SCHEDULE 14A

(RULE 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE SECURITIES

EXCHANGE ACT OF 1934

EXCHANGE ACT OF 1934

| Filed by the Registrant [x] | Filed by a Party other than the Registrant [ ] |

| Check the appropriate box: |

[ ] Preliminary Proxy Statement

[ ] Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

[ ] Definitive Proxy Statement

[x] Definitive Additional Materials

[ ] Soliciting Material Pursuant to Section 240.14a-11c or Section 240.14a-12

Cincinnati Bell Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| [x] | No fee required. | ||

| [ ] | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||

| (1) | Title of each class of securities to which the transaction applies: | ||

| (2) | Aggregate number of securities to which the transaction applies: | ||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | ||

| (4) | Proposed maximum aggregate value of transaction: | ||

| (5) | Total fee paid: | ||

| [ ] | Fee paid previously with preliminary materials. | ||

| [ ] | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||

| (1) | Amount Previously Paid: | ||

| (2) | Form, Schedule or Registration Statement No.: | ||

| (3) | Filing Party: | ||

| (4) | Date Filed: | ||

Cincinnati Bell Inc. (the “Company”) used the materials attached hereto in connection with the Company’s presentation to Institutional Shareholder Services, Inc. on April 3, 2018.

Investor PresentationApril 2018 1

This presentation may contain “forward-looking” statements, as defined in federal securities laws including the Private Securities Litigation Reform Act of 1995, which are based on our current expectations, estimates, forecasts and projections. Statements that are not historical facts, including statements about the beliefs, expectations and future plans and strategies of the Company, are forward-looking statements. Actual results may differ materially from those expressed in any forward-looking statements. The following important factors, among other things, could cause or contribute to actual results being materially and adversely different from those described or implied by such forward-looking statements including, but not limited to: those discussed in this release; we operate in highly competitive industries, and customers may not continue to purchase products or services, which would result in reduced revenue and loss of market share; we may be unable to grow our revenues and cash flows despite the initiatives we have implemented; failure to anticipate the need for and introduce new products and services or to compete with new technologies may compromise our success in the telecommunications industry; our access lines, which generate a significant portion of our cash flows and profits, are decreasing in number and if we continue to experience access line losses similar to the past several years, our revenues, earnings and cash flows from operations may be adversely impacted; negotiations with the providers of content for our video programming may not be successful, potentially resulting in our inability to carry certain programming channels, which could result in the loss of subscribers and due to the influence of some content providers, we may be forced to pay higher rates for some content, resulting in increased costs; our failure to meet performance standards under our agreements could result in customers terminating their relationships with us or customers being entitled to receive financial compensation, which would lead to reduced revenues and/or increased costs; we generate a substantial portion of our revenue by serving a limited geographic area; a large customer accounts for a significant portion of our revenues and accounts receivable and the loss or significant reduction in business from this customer would cause operating revenues to decline and could negatively impact profitability and cash flows; maintaining our telecommunications networks requires significant capital expenditures, and our inability or failure to maintain our telecommunications networks could have a material impact on our market share and ability to generate revenue; increases in broadband usage may cause network capacity limitations, resulting in service disruptions or reduced capacity for customers; we may be liable for material that content providers distribute on our networks; cyber attacks or other breaches of network or other information technology security could have an adverse effect on our business; natural disasters, terrorists acts or acts of war could cause damage to our infrastructure and result in significant disruptions to our operations; the regulation of our businesses by federal and state authorities may, among other things, place us at a competitive disadvantage, restrict our ability to price our products and services and threaten our operating licenses; we depend on a number of third party providers, and the loss of, or problems with, one or more of these providers may impede our growth or cause us to lose customers; a failure of back-office information technology systems could adversely affect our results of operations and financial condition; if we fail to extend or renegotiate our collective bargaining agreements with our labor union when they expire or if our unionized employees were to engage in a strike or other work stoppage, our business and operating results could be materially harmed; the loss of any of the senior management team or attrition among key sales associates could adversely affect our business, financial condition, results of operations and cash flows; our debt could limit our ability to fund operations, raise additional capital, and fulfill our obligations, which, in turn, would have a material adverse effect on our businesses and prospects generally; our indebtedness imposes significant restrictions on us; we depend on our loans and credit facilities to provide for our short-term financing requirements in excess of amounts generated by operations, and the availability of those funds may be reduced or limited; the servicing of our indebtedness is dependent on our ability to generate cash, which could be impacted by many factors beyond our control; we depend on the receipt of dividends or other intercompany transfers from our subsidiaries and investments; the merger (the “merger”) of Hawaiian Telcom Holdco, Inc. (“Hawaiian Telcom”) into a wholly owned subsidiary of Cincinnati Bell is subject to the receipt of clearances or approvals from various regulatory authorities, which may impose conditions that could have an adverse effect on us following the closing of the merger (the “combined company”) or, if not obtained, could prevent completion of the merger; the merger is subject to conditions, including certain conditions that may not be satisfied or completed on a timely basis, if at all, and any delay in completing the merger may reduce or eliminate the benefits expected; the pendency of the merger could materially adversely affect our future business and operations and/or result in a loss of our employees; our shareholders will be diluted by the merger; if completed, the merger may not achieve its intended results, and we and Hawaiian Telcom may be unable to successfully integrate our operations; the combined company is expected to incur expenses related to the integration of the Company and Hawaiian Telcom; the future results of the combined company will suffer if the combined company does not effectively manage its expanded operations following the merger; uncertainties associated with the merger may cause a loss of management personnel and other key employees, which could adversely affect the future business and operations of the combined company; the combined company will have substantial indebtedness following the merger and the credit ratings of the combined company or its subsidiaries may be different from what the companies currently expect; the merger may involve unexpected costs, unexpected liabilities or unexpected delays; the acquisition of OnX may not achieve its intended results, and we may be unable to successfully integrate OnX's operations; the trading price of our common shares may be volatile, and the value of an investment in our common shares may decline; the uncertain economic environment, including uncertainty in the U.S. and world securities markets, could impact our business and financial condition; our future cash flows could be adversely affected if it is unable to fully realize our deferred tax assets; adverse changes in the value of assets or obligations associated with our employee benefit plans could negatively impact shareowners’ deficit and liquidity; changes in tax laws and regulations, and actions by federal, state and local taxing authorities related to the interpretation and application of such tax laws and regulations, could have a negative impact on the our financial results and cash flows; our interpretation of the Tax Cuts and Jobs Act of 2017 could change, and have an adverse impact on financial results; third parties may claim that we are infringing upon their intellectual property, and we could suffer significant litigation or licensing expenses or be prevented from selling products; third parties may infringe upon our intellectual property, and we may expend significant resources enforcing our rights or suffer competitive injury; we could be subject to a significant amount of litigation, which could require us to pay significant damages or settlements; we could incur significant costs resulting from complying with, or potential violations of, environmental, health and human safety laws; and the possibility that the proposed transaction involving Hawaiian Telcom does not close, including due to the failure to satisfy the closing conditions and the other risks and uncertainties detailed in our filings, including our Form 10-K, with the U.S. Securities and Exchange Commission (the “SEC”) as well as Hawaiian Telcom’s filings, including its Form 10-K, with the SEC. These forward-looking statements are based on information, plans and estimates as of the date hereof and there may be other factors that may cause our actual results to differ materially from these forward-looking statements. We assume no obligation to update the information contained in this release except as required by applicable law. Safe Harbor 2

