Exhibit 99.1

Q3 2021 Letter to Shareholders

Key Highlights from Q3 200 $162M Continued Strong Growth Total Generated Premium 150 ‹ 94% growth in Total Generated Premium 100 $83M $56M ‹ Raising TGP annual guidance to +94% 50 $600-605m YoY 0 Q3 ‘19 Q3 ‘20 Q3 ‘21 ‹ $553m in Total Generated Premium in-Force; $52m increase QoQ 100 87% 89% Premium 81% Retention1 80 60 Improved Loss Ratio 40 ‹ 27pp YoY improvement +2pp 20 in Texas and California Gross Loss Ratio YoY 0 Q3 ‘19 Q3 ‘20 Q3 ‘21 ‹ 5pp YoY improvement in Attritional Loss Ratio 25 $21M Revenue ‹ Continued geographical diversification 20 15 $13M with 63% of new Hippo premium $11M outside of TX/CA 10 +64% 5 YoY 0 Combining Differentiated Q3 ‘19 Q3 ‘20 Q3 ‘21 Technology with Innovative Gross 200 Distribution Channels 155% Loss Ratio 150 128% ‹ Launching a new partnership with 100 PennyMac, accessing millions of incremental homeowners -27pp 50 n/a ‹ Differentiated technology allowing us YoY 0 Q3 ‘19 Q3 ‘20 Q3 ‘21 to quote millions of customers within days via APIs, unlocking national 80 68% scale partners Attritional 70 63% Loss Ratio2 60 ‹ Enabling our multi-carrier strategy by 50 dynamically assigning customers to 40 30 their optimal rate plan -5pp 20 10 n/a YoY 0 Q3 ‘19 Q3 ‘20 Q3 ‘21 Letter to Shareholders | Q3 2021 2

Delivering On Our Promise Dear Shareholders, Q3 was an incredibly strong quarter for Hippo. Our results demonstrate exciting progress in the areas of our business that matter most. We delivered robust growth, improved our loss ratio, and made a number of investments which will strengthen our foundation for the future. Total Generated Premium grew 94% year over year. Premium retention increased to 89%. And customer satisfaction remained among the best in class. We are now more convinced than ever that partnering with our customers to proactively protect their homes and prevent losses is setting a new standard for the industry and is positioning Hippo for long-term success. Our omni-channel distribution strategy continues to deliver. In addition to the strong results in our direct, independent agent, and builder channels, we launched a major new partnership with national home lender PennyMac, giving us the opportunity to offer quotes to millions of additional homeowners. Reflecting our strong performance in Q3 and our expectations of continued momentum in Q4, we are raising our full year guidance for Total Generated Premium from the $560 to $570 million we shared last quarter, to $600 to $605 million. We also delivered an improved loss ratio during the quarter, coming in at 128% vs. 155% a year ago. While we are pleased by the progress, we still have work to do to reach our long-term targets. Later in this letter we are describing how we are using our proprietary technology to learn and implement change at an accelerated pace to continue our momentum in this area. Another advantage that we now have is a world-class insurance leadership team. In recent months, we have welcomed new leaders of our actuarial, underwriting, and risk functions, and announced the future addition of a new leader for our claims organization. This team brings many decades of experience at leading insurance companies and sees the power in the technology platform that we’ve built to deliver better insurance results for Hippo. Letter to Shareholders | Q3 2021 3

We are excited by the rapid operational progress we are making under these new leaders. It will take time for the changes we are making to work their way into our reported results, but early signs are positive and we are more confident than ever that we will deliver. In an unpredictable environment impacted by pandemics, climate change, and inflation, we believe that our tech-driven operating agility allows us to act more quickly and decisively than our competitors, and puts us in a better position to win long-term. Assaf Wand Founder & Ceo Letter to Shareholders | Q3 2021 4

