UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934:

For the fiscal year ended: December 31, 2019

☐Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934:

For the transition period from:

| XG SCIENCES, INC. | ||||

| (Exact name of registrant as specified in its charter) |

| Michigan | 333-209131 | 20-4998896 | ||

| (State or other jurisdiction of incorporation or organization) | (Commission File No.) | (I.R.S. Employer Identification No.) |

3101 Grand Oak Drive

Lansing, MI 48911

(Address of principal executive offices) (zip code)

(517) 703-1110

(Issuer Telephone number)

Securities registered under Section 12(b) of the Act: None.

Securities registered under Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes☐ No☒

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☒ No☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes☒ No☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes☐ No☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, and whether the registrant is an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company ☒ |

Emerging growth company☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.☒

As of December 31, 2019, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $25,359,328, based on the price at which the common equity was last sold (i.e., $8.00 per share).

The number of shares outstanding of the registrant’s common stock, no par value per share, as of April 29, 2020 was 4,024,443.

TABLE OF CONTENTS

Note Regarding Forward-Looking Statements:

The information in this Annual Report on Form 10-K contains “forward-looking statements” and information within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) relating to XG Sciences, Inc., a Michigan corporation and its subsidiary, XG Sciences IP, LLC, a Michigan corporation (collectively referred to as “we”, “us”, “our”, “XG Sciences”, “XGS”, or the “Company”), which are subject to the “safe harbor” created by those sections. These forward-looking statements include, but are not limited to, statements concerning our strategy, future operations, future financial position, future revenues, projected costs, prospects and plans and objectives of management. The words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements.

These forward-looking statements involve known and unknown risks and uncertainties that could cause our actual results, performance or achievements to differ materially from those expressed or implied by the forward-looking statements, including, without limitation, the risks set forth beginning on page 13 under the section entitled “Risk Factors” herein.

XG Sciences was formed in May 2006 for the purpose of commercializing certain technology to produce graphene nanoplatelets and integrated, value-added products containing graphene nanoplatelets. First isolated and characterized in 2004, graphene is a single layer of carbon atoms configured in an atomic-scale honeycomb lattice. Among many noted properties, monolayer graphene is harder than diamonds, lighter than steel but significantly stronger, and conducts electricity better than copper. Graphene nanoplatelets are particles consisting of multiple layers of graphene. Graphene nanoplatelets have unique capabilities for energy storage, thermal conductivity, electrical conductivity, barrier properties, lubricity and the ability to impart physical property improvements when incorporated into plastics, metals or other matrices.

We believe the unique properties of graphene and graphene nanoplatelets will enable numerous new product applications and the market for such products will quickly grow to be a significant market opportunity. Our business model is to design, manufacture and sell advanced materials we call xGnP®graphene nanoplatelets and value-added products incorporating xGnP® graphene nanoplatelets. We currently have hundreds of customers trialing our products for numerous applications, including, but not limited to lithium ion batteries, lead acid batteries, thermally conductive adhesives, composites, thermal management and heat transfer, inks and coatings, printed electronics, construction materials, cement, 3-D printing and in a range of other industrial uses. We believe our proprietary processes have enabled us to be a low-cost producer of high-quality, graphene nanoplatelets and value-added integrated products containing graphene nanoplatelets and that we are well positioned to address a wide range of end-use applications.

1

Our Customers

We sell products to customers around the world and have sold materials to over 1,300 customers in 47 countries since 2008. Some of these customers are research organizations and some are commercial organizations. Our customers have included well-known automotive and OEM suppliers around the world (Ford, Johnson Controls, Magna, Honda Engineering), world-scale lithium ion battery manufacturers in the US, South Korea and China (Samsung SDI, LG Chemical, Lishen, A123) , diverse specialty material companies (3M, BASF, Henkel, Dow Chemical, DuPont) and leading research centers such as Lawrence Livermore National Laboratory and Oakridge National Laboratory. The majority of our customers are still ordering in small quantities consistent with their development and qualification work, although others have started to order in 10’s to 100’s of kilograms and some at the metric ton level.

We have also licensed some of our base manufacturing technology to other companies. Our licensees include POSCO, the fifth largest steel manufacturer in the world by 2018 tonnage output, and Cabot Corporation (“Cabot”), a leading global specialty chemicals and performance materials company. These licensees further extend our technology through their customer networks. Ultimately, we believe we may benefit in terms of royalties on sales of xGnP® graphene nanoplatelets produced and sold by our licensees.

Our Products

XG Sciences is a manufacturer of graphene nanoplatelets and value-added products that contain graphene nanoplatelets. The term “graphene” is used widely in the literature and the popular press to cover a variety of specific forms of the material. We generally think about two broad classes of graphene materials:

| 1. | One-atom thick films of carbon commonly referred to as monolayer graphene, manufactured typically from gases by assembling molecules to form relatively large, transparent sheets of material. These materials have been characterized by their performance attributes that differentiate them from other advanced materials and that may include: 200 times stronger than steel, flexible and able to stretch up to 25% of its original length, optically transparent, more electrically conductive than copper, more thermally conductive than any other known material and atomic-level barrier properties. XG Sciences does not manufacture these films and does not participate in the markets for these films and believes that, in general, the markets for these films do not compete with those for graphene nanoplatelets. |

| 2. | Ultra-thin particles of carbon that consist of layers of graphene sheets ranging in thickness from a few layers to many layers – that are commonly referred to as graphene nanoplatelets (“GNP” or “GNPs”). Because GNPs are thin and can be manufactured in a range of diameters, they are useful for a wide variety of applications. XG Sciences manufactures GNPs that range in thickness from a few nanometers and up to 10-20 nanometers and with diameters ranging from less than 1 micron and up to 100 microns. The manufacture of these graphene particles is our main area of expertise, and their use in practical applications is the focus of our sales, marketing and development activities. |

2

The well-publicized isolation and characterization of graphene in 2004 at the University of Manchester, has spawned a new class of 2D materials based on layers of carbon atoms arranged in a hexagonal array and each carbon having lone pair electrons. The unique characterization and related performance of this new class of materials is derived from their two-dimensional nature and their composition of sp2carbon atoms arranged in a hexagonal array. The ability of any new material to be exploited in industrial applications will depend on its fit-for-performance. In the case of graphene nanoplatelets, the fit-for-performance is very much related to their aspect ratio (among other factors) in that the diameter is typically significantly greater than the thickness. This is what differentiates the material from bulk graphite of high crystallinity and purity. We classify nanoplatelets consisting of largely basal planes of carbon atoms packed in a hexagonal array (i.e., graphene) as graphene nanoplatelets so long as their aspect ratio may be classified as two-dimension and are thus in the form of platelets. Such a definition implies that the thickness is nanoscale – GNPs having a thickness in the range from generally 0.6 nanometers and up to many 10’s of nanometers. We have chosen to utilize the definitions as set out by the Carbon Journal editorial team (Carbon, volume 65, pp.1-6) and Fullerex (Bulk Graphene Pricing Report, 2019) which provides classification for the various material types which provide meaningful descriptions of commercially available graphene.