This presentation contains information about adjusted earnings before interest, taxes, depreciation and amortization (Adjusted EBITDA). This is a non-GAAP financial measure used by Cincinnati Bell management when evaluating results of operations and cash flow. Management believes this measure also provide users of the financial statements with additional and useful comparisons of current results of operations and cash flows with past and future periods. Non-GAAP financial measures should not be construed as being more important than comparable GAAP measures. Detailed reconciliations of non-GAAP financial measures to comparable GAAP financial measures are available in the Investor Relations section of www.cincinnatibell.com within the Investor Relations section. The company defines Adjusted EBITDA as GAAP operating income plus depreciation, amortization, restructuring and severance related charges, (gain) loss on sale or disposal of assets, transaction costs, curtailment (gain) loss, asset impairments, components of pension and other retirement plan costs (including interest costs, asset returns, and amortization of actuarial gains and losses), and other special items. Management believes that Adjusted EBITDA provides a useful measure of operational performance. Adjusted EBITDA should not be considered as an alternative to comparable GAAP measures of profitability and may not be comparable with the measures as defined by other companies. Important Additional Information Cincinnati Bell, its directors and certain of its executive officers may be deemed to be participants in the solicitation of proxies from Cincinnati Bell shareholders in connection with the matters to be considered at Cincinnati Bell’s 2018 annual meeting. Cincinnati Bell has filed a proxy statement and WHITE proxy card with the SEC in connection with such solicitation of proxies from Cincinnati Bell shareholders. More detailed information regarding the identity of potential participants, and their direct or indirect interests, by security holdings or otherwise, is set forth in such proxy statement and other materials to be filed with the SEC in connection with Cincinnati Bell’s 2018 annual meeting. CINCINNATI BELL SHAREHOLDERS ARE STRONGLY ENCOURAGED TO READ SUCH PROXY STATEMENT AND ACCOMPANYING WHITE PROXY CARD AND OTHER DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Additional information can also be found in Cincinnati Bell’s Annual Report on Form 10-K for the year ended December 31, 2017, filed with the SEC on February 26, 2018, and in Cincinnati Bell’s Quarterly Reports on Form 10-Q. Cincinnati Bell’s shareholders will be able to obtain, free of charge, any proxy statement, any amendments or supplements to the proxy statement and any other documents filed by Cincinnati Bell with the SEC at the SEC’s website at http://www.sec.gov. In addition, copies will be available free of charge at Cincinnati Bell’s website at investor.cincinnatibell.com or by contacting Cincinnati Bell’s Investor Relations by mail at Cincinnati Bell Inc., 221 East Fourth Street, Cincinnati, Ohio 45202. Non-GAAP Financial Measures 3

Cincinnati Bell TodayCincinnati Bell’s Strategic TransformationStrong Performance Through TransformationCommitment to Shareholder Friendly Corporate Governance Table of Contents 4

Transparency: The transformation initiated by the Board aims at simplifying the business by separating the organizational structure and external reporting around two distinct, complementary businesses – Entertainment and Communications and IT Services.Scale: The creation of this new structure and the added scale through acquisition gives the market a better view for sum of the parts valuation, while giving the company added future value creation opportunity.Execution: The Board and management’s disciplined capital allocation strategy is focused on investing in the business while managing leverage. Proven track record of value creation through sale of wireless and CyrusOne assets.Governance: Strong board commitment to the highest standards of corporate governance through transparency, talent refreshment, and diversification and maintaining the right mix of necessary skills and industry experience. Cincinnati Bell’s Board Has Developed and Overseen the Right Strategy to Support Superior Long-Term Shareholder Returns 5