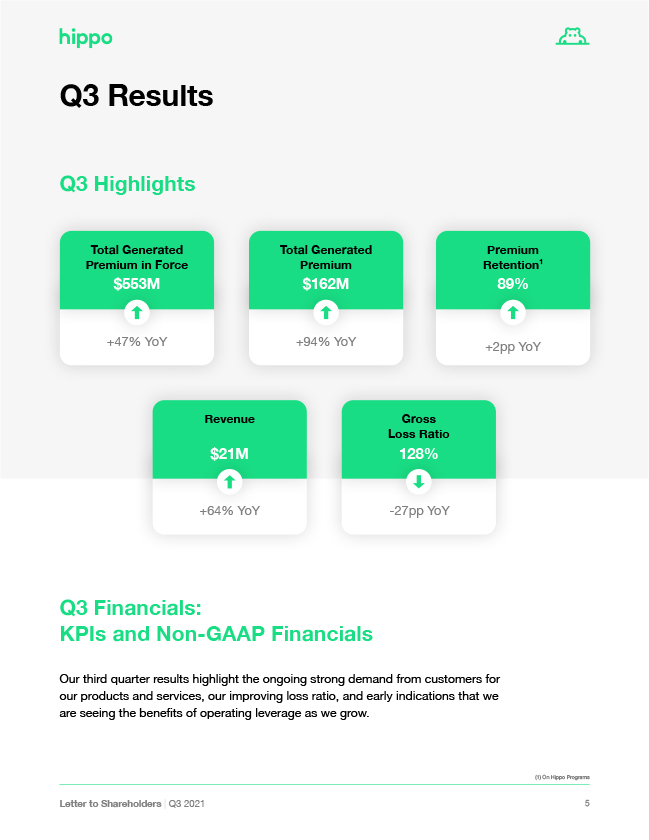

Q3 Results Q3 Highlights Total Generated Premium Revenue Premium Retention1 $162M 89% $21M +64% YoY Gross Loss Attritional Ratio Loss Ratio 128% 63% Q3 Financials: KPIs and Non-GAAP Financials Our third quarter results highlight the ongoing strong demand from customers for our products and services, our improving loss ratio, and early indications that we are seeing the benefits of operating leverage as we grow. (1) On Hippo Programs Letter to Shareholders | Q3 2021 5

