UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

For the fiscal year ended December 31, 2017

of

AGCO CORPORATION

A Delaware Corporation

IRS Employer Identification No. 58-1960019

SEC File Number 1-12930

4205 River Green Parkway

Duluth, GA 30096

(770) 813-9200

AGCO Corporation’s Common Stock is registered pursuant to Section 12(b) of the Act and is listed on the New York Stock Exchange.

AGCO Corporation is a well-known seasoned issuer.

AGCO Corporation is required to file reports pursuant to Section 13 or Section 15(d) of the Act. AGCO Corporation (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days.

Disclosure of delinquent filers pursuant to Item 405 of Regulation S-K will be contained in a definitive proxy statement, portions of which are incorporated by reference into Part III of this Form 10-K.

AGCO Corporation has submitted electronically and posted on its corporate website every Interactive Data File for the periods required to be submitted and posted pursuant to Rule 405 of Regulation S-T.

The aggregate market value of AGCO Corporation’s Common Stock (based upon the closing sales price quoted on the New York Stock Exchange) held by non-affiliates as of June 30, 2017 was approximately $4.5 billion. For this purpose, directors and officers and the entities that they control have been assumed to be affiliates. As of February 23, 2018, 79,614,896 shares of AGCO Corporation’s Common Stock were outstanding.

AGCO Corporation is a large accelerated filer and is not a shell company.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of AGCO Corporation’s Proxy Statement for the 2018 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

| TABLE OF CONTENTS | |

PART I

Item 1. Business

AGCO Corporation (“AGCO,” “we,” “us,” or the “Company”) was incorporated in Delaware in April 1991. Our executive offices are located at 4205 River Green Parkway, Duluth, Georgia 30096, and our telephone number is (770) 813-9200. Unless otherwise indicated, all references in this Form 10-K to the Company include our subsidiaries.

General

We are a leading manufacturer and distributor of agricultural equipment and related replacement parts throughout the world. We sell a full range of agricultural equipment, including tractors, combines, self-propelled sprayers, hay tools, forage equipment, seeding and tillage equipment, implements, and grain storage and protein production systems. Our products are widely recognized in the agricultural equipment industry and are marketed under a number of well-known brands, including Challenger®, Fendt®, GSI®, Massey Ferguson® and Valtra®. We distribute most of our products through approximately 4,200 independent dealers and distributors in approximately 150 countries. In addition, we also provide retail and wholesale financing through our finance joint ventures with Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A., which we refer to as “Rabobank.”

Products

The following table sets forth a description of the Company’s products and their percentage of net sales:

| Percentage of Net Sales | |||||||||||

| Product | Product Description | 2017 | 2016 | 2015 | |||||||

| Tractors | • | High horsepower tractors (100 to 600 horsepower); typically used on larger farms, primarily for row crop production | 57 | % | 57 | % | 57 | % | |||

| • | Utility tractors (40 to 100 horsepower); typically used on small- and medium-sized farms and in specialty agricultural industries, including dairy, livestock, orchards and vineyards | ||||||||||

| • | Compact tractors (under 40 horsepower); typically used on small farms and specialty agricultural industries, as well as for landscaping and residential uses | ||||||||||

| Replacement Parts | • | Replacement parts for all of the products we sell, including products no longer in production. Most of our products can be economically maintained with parts and service for a period of ten to 20 years. Our parts inventories are maintained and distributed through a network of master and regional warehouses throughout North America, South America, Europe, Africa, China and Australia in order to provide timely response to customer demand for replacement parts | 16 | % | 16 | % | 16 | % | |||

| Grain Storage and Protein Production Systems | • | Grain storage bins and related drying and handling equipment systems; seed-processing systems; swine and poultry feed storage and delivery, ventilation and watering systems; and egg production systems and broiler production equipment | 13 | % | 12 | % | 10 | % | |||

| Hay Tools and Forage Equipment, Implements & Other Equipment | • | Round and rectangular balers, loader wagons, self-propelled windrowers, forage harvesters, disc mowers, spreaders, rakes, tedders, and mower conditioners; used for the harvesting and packaging of vegetative feeds used in the cattle, dairy, horse and renewable fuel industries | 7 | % | 7 | % | 9 | % | |||

| • | Implements, including disc harrows, which cut through crop residue, leveling seed beds and mixing chemicals with the soils; heavy tillage, which break up soil and mix crop residue into topsoil, with or without prior discing; field cultivators, which prepare a smooth seed bed and destroy weeds; and drills, which are primarily used for small grain seeding | ||||||||||

| • | Planters and other planting equipment; used to apply fertilizer and plant seeds in the field, typically used in row crop seeding | ||||||||||

| • | Other equipment, including loaders; used for a variety of tasks, including lifting and transporting hay crops | ||||||||||

| Combines | • | Combines, sold with a variety of threshing technologies and complemented by a variety of crop-harvesting heads; typically used in harvesting grain crops such as corn, wheat, soybeans and rice | 4 | % | 4 | % | 4 | % | |||

| Application Equipment | • | Self-propelled, three- and four-wheeled vehicles and related equipment; for use in the application of liquid and dry fertilizers and crop protection chemicals both prior to planting crops (“pre-emergence”) and after crops emerge from the ground (“post-emergence”) | 3 | % | 4 | % | 4 | % | |||

1

Marketing and Distribution

We distribute products primarily through a network of independent dealers and distributors. Our dealers are responsible for retail sales of equipment to end users and after-sales service and support. Our distributors may sell our products through networks of dealers supported by the distributors, and our distributors also may directly market our products and provide customer service support. Our sales are not dependent on any specific dealer, distributor or group of dealers.

In some countries, we utilize associates and licensees to provide a distribution channel for our products and a source of low-cost production for certain Massey Ferguson and Valtra products. Associates are entities in which we have an ownership interest, most notably in India. Licensees are entities in which we have no ownership interest. The associate or licensee generally has the exclusive right to produce and sell Massey Ferguson or Valtra equipment in its licensed territory under such tradenames but may not sell these products in other countries. We generally license certain technology to these licensees and associates, and we may sell them certain components used in local manufacturing operations.

| Independent Dealers and Distributors | Percent of Net Sales | ||||||||||

| Geographical region | 2017 | 2017 | 2016 | 2015 | |||||||

| Europe | 1,530 | 53 | % | 53 | % | 51 | % | ||||

| North America | 1,830 | 23 | % | 24 | % | 26 | % | ||||

| South America | 250 | 13 | % | 12 | % | 13 | % | ||||

Rest of World (1) | 590 | 11 | % | 11 | % | 10 | % | ||||

____________________________________

(1) Consists of approximately 71 countries in Africa, the Middle East, Australia and Asia.

Dealer Support and Supervision

We believe that one of the most important criteria affecting a farmer’s decision to purchase a particular brand of equipment is the quality of the dealer who sells and services the equipment. We support our dealers in order to improve the quality of our dealer network. We monitor each dealer’s performance and profitability and establish programs that focus on continuous dealer improvement. Our dealers generally have sales territories for which they are responsible.

We believe that our ability to offer our dealers a full product line of agricultural equipment and related replacement parts, as well as our ongoing dealer training and support programs focusing on business and inventory management, sales, marketing, warranty and servicing matters and products, help ensure the vitality and increase the competitiveness of our dealer network. We also maintain dealer advisory groups to obtain dealer feedback on our operations.

We provide our dealers with volume sales incentives, demonstration programs and other advertising support to assist sales. We design our sales programs, including retail financing incentives, and our policies for maintaining parts and service availability with extensive product warranties, to enhance our dealers’ competitive position.

