9 282.6 274.4 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Digital Transformation in the Retail Banking Use of Digital Channels 1 Share of Transactions Online account opening flow number of current account holders (in millions) through digital channels* Individuals accounts (in thousands) 14.7 1Q21 1Q20 1Q19 12.9 11.5 561 Credit 33% 24% 18% 341 221 1.2 1.2 1.2 Investments 52% 46% 46% Mar-19 Mar-20 Mar-21 Payments 85% 84% 80% 1Q19 1Q20 1Q21 Individuals Companies * Note: Share of digital channels in the total volume (R$) of transactions in the Retail Business segment. ¹ Internet, mobile and SMS on Retail Bank. 27

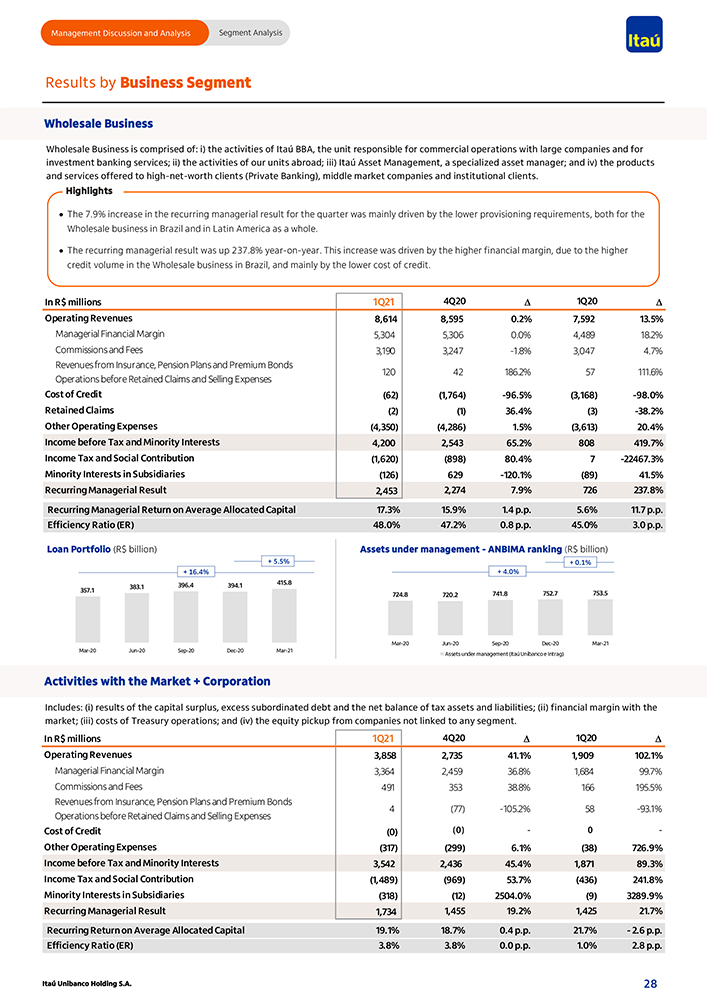

Management Discussion and Analysis Segment Analysis Results by Business Segment Wholesale Business Wholesale Business is comprised of: i) the activities of Itaú BBA, the unit responsible for commercial operations with large companies and for investment banking services; ii) the activities of our units abroad; iii) Itaú Asset Management, a specialized asset manager; and iv) the products and services offered to high-net-worth clients (Private Banking), middle market companies and institutional clients. Highlights • The 7.9% increase in the recurring managerial result for the quarter was mainly driven by the lower provisioning requirements, both for the Wholesale business in Brazil and in Latin America as a whole. • The recurring managerial result was up 237.8% year-on-year. This increase was driven by the higher financial margin, due to the higher credit volume in the Wholesale business in Brazil, and mainly by the lower cost of credit. In R$ millions 1Q21 4Q20 D 1Q20 D Operating Revenues 8,614 8,595 0.2% 7,592 13.5% Managerial Financial Margin 5,304 5,306 0.0% 4,489 18.2% Commissions and Fees 3,190 3,247 -1.8% 3,047 4.7% Revenues from Insurance, Pension Plans and Premium Bonds Operations before Retained Claims and Selling Expenses 120 42 186.2% 57 111.6% Cost of Credit (62) (1,764) -96.5% (3,168) -98.0% Retained