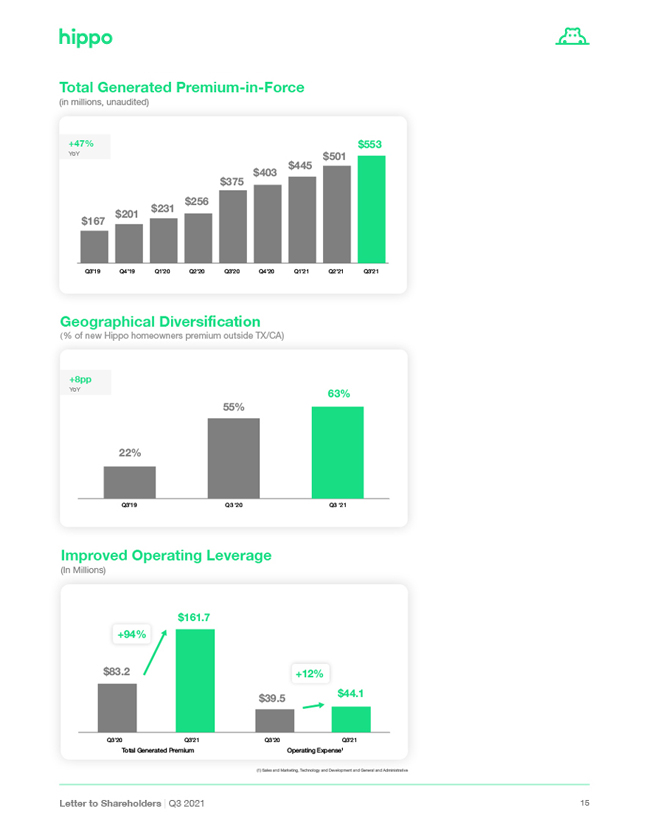

Total Generated Premium Up 94%, Revenue Up 64% Total Generated Premium, or TGP, was up 94% year over year to $162m in Q3. Pro-forma for the acquisition of Spinnaker, TGP was up 51% year over year. Additions to our book of business, or “new” total generated premium were up 66% year over year (on a proforma basis) to $75m, which is an acceleration from 53% last quarter. We continue to geographically diversify. Led by growth in Colorado and New Jersey, 63% of new Hippo homeowners premium in the quarter came from states outside of Texas and California, up from 55% last quarter. As our business grows nationally, we are continuing to develop a much more balanced portfolio of geographic exposure, which should help reduce the volatility of our loss ratio over time. Revenue was up 64% year over year to $21 million, driven by the growth in Total Generated Premium. Customers Stay With Us Premium retention remained strong and continued to edge upward, reaching 89% in the quarter. Our high retention rates are a driver of top line growth, and because loss frequency declines with customer age, a benefit to improving loss ratio over time. Loss Ratio Improving, But There’s Much Work Ahead As we highlighted last quarter, geographic concentration in homeowners insurance can result in higher loss ratio volatility. While our concentration in north Texas worked against us in the first half of 2021 due to historically bad weather, it benefited us in Q3. The industry was hit hard by the devastation of Hurricane Ida this quarter, but we managed to improve our gross loss ratio to 128%, down from 155% last year. Prior period reserves remained stable with minor favorable development. Digging deeper into the components of loss ratio, catastrophic weather losses contributed 50 percentage points of loss ratio in Q3, versus 75 percentage points a year ago. Our underlying attritional loss ratio was 63%, a five percentage point improvement from a year ago. Letter to Shareholders | Q3 2021 6

We’ve made several enhancements to promote better results. ‹ Leveraging our new carrier relationships as we implement our multi-carrier strategy. Ally filings have been made in 14 states and Incline have been in Massachusetts and North Carolina. These will allow us more flexibility in matching the right price to a customer’s risk ‹ Incorporated 5 new data sources during the quarter and added 50 new variables to our data sets which we expect to introduce in Q4 ‹ Adjusted rates, up and down, including a recently approved 24% increase in California ‹ Enhanced our home inspection processes ‹ Continued to diversify our portfolio geographically. Actions to restrict new business in portions of CA and TX, our two largest states, have been combined with growth in other strategic states Increased Sales and Marketing Efficiency Sales and Marketing increased 27% year over year to $22.4 million and we continue to generate more dollars of new TGP for each dollar of sales and marketing we spend. This trend is giving us increased confidence that our message is resonating with potential customers and as a result, we expect to invest more aggressively in 2022 to build a differentiated and nationally recognized brand in home protection. Continued Investment in Technology and Development Technology and Development increased 46% year over year to $8.3 million as we continue to invest in our platform by integrating new data sources, improving our underwriting model, onboarding new partnerships, expanding into new states, and launching new products. General and Administrative Costs General & Administrative Expenses decreased 17% to $13.4 million, with the increased costs of operating as a public company being more than offset by reductions year over year in stock-based compensation. Letter to Shareholders | Q3 2021 7

Balance Sheet and Cash Position Our cash, cash equivalents and investments at the end of the quarter stood at around $850m, positioning us well for an extended period of growth and investment. During the quarter, our AM Best rating on our insurance company, Spinnaker, was affirmed at A-. Net Loss and Adjusted EBITDA Hippo Net Loss was $30.9 million or $0.08 per share compared to a Net Loss of $38.6 million or $0.44 per share in the prior year quarter with the loss driven by the costs of our ongoing investments in platforms, technology and brand and loss ratio levels running above the targets we expect to achieve. Raising TPG Guidance Looking forward, we remain confident in our ability to execute our growth strategy and believe we will exceed the forecast we shared with you previously. We are increasing our full year guidance for Total Generated Premium from a range of $560 to $570 million to $600-$605 million. Letter to Shareholders | Q3 2021 8

Balance Sheet and Cash Position Our cash, cash equivalents and investments at the end of the quarter stood at around $850m, positioning us well for an extended period of growth and investment. During the quarter, our AM Best rating on our insurance company, Spinnaker, was affirmed at A-. Net Loss and Adjusted EBITDA Hippo Net Loss was $30.9 million or $0.08 per share compared to a Net Loss of $38.6 million or $0.44 per share in the prior year quarter with the loss driven by the costs of our ongoing investments in platforms, technology and brand and loss ratio levels running above the targets we expect to achieve. Raising TPG Guidance Looking forward, we remain confident in our ability to execute our growth strategy and believe we will exceed the forecast we shared with you previously. We are increasing our full year guidance for Total Generated Premium from a range of $560 to $570 million to $600-$605 million. Letter to Shareholders | Q3 2021 8 Appendix