Cincinnati Bell Today 6

Cincinnati Bell Today Source: Company Filings Deeply penetrated, highly redundant fiber-based network Fiber network covers ~70% of Greater Cincinnati consumer addresses, 60% of the business addresses, and 70% of the macro towersLegacy telecommunications network connecting nearly every building in Greater Cincinnati areaFiber expertise with proven investment and operating track record Entertainment & Communications IT Services & Hardware KeyAssets KeyStrategicIssues Ability to deliver flexible, innovative, end-to-end IT solutions to enterprise customersKey blue chip customer relationshipsNearly 2,800 vendor certifications with numerous industry leading technology partnersOver 1,500 employees Finding attractive opportunities to deploy capital to extend networkContinuing to increase revenues from strategic services (currently ~65%) to outpace legacy product declinesGeographic isolation Duplicative product strategies with CBTS How to expand beyond Cincinnati – organic vs. inorganicSufficient size and scale?Maintaining relevant and comprehensive product portfolio as clients shift to the cloudGaining traction with enterprise customers nationwideUndervalued as compared to relative public comps Pro Forma Revenue Mix Strong Market Position as Leading Fiber Network in Cincinnati and Management Team with 70+ Years of Combined Industry Experience Building Two Distinct, Complementary Lines of Business with Expanded Geographic Reach, Customer Diversification and Increased Runway for Growth Network IT Services 7

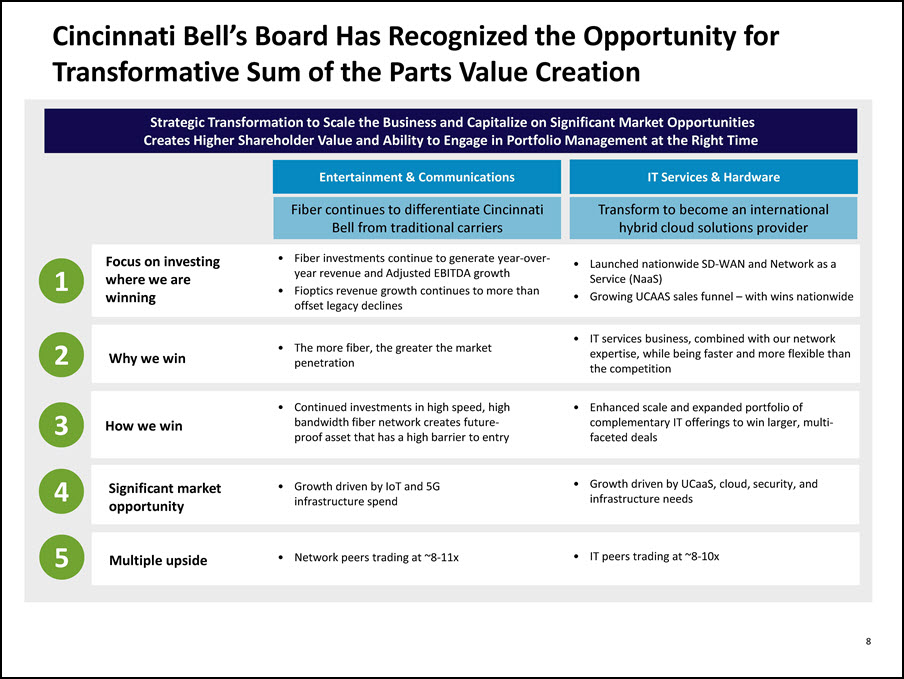

8 Entertainment & Communications IT Services & Hardware Cincinnati Bell’s Board Has Recognized the Opportunity for Transformative Sum of the Parts Value Creation Strategic Transformation to Scale the Business and Capitalize on Significant Market OpportunitiesCreates Higher Shareholder Value and Ability to Engage in Portfolio Management at the Right Time 1 Focus on investing where we are winning Fiber investments continue to generate year-over-year revenue and Adjusted EBITDA growthFioptics revenue growth continues to more than offset legacy declines Launched nationwide SD-WAN and Network as a Service (NaaS)Growing UCAAS sales funnel – with wins nationwide 2 Why we win The more fiber, the greater the market penetration IT services business, combined with our network expertise, while being faster and more flexible than the competition 3 How we win Continued investments in high speed, high bandwidth fiber network creates future-proof asset that has a high barrier to entry Enhanced scale and expanded portfolio of complementary IT offerings to win larger, multi-faceted deals 4 Significant market opportunity Growth driven by IoT and 5G infrastructure spend Growth driven by UCaaS, cloud, security, and infrastructure needs 5 Multiple upside Network peers trading at ~8-11x IT peers trading at ~8-10x Fiber continues to differentiate Cincinnati Bell from traditional carriers Transform to become an international hybrid cloud solutions provider 8