Claims (2) (1) 36.4% (3) -38.2% Other Operating Expenses (4,350) (4,286) 1.5% (3,613) 20.4% Income before Tax and Minority Interests 4,200 2,543 65.2% 808 419.7% Income Tax and Social Contribution (1,620) (898) 80.4% 7 -22467.3% Minority Interests in Subsidiaries (126) 629 -120.1% (89) 41.5% Recurring Managerial Result 2,453 2,274 7.9% 726 237.8% Recurring Managerial Return on Average Allocated Capital 17.3% 15.9% 1.4 p.p. 5.6% 11.7 p.p. Efficiency Ratio (ER) 48.0% 47.2% 0.8 p.p. 45.0% 3.0 p.p. Loan Portfolio (R$ billion) Assets under management—ANBIMA ranking (R$ billion) + 5.5% + 0.1% + 16.4% + 4.0% 383.1 396.4 394.1 415.8 357.1 724.8 720.2 741.8 752.7 753.5 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Assets under management (Itaú Unibanco e Intrag) Activities with the Market + Corporation Includes: (i) results of the capital surplus, excess subordinated debt and the net balance of tax assets and liabilities; (ii) financial margin with the market; (iii) costs of Treasury operations; and (iv) the equity pickup from companies not linked to any segment. In R$ millions 1Q21 4Q20 D 1Q20 D Operating Revenues 3,858 2,735 41.1% 1,909 102.1% Managerial Financial Margin 3,364 2,459 36.8% 1,684 99.7% Commissions and Fees 491 353 38.8% 166 195.5% Revenues from Insurance, Pension Plans and Premium Bonds Operations before Retained Claims and Selling Expenses 4 (77) -105.2% 58 -93.1% Cost of Credit (0) (0)—0—Other Operating Expenses (317) (299) 6.1% (38) 726.9% Income before Tax and Minority Interests 3,542 2,436 45.4% 1,871 89.3% Income Tax and Social Contribution (1,489) (969) 53.7% (436) 241.8% Minority Interests in Subsidiaries (318) (12) 2504.0% (9) 3289.9% Recurring Managerial Result 1,734 1,455 19.2% 1,425 21.7% Recurring Return on Average Allocated Capital 19.1% 18.7% 0.4 p.p. 21.7%—2.6 p.p. Efficiency Ratio (ER) 3.8% 3.8% 0.0 p.p. 1.0% 2.8 p.p. Itaú Unibanco Holding S.A. 28

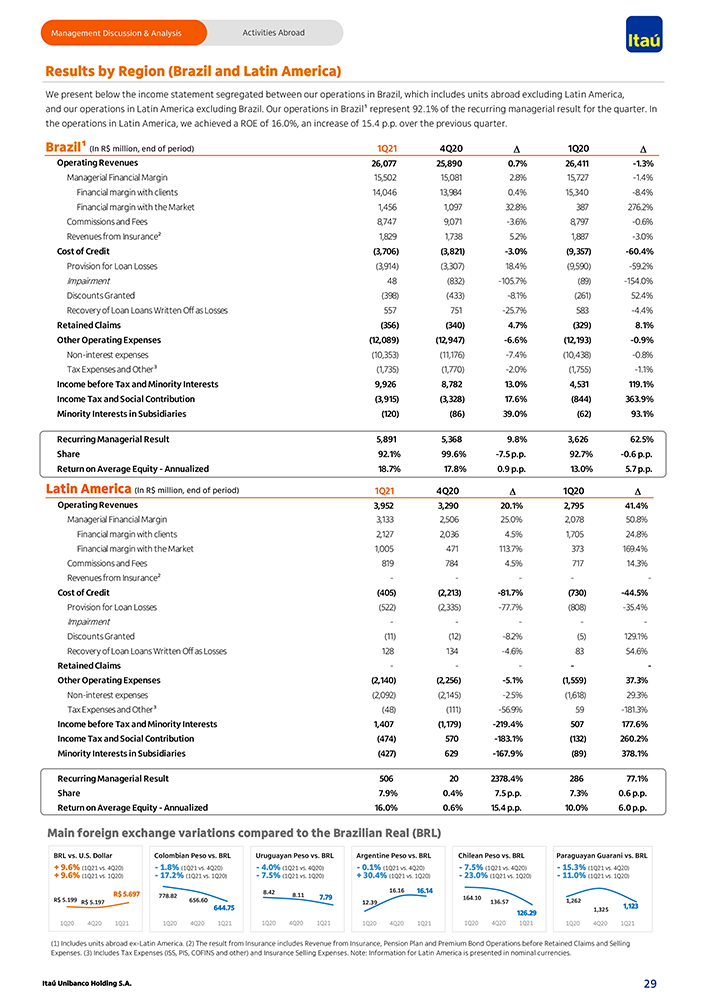

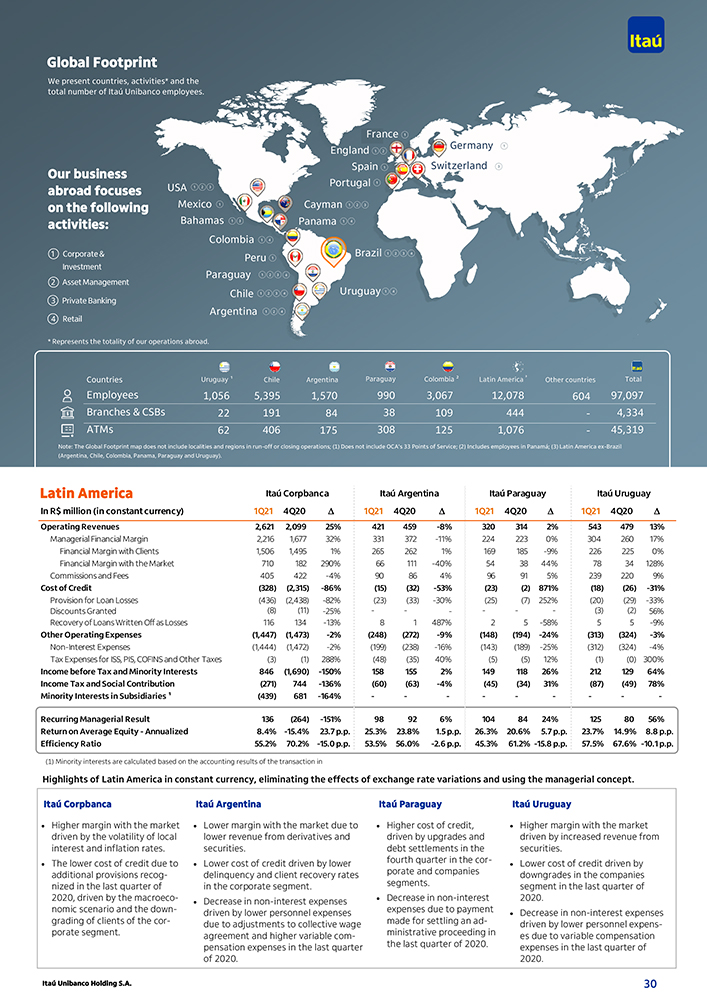