Graphene Product Definitions Based on Layer Thickness

| Number of Layers | Product Description | |

| 1 | Graphene (monolayer) | |

| 1-3 | Very Few Layer Graphene (vFLG) | |

| 2-5 | Few Layer Graphene (FLG) | |

| 2-10 | Multilayer Graphene (MLG) | |

| >10 | Graphene Nanoplatelets (GNPs) |

Bulk Materials.

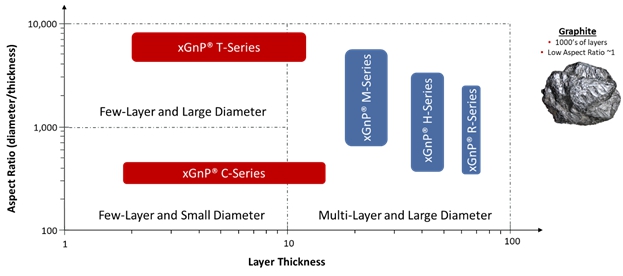

We sell bulk materials under the trademarked brand name of xGnP®graphene nanoplatelets. These materials are produced in various grades, which are analogous to average platelet thickness, and average platelet diameters. There are three commercial grades (Grades H, M & R), each of which is offered in three standard platelet diameters and a fourth, C Grade, which is offered in three standard surface areas. We also have access to other development grades (Grade T, for example), but which are not yet made available commercially and have been used internally for those products containing graphene nanoplatelets. These bulk materials, which normally ship in the form of a dry powder, are especially applicable for use as additives in polymeric or metallic composites, or in coatings or other formulations where particular electrical, thermal or barrier performance are desired by our customers. We also offer our material in the form of dispersions of nanoplatelets in liquids such as water, alcohol, or organic solvents, or mixed into resins or polymers such as thermoplastics or thermosets. We use two different commercial processes to produce these bulk materials:

| Grade H/M/R/T materials are produced through chemical intercalation of natural graphite followed by thermal exfoliation using a proprietary process developed by us. The “grade” designates the thickness and surface characteristics of the material, and each grade is available in various average particle/platelet diameters. Surface area, calculated by the Brunauer, Emmet, and Teller (BET) Method, is used as a convenient proxy for thickness, so each grade of products produced through chemical intercalation is designated by its average surface area, which ranges from 50 to 150 m2/gram of material. We are able to extend the surface area higher (250 m2/gram for T Grade) but are not yet producing these materials in metric-ton quantities. As the market need emerges for this class of materials, we anticipate scaling them. For example, we introduced a new Grade of xGnP® powders, R-Grade, with improved electrical conductivity targeting use in applications for electrically and thermally conductive ink and composites and have scaled R-Grade to metric-ton quantities. |

| Grade C materials are produced through a high-shear mechanical exfoliation using a proprietary process and equipment that we invented, designed, constructed and patented. The Grade C materials are smaller platelet diameters than those grades produced through chemical exfoliation, and Grade C materials are designated by their BET surface area, which ranges from 300 to 800 m2/gram. We are able to produce C-Grade materials having other surface areas and may make those available commercially as needed by our customers. |

The following graphic depicts xGnP®graphene nanoplatelets as a function of both layer thickness and aspect ratio (thickness by diameter), two key parameters which will influence their performance in a range of industrial applications. The performance of graphene nanoplatelets in a specific application is primarily a function of the platelet’s diameter, thickness, planarity (or more broadly – morphology), and, to some extent, the nature and concentration of any chemical groups on the platelets. There are other factors that may impact performance, such as optimized dispersion, product form delivered to the customer (powder vs. slurry), and so on. However, for the most part, performance in an application is related to the physical characteristics of the nanoplatelets. XG Sciences is skilled in the design and manufacture of graphene nanoplatelets and our two proprietary manufacturing processes allow for the production of a broad product portfolio varying across a broad range of both thickness and diameter, the two variables most likely related to performance in a range of end-use applications.

3

XG Sciences’ Graphene Nanoplatelet Product Portfolio and Versus Graphite

We believe we are a “platform play” in advanced materials, because our proprietary processes allow us to produce varying grades of graphene nanoplatelets that may be mapped to a variety of applications and in many end-use market segments. While we supply bulk materials consisting of various forms of xGnP® graphene nanoplatelets and in the form of dispersions of nanoplatelets in liquids such as water, alcohol or organic solvents, we also produce products that contain graphene nanoplatelets which we refer to as integrated products. We have done this to further differentiate our products from those potential suppliers offering only graphene nanoplatelets in powder form.

Composites. Our composites, integrated-products portfolio includes resins derived from a range of thermoplastics and thermosets into which our xGnP® graphene nanoplatelets are compounded. These products are supplied as master batches of resins with graphene nanoplatelets pre-dispersed such that their performance has been optimized for use in various end-use applications that may include industrial, automotive and sporting goods and which have demonstrated efficacy in standard injection molding, compression molding, blow molding and 3-D processes, to name but a few. Our current product portfolio of polymer resins containing various forms of our xGnP®graphene nanoplatelets and in varying concentration includes polyurethane (XGPU), polypropylene (XGPP), polyethylene terephthalate (XGPET), vinyl ester (XGVE), polyetherimide (XGPEI) and high-density polyethylene (XGHDPE). Other polymers may be added over time depending on the end-market and customer needs. In addition, we offer various bulk materials with demonstrated efficacy in plastic composites to impart improved physical performance to such matrices, which may be supplied as dry powders or as aqueous-based or solvent-based dispersions or cakes, as described previously. We have also targeted use of our graphene nanoplatelets as an additive in cement mixtures which we believe results in improved barrier resistance, durability, toughness and corrosion protection. Our GNP Concrete Additive product promotes the formation of more uniform and smaller-grain cement structure, improving both flexural and compressive strength. In addition, the embedded graphene nanoplatelets will stop cracks from forming and retard crack propagation, should any cracks form – the combination of which will further improve cement lifetime and durability.

Inks and Coatings. These consist of specially formulated dispersions of xGnP®together with solvents, binders, and other additives to make electrically or thermally conductive products designed for printing or coating and which are showing promise in diverse customer applications such as advanced packaging, electrostatic dissipation and thermal management. We also offer a set of standardized ink formulations suitable for printing. These inks offer the capability to print electrical circuits or antennas and may be suitable for other electrical or thermal applications and can be further customized for specific customer requirements.

Energy Storage Materials. These consist of specialty advanced materials that have been formulated for specific applications in the energy storage segment. We offer various bulk materials for use as conductive additives for cathodes and anodes in lithium-ion batteries, as additives to anode slurries for lead-carbon batteries, as a component in coatings for current collectors used in lithium-ion batteries and we are investigating the use of our materials as part of other energy-storage components.

4

Thermal Management Materials. These consist mainly of various thermal interface materials (“TIM’s”) in the form of custom greases or pastes. Our custom thermal interface materials are also designed to be used in various high temperature environments. Additionally, we offer various bulk materials for use as active components in adhesives, liquids, coatings and plastic composites to impart improved thermal management performance to such matrices.

Our Focus Areas

We prioritize our efforts in specific areas and with specific customers that we believe represent opportunities for either relatively near-term revenue or especially large and attractive markets. At this time, we are focused on four key vertical markets: Automotive, Sporting Goods, Packaging and Industrial. The following graphic provides examples of target applications within each of the four key verticals where XG Sciences has either commercial sales or is in development with one or more customers.