TEV / 2018E Adjusted EBITDA (Including Stock–Based Compensation) Avg.: 9.5x Avg.: 8.9x Valuation Upside in Both Businesses with Increased Scale and Financial Transparency Fiber / Cable IT Solutions & Services Source: Wall Street research, Bloomberg & Capital IQ; Market data as of 3/26/18[1] Based on consensus 2018E midpoint EBITDA guidance of $323mm[2] Based on management 2018 estimates (midpoint of adjusted EBITDA guidance) 2 9 1

Cincinnati Bell’s Strategic Transformation 10

Fioptics Growth Wireline Capex Last 3 Years as % of Revenue Expanded our fiber network to reach 70% of the homes and businesses in Greater Cincinnati (53% FTTH)We are winning against national competitors where we have fiber, with 40% Fioptics penetration that is ~50% where we have FTTH, and significant Fioptics contribution to revenue growth We Are Investing Where We Are Winning… Entertainment & Communications CAGR: 41% 1 3 2 3 Source: Company filings and Capital IQ[1] Excludes Level 3 and adjusted for data centers[2] Pro forma for FairPoint[3] Historicals reflect actuals and are not adjusted to pro forma Verizon CTF, ELNK or Broadview[4] CBB reflects 50 Mbps or more; CTL reflects 40 Mbps or more as of Q2 2016[5] Not pro forma for Level 3 or EarthLink[6] Expects 20% of homes with GPON / 1 Gbps by 2019 Fiber Availability 4 5 5,6 +25 Mbps1 FTTH / 1 Gbps 11

Growth in Network Capacity and Speed Demands 5G and Small Cell Opportunity Market opportunity for 5G accelerationVerizon plans to deploy 8k to 10k small cells in Boston, investing $300 million over six yearsAT&T plans to launch mobile 5G in 12 U.S. markets this yearUBS research estimates 500x increase in small cell sites to support 5G densification in NYC, based on mmWave spectrum and 100 meter propagation distance CAGR: 62% Source: Nokia, Wall Street research and news articles [1] Cisco VNI Forecast as of 6/6/17[2] G. Fast is “Fast access to subscriber terminals” and is a standard to offer fiber-like speeds over copper wires[3] VDSL stands for “very high bit rate digital subscriber line” and is digital subscriber line technology that provides data transmission faster than asymmetric data subscriber lines[4] SNL Small Cell and Tower Projections as of 8/30/17 Entertainment & Communications Cincinnati Bell is Well-Positioned to Capitalize on 5G and Small Cell Opportunities …Which Creates Competitive Advantages And Future Growth Opportunities 2 3 FTTN CAGR: 23% Forecast Global Data Traffic (PB/Month)1 Speed Capability (Mbps) 4 Not a matter of “IF” high bandwidth is necessary but a matter of when not having it makes you irrelevant 12

Merger with Hawaiian Telcom Represents Opportunity to Scale Cincinnati Bell’s Fiber Success in Another Attractive Market Growth Opportunity Hawaii’s fiber-centric technology leader providing voice, video, broadband, data center and cloud solutionsIncumbent position with leading market share and strong brand equity BusinessDescription Approval Process & Closing Expected Cost Synergies* Network: ~$11mm annually *To be realized within two years post-close, and excluding potential revenue synergies from cross-selling opportunities Approved by Hawaiian Telcom shareholders Cleared the HSR review period Received approval from Hawaii DCCA Cable Television DivisionPending approval from FCC and Hawaiian PUCClosing expected in H2 2018Will add two existing Hawaiian Telcom directors to the CBB board at close Cincinnati Bell Network Map Hawaiian Telcom Network Map Entertainment & Communications Adds operational scale and expands the Company’s fiber-significant footprint and commercial opportunity to HawaiiMDU growth opportunity and strategic subset a Trans-Pacific cable assetOpportunity to continue fiber investment in Hawaii – currently 66% FTTH in Oahu, with opportunity to continue Oahu build and invest in other islands where ROI makes sense Combined Network business with over 14k fiber route miles 13

Local market focus – efficient, quick to respond and loyal customersLeader in fiber roll outOTT partnerships to bundle videoPartnerships / managed Wi-Fi products and retail stores Consumer / SMBEnterpriseCarrier services (backhaul, interconnect, small cell, etc.)Public Wi-Fi / DASDark Fiber Over 14k fiber route miles in Cincinnati and Hawaii24k+ fiber lit buildings in Cincinnati and Hawaii Recent win provides wireless tower backhaul services to >90% of towers in Cincinnati and >80% in Hawaii; 250 small cell sites in Cincinnati400k+ broadband subs in Cincinnati and HawaiiLong haul, middle mile and last mile access network across CincinnatiNo competitor with dense fiber built to the same extent as CBBLocal and pole agreements Entertainment & Communications Smart city / public Wi-FiFixed wireless applications Transformation Has Created A Unique Network & Communications Platform Dense Fiber Network Multi-Platform Capabilities InnovativeStrategy While ultra-localized focus allows us to beat the large national players – we are your hometown team in Cincinnati and Hawaii 14

Acquisition of OnX, Creating A Leading North American IT Services Provider… Growth Opportunity BusinessDescription Closing and 4Q17 Contribution Expected Cost Synergies* Expansion of geographic footprint and addressable market beyond Cincinnati to accelerate momentum in IT servicesAttractive enterprise customer base adding diversification and cross-selling opportunities Closed on October 2, 20174Q17 Contribution:$150mm in revenue OnX provides industry-leading technology services and solutions to enterprise customers in the U.S., Canada and the U.K. ~$10mm annually *To be realized within two years post-close, and excluding potential revenue synergies from cross-selling opportunities Offices 20+Offices 2,000+Customers Key Technology Partners / Certifications Combined IT Services business with a diversified customer base and increased geographic footprint 14 IT Services & Hardware

