UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) |

| OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) |

| OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

| SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) |

| OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number 001-14370

COMPAÑÍA DE MINAS BUENAVENTURA S.A.A.

(Exact name of Registrant as specified in its charter)

BUENAVENTURA MINING COMPANY INC.

(Translation of Registrant’s name into English)

REPUBLIC OF PERU

(Jurisdiction of incorporation or organization)

CARLOS VILLARAN 790

SANTA CATALINA, LIMA 13, PERU

(Address of principal executive offices)

Carlos E. Gálvez, Vice President and Chief Financial Officer

Telephone: (511) 419-2540

Facsimile: (511) 471-7349

Address: Carlos Villaran 790, Santa Cataline, Lima 13, Peru

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

Common shares, nominal (par) value of ten Peruvian Nuevos Soles per share | New York Stock Exchange Inc.٭ Lima Stock Exchange | |

American Depositary Shares (ADSs) representing one Common share each | New York Stock Exchange Inc. |

٭ Not for trading but only in connection with the registration of ADSs pursuant to the requirements of the Securities Exchange Commission

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

| Common shares nominal (par) value of S/.10.00 per share | 274,889,924 | * | ||

| Investment shares nominal (par) value of S/.10.00 per share | 744,640 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Board ¨ | Other x |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

TABLE OF CONTENTS

| Page | ||

| INTRODUCTION | 1 | |

| ITEM 1. | Identity of Directors, Senior Management and Advisers | 3 |

| ITEM 2. | Offer Statistics and Expected Timetable | 3 |

| ITEM 3. | Key Information | 3 |

| ITEM 4. | Information on the Company | 24 |

| ITEM 4A. | Unresolved Staff Comments | 100 |

| ITEM 5. | Operating and Financial Review and Prospects | 101 |

| ITEM 6. | Directors, Senior Management and Employees | 149 |

| ITEM 7. | Major Shareholders and Related Party Transactions | 156 |

| ITEM 8. | Financial Information | 158 |

| ITEM 9. | The Offer and Listing | 161 |

| ITEM 10. | Additional Information | 164 |

| ITEM 11. | Quantitative and Qualitative Disclosures About Market Risk | 175 |

| ITEM 12. | Description of Securities Other Than Equity Securities | 176 |

| PART II | ||

| ITEM 13. | Defaults, Dividend Arrearages and Delinquencies | 176 |

| ITEM 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 176 |

| ITEM 15. | Controls and Procedures | 177 |

| ITEM 16A. | Audit Committee Financial Expert | 178 |

| ITEM 16B. | Code of Ethics | 179 |

| ITEM 16C. | Principal Accountant Fees and Services | 179 |

| ITEM 16D. | Exemptions from the Listing Standards for Audit Committees | 180 |

| ITEM 16E. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 180 |

| ITEM 16F. | Change in Registrant’s Certifying Accountant | 180 |

| ITEM 16G. | Corporate Governance | 180 |

| PART III | ||

| ITEM 17. | Financial Statements | 180 |

| ITEM 18. | Financial Statements | 181 |

| ITEM 19. | Exhibits | 182 |

INTRODUCTION

Presentation of Financial Information

As used in this Annual Report on Form 20-F, or Annual Report, unless the context otherwise requires, references to “we,” “us,” “our,” “Company,” “BVN” or “Buenaventura” mean Compañía de Minas Buenaventura S.A.A. and its consolidated subsidiaries. Unless otherwise specified or the context otherwise requires, references to “$”, “US$”, “Dollars” and “U.S. Dollars” are to United States Dollars, and references to “S/.”, “Nuevo Sol” or “Nuevos Soles” are to Peruvian Nuevos Soles, the legal currency of the Republic of Peru, or Peru.