XGS Market/Application Focus Areas

Addressable Markets

The markets for our materials are large and growing. As one example, the 2019 North American packaging market for plastic bottles and containers was estimated to be more than $34 billion (Mordor Intelligence). Further, Mordor estimated the 2019 global market for PET water bottles at 543.8 billion units. XG Sciences is engaged with customers in North America targeting the use of xGnP® graphene nanoplatelets in a range of packaging applications, including water bottles, and we are expanding our market activities into other geographies. If each water bottle produced in 2019 were to incorporate just 1 milligram of xGnP®graphene nanoplates, the total revenue available to XG Sciences may range from $200 to $300 million, depending on product form. A second example is for use in tires where graphene-based products may bring significant advancements. A typical tire is a composite of several parts: sidewalls, inner liner and the tire tread - which itself is a rubber component comprising a steel chord reinforcement of a particulate-reinforced rubber network. If one considers that the tire tread is the only part of the vehicle’s contact with the road, it becomes apparent that all sources of energy dissipation are via the tread material and will have a major influence on total performance such as handling, fuel efficiency and braking performance. Data are starting to show that incorporation of graphene nanoplatelets into the production of a tire tread can significantly impact the rolling resistance and abrasion resistance, both of which will result in improved fuel efficiency and tire lifetime. These performance attributes also seem to come with improvements in such properties as tear strength and tensile performance, allowing formulators to target a wide range of passenger vehicle, truck and off-road applications. Based on data from the European Rubber Journal (January 9, 2019 and according the International Rubber Study Group), the 2019 global rubber market used in tires is estimated at 30 million metric tons. If graphene is used in only 20% of tires and adopted at 1 weight percent based on the rubber content, then the demand could easily exceed 60,000 metric tons for graphene-related materials. In a third example, there is an industry-wide need to continue to drive light weighting in vehicles. The primary objective is to save on fuel consumption for cars still using internal combustion engines, but also to extend drive time for emerging electrical vehicles. Data from the Department of Energy (“Materials Technologies: Goals, Strategies, and Top Accomplishments”, Department of Energy, Vehicle Technologies Program, August 2010) indicate that in 1977, conventional steel comprised 75% of the materials used in the manufacture of an auto. By 2010, that number was reduced to about 65% with a significant increase in high-strength steel, aluminum and polymer composites. In order to meet the industry light-weighting targets, it is estimated that by 2035, polymer composite usage will increase to 20% of all materials. Improvements to today’s composite materials are needed for this to occur and graphene nanoplatelets are a good candidate to enable the broad adoption of polymer composites for use in automotive manufacture. In 2018, 71 million cars were produced globally (Estimated Worldwide automobile production, Statista.com). If we assume an average car weights 1500 kilograms (DOE Lightweighting Efforts for Sustainable Transportation”,2nd Lightweighting summit, March 5, 2015) and based on DOE estimates (“Materials Technologies: Goals, Strategies, and Top Accomplishments”, Department of Energy, Vehicle Technologies Program, August 2010), approximately 100 kilograms is comprised of polymers/composites (and certainly the potential for more in the future), and if graphene-related products were to be adopted at just 1 weight percent, then there is the potential demand of over 71,000 metric tons for graphene-related materials.

5

Commercialization Process

Because graphene is a new material, most of our customers are still developing applications that use our products. Commercialization is a process, the exact timing of which is often difficult to predict. It starts with our own internal R&D to validate performance for an identified market or customer-specific need. Our customers then validate the performance of our materials and determine whether our products can be incorporated into their manufacturing processes. This is initially done at pilot production scale levels. Our customers then introduce products incorporating our materials to their own customers to further validate performance. After their customers have validated performance, our customers will then move to commercial scale production. Every customer goes through the same process, but will do so at varying speeds, depending on the customer, the product application and the end-use market. Thus, we are not always able to predict when our customers will begin ordering commercial volumes of our materials or predict their expected volumes over time. However, as customers move through the process, we generally receive feedback and gain greater insights regarding their commercialization plans. According to our respective customers, the following are just some examples of where our products are providing value to our customers at levels that are either in commercial production or we believe will warrant their use on a commercial basis:

| ● | In 2018, Callaway Golf Company introduced new dual-core Chrome Soft and Chrome Soft X golf balls incorporating our xGnP®graphene nanoplatelets into the outer core, resulting in a new class of golf ball that enables higher driving speeds, greater distance and increased control, which is allowing Callaway to command a premium price for their golf balls in the marketplace and in 2019 expanded the technology to incorporate our xGnP® into the E·R·C Soft line of golf balls; and |

| ● | Ford Motor Company for polyurethane based foams for use in Ford and Lincoln light truck and passenger car, demonstrating a 17 percent enhancement in Noise, Vibration and Harshness (NVH) sound absorption, a 20 percent improvement in mechanical properties and a 30 percent improvement in heat endurance properties, compared with that of the foam used without graphene; and |

| ● | Light emitting diode module and product company demonstrated approximately 50% improvement in thermal management capability when compared to existing commercial thermal management products, translating into a 15% improvement in thermal management at the device level; and |

| ● | Lead acid battery manufacturers incorporating our materials in the commercial supply of batteries demonstrating improvements in measured cycle life, capacity and charge acceptance; and |

| ● | U.S. bottling company adopting commercial use of our graphene nanoplatelets in PET water bottles to improve modulus (10% with minimal affect to color and up to 200% with color change), shelf life and energy savings during processing; and |

| ● | Plastics composite part manufacturer demonstrating 7-30% improvement in strength and 40% improvement in modulus when used in sheet molding compound; and |

| ● | Plastic composite parts manufacturer demonstrating 25% increase in tensile strength and 15% improvement in flex modulus for a high-density polyethylene composite, and Plastics manufacturer demonstrating up to 25% increase in tensile modulus, 15% increase in tensile strength and 8x increase in puncture impact for nylon-based thermoplastics. |

The process of “designing-in” new materials is relatively complex and involves the use of relatively small amounts of the new material in laboratory and engineering development for an extended period of time. Following successful development, customers that incorporate our materials into their products will then order much larger quantities of material to support commercial production. Although, our customers are under no obligation to report to us on the usage of our materials, some have indicated that they have introduced or will soon introduce commercial products that use our materials. Thus, while many of our customers are currently purchasing our materials in kilogram (one or two pound) quantities, some have begun to purchase at multiple ton quantities and we believe many will require tens of tons or even hundreds of tons of material as they commercialize products that incorporate our materials. We also believe that those customers already in production will increase their order volume as demand increases and others will begin to move into commercial volume production as they gain more experience in working with our materials and engage new customers.