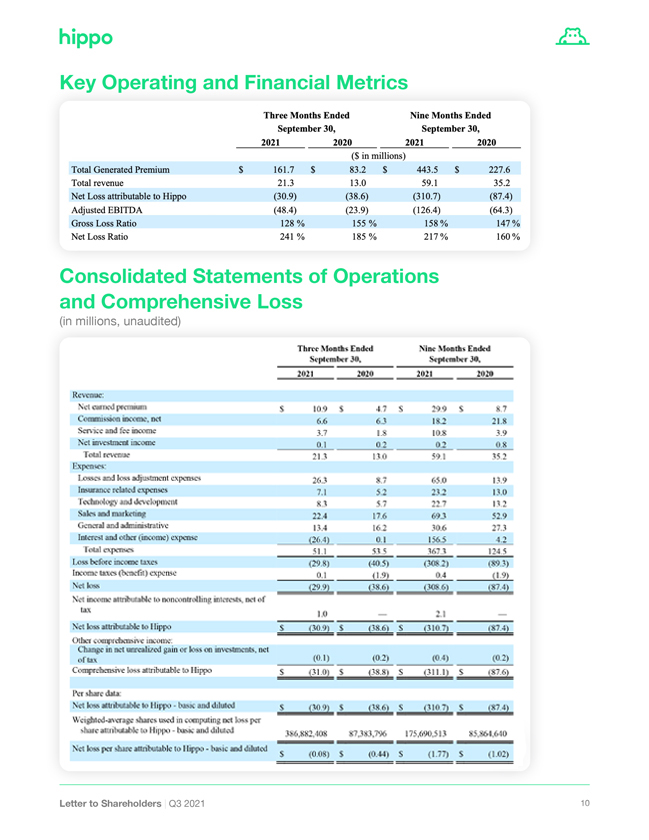

Key Operating and Financial Metrics Three Months Ended Nine Months Ended September 30, September 30, 2021 2020 2021 2020 ($ in millions) Total Generated Premium $ 161.7 $ 83.2 $ 443.5 $ 227.6 Total revenue 21.3 13.0 59.1 35.2 Net Loss attributable to Hippo (30.9) (38.6) (310.7) (87.4) Adjusted EBITDA (48.4) (23.9) (126.4) (64.3) Gross Loss Ratio 128 % 155 % 158 % 147 % Net Loss Ratio 241 % 185 % 217 % 160 % Consolidated Statements of Operations and Compressive Loss (in millions, unaudited) Three Months Ended September 30, Nine Months Ended September 30, 2021 2020 2021 2020 Revenue: Net earned premium $ 10.9 $ 4.7 $ 29.9 $ 8.7 Commission income, net 6.6 6.3 18.2 21.8 Service and fee income 3.7 1.8 10.8 3.9 Net investment income 0.1 0.2 0.2 0.8 Total revenue 21.3 13.0 59.1 35.2 Expenses: Losses and loss adjustment expenses 26.3 8.7 65.0 13.9 Insurance related expenses 7.1 5.2 23.2 13.0 Technology and development 8.3 5.7 22.7 13.2 Sales and marketing 22.4 17.6 69.3 52.9 General and administrative 13.4 16.2 30.6 27.3 Interest and other (income) expense (26.4) 0.1 156.5 4.2 Total expenses 51.1 53.5 367.3 124.5 Loss before income taxes (29.8) (40.5) (308.2) (89.3) Income taxes (benefit) expense 0.1 (1.9) 0.4 (1.9) Net loss (29.9) (38.6) (308.6) (87.4) Net income attributable to noncontrolling interests, net of tax 1.0 — 2.1 — Net loss attributable to Hippo $ (30.9) $ (38.6) $ (310.7) (87.4) Other comprehensive income: Change in net unrealized gain or loss on investments, net of tax (0.1) (0.2) (0.4) (0.2) Comprehensive loss attributable to Hippo $ (31.0) $ (38.8) $ (311.1) $ (87.6) Per share data: Net loss attributable to Hippo—basic and diluted $ (30.9) $ (38.6) $ (310.7) $ (87.4) Weighted-average shares used in computing net loss per share attributable to Hippo—basic and diluted 386,882,408 87,383,796 175,690,513 85,864,640 Net loss per share attributable to Hippo—basic and diluted $ (0.08) $ (0.44) $ (1.77) $ (1.02)