Management Discussion & Analysis Activities Abroad [Graphic Appears Here] Results by Region (Brazil and Latin America) We present below the income statement segregated between our operations in Brazil, which includes units abroad excluding Latin America, and our operations in Latin America excluding Brazil. Our operations in Brazil¹ represent 92.1% of the recurring managerial result for the quarter. In the operations in Latin America, we achieved a ROE of 16.0%, an increase of 15.4 p.p. over the previous quarter. Brazil¹ (In R$ million, end of period) 1Q21 4Q20 D 1Q20 D Operating Revenues 26,077 25,890 0.7% 26,411 -1.3% Managerial Financial Margin 15,502 15,081 2.8% 15,727 -1.4% Financial margin with clients 14,046 13,984 0.4% 15,340 -8.4% Financial margin with the Market 1,456 1,097 32.8% 387 276.2% Commissions and Fees 8,747 9,071 -3.6% 8,797 -0.6% Revenues from Insurance² 1,829 1,738 5.2% 1,887 -3.0% Cost of Credit (3,706) (3,821) -3.0% (9,357) -60.4% Provision for Loan Losses (3,914) (3,307) 18.4% (9,590) -59.2% Impairment 48 (832) -105.7% (89) -154.0% Discounts Granted (398) (433) -8.1% (261) 52.4% Recovery of Loan Loans Written Off as Losses 557 751 -25.7% 583 -4.4% Retained Claims (356) (340) 4.7% (329) 8.1% Other Operating Expenses (12,089) (12,947) -6.6% (12,193) -0.9% Non-interest expenses (10,353) (11,176) -7.4% (10,438) -0.8% Tax Expenses and Other³ (1,735) (1,770) -2.0% (1,755) -1.1% Income before Tax and Minority Interests 9,926 8,782 13.0% 4,531 119.1% Income Tax and Social Contribution (3,915) (3,328) 17.6% (844) 363.9% Minority Interests in Subsidiaries (120) (86) 39.0% (62) 93.1% Recurring Managerial Result 5,891 5,368 9.8% 3,626 62.5% Share 92.1% 99.6% -7.5 p.p. 92.7% -0.6 p.p. Return on Average Equity—Annualized 18.7% 17.8% 0.9 p.p. 13.0% 5.7 p.p. Latin America (In R$ million, end of period) 1Q21 4Q20 D 1Q20 D Operating Revenues 3,952 3,290 20.1% 2,795 41.4% Managerial Financial Margin 3,133 2,506 25.0% 2,078 50.8% Financial margin with clients 2,127 2,036 4.5% 