Commercialization Trends

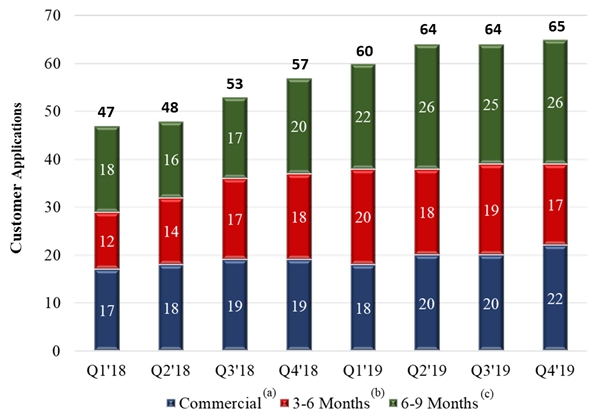

We are tracking the commercial and development status of more than 75 different customer applications using our materials with some customers pursuing multiple applications. As of December 31, 2019, we had twenty-two (22) specific customer applications where our materials are incorporated into our customers’ products and such customers are actively selling these products to their own customers. In addition, we have another seventeen (17) customer applications where our customers have indicated that they expect to begin shipping product incorporating our materials in the next 3 – 6 months and have another twenty-six (26) customer applications where our customers have indicated an intent to commercialize in the next 6 – 9 months. We are also working with numerous additional customers that have not yet indicated an exact date for commercialization, but we believe have the potential to contribute to meaningful revenue in 2020 and 2021. The following graphic demonstrates the commercialization trends over the past 8 fiscal quarters as an increasing number of customers indicate their intent to commercialize applications and move into actively selling or promoting products for future sales.

6

| (a) | Customer applications where our materials are used in customer products and they are actively selling them to their customers or actively promoting them for future sales. |

| (b) | Customer applications where our customers are indicating that they expect to begin shipping products incorporating our materials in the next 3-6 months. |

| (c) | Customer applications where our customers are indicating an intent to commercialize in the next 6-9 months. |

Our Intellectual Property

Some of our proprietary manufacturing processes were developed at Michigan State University (MSU) and licensed to us in 2006. We license three U.S. patents and patent applications from MSU. On August 8, 2016, we signed an agreement acquiring an exclusive license with Metna Co. (Metna) to Metna’s background IP for use of graphene nanoplatelets as additives to concrete mixtures. For purposes of the agreement, Metna’s background IP relates to the U.S. Patent 8,951,343. Also, on August 8, 2016, we entered into a second agreement for an exclusive license related to all Metna’s background technology and foreground technology, including any jointly owned foreground technology where the end use is known to be any graphite additive dispersed in concrete mixtures. On April 25, 2019 we signed an Intellectual Property License, Joint Development and Commercialization Agreement with Niagara Bottling acquiring exclusive license to certain of Niagara’s patents and applications relating to the use of graphene nanoplatelets in packaging applications. For purposes of the agreement, Niagara’s IP relates to five (5) U.S. patents and patent applications and two (2) international applications. Over time, our scientists and engineers have made many further discoveries and inventions that, as of December 31, 2019, are embodied in the form of : seventeen (17) additional U.S. patents, twenty-three (23) foreign patents, twelve (12) additional U.S. patent applications and numerous trade secrets. For many of the applications filed in the U.S., additional filings are made in other countries such as the European Union, Japan, South Korea, China, Taiwan or other applicable countries. As of December 31, 2019, we maintained twenty-three (23) international patent applications. These filings and analyses are made on a case-by-case basis. Typically, patents that are defensive in nature are not filed abroad, while those that are protective of active XGS products or applications are filed in relevant countries abroad. Our general IP strategy is to keep as trade secrets those manufacturing processes that are difficult to enforce should they be disclosed and to seek patent coverage for other manufacturing processes, materials derived from those processes, unique combinations of materials and end uses of materials containing graphene nanoplatelets. We believe that the combination of our rights under various licenses, our patents and patent applications, and our trade secrets create a robust intellectual property position.

7

Our Manufacturing Capacity

We completed the first phase of expansion in our 64,000 square-foot facility located in Mason, MI in the first half of 2018. The expansion has added 90 metric tons of graphene nanoplatelet production capacity, bringing the total capacity of the facility up to approximately 180 metric tons of dry powder. Phase two of the expansion was partially complete by year-end 2018 and resulted in up to ~270 metric tons of total graphene nanoplatelet output capacity at the facility. We completed the last portion of the Phase two expansion in the first half of 2019, resulting in up to ~400 metric tons of total graphene nanoplatelet output capacity. Manufacturing capacity is a function of product mix within a given facility. We make a range of products in our facilities that vary in their manufacturing time. It is therefore practical to consider capacity as an output range in order to reflect product mix. Our annual graphene nanoplatelet output capacity across both of our manufacturing facilities, as of December 31, 2019, ranged from approximately 225 metric tons up to approximately 450 metric tons. XG’s increasing graphene nanoplatelet capacity will support the growing demand for our products over the next several fiscal quarters and will serve as input materials to integrated products containing our graphene nanoplatelets. However, additional manufacturing capabilities for certain value-added products and certain bulk materials remain to be developed and may require the acquisition of additional facilities. In particular, the production processes for certain integrated products will require additional capital and may require additional facilities to meet expected future customer demand.

Some of the Company’s products are new products that have not yet been fully developed and for which manufacturing operations have not yet been fully scaled. Although we believe we will continue to scale our production capability and revenue in 2020, for some target products we have not yet demonstrated the capability to produce sufficient materials to generate the ongoing revenues necessary to sustain our operations in the long-term. For other target products, we have demonstrated sufficient scale to reach revenue and profits resulting in cash positive status, however, the impact of COVID-19 on our customer’s production plans and the ability for those customer with whom we are in development to introduce new products, may impact our ability to meet our commercial targets for the foreseeable future. For additional information please see “Risk Factors” herein.

Our Lead Investors

Since inception and through December 31, 2019, we have raised approximately $50 million of capital through the issuance of equity and equity-linked securities, $4 million through licensing fees and $10 million through the issuance of certain lease and senior debt obligations. Each of the entities below, after considerable due diligence, decided to take an equity position, license some of our technology or provided funding in the form of a secured loan. Notable investors and licensees in the Company are included in the funding history of the Company summarized below.

| Timing | Investor Class | Amount | ||

| 2006-2009 | Angel Groups, HNW Individuals | $2 million | ||

| 2010 | Hanwha Chemical | $3 million | ||

| 2010 | ASC-XGS, LLC | $1.6 million | ||

| 2011 | POSCO | $4 million | ||

| 2011 | Cabot Corp | $4 million license agreement | ||

| 2014 | Samsung Ventures | $3 million | ||

| 2014 | POSCO pre-emptive rights | $1.2 million | ||

| 2014/15 | Aspen/XGS II | $10 million + $1 million lease | ||

| 2015 | Series B | $4.3 million | ||

| 2016 | Dow Chemical | $10 million senior credit facility | ||

| 2016-2019 | Public Offering | $21 million (including $3 million from Soulbrain) |

8

Our Competitive Strengths

We believe that we are a leader in the emerging global market for graphene nanoplatelets. The following competitive strengths distinguish us in our industry:

Our know-how and ability to tailor our products for use in multiple applications. Many of our products and product-development activities target use of our xGnP® graphene nanoplatelets in various matrices to form composite products that are then used by our customers. We have extensive knowledge of how to tailor our products to deliver performance as composite products in various applications and we also have knowledge of how to tailor other components of a composite to adjust the performance of the composite for use in various applications. We also have knowledge of how to tailor our products for a range of other end-use markets and applications that may include: 3-D printing, anti-corrosive coatings, automotive coatings, thermally conductive adhesives, thermal interface materials/compounds, tires, thermal coatings and sporting goods equipment.