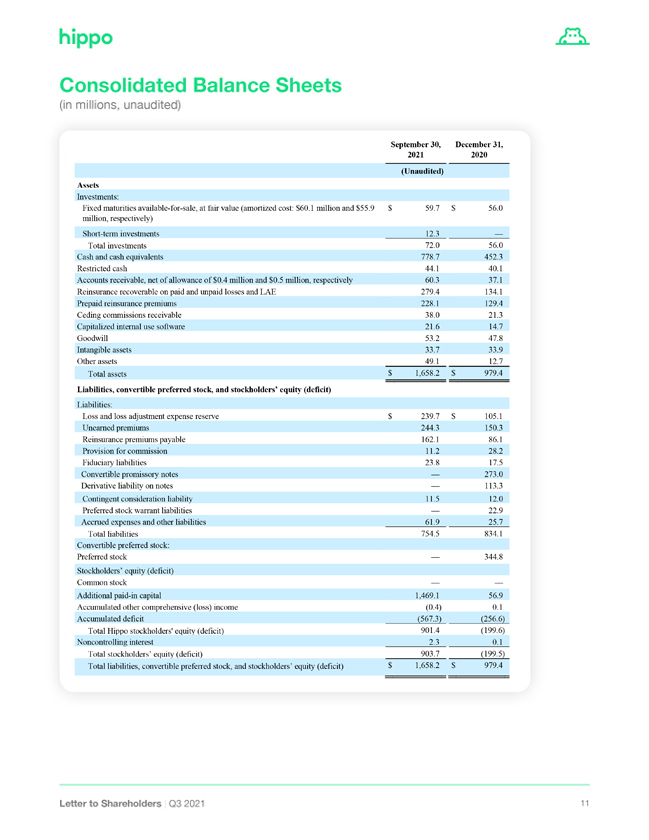

Consolidated Balance Sheets (in millions, unaudited) September 30, 2021 December 31, 2020 (Unaudited) Assets Investments: Fixed maturities available-for-sale, at fair value (amortized cost: $60.1 million and $55.9 million, respectively) $ 59.7 $ 56.0 Short-term investments 12.3 — Total investments 72.0 56.0 Cash and cash equivalents 778.7 452.3 Restricted cash 44.1 40.1 Accounts receivable, net of allowance of $0.4 million and $0.5 million, respectively 60.3 37.1 Reinsurance recoverable on paid and unpaid losses and LAE 279.4 134.1 Prepaid reinsurance premiums 228.1 129.4 Ceding commissions receivable 38.0 21.3 Capitalized internal use software 21.6 14.7 Goodwill 53.2 47.8 Intangible assets 33.7 33.9 Other assets 49.1 12.7 Total assets $ 1,658.2 $ 979.4 Liabilities, convertible preferred stock, and stockholders’ equity (deficit) Liabilities: Loss and loss adjustment expense reserve $ 239.7 $ 105.1 Unearned premiums 244.3 150.3 Reinsurance premiums payable 162.1 86.1 Provision for commission 11.2 28.2 Fiduciary liabilities 23.8 17.5 Convertible promissory notes — 273.0 Derivative liability on notes — 113.3 Contingent consideration liability 11.5 12.0 Preferred stock warrant liabilities — 22.9 Accrued expenses and other liabilities 61.9 25.7 Total liabilities 754.5 834.1 Commitments and contingencies (Note 12) Convertible preferred stock: Preferred stock — 344.8 Stockholders’ equity (deficit) Common stock — — Additional paid-in capital 1,469.1 56.9 Accumulated other comprehensive (loss) income (0.4) 0.1 Accumulated deficit (567.3) (256.6) Total Hippo stockholders’ equity (deficit) 901.4 (199.6) Noncontrolling interest 2.3 0.1 Total stockholders’ equity (deficit) 903.7 (199.5) Total liabilities, convertible preferred stock, and stockholders’ equity (deficit) $ 1,658.2 $ 979.4