Manufacturing and Suppliers

Manufacturing and Assembly

We manufacture and assemble our products in 51 locations worldwide, including seven locations where we operate joint ventures. Our locations are intended to optimize capacity, technology or local costs. Furthermore, we continue to balance our manufacturing resources with externally-sourced machinery, components and/or replacement parts to enable us to better control costs, inventory levels and our supply of components. We believe that our manufacturing facilities are sufficient to meet our needs for the foreseeable future. Please refer to Item 2, “Properties,” where a listing of our principal manufacturing locations is presented.

Our AGCO Power engines division produces diesel engines, gears and generating sets. The diesel engines are manufactured for use in a portion of our tractors, combines and sprayers, and also are sold to third parties. AGCO Power specializes in the manufacturing of off-road engines in the 75 to 600 horsepower range.

2

Third-Party Suppliers

We externally source some of our machinery, components and replacement parts from third-party suppliers. Our production strategy is intended to optimize our research and development and capital investment requirements and to allow us greater flexibility to respond to changes in market conditions.

We purchase some fully-manufactured tractors from Tractors and Farm Equipment Limited (“TAFE”), Carraro S.p.A. and Iseki & Company, Limited. We also purchase other tractors, implements and hay and forage equipment from various third-party suppliers. Refer to “Related Parties” within Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” for further discussion of our relationship with TAFE. In addition to the purchase of machinery, third-party suppliers supply us with significant components used in our manufacturing operations. We select third-party suppliers that we believe are low cost, high quality and possess the most appropriate technology. We also assist in the development of these products or component parts based upon our own design requirements. Our past experience with outside suppliers generally has been favorable.

Seasonality

Generally, retail sales by dealers to farmers are highly seasonal and are a function of the timing of the planting and harvesting seasons. To the extent practicable, we attempt to ship products to our dealers and distributors on a level basis throughout the year to reduce the effect of seasonal retail demands on our manufacturing operations and to minimize our investment in inventory. Our financing requirements are subject to variations due to seasonal changes in working capital levels, which typically increase in the first half of the year and then decrease in the second half of the year. The fourth quarter is also typically a period for higher retail sales because of our customers’ year-end tax planning considerations, the increase in the availability of funds from completed harvests and the timing of dealer incentives.

Competition

The agricultural industry is highly competitive. We compete with several large national and international full-line suppliers, as well as numerous short-line and specialty manufacturers with differing manufacturing and marketing methods. Our two principal competitors on a worldwide basis are Deere & Company and CNH Industrial N.V. We have regional competitors around the world that have significant market share in a single country or a group of countries.

We believe several key factors influence a buyer’s choice of farm equipment, including the strength and quality of a company’s dealers, the quality and pricing of products, dealer or brand loyalty, product availability, terms of financing and customer service. See “Marketing and Distribution” for additional information.

Engineering and Research

We make significant expenditures for engineering and applied research to improve the quality and performance of our products, to develop new products and to comply with government safety and engine emissions regulations.

In addition, we also offer a variety of precision farming technologies that provide farmers with the capability to enhance productivity and profitability on the farm. These technologies are installed in our products and include satellite-based steering, field data collection, yield mapping and telemetry-based fleet management systems.

Wholesale Financing

Primarily in the United States and Canada, we engage in the standard industry practice of providing dealers with floor plan payment terms for their inventories of farm equipment for extended periods generally through our AGCO Finance joint ventures. The terms of our wholesale finance agreements with our dealers vary by region and product line, with fixed payment schedules on all sales, generally ranging from one to 12 months. In the United States and Canada, dealers typically are not required to make an initial down payment, and our terms allow for an interest-free period generally ranging from one to 12 months, depending on the product. Amounts due from sales to dealers in the United States and Canada are immediately due upon a retail sale of the underlying equipment by the dealer, with the exception of sales of grain storage and protein production systems, as discussed further below. If not previously paid by the dealer, installment payments generally are required beginning after the interest-free period with the remaining outstanding equipment balance generally due within 12 months after shipment. In limited circumstances, we provide sales terms, and in some cases, interest-free periods that are longer than 12 months for certain products. These typically are specified programs, predominantly in the United States and Canada, where interest is charged after a period of up to 24 months, depending on the year of the sale and the dealer or distributor ordering or their sales

3

volume during the preceding year. We also provide financing to dealers on used equipment accepted in trade. We generally obtain a security interest in the new and used equipment we finance.

Typically, sales terms outside the United States and Canada are of a shorter duration, generally ranging from 30 to 180 days. In many cases, we retain a security interest in the equipment sold on extended terms. In certain international markets, our sales are generally backed by letters of credit or credit insurance.

Sales of grain storage and protein production systems both in the United States and in other countries generally are payable within 30 days of shipment. In certain countries, sales of such systems in which the Company is responsible for construction or installation and which may be contingent upon customer acceptance, payment terms vary by market and product, with fixed payment schedules on all sales.

We have an agreement to permit transferring, on an ongoing basis, a majority of our wholesale receivables in North America, Europe and Brazil to our AGCO Finance joint ventures in the United States, Canada, Europe and Brazil. Upon transfer, the wholesale receivables maintain standard payment terms, including required regular principal payments on amounts outstanding and interest charges at market rates. Qualified dealers may obtain additional financing through our U.S., Canadian, European and Brazilian finance joint ventures at the joint ventures’ discretion. In addition, AGCO Finance joint ventures may provide wholesale financing directly to dealers in Europe, Brazil and Australia.

Retail Financing

Our AGCO Finance joint ventures offer financing to most of the end users of our products. Besides contributing to our overall profitability, the AGCO Finance joint ventures can enhance our sales efforts by tailoring retail finance programs to prevailing market conditions. Our finance joint ventures are located in the United States, Canada, Europe, Brazil, Argentina and Australia and are owned by AGCO and by a wholly-owned subsidiary of Rabobank. Refer to “Finance Joint Ventures” within Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” for further information.

In addition, Rabobank is the primary lender with respect to our credit facility and our senior term loan, as are more fully described in “Liquidity and Capital Resources” within Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Our historical relationship with Rabobank has been strong, and we anticipate its continued long-term support of our business.

Intellectual Property

We own and have licenses to the rights under a number of domestic and foreign patents, trademarks, trade names and brand names relating to our products and businesses. We defend our patent, trademark and trade and brand name rights primarily by monitoring competitors’ machines and industry publications and conducting other investigative work. We consider our intellectual property rights, including our right to use our trade and brand names, important in the operation of our businesses. However, we do not believe we are dependent on any single patent, trademark, trade name or group of patents or trademarks, trade names or brand names. We intend to maintain the separate strengths and identities of our core brand names and product lines.

Environmental Matters and Regulation

We are subject to environmental laws and regulations concerning emissions to the air, discharges of processed or other types of wastewater, and the generation, handling, storage, transportation, treatment and disposal of waste materials. These laws and regulations are constantly changing, and the effects that they may have on us in the future are impossible to predict with accuracy. It is our policy to comply with all applicable environmental, health and safety laws and regulations, and we believe that any expense or liability we may incur in connection with any noncompliance with any law or regulation or the cleanup of any of our properties will not have a materially adverse effect on us.

The engines manufactured by our AGCO Power engine division, which specializes in the manufacturing of non-road engines in the 75 to 600 horsepower range, currently comply with emissions standards and related requirements set by European, Brazilian and U.S. regulatory authorities, including both the United States Environmental Protection Agency and various state authorities. We expect to meet future emissions requirements through the introduction of new technology to our engines and exhaust after-treatment systems, as necessary. In some markets (such as the United States), we must obtain governmental environmental approvals in order to import our products, and these approvals can be difficult or time-consuming to obtain or may not be obtainable at all. For example, our AGCO Power engine division and our engine suppliers are subject to air quality standards, and production at our facilities could be impaired if AGCO Power and these suppliers are unable to timely

4

respond to any changes in environmental laws and regulations affecting engine emissions. Compliance with environmental and safety regulations has added, and will continue to add, to the cost of our products and increase the capital-intensive nature of our business.