The strength of our intellectual property. Because of our focus on manufacturing process development, we believe we have one of the world’s strongest internal knowledge bases in graphene nanoplatelet manufacturing, with most of our proprietary knowledge maintained as trade secrets to avoid the disclosures required by patenting. The thirty-three (33) U.S. patents and patent applications that we are currently managing (including those under license from MSU and Metna) and thirty-seven (37) international patents and patent applications add value by protecting specific equipment, or high-value end-user product applications. The fact that two global companies have evaluated and licensed certain aspects of our production technology provides independent evidence of our technology’s effectiveness.

The breadth of our product offering. To our knowledge, we have the broadest product offering in our industry. In addition to offering four standard grades of bulk graphene nanoplatelet materials in a range of diameters and surface areas, we offer three standard ink formulations, resistive heating formulations and optional custom dispersions and formulations of our bulk materials. We also offer an XG TIM® thermal interface material and a GNP® Cement Additive product. We also offer polymer resins containing various forms of our xGnP®graphene nanoplatelets and in varying concentration and including polyurethane (XGPU), polypropylene (XGPP), polyethylene terephthalate (XGPET), vinyl ester (XGVE), polyetherimide (XGPEI) and high-density polyethylene (XGHDPE). Other polymers may be added over time depending on the end-market and customer needs.

The low-cost nature of our manufacturing processes. We believe our manufacturing processes are among the lowest-cost approaches to the manufacturing graphene nanoplatelets (subject to economies of scale) based on our internal modelling of competitive processes as well as our analysis of alternative technologies.

Our corporate partners. Four global corporations (Samsung, POSCO, Soulbrain and Hanwha Chemical) have invested over $14 million in XGS, giving us a significant global reach as well as the ability to leverage the assets of our partners. In addition, The Dow Chemical Company, or Dow, has extended $10 million in senior debt financing, of which we have drawn down $9 million as of December 31, 2019.

Our licensees should accelerate our entry into large markets. Cabot Corporation, the largest U.S.-based manufacturer of carbon particles, and POSCO, one of the world’s largest steel producers, have licensed parts of our production technology. We believe these licensees will help us distribute our products and value-added products made with our xGnP®nanoplatelets more rapidly than we could do on our own.

The number of development partners that are working with our materials. As of December 31, 2019, we had supplied materials to 303 universities or government laboratories in 41 different countries around the world. We also supply our products to a number of other organizations for the purposes of commercial design and manufacture. These other organizations include 3M, Amazon, BASF, Callaway Golf, Dow Chemical, Ford Motor Company, LG Chem, Michelin, Niagara Bottling, PPG, Raytheon, Samsung, Sherwin-Williams and The Boeing Company.

The number of commercial customers purchasing and working with our materials. As of December 31, 2019, we have supplied materials to 1,237 commercial companies around the world (in addition to universities and research laboratories) who are assessing their performance and potentially designing them into products. We have more than 75 active development relationships where we are working with end-use customers to design products for commercial use. We believe that these relationships will continue to expand.

As a result of these factors, we believe XG Sciences is a leader in the emerging global market for graphene nanoplatelets. Other independent observers have agreed with this assessment. For example, Lux Research, in a January 2019 summary stated “XG Sciences, while still in the red, now has a clear path to profitability; it is a leader in high quality graphene, and clients looking to develop novel graphene-containing products should consider it as a partner.”

Self-Underwritten Offering

We filed a Registration Statement on Form S-1 (File No. 333-209131) with the SEC on April 11, 2016 which was declared effective by the SEC on April 13, 2016 (as amended, the “Registration Statement”). The Registration Statement registered up to 3,000,000 shares of common stock at a fixed price of $8.00 per share to the general public in a self-underwritten offering (the “Offering” or our “IPO”). Post-Effective Amendment No. 1 to the Registration Statement was declared effective August 26, 2016, Post-Effective Amendment No. 2 was declared effective August 31, 2016, Post-Effective Amendment No. 3 was declared effective January 17, 2017, and Post-Effective Amendments No. 4 and No. 5 were dated April 12, 2017 and were declared effective April 14, 2017. Post-Effective Amendment No. 6 was declared effective June 26, 2018. The Offering terminated upon expiration of the Registration Statement on April 12, 2019. Although we have sold shares of our common stock in our IPO pursuant to an effective Registration Statement, we have not yet listed any of our capital stock for trading or quotation on any exchanges or the over-the-counter bulletin board.

9

As of December 31, 2019, the Company sold 2,615,425 shares under the Registration Statement at a price of $8.00 per share for proceeds of $20,923,400.

Pursuant to the Certificate of Designation for our Series A Preferred Stock, as amended (“Series A Stock”), and our Series B Preferred Stock, as amended (“Series B Stock”), all then-outstanding shares of Series A Stock and Series B Stock will automatically convert into shares of common stock upon (i) the listing of the Company’s common stock on a Qualified National Exchange (a securities exchange registered with the SEC under Section 6(a) of the Securities Exchange Act of 1934, as amended “Exchange Act”), such as the NASDAQ Capital Market or the New York Stock Exchange, or (ii) the quotation of our common stock on the OTCQB or OTCQX marketplaces operated by OTC Markets Group, Inc. (“OTC Markets”), and the act of achieving such listing or quotation is referred to hereafter as a “Public Listing” in this report. As a result, there will only be one class of equity securities outstanding — common stock — after we achieve a Public Listing, because there will be no other series of preferred stock issued and outstanding at such time. Prior to any such listing, the Series A Stock and Series B Stock may be voluntarily converted into shares of common stock at the then-current conversion rate for each series of Preferred Stock (current rate is 1.875 shares of common stock for 1 share of Series A Stock and 1 share of common stock for 1 share of Series B Stock). While there are no definitive plans to do a Public Listing as of the date of this report, the Company targets achieving a Public Listing in the next 24 months, market conditions permitting.

Public Listing

In order to achieve a Public Listing, we will have to meet certain initial listing qualifications of the Qualified National Exchange or the OTC Markets on which we are seeking the Public Listing. In addition, we will need to have market makers agree to make a market in our common stock and file a FINRA Form 15c211 with the SEC on our behalf before we can achieve a Public Listing, and we will also need to remain current in our quarterly and annual filings with the SEC. Although we intend to seek a Public Listing, we cannot make any assurances that our common stock will ever be quoted or traded on a Qualified National Exchange or the OTC Markets or that any market for our common stock will develop.

Employees

As of December 31, 2019, we had 39 full-time employees and 2 part-time employees. 3 of these employees were contract employees who may generally be hired as permanent employees after 3 – 6 months. Employees include the following four senior managers that report to the CEO: Chief Financial Officer, Chief Commercial Officer, Vice President of Operations and Chief Technologist. The Company employs a total of 7 full-time scientists and technicians in its R&D group, including the Chief Technologist.