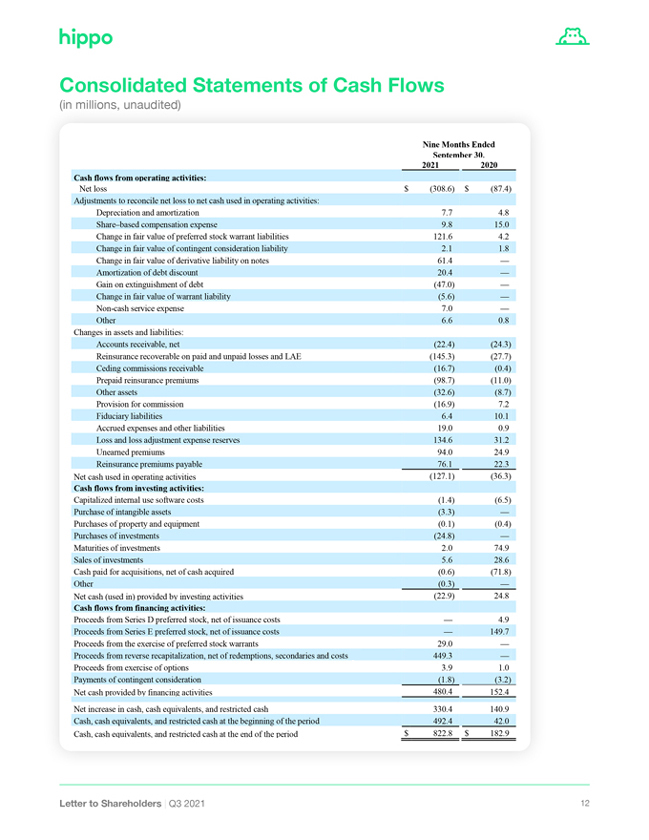

Consolidated Statements of Cash Flows (in millions, unaudited) Nine Months Ended September 30, 2021 2020 Cash flows from operating activities: Net loss $ (308.6) $ (87.4) Adjustments to reconcile net loss to net cash used in operating activities: Depreciation and amortization 7.7 4.8 Share–based compensation expense 9.8 15.0 Change in fair value of preferred stock warrant liabilities 121.6 4.2 Change in fair value of contingent consideration liability 2.1 1.8 Change in fair value of derivative liability on notes 61.4 — Amortization of debt discount 20.4 — Gain on extinguishment of debt (47.0) — Change in fair value of warrant liability (5.6) — Non-cash service expense 7.0 — Other 6.6 0.8 Changes in assets and liabilities: Accounts receivable, net (22.4) (24.3) Reinsurance recoverable on paid and unpaid losses and LAE (145.3) (27.7) Ceding commissions receivable (16.7) (0.4) Prepaid reinsurance premiums (98.7) (11.0) Other assets (32.6) (8.7) Provision for commission (16.9) 7.2 Fiduciary liabilities 6.4 10.1 Accrued expenses and other liabilities 19.0 0.9 Loss and loss adjustment expense reserves 134.6 31.2 Unearned premiums 94.0 24.9 Reinsurance premiums payable 76.1 22.3 Net cash used in operating activities (127.1) (36.3) Cash flows from investing activities: Capitalized internal use software costs (1.4) (6.5) Purchase of intangible assets (3.3) — Purchases of property and equipment (0.1) (0.4) Purchases of investments (24.8) — Maturities of investments 2.0 74.9 Sales of investments 5.6 28.6 Cash paid for acquisitions, net of cash acquired (0.6) (71.8) Other (0.3) — Net cash (used in) provided by investing activities (22.9) 24.8 Cash flows from financing activities: Proceeds from Series D preferred stock, net of issuance costs — 4.9 Proceeds from Series E preferred stock, net of issuance costs — 149.7 Proceeds from the exercise of preferred stock warrants 29.0 — Proceeds from reverse recapitalization, net of redemptions, secondaries and costs 449.3 — Proceeds from exercise of options 3.9 1.0 Payments of contingent consideration (1.8) (3.2) Net cash provided by financing activities 480.4 152.4 Net increase in cash, cash equivalents, and restricted cash 330.4 140.9 Cash, cash equivalents, and restricted cash at the beginning of the period 492.4 42.0 Cash, cash equivalents, and restricted cash at the end of the period $ 822.8 $ 182.9