Climate change, as a result of emissions of greenhouse gases, is a significant topic of discussion and may generate U.S. and other regulatory responses. It is impracticable to predict with any certainty the impact on our business of climate change or the regulatory responses to it, although we recognize that they could be significant. The most direct impacts are likely to be an increase in energy costs, which would increase our operating costs (through increased utility and transportation costs) and an increase in the costs of the products we purchase from others. In addition, increased energy costs for our customers could impact demand for our equipment. It is too soon for us to predict with any certainty the ultimate impact of additional regulation, either directionally or quantitatively, on our overall business, results of operations or financial condition.

Regulation and Government Policy

Domestic and foreign political developments and government regulations and policies directly affect the agricultural industry and indirectly affect the agricultural equipment business in the United States and abroad. The application, modification or adoption of laws, regulations or policies could have an adverse effect on our business.

We have manufacturing facilities or other physical presence in approximately 32 countries and sell our products in approximately 150 countries. This subjects us to a range of trade, product, foreign exchange, employment, tax and other laws and regulations, in addition to the environmental regulations discussed previously, in a significant number of jurisdictions. Many jurisdictions and a variety of laws regulate the contractual relationships with our dealers. These laws impose substantive standards on the relationships between us and our dealers, including events of default, grounds for termination, non-renewal of dealer contracts and equipment repurchase requirements. Such laws could adversely affect our ability to terminate our dealers.

In addition, each of the jurisdictions within which we operate or sell products has an important interest in the success of its agricultural industry and the consistency of the availability of reasonably priced food sources. These interests result in active political involvement in the agricultural industry, which, in turn, can impact our business in a variety of ways.

Employees

As of December 31, 2017, we employed approximately 20,500 employees, including approximately 4,500 employees in the United States and Canada. A majority of our employees at our manufacturing facilities, both domestic and international, are represented by collective bargaining agreements and union contracts with terms that expire on varying dates. We currently do not expect any significant difficulties in renewing these agreements.

5

Available Information

Our Internet address is www.agcocorp.com. We make the following reports filed by us available, free of charge, on our website under the heading “SEC Filings” in our website’s “Investors” section:

| • | annual reports on Form 10-K; |

| • | quarterly reports on Form 10-Q; |

| • | current reports on Form 8-K; |

| • | proxy statements for the annual meetings of stockholders; |

| • | reports on Form SD; and |

| • | Forms 3, 4 and 5 |

These reports are made available on our website as soon as practicable after they are filed with the Securities and Exchange Commission (“SEC”).

We also provide corporate governance and other information on our website. This information includes:

| • | charters for the standing committees of our board of directors, which are available under the heading “Charters of the Committees of the Board” in the “Governance, Committees, & Charters” section of the “Corporate Governance” section of our website located under “Investors,” and |

| • | our Global Code of Conduct, which is available under the heading “Global Code of Conduct” in the “Corporate Governance” section of our website located under “Investors.” |

In addition, in the event of any waivers of our Global Code of Conduct, those waivers will be available under the heading “Corporate Governance” of our website.

Financial Information on Geographical Areas

For financial information on geographical areas, see Note 15 of our Consolidated Financial Statements contained in Item 8, “Financial Statements and Supplementary Data,” under the caption “Segment Reporting,” which is incorporated herein by reference.

6

Item 1A. Risk Factors

We make forward-looking statements in this report, in other materials we file with the SEC or otherwise release to the public and on our website. In addition, our senior management makes forward-looking statements orally to analysts, investors, the media and others. Statements concerning our future operations, prospects, strategies, products, manufacturing facilities, legal proceedings, financial condition, future financial performance (including growth and earnings) and demand for our products and services, and other statements of our plans, beliefs or expectations, including the statements contained in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” regarding net sales, industry conditions, currency translation impacts, market demand, farm incomes, weather conditions, commodity prices, general economic conditions, availability of financing, working capital, capital expenditure and debt service requirements, margins, production volumes, cost reduction initiatives, investments in product development, compliance with financial covenants, support of lenders, recovery of amounts under guarantee, uncertain income tax provisions, funding of our pension and postretirement benefit plans, or realization of net deferred tax assets, are forward-looking statements. The forward-looking statements we make are not guarantees of future performance and are subject to various assumptions, risks and other factors that could cause actual results to differ materially from those suggested by the forward-looking statements. These factors include, among others, those set forth below and in the other documents that we file with the SEC. There also are other factors that we may not describe, generally because we currently do not perceive them to be material, that could cause actual results to differ materially from our expectations.

We expressly disclaim any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Our financial results depend entirely upon the agricultural industry, and factors that adversely affect the agricultural industry generally, including declines in the general economy, increases in farm input costs, weather conditions, lower commodity prices and changes in the availability of financing for our retail customers, will adversely affect us.

Our success depends entirely on the vitality of the agricultural industry. Historically, the agricultural industry, including the agricultural equipment business, has been cyclical and subject to a variety of economic and other factors. Sales of agricultural equipment generally are related to the economic health of the agricultural industry, which is affected by farm income, farm input costs, debt levels and land values, all of which reflect levels of commodity prices, acreage planted, crop yields, agricultural product demand, including crops used as renewable energy sources, government policies and government subsidies. Sales also are influenced by economic conditions, interest rate and exchange rate levels, and the availability of financing for retail customers. Trends in the industry, such as farm consolidations, may affect the agricultural equipment market. In addition, weather conditions, such as floods, heat waves or droughts, and pervasive livestock or crop diseases can affect farmers’ buying decisions. Downturns in the agricultural industry due to these or other factors, which could vary by market, are likely to result in decreases in demand for agricultural equipment, which would adversely affect our sales, growth, results of operations and financial condition. Moreover, the unpredictable nature of many of these factors and the resulting volatility in demand make it difficult for us to accurately predict sales and optimize production. This, in turn, can result in higher costs, including inventory carrying costs and underutilized manufacturing capacity. During previous downturns in the farm sector, we experienced significant and prolonged declines in sales and profitability, and we expect our business to remain subject to similar market fluctuations in the future.

The agricultural equipment industry is highly seasonal, and seasonal fluctuations significantly impact results of operations and cash flows.

The agricultural equipment business is highly seasonal, which causes our quarterly results and our cash flow to fluctuate during the year. Farmers generally purchase agricultural equipment in the Spring and Fall in conjunction with the major planting and harvesting seasons. In addition, the fourth quarter typically is a significant period for retail sales because of our customers’ year-end tax planning considerations, the increase in availability of funds from completed harvests and the timing of dealer incentives. Our net sales and income from operations historically have been the lowest in the first quarter and have increased in subsequent quarters as dealers anticipate increased retail sales in subsequent quarters.

Most of our sales depend on the availability of retail customers obtaining financing, and any disruption in their ability to obtain financing, whether due to economic downturns or otherwise, will result in the sale of fewer products by us. In addition, the collectability of receivables that are created from our sales, as well as from such retail financing, is critical to our business.

Most retail sales of our products are financed, either by AGCO Finance joint ventures or by a bank or other private lender. Our AGCO Finance joint ventures, which are controlled by Rabobank and are dependent upon Rabobank for financing

7

as well, finance approximately 40% of the retail sales of our tractors and combines in the markets where the joint ventures operate. Any difficulty by Rabobank in continuing to provide that financing, or any business decision by Rabobank as the controlling member not to fund the business or particular aspects of it (for example, a particular country or region) would require the joint ventures to find other sources of financing (which may be difficult to obtain) or would require us to find another source of retail financing for our customers, or our customers would be required to utilize other retail financing providers. A result of an economic downturn would be that financing for capital equipment purchases generally would become more difficult or more expensive to obtain. To the extent that financing is not available, or available only at unattractive prices, our sales would be negatively impacted.