Corporate Information

XG Sciences, Inc. was incorporated on May 23, 2006 in the State of Michigan and is organized as a “C” corporation under the applicable laws of the United States and State of Michigan. We do not currently have any affiliated companies or joint venture partners, and we have one wholly owned subsidiary called XG Sciences IP, LLC. This subsidiary was created in 2014 for the purpose of holding our intellectual property. Our headquarters and principal executive offices are located at 3101 Grand Oak Drive, Lansing, Michigan, 48911 and our telephone number is (517) 703-1110. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to section 13(a) or 15(d) of the Exchange Act are available free of charge through our website as soon as reasonably practicable after we electronically file with or furnish them to the SEC, and are available in print to any stockholder who requests a copy.

Our website address ishttp://www.xgsciences.com, although the information contained in, or that can be accessed through, our website is not part of this filing. You may also contact Dr. Philip Rose, our Chief Executive Officer via email atp.rose@xgsciences.com. Additionally, the SEC maintains a website that contains reports, proxy statements, information statements and other information regarding issuers, including us, that file electronically with the SEC at www.sec.gov.

10

Risks Relating to Our Business and Industry

We will need to raise substantial additional capital in the future to fund our operations and we may be unable to raise such funds when needed and on acceptable terms, which could have a materially adverse effect on our business.

Developing, manufacturing and selling nanomaterials in commercially-viable quantities requires substantial funding. As of December 31, 2019, we had cash, cash equivalents and restricted cash on hand of $1,129,702. We believe our cash is sufficient to fund our operations for the next twelve months (through April 2021) when taking into account various sources of funding and cash received from continued commercial sales transactions. We intend that the primary means for raising funds will be through equity offerings that may include: private placement with one or more strategic investors, offering of shares of common stock to the public through a self-underwritten offering or through an underwritten offering with a bank in parallel with a listing on a Qualified National Exchange. There can be no assurance that we will be able to raise additional equity capital in subsequent equity offerings or that the terms and conditions of any future financings will be workable or acceptable to us and our stockholders. Our continuation as a going concern is dependent upon continued financial support from our shareholders, our ability to obtain necessary equity and/or debt financing to continue operations, and the attainment of profitable operations. In the event that we are not able to raise substantial additional funds in the future with terms that are acceptable, or adjust our business model accordingly, we may be forced to curtail or cease operations and investors could lose all or a significant part of their investment, or we could be prevented from making our periodic filings under the Exchange Act.

A pandemic, epidemic or outbreak of an infectious disease in the markets in which we operate or that otherwise impacts our facilities or suppliers could adversely impact our business.

We expect that a pandemic, epidemic, or outbreak of an infectious disease including the recent outbreak of respiratory illness caused by the novel COVID-19 virus first identified in Wuhan, Hubei Province, China (“COVID-19) will continue to affect our markets, facilities, customers and employees, and our business could continue to be adversely affected in the future. Consequences of the coronavirus outbreak are resulting in disruptions in or restrictions on our ability to travel and the ability of manufacturers, including many of our customers, to maintain normal operations. If such an infectious disease broke out at our facilities, or if, due to governmental or other restrictions, our facilities are unable to operate for an extended period of time, our operations may be affected significantly, our productivity may be affected, our ability to complete projects in accordance with our contractual obligations may be affected, and our ability to manufacture and sell our graphene nanoplatelets may be hindered. If the suppliers that we rely on for raw materials and other supplies to conduct operations are affected by COVID-19, we may not be able to fill orders that are received or our cost of sales may increase, and our financial position may suffer. If our customers are affected by COVID-19, orders for our products may be delayed or cancelled, and our financial position may suffer. Further, infectious outbreak may continue to cause disruption to the U.S. economy, or the economies of the markets in which we operate such as China and South Korea, and cause shortages of materials, labor and transportation which could affect our customers’ ability to produce finished products utilizing our graphene nanoplatelets, affect production capacity and business confidence, or cause economic changes that we cannot anticipate. Overall, the potential impact of a pandemic, epidemic or outbreak of an infectious disease with respect to our markets or our facilities is difficult to predict and could continue to adversely impact our business for an indefinite period of time. In response to the COVID-19 situation, federal, state and local governments (or other governments or bodies in markets in which we operate) have placed restrictions on travel and conducting or operating business activities. At this time, those restrictions are very fluid and evolving, and when such restrictions will be lifted is unknown. We have been and will continue to be impacted by those restrictions. Given that the type, degree and length of such restrictions are not known at this time, we cannot predict the overall impact of such restrictions on us, our customers, our employees, our supply and distribution chains, others that we work with or the overall economic environment. As such, the impact these restrictions may have on our financial position, operating results and liquidity cannot be reasonably estimated at this time, but we expect the impact to be material. In addition, due to the speed with which the COVID-19 situation is developing and evolving, there is uncertainty around its ultimate impact on public health, business operations and the overall economy; therefore, the negative impact on our financial position, operating results and liquidity cannot be reasonably estimated at this time, but we expect the impact to be material.

We could be adversely affected by our exposure to customer concentration risk.

We are subject to customer concentration risk as a result of our reliance on relatively few customers for a significant portion of our revenues. We had 1 customer whose purchases accounted for 41% and 72% of revenue in the twelve months ended December 31, 2019 and 2018, respectively. In 2019, we had 4 customers whose purchases accounted for 79% of revenue. Due to the nature of our business and the relatively large size of many of the applications our customers are developing, we anticipate that we will be dependent on a relatively small number of customers for the majority of our revenues for the next few years, and if one or more of these customers does not place orders, there would be a risk of significant loss of future revenues, which could in turn have a material adverse effect on our business and on your investment.

11

Downturns in general economic conditions could adversely affect our profitability.

Downturns in general economic conditions such as the economic conditions that have coincided with COVID 19 can cause fluctuations in demand for our products, product prices, volumes and gross margins. Future economic conditions may not be favorable to our industry. A decline in the demand for our products or a shift to lower-margin products due to deteriorating economic conditions could adversely affect sales of our products and our profitability and could also result in impairments of certain of our assets.

Furthermore, any uncertainty in economic conditions may result in a slowdown to the global economy that could affect our business by reducing the prices that our customers may be able or willing to pay for our products or by reducing the demand for our products. Due to our customer concentration risk, the loss of one or more of our large customers could significantly affect our business, operating results and financial condition.

If we are unable to continue as a going concern, our securities will have little or no value.

The report of our independent registered public accounting firm that accompanies our consolidated financial statements for the year ended December 31, 2019 contains a going concern qualification in which such firm expressed substantial doubt about our ability to continue as a going concern. We currently anticipate that our cash and cash equivalents will be sufficient to fund our operations through April 2021, without raising additional capital. We believe that we will need to raise approximately $500,000 to $1,000,000 of additional capital in order to continue our operations for the next twelve months in a minimal to no revenue growth environment. Our continuation as a going concern is dependent upon continued financial support from our shareholders, our ability to obtain necessary equity and/or debt financing to continue operations, and growth in revenue from operations. These factors raise substantial doubt regarding our ability to continue as a going concern. We cannot make any assurances that additional financings will be available to us and, if available, completed on a timely basis, on acceptable terms or at all. If we are unable to complete an equity or debt offering, or otherwise obtain sufficient financing when and if needed, it would negatively impact our business and operations. It could also lead to the reduction or suspension of our operations and ultimately force us to cease our operations.

We have a limited operating history, an accumulated deficit and a stockholders’ deficit, making it difficult for you to evaluate our business and your investment.