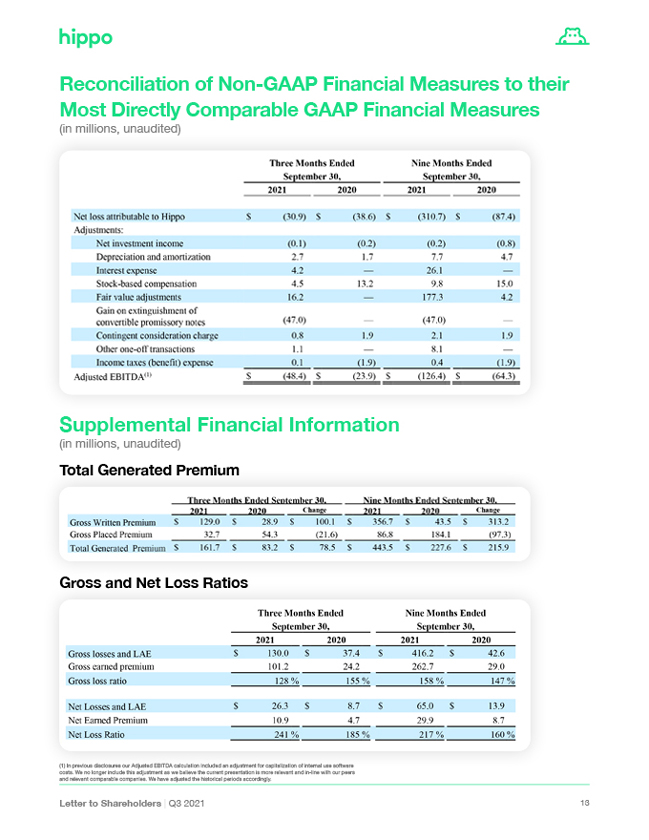

Reconciliation of Non-GAAP Financial Measures to their Most Directly Comparable GAAP Financial Measures (in millions, unaudited) Three Months Ended Nine Months Ended September 30, September 30, 2021 2020 2021 2020 Net loss attributable to Hippo $ (30.9) $ (38.6) $ (310.7) $ (87.4) Adjustments: Net investment income (0.1) (0.2) (0.2) (0.8) Depreciation and amortization 2.7 1.7 7.7 4.7 Interest expense 4.2 — 26.1 — Stock-based compensation 4.5 13.2 9.8 15.0 Fair value adjustments 16.2 — 177.3 4.2 Gain on extinguishment of convertible promissory notes (47.0) — (47.0) — Contingent consideration charge 0.8 1.9 2.1 1.9 Other one-off transactions 1.1 — 8.1 — Income taxes (benefit) expense 0.1 (1.9) 0.4 (1.9) Adjusted EBITDA(1) $ (48.4) $ (23.9) $ (126.4) $ (64.3) (1) In previous disclosures, our Adjusted EBITDA calculation included an adjustment for capitalization of internal use software costs. We no longer include this adjustment, as we believe the current presentation is more relevant and in-line with our peers and relevant comparable companies. We have adjusted the historical periods accordingly. Supplemental Financial Information (in millions, unaudited) Total Generated Premium Three Months Ended September 30, Nine Months Ended September 30, 2021 2020 Change 2021 2020 Change Gross Written Premium $ 129.0 $ 28.9 $ 100.1 $ 356.7 $ 43.5 $ 313.2 Gross Placed Premium 32.7 54.3 (21.6) 86.8 184.1 (97.3) Total Generated Premium $ 161.7 $ 83.2 $ 78.5 $ 443.5 $ 227.6 $ 215.9 Gross and Net Loss Ratios Three Months Ended Nine Months Ended September 30, September 30, 2021 2020 2021 2020 Gross losses and LAE $ 130.0 $ 37.4 $ 416.2 $ 42.6 Gross earned premium 101.2 24.2 262.7 29.0 Gross loss ratio 128 % 155 % 158 % 147 % Net Losses and LAE $ 26.3 $ 8.7 $ 65.0 $ 13.9 Net Earned Premium 10.9 4.7 29.9 8.7 Net Loss Ratio 241 % 185 % 217 % 160 %