1,705 24.8% Financial margin with the Market 1,005 471 113.7% 373 169.4% Commissions and Fees 819 784 4.5% 717 14.3% Revenues from Insurance² — ——Cost of Credit (405) (2,213) -81.7% (730) -44.5% Provision for Loan Losses (522) (2,335) -77.7% (808) -35.4% Impairment — ——Discounts Granted (11) (12) -8.2% (5) 129.1% Recovery of Loan Loans Written Off as Losses 128 134 -4.6% 83 54.6% Retained Claims — ——Other Operating Expenses (2,140) (2,256) -5.1% (1,559) 37.3% Non-interest expenses (2,092) (2,145) -2.5% (1,618) 29.3% Tax Expenses and Other³ (48) (111) -56.9% 59 -181.3% Income before Tax and Minority Interests 1,407 (1,179) -219.4% 507 177.6% Income Tax and Social Contribution (474) 570 -183.1% (132) 260.2% Minority Interests in Subsidiaries (427) 629 -167.9% (89) 378.1% Recurring Managerial Result 506 20 2378.4% 286 77.1% Share 7.9% 0.4% 7.5 p.p. 7.3% 0.6 p.p. Return on Average Equity—Annualized 16.0% 0.6% 15.4 p.p. 10.0% 6.0 p.p. Main foreign exchange variations compared to the Brazilian Real (BRL) BRL vs. U.S. Dollar Colombian Peso vs. BRL Uruguayan Peso vs. BRL Argentine Peso vs. BRL Chilean Peso vs. BRL Paraguayan Guarani vs. BRL + 9.6% (1Q21 vs. 4Q20)—1.8% (1Q21 vs. 4Q20)—4.0% (1Q21 vs. 4Q20)—0.1% (1Q21 vs. 4Q20)—7.5% (1Q21 vs. 4Q20)—15.3% (1Q21 vs. 4Q20) + 9.6% (1Q21 vs. 1Q20)—17.2% (1Q21 vs. 1Q20)—7.5% (1Q21 vs. 1Q20) + 30.4% (1Q21 vs. 1Q20)—23.0% (1Q21 vs. 1Q20)—11.0% (1Q21 vs. 1Q20) R$ 5.697 778.82 8.42 8.11 7.79 16.16 16.14 R$ 5.199 R$ 5.197 656.60 12.39 164.10 136.57 1,262 644.75 126.29 1,325 1,123 1Q20 4Q20 1Q21 1Q20 4Q20 1Q21 1Q20 4Q20 1Q21 1Q20 4Q20 1Q21 1Q20 4Q20 1Q21 1Q20 4Q20 1Q21 (1) Includes units abroad ex-Latin America. (2) The result from Insurance includes Revenue from Insurance, Pension Plan and Premium Bond Operations before Retained Claims and Selling Expenses. (3) Includes Tax Expenses (ISS, PIS, COFINS and other) and Insurance Selling Expenses. Note: Information for Latin America is presented in nominal currencies. Itaú Unibanco Holding S.A. 29