$402bn Market Fragmented IT Services Market1 Top Provider 4% Next Top 10 Providers 25% Growing Markets …which Positions Cincinnati Bell to Tap Into a Fragmented and Growing IT Services Market… Scaling to Create Strategic Flexibility Q4 ’17 Service Revenue Mix [1] Based on Gartner research; Market defined as 2016A North America IT Services market [2] Based on Gartner research[3] Market size in billions, figures represent North America estimates[4] Includes cloud-based conferencing, telephony and messaging 5 Other Service Providers71% IT Services & Hardware 16 Goal of $100mm Adj. EBITDA to create scale Market2 2017 Market Size3 2015-2020 CAGR Cloud-Based Unified Communications4 $109 13% IaaS (Cloud) 18 32% Enterprise Security Services 22 10% Tech Consulting & Implementation 120 3%

($ mm) Recent Strategic Initiatives Growing Higher Margin Recurring Services …Focused on Growing Higher Margin, Recurring IT Services Launched nationwide SD-WAN and NaaS productsReorganized segment adding CLEC commercial operations to highlight strength of growing UCaaS businessRecent win of national NaaS project to start in H2 2018 (providing SD-WAN and UCaaS to 3,500 retail locations) 1 1 [1] Includes OnX as of October 3, 2017[2] Pro Forma revenue includes OnX revenue for the twelve months ended December 31, 2017 as disclosed in Cincinnati Bell’s 2017 Form 10-K Creating Hybrid IT Solutions Provider Well Positioned to Capitalize on Significant Market Opportunities Presented by UCaaS, Cloud, Security, and Infrastructure Needs IT Services & Hardware Diversifying Customer Mix GE Revenue % of IT Services & Hardware Revenue 2016 2017(PF) 17 2

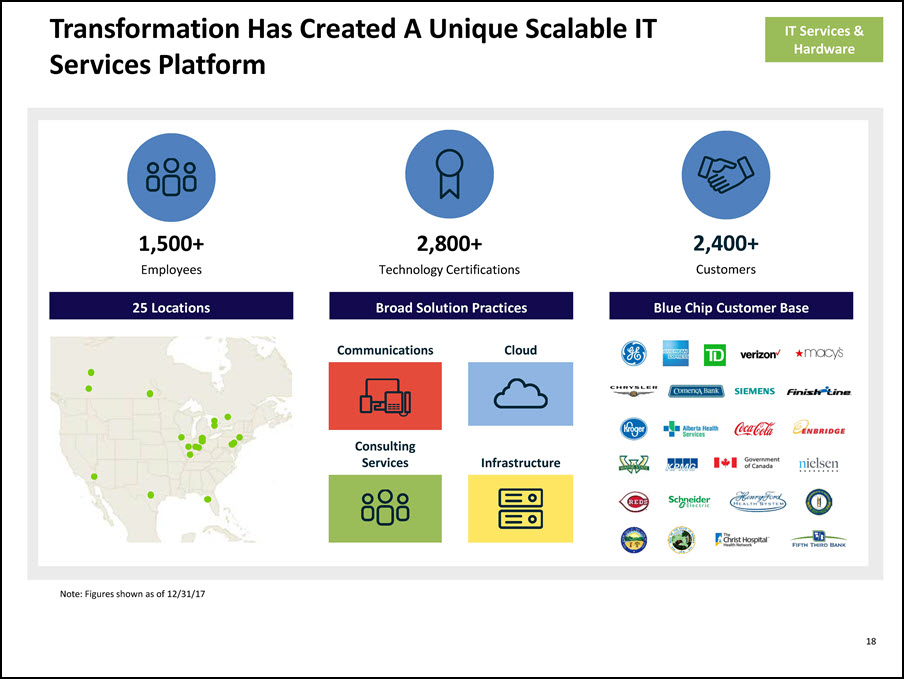

Transformation Has Created A Unique Scalable IT Services Platform 1,500+ Employees 2,400+Customers 2,800+ Technology Certifications Communications Cloud Infrastructure Consulting Services Broad Solution Practices 25 Locations Blue Chip Customer Base Note: Figures shown as of 12/31/17 IT Services & Hardware 18

Strong Performance Through Transformation 19

Execution of Strategy Has Continued to Yield Results… Strategic Revenue Growth [1] Total revenue excluding CyrusOne, wireless, accounting adjustments recorded for reporting of discontinued operations and eliminations 2 Disciplined Capital Allocation Strategy Investments in fiber and IT solutions create platforms for long-term valueMonetized CyrusOne and wireless assets – improved leverage profile from ~6x in 2013 to ~4x in 2017Ability to fund fiber investments through cash flow Strategic Revenue CAGR: 18% % of Total Revenue1 30% 34% 38% 46% 54% 55% ($ in mm) Reorganizing to Facilitate Growth and Cost Management 20 Completed internal reorganization leading to two distinct business units, with the appropriate scale, structure and leadership committed to driving their respective brands forwardReporting changes beginning 1Q’18 to improve investors’ ability to appropriately value these services independentlyTransferring commercial CLEC operations out of E&C into IT services to consolidate VoIP operations, and highlight the strength of our growing UCaaS businessIT Services & Hardware will report revenue by product practices: communications, cloud, consulting & infrastructure, demonstrating the breadth of our services