Both AGCO and our AGCO Finance joint ventures have substantial accounts receivable from dealers and retail customers, and we would both be adversely impacted if the collectability of these receivables was not consistent with historical experience. This collectability is dependent on the financial strength of the farm industry, which in turn is dependent upon the general economy and commodity prices, as well as several of the other factors discussed in this “Risk Factors” section. In addition, the AGCO Finance joint ventures may experience credit losses that exceed expectations and adversely affect their financial condition and results of operations. The finance joint ventures may also experience residual value losses that exceed expectations caused by lower pricing for used equipment and higher than expected returns at lease maturity. To the extent that defaults and losses are higher than expected, our equity in the net earnings of the finance joint ventures could be less, or there could be losses, which could materially impact our financial results.

Our success depends on the introduction of new products, which requires substantial expenditures.

Our long-term results depend upon our ability to introduce and market new products successfully. The success of our new products will depend on a number of factors, including:

| • | innovation; |

| • | customer acceptance; |

| • | the efficiency of our suppliers in providing component parts and of our manufacturing facilities in producing final products; and |

| • | the performance and quality of our products relative to those of our competitors. |

As both we and our competitors continuously introduce new products or refine versions of existing products, we cannot predict the level of market acceptance or the amount of market share our new products will achieve. We have experienced delays in the introduction of new products in the past, and we cannot provide any assurances that we will not experience delays in the future. Any delays or other problems with our new product launches will adversely affect our operating results. In addition, introducing new products can result in decreases in revenues from our existing products. Consistent with our strategy of offering new products and product refinements, we expect to continue to use a substantial amount of capital for product development and refinement. We may need more funding for product development and refinement than is readily available, which could adversely affect our business, financial condition or results of operations.

Our expansion plans in emerging markets entail significant risks.

Our strategy includes establishing a greater manufacturing and/or marketing presence in emerging markets such as China, Africa and Russia. In addition, we are expanding our use of component suppliers in these markets. As we progress with these efforts, it will involve a significant investment of capital and other resources and entail various risks. These include risks attendant to obtaining necessary governmental approvals and the construction of the facilities in a timely manner and within cost estimates, the establishment of supply channels, the commencement of efficient manufacturing operations, and, ultimately, the acceptance of the products by our customers. While we expect the expansion to be successful, should we encounter difficulties involving these or similar factors, it may not be as successful as we anticipate.

We face significant competition and if we are unable to compete successfully against other agricultural equipment manufacturers, we would lose customers and our net sales and profitability would decline.

The agricultural equipment business is highly competitive, particularly in our major markets. Our two key competitors, Deere & Company and CNH Industrial N.V., are substantially larger than we are and have greater financial and other resources. In addition, in some markets, we compete with smaller regional competitors with significant market share in a single country or group of countries. Our competitors may substantially increase the resources devoted to the development and marketing, including discounting, of products that compete with our products. In addition, competitive pressures in the

8

agricultural equipment business may affect the market prices of new and used equipment, which, in turn, may adversely affect our sales margins and results of operations.

We maintain an independent dealer and distribution network in the markets where we sell products. The financial and operational capabilities of our dealers and distributors are critical to our ability to compete in these markets. In addition, we compete with other manufacturers of agricultural equipment for dealers. If we are unable to compete successfully against other agricultural equipment manufacturers, we could lose dealers and their end customers and our net sales and profitability may decline.

Rationalization or restructuring of manufacturing facilities, and plant expansions and system upgrades at our manufacturing facilities, may cause production capacity constraints and inventory fluctuations.

The rationalization of our manufacturing facilities has at times resulted in, and similar rationalizations or restructurings in the future may result in temporary constraints upon our ability to produce the quantity of products necessary to fill orders and thereby complete sales in a timely manner. In addition, system upgrades at our manufacturing facilities that impact ordering, production scheduling and other related manufacturing processes are complex, and could impact or delay production targets. A prolonged delay in our ability to fill orders on a timely basis could affect customer demand for our products and increase the size of our product inventories, causing future reductions in our manufacturing schedules and adversely affecting our results of operations. Moreover, our continuous development and production of new products often involves the retooling of existing manufacturing facilities. This retooling may limit our production capacity at certain times in the future, which could adversely affect our results of operations and financial condition. In addition, the expansion and reconfiguration of existing manufacturing facilities, as well as the start up of new manufacturing operations in emerging markets, such as China and Russia, could increase the risk of production delays, as well as require significant investments of capital.

We depend on suppliers for components, parts and raw materials for our products, and any failure by our suppliers to provide products as needed, or by us to promptly address supplier issues, will adversely impact our ability to timely and efficiently manufacture and sell products. We also are subject to raw material price fluctuations, which can adversely affect our manufacturing costs.

Our products include components and parts manufactured by others. As a result, our ability to timely and efficiently manufacture existing products, to introduce new products and to shift manufacturing of products from one facility to another depends on the quality of these components and parts and the timeliness of their delivery to our facilities. At any particular time, we depend on many different suppliers, and the failure by one or more of our suppliers to perform as needed will result in fewer products being manufactured, shipped and sold. If the quality of the components or parts provided by our suppliers is less than required and we do not recognize that failure prior to the shipment of our products, we will incur higher warranty costs. The timely supply of component parts for our products also depends on our ability to manage our relationships with suppliers, to identify and replace suppliers that fail to meet our schedules or quality standards, and to monitor the flow of components and accurately project our needs. The shift from our existing suppliers to new suppliers, including suppliers in emerging markets in the future, also may impact the quality and efficiency of our manufacturing capabilities, as well as impact warranty costs. A significant increase in the price of any component or raw material could adversely affect our profitability. We cannot avoid exposure to global price fluctuations, such as occurred in the past with the costs of steel and related products, and our profitability depends on, among other things, our ability to raise equipment and parts prices sufficient enough to recover any such material or component cost increases.

A majority of our sales and manufacturing take place outside the United States, and, as a result, we are exposed to risks related to foreign laws, taxes, economic conditions, labor supply and relations, political conditions and governmental policies as well as U.S. laws governing who we sell to and how we conduct business. These risks may delay or reduce our realization of value from our international operations.

A majority of our sales are derived from sales outside the United States. The foreign countries in which we do the most significant amount of business are Germany, France, Brazil, the United Kingdom, Finland and Canada. In addition, we have significant manufacturing operations in France, Germany, Brazil, Italy and Finland and have established manufacturing operations in emerging markets, such as China. Many of our sales involve products that are manufactured in one country and sold in a different country and therefore, our results of operations and financial condition will be adversely affected by adverse changes in laws, taxes and tariffs, trade restrictions, economic conditions, labor supply and relations, political conditions and governmental policies of the countries in which we conduct business. Our business practices in these foreign countries must comply with U.S. law, including limitations on where and to whom we may sell products and the Foreign Corrupt Practices Act (“FCPA”). We have a compliance program in place designed to reduce the likelihood of potential violations of these laws, but

9

we cannot provide assurances that past violations have not occurred or that future violations will not occur. Significant violations could subject us to fines and other penalties as well as increased compliance costs. Some of our international operations also are, or might become, subject to various risks that are not present in domestic operations, including restrictions on dividends and the repatriation of funds. Foreign developing markets may present special risks, such as unavailability of financing, inflation, slow economic growth, price controls and difficulties in complying with U.S. regulations.