XG Sciences, Inc. was incorporated on May 23, 2006, and is an advanced materials company. We sell bulk nanomaterials or products made with these materials to other companies for incorporation into their products. To date, there has been limited incorporation of our materials or products into customer products that are released for commercial sale. Because there is a limited demonstrated history of commercial success for our products, it is difficult to evaluate whether our products will ultimately be successful in the market. It is possible that larger and or extended commercial success may never happen and that we will never achieve the level of revenues necessary to sustain our business or continue to attract additional financing.

Many of our products represent new products that have not yet been fully developed and for which manufacturing operations have not yet been fully scaled. This means that investors are subject to all of the risks incident to the creation and development of multiple new products and their associated manufacturing processes.

As of December 31, 2019, and December 31, 2018, we have an accumulated deficit from operations of $(65,581,128) and $(55,687,160), respectively. As of December 31, 2019, and December 31, 2018, our total stockholder’s equity was $(2,146,797) and $4,990,719, respectively. The deficit reflects net losses in each period since our inception incurred through development of nanomaterials without the presence of large-scale adoption to generate substantial revenues to cover development costs and generate a profit. We have never paid a dividend. Also, since inception, we have not generated sufficient revenues to cover our fixed expenses or sustain our business in any financial reporting period. Nor have we demonstrated the capability to produce sufficient materials to generate the ongoing revenues necessary to sustain our operations in the long-term. There can be no assurance that we will ever produce a profit.

Because we are subject to these uncertainties, there may be risks that management has failed to anticipate and you may have a difficult time evaluating our business and your investment in our Company. Our ability to become profitable depends primarily on our ability to successfully commercialize our products in the future. Even if we successfully develop and market our products, we may not generate sufficient or sustainable revenue to achieve or sustain profitability, which could cause us to cease or curtail operations. In such case, you would likely lose all or a significant part of your investments.

We have limited experience in the higher volume manufacturing that will be required to support profitable operations, and the risks associated with scaling to larger production quantities may be substantial.

We have limited experience manufacturing our products. We have established initial commercial or pilot-scale production facilities for our bulk powders and certain integrated products. In order to develop the capacity to produce much higher volumes, it will be necessary to produce multiples of existing processes or engineer new production processes in some cases.

We have completed the initial phases of building out our 64,000 square foot manufacturing facility in Mason, MI, but there can be no assurance that this new facility will continue to be expanded in the future on time or as planned. In addition, due to recent events surrounding our business and the COVID-19 pandemic, in March of 2020, we restructured our organization by reducing headcount by 45%, by furloughing substantially all manufacturing employees and by implementing temporary salary reductions ranging from 15-20% which has resulted in a 58% reduction in annual payroll and related costs. In April 2020, we furloughed additional employees in our R&D and Engineering departments. We expect that these actions could have a material impact on our ability to scale up our production processes, and there is no guarantee that we will be able to economically scale-up our production processes to the levels required. If we are unable to scale-up our production processes and facilities to support sustainable sales levels, the Company may be forced to curtail or cease operations and investors could lose all or a significant part of their investment.

12

Projection of fixed monthly expenses and operating losses for the near future means that investors may not earn a return on their investment or may lose their investment.

Because of the nature of our business, we project considerable fixed expenses that will lead to projected monthly deficits for the near future. Fixed manufacturing expenses to maintain production facilities, compensation expenses for scientists and other critical personnel, and ongoing rent and utilities amount to several hundred thousand dollars per month, and we believe that such expenses are required as a precursor to significant customer sales. However, there can be no assurance that monthly sales will ever reach a sufficient level to cover the cost of ongoing monthly expenses and if they do, are maintained for a sustainable period of time. If sufficient regular monthly sales are not generated to cover these fixed expenses, we will continue to experience monthly cash flow deficits which, if not eliminated, will require continuing new investment in the Company. If monthly cash flow deficits continue beyond levels that investors find tolerable, we may not be able to raise additional funds and may be forced to curtail or cease operations and investors could lose all or a significant part of their investment.

We have a long and complex sales cycle and have not demonstrated the ability to operate successfully in this environment.

It has been our experience since our inception that the average sales cycle for our products can range from one to seven years from the time a customer begins testing our products until the time that they could be successfully used in a commercial product. The product introduction timing will vary based on the target market, with automotive uses typically being toward the long end and consumer products toward the shorter end. We have a limited track record of success in completing customer development projects, which makes it difficult for investors to fully evaluate the likelihood of our future success. The sales and development cycle for our products is subject to customer budgetary constraints, internal acceptance procedures, competitive product assessments, scientific and development resource allocations, and other factors beyond our control. If we are not able to successfully accommodate these factors to enable customer development success, we will be unable to achieve sufficient sales to reach profitability. In this case, we may not be able to raise additional funds and may be forced to curtail or cease operations and investors could lose all or a significant part of their investment.

Our revenues often fluctuate significantly based on one-off orders from customers or from the recognition of non-product revenues which vary from period-to-period, which may materially impact our financial results from period to period.

Because of the potential for large revenue swings from one-time, large orders or grants (or other such non-product revenue), it may be difficult to accurately forecast the needs for inventory, working capital, and other financial resources from period-to-period. Such orders would require a significant short-term increase in our production capacity and would require the financial resources to add staff and support the associated working capital. If such large, one-time orders were not handled smoothly, customer confidence in us as a viable supplier could be reduced and we might not succeed in capturing the additional larger orders that may be reflected in our business plan.

We operate in an advanced technology arena where hypothesized properties and benefits of our products may not be achieved in practice, or in which technological change may alter the attractiveness of our products.

Because there is only limited sustained history of successful use of our products in commercial applications, there is no assurance that broad successful commercial applications may be broadly technically feasible. Many of the scientific and engineering data related to our products has been generated in our own laboratories or in laboratory environments at our customers or third-parties, like universities and national laboratories. It is well known that laboratory data is not always representative of commercial applications.

Likewise, we operate in a market that is subject to rapid technological change. Part of our business strategy is to monitor such change and take steps to remain technologically current, but there is no assurance that such strategy will be successful. If we are not able to adapt to new advances in materials sciences, or if unforeseen technologies or materials emerge that are not compatible with our products and services or that could replace our products and services, our revenues and business prospects would likely be adversely affected. Such an occurrence may have severe consequences, including the potential for our investors to lose all or a significant part of their investment.

13

Competitors that are larger and better funded may cause us to be unsuccessful in selling our products.

We operate in a market in which there are competitors. Global research is being conducted by substantially larger companies who have greater financial, personnel, technical, and marketing resources. There can be no assurance that our strategy of offering better materials based on our proprietary graphene nanoplatelets will be able to compete with other companies, many of whom will have significantly greater resources, on a continuing basis. In the event that we cannot compete successfully, we may be forced to cease or curtail operations and investors may lose all or a significant part of their investment.

We are dependent on key employees.