Investments in Fiber Showing Results for Shareholders …Generating Above-Market Revenue Growth… Source: Company filings [1] Pro forma for FairPoint[2] Pro forma for EarthLink[3] Excludes Level 3 and adjusted for data center sale[4] Pro forma for CTF acquisition Our fiber-dense network differentiates us from traditional carriers, allowing us to overcome legacy declines in each quarter of 2017 3 1 2 E&C E&C 1 2 3 Q4 ‘17 vs Q4 ‘16 2017 vs 2016 4 21

Total Shareholder Return …And Outperforming the Wireline Sector Over the Long-Run… Source: Capital IQ as of 3/26/18Note: Companies shown based on wireline focus and similar market cap size. Wireline average includes CNSL, CTL, WIN and FTR. 22 2013 2017 2014 05/31: Leigh Fox became CEO 09/01: Leigh Fox appointed COO and Andy Kaiser appointed CFO 2016 2015 2018 Data center IPO of CyrusOne monetized for +$1.8bn 07/10: Announced combinations with HCOM (expected H2’18) and OnX (completed 10/2) ~$660mm invested in fiber assets from 2013 to 2017Improved leverage profile from ~6x in 2013 to ~4x in 2017 04/07: Sold wireless assets to Verizon Ongoing pressures from FCC mandated rate reductions in carrier market Successful reorganization National carriers increased focus on improving network efficiencies The FCC has maintained significant regulatory restraints on the traditional ILECs while increasing opportunities for new competitive entrants Structural industry challenges The Board has actively guided CBB’s strategic transfor-mation (10.5%) (15.7%) (31.6%) (50.5%) (79.2%) (80.6%) 01/31: Ted Torbeck named CEO

TEV / Adjusted EBITDA Multiples1 …With Improved Valuation as a Result of the Transformation Source: Wall Street research, company filings, Capital IQ as of 3/26/18Note: EBITDA adjusted to include SBC[1] FTR and WIN multiples are pro forma; reflects forward year adjusted EBITDA for multiples (2015E and 2018E) at each point in time[2] TEV adjusted for value of CyrusOne equity ($893mm as of 3/26/15)[3] Based on consensus 2018E midpoint EBITDA guidance of $323mm[4] Multiple adjusted pro forma for FTR’s acquisition of CA, FL and TX assets CTL is the Only Other Wireline Company to Increase its Multiple, Which Increased Only After the Acquisition of a Larger “Pure Play" Fiber Provider in Level 3 2 4 23 3