Domestic and foreign political developments and government regulations and policies directly affect the international agricultural industry, which affects the demand for agricultural equipment. If demand for agricultural equipment declines, our sales, growth, results of operations and financial condition will be adversely affected. The application, modification or adoption of laws, regulations, trade agreements or policies adversely affecting the agricultural industry, including the imposition of import and export duties and quotas, expropriation and potentially burdensome taxation, could have an adverse effect on our business. The ability of our international customers to operate their businesses and the health of the agricultural industry, in general, are affected by domestic and foreign government programs that provide economic support to farmers. As a result, farm income levels and the ability of farmers to obtain advantageous financing and other protections would be reduced to the extent that any such programs are curtailed or eliminated. Any such reductions likely would result in a decrease in demand for agricultural equipment. For example, a decrease or elimination of current price protections for commodities or of subsidy payments for farmers in the European Union, the United States, Brazil or elsewhere in South America could negatively impact the operations of farmers in those regions, and, as a result, our sales may decline if these farmers delay, reduce or cancel purchases of our products. In emerging markets, some of these (and other) risks can be greater than they might be elsewhere. In addition, in some cases, the financing provided by our joint ventures with Rabobank or by others is supported by a government subsidy or guarantee. The programs under which those subsidies and guarantees are provided generally are of limited duration and subject to renewal and contain various caps and other limitations. In some markets, for example Brazil, this support is quite significant. In the event the governments that provide this support elect not to renew these programs, and were financing not available on reasonable terms, whether through our joint ventures or otherwise, our sales would be negatively impacted.

As a result of the multinational nature of our business and the acquisitions that we have made over time, our corporate and tax structures are complex, with a significant portion of our operations being held through foreign holding companies. As a result, it can be inefficient, from a tax perspective, for us to repatriate or otherwise transfer funds, and we may be subject to a greater level of tax-related regulation and reviews by multiple governmental units than would companies with a more simplified structure. In addition, our foreign and U.S. operations routinely sell products to, and license technology to other operations of ours. The pricing of these intra-company transactions is subject to regulation and review as well. While we make every effort to comply with all applicable tax laws, audits and other reviews by governmental units could result in our being required to pay additional taxes, interest and penalties.

On June 23, 2016, the U.K. held a referendum in which voters approved an exit from the E.U., commonly referred to as “Brexit.” As a result of the referendum, it is expected that the British government will negotiate the terms of the U.K.’s future relationship with the E.U. Although it is unknown what those terms will be, it is possible that there will be greater restrictions on imports and exports between the U.K. and E.U. countries, increased regulatory complexities, and increased currency volatility, any of which could adversely affect our operations and financial results.

We can experience substantial and sustained volatility with respect to currency exchange rate and interest rate changes, which can adversely affect our reported results of operations and the competitiveness of our products.

We conduct operations in a variety of currencies. Our production costs, profit margins and competitive position are affected by the strength of the currencies in countries where we manufacture or purchase goods relative to the strength of the currencies in countries where our products are sold. In addition, we are subject to currency exchange rate risk to the extent that our costs are denominated in currencies other than those in which we denominate sales and to risks associated with translating the financial statements of our foreign subsidiaries from local currencies into United States dollars. Similarly, changes in interest rates affect our results of operations by increasing or decreasing borrowing costs and finance income. Our most significant transactional foreign currency exposures are the Euro, the Brazilian real and the Canadian dollar in relation to the United States dollar, and the Euro in relation to the British pound. Where naturally offsetting currency positions do not occur, we attempt to manage these risks by economically hedging some, but not necessarily all, of our exposures through the use of foreign currency forward exchange or option contracts. As with all hedging instruments, there are risks associated with the use of foreign currency forward exchange or option contracts, interest rate swap agreements and other risk management contracts. While the use of such hedging instruments provides us with protection for a finite period of time from certain fluctuations in currency exchange and interest rates, when we hedge we forego part or all the benefits that might result from favorable fluctuations in currency exchange and interest rates. In addition, any default by the counterparties to these transactions could

10

adversely affect us. Despite our use of economic hedging transactions, currency exchange rate or interest rate fluctuations may adversely affect our results of operations, cash flow and financial condition.

We are subject to extensive environmental laws and regulations, including increasingly stringent engine emissions standards, and our compliance with, or our failure to comply with, existing or future laws and regulations could delay production of our products or otherwise adversely affect our business.

We are subject to increasingly stringent environmental laws and regulations in the countries in which we operate. These regulations govern, among other things, emissions into the air, discharges into water, the use, handling and disposal of hazardous substances, waste disposal and the remediation of soil and groundwater contamination. Our costs of complying with these or any other current or future environmental regulations may be significant. For example, several countries have adopted more stringent environmental regulations regarding emissions into the air, and it is possible that new emissions-related legislation or regulations will be adopted in connection with concerns regarding greenhouse gases. In addition, we may be subject to liability in connection with properties and businesses that we no longer own or operate. We may be adversely impacted by costs, liabilities or claims with respect to our operations under existing laws or those that may be adopted in the future that could apply to both future and prior conduct. If we fail to comply with existing or future laws and regulations, we may be subject to governmental or judicial fines or sanctions, or we may not be able to sell our products and, therefore, our business and results of operations could be adversely affected.

In addition, the products that we manufacture or sell, particularly engines, are subject to increasingly stringent environmental regulations. As a result, on an ongoing basis we incur significant engineering expenses and capital expenditures to modify our products to comply with these regulations. Further, we may experience production delays if we or our suppliers are unable to design and manufacture components for our products that comply with environmental standards. For instance, as we are required to meet more stringent engine emission reduction standards that are applicable to engines we manufacture or incorporate into our products, we expect to meet these requirements through the introduction of new technology to our products, engines and exhaust after-treatment systems, as necessary. Failure to meet such requirements could materially affect our business and results of operations.

We are subject to SEC disclosure obligations relating to “conflict minerals” (columbite-tantalite, cassiterite (tin), wolframite (tungsten) and gold) that are sourced from the Democratic Republic of Congo or adjacent countries. Complying with these requirements has and will require us to incur additional costs, including the costs to determine the sources of any conflict minerals used in our products and to modify our processes or products, if required. As a result, we may choose to modify the sourcing, supply and pricing of materials in our products. In addition, we may face reputational and regulatory risks if the information that we receive from our suppliers is inaccurate or inadequate, or our process in obtaining that information does not fulfill the SEC’s requirements. We have a formal policy with respect to the use of conflict minerals in our products that is intended to minimize, if not eliminate, conflict minerals sourced from the covered countries to the extent that we are unable to document that they have been obtained from conflict-free sources.

Our labor force is heavily unionized, and our contractual and legal obligations under collective bargaining agreements and labor laws subject us to the risks of work interruption or stoppage and could cause our costs to be higher.

Most of our employees, most notably at our manufacturing facilities, are subject to collective bargaining agreements and union contracts with terms that expire on varying dates. Several of our collective bargaining agreements and union contracts are of limited duration and, therefore, must be re-negotiated frequently. As a result, we incur various administrative expenses associated with union representation of our employees. Furthermore, we are at greater risk of work interruptions or stoppages than non-unionized companies, and any work interruption or stoppage could significantly impact the volume of products we have available for sale. In addition, collective bargaining agreements, union contracts and labor laws may impair our ability to reduce our labor costs by streamlining existing manufacturing facilities or restructuring our business because of limitations on personnel and salary changes and similar restrictions.

We have significant pension obligations with respect to our employees and our available cash flow may be adversely affected in the event that payments became due under any pension plans that are unfunded or underfunded. Declines in the market value of the securities used to fund these obligations result in increased pension expense in future periods.