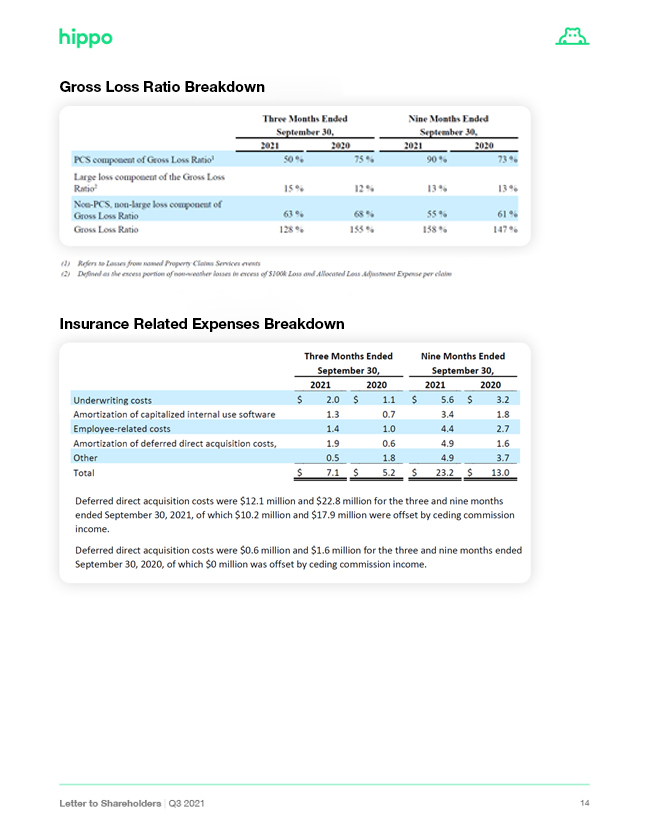

Three Months Ended Nine Months Ended September 30, September 30, 2021 2020 2021 2020 PCS component of Gross Loss Ratio1 50 % 75 % 90 % 73 % Large loss component of the Gross Loss Ratio2 15 % 12 % 13 % 13 % Non-PCS, non-large loss component of Gross Loss Ratio 63 % 68 % 55 % 61 % Gross Loss Ratio 128 % 155 % 158 % 147 % (1) Refers to Losses from named Property Claims Services events (2) Defined as the excess portion of non-weather losses in excess of $100k Loss and Allocated Loss Adjustment Expense per claim Three Months Ended Nine Months Ended September 30, September 30, 2021 2020 2021 2020 Underwriting costs $ 2.0 $ 1.1 $ 5.6 $ 3.2 Amortization of capitalized internal use software 1.3 0.7 3.4 1.8 Employee-related costs 1.4 1.0 4.4 2.7 Amortization of deferred direct acquisition costs, net 1.9 0.6 4.9 1.6 Other 0.5 1.8 4.9 3.7 Total $ 7.1 $ 5.2 $ 23.2 $ 13.0 Deferred direct acquisition costs were $12.1 million and $22.8 million for the three and nine months ended September 30, 2021, of which $10.2 million and $17.9 million were offset by ceding commission income. Deferred direct acquisition costs were $0.6 million and $1.6 million for the three and nine months ended September 30, 2020, of which $0 million was offset by ceding commission income.

Improved Operating Leverage (In Millions) $181.7 +94% $83.2 +12% $39.5 $44.1 0 Q3’20 Q3’21 Q3’20 Q3’21 Total Generated Premium Operating Expense1 (1) Sales and Marketing, Technology and Development and General and Administrative Geographical Diversification +8pp YoY 63% 55% 22% Q3’19 Q3 ‘20 Q3 ‘21 Letter to Shareholders | Q3 2021 15