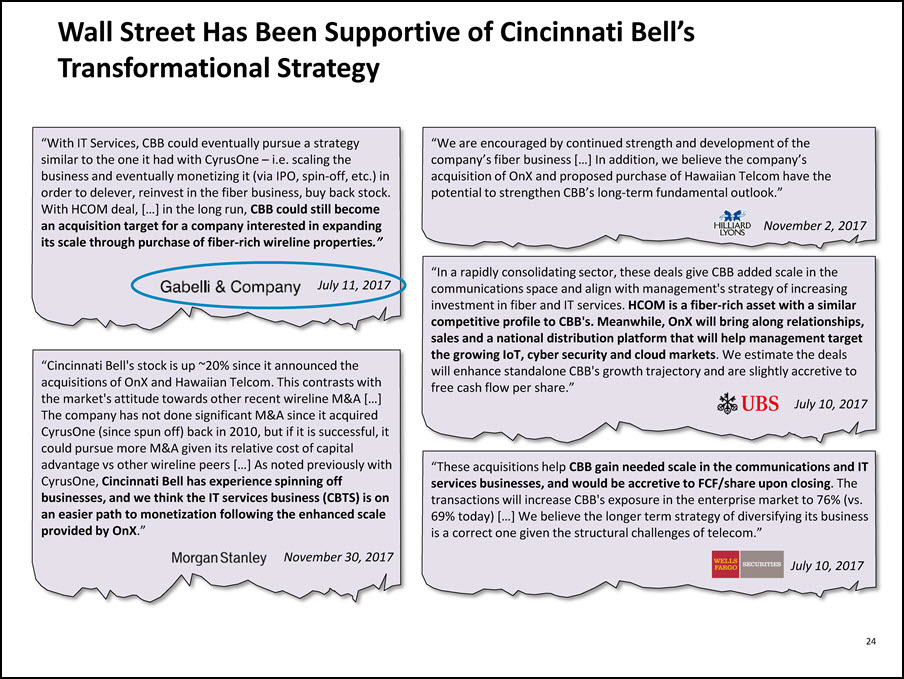

“We are encouraged by continued strength and development of the company’s fiber business […] In addition, we believe the company’s acquisition of OnX and proposed purchase of Hawaiian Telcom have the potential to strengthen CBB’s long-term fundamental outlook.” November 2, 2017 “Cincinnati Bell's stock is up ~20% since it announced the acquisitions of OnX and Hawaiian Telcom. This contrasts with the market's attitude towards other recent wireline M&A […] The company has not done significant M&A since it acquired CyrusOne (since spun off) back in 2010, but if it is successful, it could pursue more M&A given its relative cost of capital advantage vs other wireline peers […] As noted previously with CyrusOne, Cincinnati Bell has experience spinning off businesses, and we think the IT services business (CBTS) is on an easier path to monetization following the enhanced scale provided by OnX.” November 30, 2017 “In a rapidly consolidating sector, these deals give CBB added scale in the communications space and align with management's strategy of increasing investment in fiber and IT services. HCOM is a fiber-rich asset with a similar competitive profile to CBB's. Meanwhile, OnX will bring along relationships, sales and a national distribution platform that will help management target the growing IoT, cyber security and cloud markets. We estimate the deals will enhance standalone CBB's growth trajectory and are slightly accretive to free cash flow per share.” July 10, 2017 Wall Street Has Been Supportive of Cincinnati Bell’s Transformational Strategy “These acquisitions help CBB gain needed scale in the communications and IT services businesses, and would be accretive to FCF/share upon closing. The transactions will increase CBB's exposure in the enterprise market to 76% (vs. 69% today) […] We believe the longer term strategy of diversifying its business is a correct one given the structural challenges of telecom.” July 10, 2017 “With IT Services, CBB could eventually pursue a strategy similar to the one it had with CyrusOne – i.e. scaling the business and eventually monetizing it (via IPO, spin-off, etc.) in order to delever, reinvest in the fiber business, buy back stock. With HCOM deal, […] in the long run, CBB could still become an acquisition target for a company interested in expanding its scale through purchase of fiber-rich wireline properties.” July 11, 2017 24

Commitment to Shareholder Friendly Corporate Governance 25

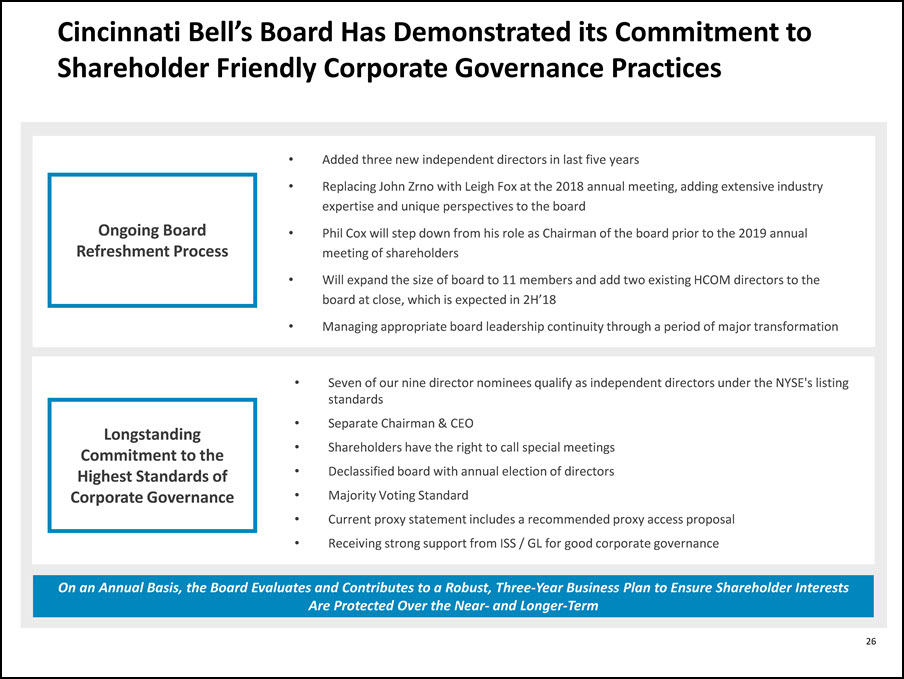

Added three new independent directors in last five yearsReplacing John Zrno with Leigh Fox at the 2018 annual meeting, adding extensive industry expertise and unique perspectives to the boardPhil Cox will step down from his role as Chairman of the board prior to the 2019 annual meeting of shareholdersWill expand the size of board to 11 members and add two existing HCOM directors to the board at close, which is expected in 2H’18Managing appropriate board leadership continuity through a period of major transformation Seven of our nine director nominees qualify as independent directors under the NYSE's listing standardsSeparate Chairman & CEOShareholders have the right to call special meetingsDeclassified board with annual election of directorsMajority Voting StandardCurrent proxy statement includes a recommended proxy access proposalReceiving strong support from ISS / GL for good corporate governance Ongoing Board Refreshment Process Longstanding Commitment to the Highest Standards of Corporate Governance Cincinnati Bell’s Board Has Demonstrated its Commitment to Shareholder Friendly Corporate Governance Practices 26 On an Annual Basis, the Board Evaluates and Contributes to a Robust, Three-Year Business Plan to Ensure Shareholder Interests Are Protected Over the Near- and Longer-Term