A portion of our active and retired employees participate in defined benefit pension plans under which we are obligated to provide prescribed levels of benefits regardless of the value of the underlying assets, if any, of the applicable pension plan. To the extent that our obligations under a plan are unfunded or underfunded, we will have to use cash flow from operations and other sources to pay our obligations either as they become due or over some shorter funding period. In addition, since the assets that we already have provided to fund these obligations are invested in debt instruments and other securities,

11

the value of these assets varies due to market factors. Historically, these fluctuations have been significant and sometimes adverse, and there can be no assurances that they will not be significant in the future. We are also subject to laws and regulations governing the administration of our pension plans in certain countries, and the specific provisions, benefit formulas and related interpretations of such laws, regulations and provisions can be complex. Failure to properly administer the provisions of our pension plans and comply with applicable laws and regulations could have an adverse impact to our results of operations. As of December 31, 2017, we had substantial unfunded or underfunded obligations related to our pension and other postretirement health care benefits. See the notes to our Consolidated Financial Statements contained in Item 8 for more information regarding our unfunded or underfunded obligations.

Our business routinely is subject to claims and legal actions, some of which could be material.

We routinely are a party to claims and legal actions incidental to our business. These include claims for personal injuries by users of farm equipment, disputes with distributors, vendors and others with respect to commercial matters, and disputes with taxing and other governmental authorities regarding the conduct of our business. While these matters generally are not material, it is entirely possible that a matter will arise that is material to our business.

In addition, we use a broad range of technology in our products. We developed some of this technology, we license some of this technology from others, and some of the technology is embedded in the components that we purchase from suppliers. From time-to-time, third parties make claims that the technology that we use violates their patent rights. While to date none of these claims have been significant, we cannot provide any assurances that there will not be significant claims in the future or that currently existing claims will not prove to be more significant than anticipated.

We have a substantial amount of indebtedness, and, as a result, we are subject to certain restrictive covenants and payment obligations that may adversely affect our ability to operate and expand our business.

Our credit facility and certain other debt agreements have various financial and other covenants that require us to maintain certain total debt to EBITDA and interest coverage ratios. In addition, the credit facility and certain other debt agreements contain other restrictive covenants such as the incurrence of indebtedness and the making of certain payments, including dividends, and are subject to acceleration in the event of default. If we fail to comply with these covenants and are unable to obtain a waiver or amendment, an event of default would result.

If any event of default were to occur, our lenders could, among other things, declare outstanding amounts due and payable, and our cash may become restricted. In addition, an event of default or declaration of acceleration under our credit facility or certain other debt agreements could also result in an event of default under our other financing agreements.

Our substantial indebtedness could have other important adverse consequences such as:

| • | requiring us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, which would reduce the availability of our cash flow to fund future working capital, capital expenditures, acquisitions and other general corporate purposes; |

| • | increasing our vulnerability to general adverse economic and industry conditions; |

| • | limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| • | restricting us from being able to introduce new products or pursuing business opportunities; |

| • | placing us at a competitive disadvantage compared to our competitors that may have less indebtedness; and |

| • | limiting, along with the financial and other restrictive covenants in our indebtedness, among other things, our ability to borrow additional funds, pay cash dividends or engage in or enter into certain transactions. |

Our business increasingly is subject to regulations relating to privacy and data protection, and if we violate any of those regulations or otherwise are the victim of a cyber attack, we could incur significant losses and liability.

Increasingly the United States, the European Union and other governmental entities are imposing regulations designed to protect the collection, maintenance and transfer of personal information. For example, the European Union adopted the General Data Protection Regulation (the “GDPR”) that will impose more stringent data protection requirements and greater penalties for non-compliance beginning in May 2018. The GDPR also protects a broader set of personal information than traditionally has been protected and provides for a right of “erasure.” Other regulations govern the collection and transfer of financial data and data security generally. These regulations generally impose penalties in the event of violations. As a result, we could be subject to cyber attacks that, if successful, could compromise our information technology systems and our ability

12

to conduct business. While we attempt to comply with all applicable cybersecurity regulations, their implementation is complex, and, if we are not successful, we may be subject to penalties and claims for damages from the impacted individuals.

In addition, our business relies on the Internet as well as other electronic communications systems that, by their nature, may be subject to efforts by so-called “hackers” to either disrupt our business or steal data or funds. While we strive to maintain customary protections against hackers, there can be no assurance that at some point a hacker will not breach those safeguards and damage our business, possibly materially. These damages could take many forms, including the interruption of our business, the loss of important data, and damage to our reputation.

We may encounter difficulties in integrating businesses we acquire and may not fully achieve, or achieve within a reasonable time frame, expected strategic objectives and other expected benefits of the acquisitions.

From time-to-time we seek to expand through acquisitions of other businesses. We expect to realize strategic and other benefits as a result of our acquisitions, including, among other things, the opportunity to extend our reach in the agricultural industry and provide our customers with an even wider range of products and services. However, it is impossible to predict with certainty whether, or to what extent, these benefits will be realized or whether we will be able to integrate acquired businesses in a timely and effective manner. For example:

| • | the costs of integrating acquired businesses and their operations may be higher than we expect and may require significant attention from our management; |

| • | the businesses we acquire may have undisclosed liabilities, such as environmental liabilities or liabilities for violations of laws, such as the FCPA, that we did not expect; and |

| • | our ability to successfully carry out our growth strategies for acquired businesses will be affected by, among other things, our ability to maintain and enhance our relationships with their existing customers, our ability to provide additional product distribution opportunities to them through our existing distribution channels, changes in the spending patterns and preferences of customers and potential customers, fluctuating economic and competitive conditions and our ability to retain their key personnel. |

Our ability to address these issues will determine the extent to which we are able to successfully integrate, develop and grow acquired businesses and to realize the expected benefits of these transactions. Our failure to do so could have a material adverse effect on our revenues, operating results and financial condition following the transactions.

Changes to United States tax, tariff and import/export regulations may have a negative effect on global economic conditions, financial markets and our business.

There have been ongoing discussions and commentary regarding potential significant changes to United States trade policies, treaties, tariffs and taxes. Although it changes from period to period, we generally have substantial imports into the United States of products and components that are either produced in our foreign locations or are purchased from foreign suppliers, and also have substantial exports of products and components that we manufacture in the United States. The impact of any changes to current trade, tariff or tax policies relating to imports and exports of goods is dependent on factors such as the treatment of exports as a credit to imports, and the introduction of any tariffs or taxes relating to imports from specific countries. It is unclear what changes might be considered or implemented and what response to any such changes may be by the governments of other countries. Any changes that increase the cost of international trade or otherwise impact the global economy could have a material adverse effect our business, financial condition and results of operations.

On December 22, 2017, the Tax Cuts and Jobs Act (the “2017 Tax Act”) was enacted in the United States. The 2017 Tax Act includes a number of changes to existing U.S. tax laws that impact us, including a reduction of the U.S. corporate income tax rate from 35 percent to 21 percent for tax years beginning after December 31, 2017. The 2017 Tax Act also provides for a one-time transition tax on certain foreign earnings and the acceleration of depreciation for certain assets placed into service after September 27, 2017, as well as prospective changes beginning in 2018, including the repeal of the domestic manufacturing deduction, capitalization of research and development expenditures, additional limitations on executive compensation and limitations on the deductibility of interest. Our Consolidated Financial Statements reflect both the income tax effects of the 2017 Tax Act for which the accounting is complete as well as provisional amounts for those specific income tax effects of the 2017 Tax Act for which the accounting is incomplete but a reasonable estimate could be determined. The final impact of the tax reform legislation may differ materially due to factors such as further refinement of our calculations, changes in interpretations and assumptions that we and our advisors have made, additional guidance that may be issued in the future by the U.S. government, and actions that the we may take as a result of the tax reform legislation. When more guidance and interpretations are released, specifically with respect to the transition tax and future repatriation of foreign earnings to the U.S.,

13

the Company will complete its accounting and revise any provisional estimates, if required. Future tax changes and interpretations could be adverse to our business or operations, such as new or additional taxes imposed on earnings and/or reinvested earnings of our foreign subsidiaries. The aggregate impact of such legislation could have a material adverse impact on our cash flows and results of operations.