Our operations and product development are dependent upon the experience and knowledge of Philip Rose, our Chief Executive Officer. If he was to resign or be terminated, our business would be adversely affected in the short term, and his departure could disrupt the business enough to endanger your investment. We also depend on Jacqueline Lemke, Chief Financial Officer, Dr. Leroy Magwood, Chief Technologist, and Scott Murray, Vice President of Operations. If the services of any of these individuals should become unavailable, our business operations might be adversely affected. We hold “Key Person” insurance of $5 million on our CEO, Philip Rose, but do not hold any other “Key Person” insurance, and, if several of these individuals became unavailable at the same time, our ability to continue normal business operations might be adversely affected, to the extent that revenue or profits could be diminished and you could lose all or a significant part of your investment.

Our success depends in part on our ability to protect our intellectual property rights, and our inability to enforce these rights could have a material adverse effect on our competitive position.

We rely on the patent, trademark, copyright and trade-secret laws of the United States and the countries where we do business to protect our intellectual property rights. We may be unable to prevent third parties from using our intellectual property without our authorization. The unauthorized use of our intellectual property could reduce any competitive advantage we have developed, reduce our market share or otherwise harm our business. In the event of unauthorized use of our intellectual property, litigation to protect or enforce our rights could be costly, and we may not prevail.

Many of our technologies are not covered by any patent or patent application, and our issued and pending U.S. and non-U.S. patents may not provide us with any competitive advantage and could be challenged by third parties. Our inability to secure issuance of our pending patent applications may limit our ability to protect the intellectual property rights these pending patent applications were intended to cover. Our competitors may attempt to design around our patents to avoid liability for infringement and, if successful, our competitors could adversely affect our market share. Furthermore, the expiration of our patents may lead to increased competition.

Our pending trademark applications may not be approved by the responsible governmental authorities and, even if these trademark applications are granted, third parties may seek to oppose or otherwise challenge these trademark applications. A failure to obtain trademark registrations in the United States and in other countries could limit our ability to protect our products and their associated trademarks and impede our marketing efforts in those jurisdictions.

In addition, effective patent, trademark, copyright and trade secret protection may be unavailable or limited in some foreign countries. In some countries, we do not apply for patent, trademark or copyright protection. We also rely on unpatented proprietary manufacturing expertise, continuing technological innovation and other trade secrets to develop and maintain our competitive position. Although we enter into confidentiality agreements with our employees and generally with third parties to protect our intellectual property, these confidentiality agreements are limited in duration and could be breached and may not provide meaningful protection of our trade secrets or proprietary manufacturing expertise. Adequate remedies may not be available if there is an unauthorized use or disclosure of our trade secrets and manufacturing expertise. In addition, others may obtain knowledge about our trade secrets through independent development or by legal means. The failure to protect our processes, apparatuses, technology, trade secrets and proprietary manufacturing expertise, methods and compounds could have a material adverse effect on our business by jeopardizing critical intellectual property.

Where a product formulation or process is kept as a trade secret, third parties may independently develop or invent and patent products or processes identical to our trade-secret products or processes. This could have an adverse impact on our ability to make and sell products or use such processes and could potentially result in costly litigation in which we might not prevail.

We could face intellectual property infringement claims that could result in significant legal costs and damages and impede our ability to produce key products, which could have a material adverse effect on our business, financial condition and results of operations.

14

If we are unable to implement and maintain effective internal control over financial reporting, our stock could be less attractive to potential investors.

We are required to establish and maintain appropriate internal controls over financial reporting, subject to exemptions that we avail ourselves of under the JOBS Act discussed below. Failure to establish such controls, or any failure of such controls once established, could adversely impact our public disclosures regarding our business, financial condition or results of operations. Any failure of our controls could also prevent us from maintaining accurate accounting records and discovering accounting errors and financial frauds. Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require annual assessment of our internal control over financial reporting, and the standards that must be met for management to assess the internal control over financial reporting as effective are new and complex, and require significant documentation, testing and possible remediation to meet the detailed standards. In November 2018, the Company hired a CFO to oversee the finance and reporting function, modify processes to mitigate segregation of duties issues and increase supervisory and review controls.

In addition, management’s assessment of internal controls over financial reporting may identify material weaknesses and conditions that need to be addressed in our internal controls over financial reporting or other matters that may raise concerns for investors in the future. Any actual or perceived weaknesses and conditions that need to be addressed in our internal control over financial reporting, disclosure of management’s assessment of our internal controls over financial reporting, or at such time as we are no longer subject to exemptions under the JOBS Act, disclosure of our independent registered public accounting firm’s report on management’s assessment of our internal controls over financial reporting, may have an adverse impact on our ability to sell our common stock.

Future adverse regulations could affect the viability of the business.

Our bulk products have been approved for sale in the United States by the U.S. Environmental Protection Agency after a detailed review of our products and production processes. In most cases, as far as we are aware, there are no current regulations elsewhere in the world that prevent or prohibit the sale of our products. Nevertheless, the sale of nano-materials is a subject of regulatory discussion and review in many countries around the world. In some cases, there is a discussion of potential testing requirements for toxicity or other health effects of nano-materials before they can be sold in certain jurisdictions. If such regulations are enacted in the future, our business could be adversely affected because of the requirement for expensive and time-consuming tests or other regulatory compliance. If our nano-materials are found to be toxic, such finding could have a material impact on our business and on the production and sale of our products. There can be no assurance that future regulations might not severely limit or even prevent the sale of our products in major markets, in which case our financial prospects might be severely limited, causing investors to lose all or a significant part of their investment.

Compliance with changing regulation of corporate governance and public disclosure will result in additional expenses and will divert time and attention away from revenue generating activities.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002 and related SEC regulations, have significantly increased the costs and risks associated with accessing the public markets and public reporting. Our management team will need to invest significant management time and financial resources to comply with both existing and evolving standards for public companies, which will lead to increased general and administrative expenses and a diversion of management time and attention from revenue generating activities to compliance activities, which could have an adverse effect on our business.

Given our limited resources, we may not effectively manage our growth.

There is no guarantee that we have the resources, financial or operational, required to manage our growth. This is particularly true as we expand facilities and manufacture our products on a greater commercial scale. Furthermore, rapid growth in our operations may place a significant strain on our management, administrative, operational and financial infrastructure. The inability to adequately manage our growth could have a material and adverse effect on our business, financial condition or results of operations, thus resulting in a lower quoted price of our common stock.

15

An increase in the cost of raw materials or electricity might affect our profits.

Any increase in the prices of our raw materials or energy might affect the overall cost of our products. If we are not able to raise our prices to pass on increased costs to our customers, we would be unable to maintain our existing profit margins. Our major cost components include items such as graphite, acids and bases, and electricity, which items are normally readily available industrial commodities. During our history as a business, we have not seen any material impact (as defined by GAAP) on our cost structure from fluctuations in raw material or energy costs, but this could change in the future, especially given the impact of COVID-19 and its impact on the global economy.

Our results of operations could deteriorate if our manufacturing operations were substantially disrupted for an extended period.

In addition to the disruptions to our manufacturing operations caused by COVID-19, our manufacturing operations are subject to disruption due to extreme weather conditions, floods and similar events, major industrial accidents, strikes and lockouts, adoption of new laws or regulations, changes in interpretations of existing laws or regulations or changes in governmental enforcement policies, civil disruption, riots, terrorist attacks, war, and other events. We cannot assure you that no such events will occur. If such an event occurs, it could have a material adverse effect on us.

Some health effects of nanotechnology are unknown.