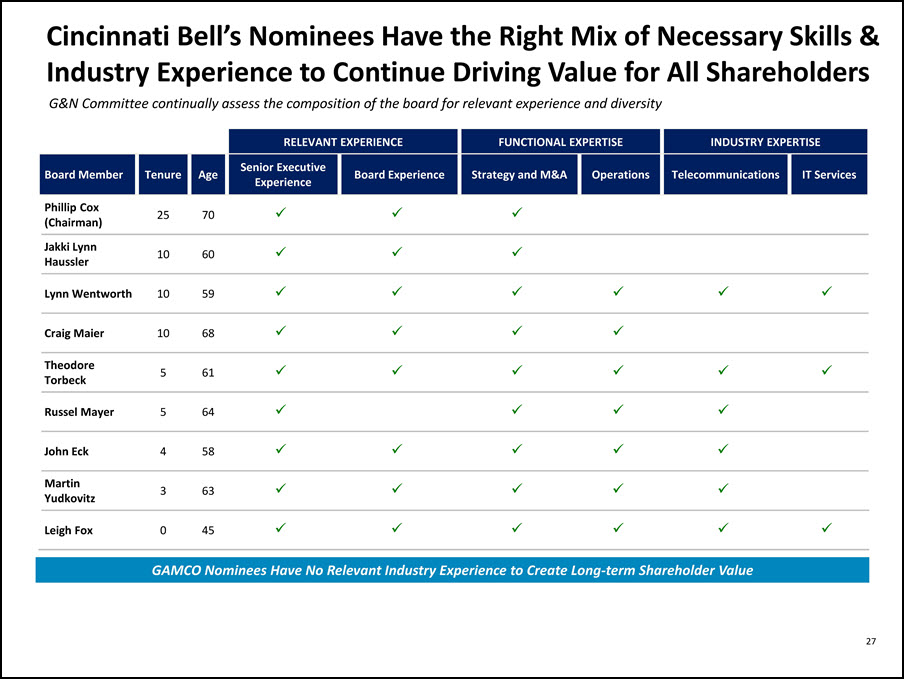

RELEVANT EXPERIENCE FUNCTIONAL EXPERTISE INDUSTRY EXPERTISE Board Member Tenure Age Senior Executive Experience Board Experience Strategy and M&A Operations Telecommunications IT Services Phillip Cox (Chairman) 25 70 Jakki Lynn Haussler 10 60 Lynn Wentworth 10 59 Craig Maier 10 68 Theodore Torbeck 5 61 Russel Mayer 5 64 John Eck 4 58 Martin Yudkovitz 3 63 Leigh Fox 0 45 27 Cincinnati Bell’s Nominees Have the Right Mix of Necessary Skills & Industry Experience to Continue Driving Value for All Shareholders G&N Committee continually assess the composition of the board for relevant experience and diversity GAMCO Nominees Have No Relevant Industry Experience to Create Long-term Shareholder Value 27

DIRECTOR EXPERIENCE & EXPERTISE Russel MayerOctober 2013*Brings relevant industry experience from the customer’s perspective Over 35 years of information technology and business process improvement experience at large, global organizations:Previously held several, executive-level information technology and business process improvement positions at General Electric.Most recently served as Executive Vice President, CIO, and Quality Leader at GE Healthcare from 2009 to 2012.Prior to that, held multiple positions at Chiquita Brands, Republic Steel and Enduro Stainless. John EckOctober 2014*Brings relevant industry experience from the perspective of a producer and distributor of media content Over 30 years of media and information technology experience at Univision, NBC Universal and General Electric:Serves as Chief Operations Officer and Executive Vice President, Operations and Technology, at Univision Communications, Inc., a leading Hispanic media company in the United States.Previously worked at NBC Universal (“NBCU”) for 18 years, most recently serving as President, Media Works.Prior to joining NBCU, Mr. Eck held various other executive and financial positions at General Electric. Martin YudkovitzJuly 2015*Brings relevant industry experience having led large strategic business innovation initiatives Over 30 years of experience in the broadcast and media entertainment industries:Served as Head of The Walt Disney Company’s Strategic Innovation Group (2010 through 2015).Served as the Senior Vice President for Corporate Strategy and Business Development at Disney (2005-2010) and as President of TiVo (2003-2005).Previously a long-time senior executive at NBC – was a key member of the teams that developed and launched the CNBC and MSNBC networks. Recent Independent Directors Added to Cincinnati Bell’s Board, Providing Relevant Perspectives and Industry Expertise 28

29 Board Composition and Diversity Consistent with S&P 1500 Companies Board Composition Comparison Source: IRRC Institute & ISS Board Refreshment Trends, Jan 2017Note: CBB shows new board composition after the departure of John Zrno and addition of Leigh Fox

Conclusion: Cincinnati Bell Has the Right Team, Strategy and Governance to Deliver Superior Long-Term Shareholder Returns 30 Transparency: The transformation initiated by the Board aims at simplifying the business by separating the organizational structure and external reporting around two distinct, complementary businesses – Entertainment and Communications and IT Services.Scale: The creation of this new structure and the added scale through acquisition gives the market a better view for sum of the parts valuation, while giving the company added future value creation opportunity.Execution: The Board and management’s disciplined capital allocation strategy is focused on investing in the business while managing leverage. Proven track record of value creation through sale of wireless and CyrusOne assets.Governance: Strong board commitment to the highest standards of corporate governance through transparency, talent refreshment, and diversification and maintaining the right mix of necessary skills and industry experience.

Appendix 31

Summary of Defined Terms and Abbreviations UCaaS – unified communications as a serviceMDU – multi-dwelling unitFTTN – fiber-to-the-nodeFTTH – fiber-to-the-home Fiber availability – % of total market homes with FTTN and/or FTTH availableSMB – small and medium size businessesDAS – distributed antenna systemsOTT – over-the-top (often referring to video streaming services delivered outside the bundle via the internet)FHSI – fiber-based high speed internetSD-WAN – software defined wide area networkNaaS – network as a serviceCLEC – competitive local exchange carrier 32