Item 1B. Unresolved Staff Comments

Not applicable.

14

Item 2. Properties

Our principal manufacturing locations and/or properties as of January 31, 2018, were as follows:

| Location | Description of Property | Leased (Sq. Ft.) | Owned (Sq. Ft.) | |||||

| United States: | ||||||||

| Assumption, Illinois | Manufacturing/Sales and Administrative Office | 933,900 | ||||||

| Batavia, Illinois | Parts Distribution | 310,200 | ||||||

| Duluth, Georgia | Corporate Headquarters | 159,000 | ||||||

| Hesston, Kansas | Manufacturing | 1,461,800 | ||||||

| Jackson, Minnesota | Manufacturing | 51,400 | 986,400 | |||||

| International: | ||||||||

Beauvais, France(1) | Manufacturing | 14,300 | 1,566,600 | |||||

| Breganze, Italy | Manufacturing | 1,562,000 | ||||||

| Ennery, France | Parts Distribution | 700,000 | 360,300 | |||||

| Linnavuori, Finland | Manufacturing | 16,600 | 396,300 | |||||

| Hohenmölsen, Germany | Manufacturing | 437,000 | ||||||

| Marktoberdorf, Germany | Manufacturing | 159,000 | 1,472,200 | |||||

| Wolfenbüttel, Germany | Manufacturing | 538,200 | ||||||

| Stockerau, Austria | Manufacturing | 160,700 | ||||||

| Biatorbagy, Hungary | Manufacturing | 224,500 | ||||||

| Thisted, Denmark | Manufacturing | 133,200 | 295,300 | |||||

| Suolahti, Finland | Manufacturing/Parts Distribution | 48,100 | 553,000 | |||||

| Canoas, Brazil | Regional Headquarters/Manufacturing | 1,120,000 | ||||||

| Mogi das Cruzes, Brazil | Manufacturing | 727,200 | ||||||

| Santa Rosa, Brazil | Manufacturing | 508,900 | ||||||

| Changzhou, China | Manufacturing | 241,100 | 767,000 | |||||

_______________________________________

| (1) | Includes our joint venture, GIMA, in which we own a 50% interest. |

We consider each of our facilities to be in good condition and adequate for its present use. We believe that we have sufficient capacity to meet our current and anticipated manufacturing requirements.

15

Item 3. Legal Proceedings

The Environmental Protection Agency of Victoria, Australia issued a notice to our Australian subsidiary regarding remediation of contamination of a property located in a suburb of Melbourne, Australia. The property was owned and divested by our subsidiary before our subsidiary was acquired by us. Our Australian subsidiary is in correspondence with the Environmental Protection Agency concerning the notice. At this time, we are not able to determine whether our subsidiary might have any liability or the nature and cost of any possible required remediation.

In August 2008, as part of a routine audit, the Brazilian taxing authorities disallowed deductions relating to the amortization of certain goodwill recognized in connection with a reorganization of our Brazilian operations and the related transfer of certain assets to our Brazilian subsidiaries. The amount of the tax disallowance through December 31, 2017, not including interest and penalties, was approximately 131.5 million Brazilian reais (or approximately $39.7 million). The amount ultimately in dispute will be significantly greater because of interest and penalties. We have been advised by our legal and tax advisors that our position with respect to the deductions is allowable under the tax laws of Brazil. We are contesting the disallowance and believe that it is not likely that the assessment, interest or penalties will be required to be paid. However, the ultimate outcome will not be determined until the Brazilian tax appeal process is complete, which could take several years.

We are a party to various other legal claims and actions incidental to our business. We believe that none of these claims or actions, either individually or in the aggregate, is material to our business or financial statements as a whole, including our results of operations and financial condition.

Item 4. Mine Safety Disclosures

Not Applicable.

16

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is listed on the New York Stock Exchange (“NYSE”) and trades under the symbol AGCO. As of the close of business on February 23, 2018, the closing stock price was $68.44, and there were 315 stockholders of record (this number does not include stockholders who hold their stock through brokers, banks and other nominees). The following table sets forth, for the periods indicated, the high and low sales prices for our common stock for each quarter within the last two years, as reported on the NYSE, as well as the amount of the dividend paid.

| High | Low | Dividend | |||||||||

| 2017 | |||||||||||

| First Quarter | $ | 64.90 | $ | 57.76 | $ | 0.14 | |||||

| Second Quarter | 68.04 | 58.01 | 0.14 | ||||||||

| Third Quarter | 74.40 | 64.36 | 0.14 | ||||||||

| Fourth Quarter | 75.95 | 65.30 | 0.14 | ||||||||

| High | Low | Dividend | |||||||||

| 2016 | |||||||||||

| First Quarter | $ | 53.35 | $ | 42.40 | $ | 0.13 | |||||

| Second Quarter | 56.00 | 44.68 | 0.13 | ||||||||

| Third Quarter | 50.21 | 45.47 | 0.13 | ||||||||

| Fourth Quarter | 61.22 | 48.78 | 0.13 | ||||||||

Dividend Policy

On January 25, 2018, our Board of Directors approved an increase in our quarterly dividend from $0.14 per share to $0.15 per share beginning in the first quarter of 2018. Future dividends will be subject to our Board of Directors’ approval. We cannot provide any assurance that we will continue to pay dividends in the future. Although we are in compliance with all provisions of our debt agreements, our credit facility and senior term loans contain restrictions on our ability to pay dividends in certain circumstances. Refer to Note 9 of our Consolidated Financial Statements for further information.

17

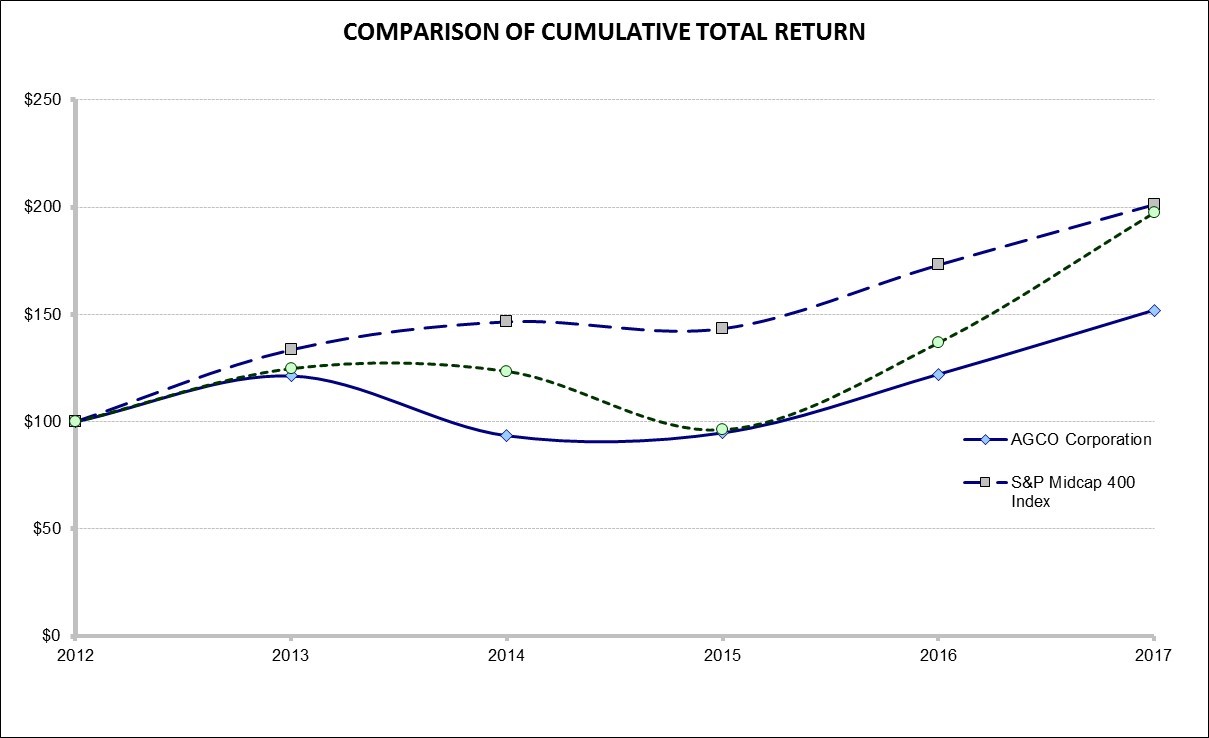

Performance Graph

The following presentation is a line graph of our cumulative total shareholder return on our common stock on an indexed basis as compared to the cumulative total return of the S&P Mid-Cap 400 Index and a self-constructed peer group (“Peer Group”) for the five years ended December 31, 2017. Our total returns in the graph are not necessarily indicative of future performance.

| Cumulative Total Return for the Years Ended December 31 | ||||||||||||||||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |||||||||||||||||||

| AGCO Corporation | $ | 100.00 | $ | 121.36 | $ | 93.50 | $ | 94.80 | $ | 122.12 | $ | 152.04 | ||||||||||||

| S&P Midcap 400 Index | 100.00 | 133.50 | 146.54 | 143.35 | 173.08 | 201.20 | ||||||||||||||||||

| Peer Group Index | 100.00 | 124.92 | 124.30 | 96.34 | 137.24 | 198.60 | ||||||||||||||||||

The total return assumes that dividends were reinvested and is based on a $100 investment on December 31, 2012.

The Peer Group Index is a self-constructed peer group of companies that includes: Caterpillar Inc., CNH Industrial NV, Cummins Inc., Deere & Company, Eaton Corporation Plc., Ingersoll-Rand Plc., Navistar International Corporation, PACCAR Inc., Parker-Hannifin Corporation and Terex Corporation.

18

Item 6. Selected Financial Data

The following tables present our selected consolidated financial data. The data set forth below should be read together with Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our historical Consolidated Financial Statements and the related notes. The Consolidated Financial Statements as of December 31, 2017 and 2016 and for the years ended December 31, 2017, 2016 and 2015 and the reports thereon are included in Item 8, “Financial Statements and Supplementary Data.” The historical financial data may not be indicative of our future performance.

| Years Ended December 31, | ||||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| (In millions, except per share data) | ||||||||||||||||||||

| Operating Data: | ||||||||||||||||||||

| Net sales | $ | 8,306.5 | $ | 7,410.5 | $ | 7,467.3 | $ | 9,723.7 | $ | 10,786.9 | ||||||||||

| Gross profit | 1,765.3 | 1,515.5 | 1,560.6 | 2,066.3 | 2,390.6 | |||||||||||||||

| Income from operations | 403.3 | 288.4 | 361.1 | 646.5 | 900.7 | |||||||||||||||

| Net income | 189.3 | 160.2 | 264.0 | 404.2 | 592.3 | |||||||||||||||

| Net (income) loss attributable to noncontrolling interests | (2.9 | ) | (0.1 | ) | 2.4 | 6.2 | 4.9 | |||||||||||||

| Net income attributable to AGCO Corporation and subsidiaries | $ | 186.4 | $ | 160.1 | $ | 266.4 | $ | 410.4 | $ | 597.2 | ||||||||||

| Net income per common share — diluted | $ | 2.32 | $ | 1.96 | $ | 3.06 | $ | 4.36 | $ | 6.01 | ||||||||||

| Cash dividends declared and paid per common share | $ | 0.56 | $ | 0.52 | $ | 0.48 | $ | 0.44 | $ | 0.40 | ||||||||||

| Weighted average shares outstanding — diluted | 80.2 | 81.7 | 87.1 | 94.2 | 99.4 | |||||||||||||||

| As of December 31, | ||||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||

| (In millions, except number of employees) | ||||||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 367.7 | $ | 429.7 | $ | 426.7 | $ | 363.7 | $ | 1,047.2 | ||||||||||

| Total assets | 7,971.7 | 7,168.4 | 6,497.7 | 7,364.5 | 8,390.2 | |||||||||||||||

| Total long-term debt, excluding current portion and debt issuance costs | 1,618.1 | 1,610.0 | 925.2 | 993.3 | 932.9 | |||||||||||||||

| Stockholders’ equity | 3,095.3 | 2,837.2 | 2,883.3 | 3,496.9 | 4,044.8 | |||||||||||||||

| Other Data: | ||||||||||||||||||||

| Number of employees | 20,462 | 19,795 | 19,588 | 20,828 | 22,111 | |||||||||||||||

19

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

We are a leading manufacturer and distributor of agricultural equipment and related replacement parts throughout the world. We sell a full range of agricultural equipment, including tractors, combines, self-propelled sprayers, hay tools, forage equipment, seeding and tillage equipment, implements, and grain storage and protein production systems. Our products are widely recognized in the agricultural equipment industry and are marketed under a number of well-known brand names, including: Challenger®, Fendt®, GSI®, Massey Ferguson® and Valtra®. We distribute most of our products through a combination of approximately 4,200 dealers and distributors as well as associates and licensees. In addition, we provide retail financing through our finance joint ventures with Rabobank.

Financial Highlights

We sell our equipment and replacement parts to our independent dealers, distributors and other customers. A large majority of our sales are to independent dealers and distributors that sell our products to end users. To the extent practicable, we attempt to sell products to our dealers and distributors on a level basis throughout the year to reduce the effect of seasonal demands on our manufacturing operations and to minimize our investment in inventories. However, retail sales by dealers to farmers are highly seasonal and are linked to the planting and harvesting seasons. In certain markets, particularly in North America, there is often a time lag, which varies based on the timing and level of retail demand, between our sale of the equipment to the dealer and the dealer’s sale to a retail customer.

The following table sets forth, for the periods indicated, the percentage relationship to net sales of certain items included in our Consolidated Statements of Operations:

| Years Ended December 31, | ||||||||

2017 (1) | 2016 (1) | 2015 (1) | ||||||

| Net sales | 100.0 | % | 100.0 | % | 100.0 | % | ||

| Cost of goods sold | 78.7 | 79.5 | 79.1 | |||||

| Gross profit | 21.3 | 20.5 | 20.9 | |||||

| Selling, general and administrative expenses | 11.7 | 11.7 | 11.4 | |||||

| Engineering expenses | 3.9 | 4.0 | 3.8 | |||||

| Restructuring expenses | 0.1 | 0.2 | 0.3 | |||||

| Amortization of intangibles | 0.7 | 0.7 | 0.6 | |||||

| Income from operations | 4.9 | 3.9 | 4.8 | |||||

| Interest expense, net | 0.5 | 0.7 | 0.6 | |||||

| Other expense, net | 0.9 | 0.4 | 0.5 | |||||

| Income before income taxes and equity in net earnings of affiliates | 3.4 | 2.8 | 3.7 | |||||

| Income tax provision | 1.6 | 1.2 | 1.0 | |||||

| Income before equity in net earnings of affiliates | 1.8 | 1.5 | 2.8 | |||||

| Equity in net earnings of affiliates | 0.5 | 0.6 | 0.8 | |||||

| Net income | 2.3 | 2.2 | 3.5 | |||||

| Net loss attributable to noncontrolling interests | — | — | — | |||||

| Net income attributable to AGCO Corporation and subsidiaries | 2.3 | % | 2.2 | % | 3.6 | % | ||

____________________________________

| (1) | Rounding may impact summation of amounts. |

2017 Compared to 2016