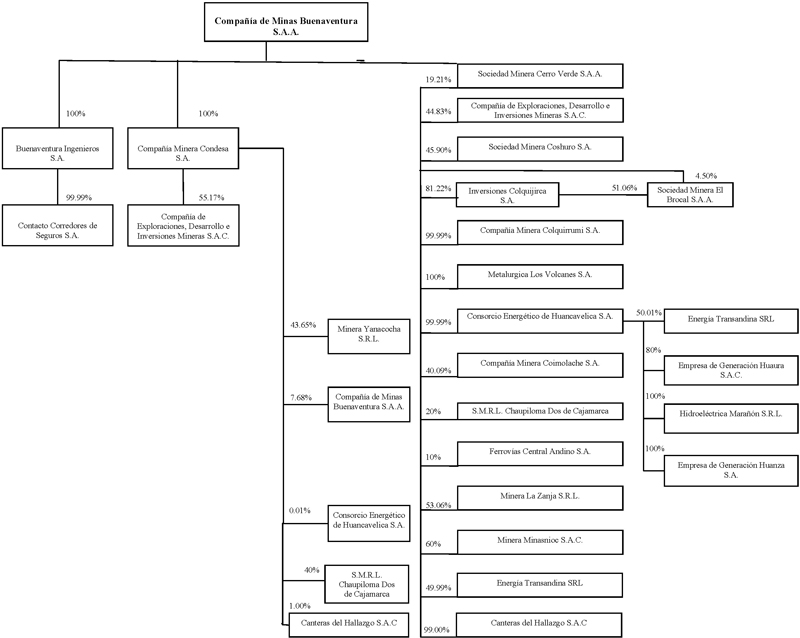

Until December 31, 2005, we and our subsidiaries maintained our financial books and records in Nuevos Soles, the functional and reporting currency until such date. Effective January 1, 2006, we changed our functional and reporting currency from Nuevos Soles to U.S. Dollars. See Note 2.1(f) to our audited consolidated financial statements as of December 31, 2007 and 2008 and for the years ended December 31, 2006, 2007 and 2008, or the Financial Statements, for an explanation of the main reasons supporting this change. We present our consolidated financial statements in conformity with accounting principles generally accepted in Peru, which we refer to as Peruvian GAAP. See Note 33 to the Financial Statements for a description of the significant differences between the accounting principles we follow under Peruvian GAAP and the accounting principles generally accepted in the United States of America, which we refer to as U.S. GAAP, and Note 34 to the Financial Statements for a reconciliation to U.S. GAAP of net income and shareholders’ equity for the periods covered. Pursuant to the rules of the United States Securities and Exchange Commission, or the Commission, this Annual Report includes certain separate financial statements and other financial information of Minera Yanacocha S.R.L., or Yanacocha, and Sociedad Minera Cerro Verde S.A.A., or Cerro Verde. Yanacocha and Cerro Verde maintain their financial books and records in U.S. Dollars and present their financial statements in accordance with U.S. GAAP and Peruvian GAAP, reconciled to U.S. GAAP, respectively.

We record our investments in Yanacocha and Cerro Verde in accordance with the equity method as described in “Item 5. Operating and Financial Review and Prospects—The Company—General” and Note 2.1(e) to the Financial Statements. Our partnership interest in Yanacocha has been calculated at 43.65 percent for the years ended December 31, 2007 and 2008. As of December 31, 2008 and 2007, our equity interest in Cerro Verde was 19.05 and 18.50 percent, respectively.

Exchange Rates

Effective January 1, 2006, our functional and reporting currency changed from the Nuevo Sol to the Dollar. This change resulted from an evaluation of the currency denominations of our cash flows in recent years and, in particular, reflects the increasing significance of dividends from affiliates denominated in Dollars to our financial position, results of operation and cash flows. Profit and loss accounts for year ended December 31, 2005 were translated into Dollars using the average exchange rate of US$1.00 to S/.3.305.

The translation of amounts expressed in nominal or constant Nuevos Soles with purchasing power as of a specified date by the then-prevailing exchange rate may result in presentation of Dollar amounts that differ from the Dollar amounts that would have been obtained by translating nominal or constant Nuevos Soles with purchasing power as of another specified date by the prevailing exchange rate on that specified date. See “Item 3. Key Information—Exchange Rates” for information regarding the average rates of exchange between the Nuevo Sol and the Dollar for the periods specified therein.

1

Certain amounts and percentages have been rounded for presentation purposes and may not sum exactly.

Forward-Looking Statements

Certain statements contained in this Annual Report contain “forward-looking” information (as defined in the U.S. Private Securities Litigation Reform Act of 1995) that involve risks and uncertainties, including those concerning our and Yanacocha’s costs and expenses, results of exploration, the continued improving efficiency of operations, prevailing market prices of gold, silver and other metals mined, the success of joint ventures, estimates of future exploration, production, subsidiaries’ plans for capital expenditures, estimates of reserves and Peruvian political, economic and legal developments. Additional forward-looking statements related to Cerro Verde contained in this Annual Report include those concerning costs and expenses, the continued improving efficiency of operations, prevailing market prices of copper and molybdenum, production and Peruvian political, economic and legal developments. These forward-looking statements reflect our view with respect to our, Yanacocha’s and Cerro Verde’s future financial performance. Actual results could differ materially from those projected in the forward-looking statements as a result of a variety of factors discussed elsewhere in this Annual Report, including but not limited to those discussed under “Item 3. Key Information—Risk Factors.”

2

PART I

| ITEM 1. | Identity of Directors, Senior Management and Advisers |

Not applicable.

| ITEM 2. | Offer Statistics and Expected Timetable |

Not applicable.

| ITEM 3. | Key Information |

Selected Financial Data

Selected Financial Information and Operating Data

The following information should be read in conjunction with, and is qualified in its entirety by reference to, the Financial Statements including the notes thereto appearing elsewhere in this Annual Report. The selected financial information as of December 31, 2007 and 2008, and for the years ended December 31, 2006, 2007 and 2008, is derived from the Financial Statements appearing elsewhere in this Annual Report. The selected financial information as of and for the years ended December 31, 2004 and 2005 has been derived from consolidated financial statements and related notes thereto which are not included in this Annual Report. The report of Medina, Zaldivar, Paredes & Asociados (a member firm of Ernst & Young Global) on our 2007 and 2008 Financial Statements appears elsewhere in this Annual Report. The Financial Statements are prepared and presented in accordance with Peruvian GAAP, which differ in certain respects from U.S. GAAP. Note 33 to the Financial Statements provides a description of the principal differences between Peruvian GAAP and U.S. GAAP as such differences relate to us, and Note 34 to the Financial Statements provides a reconciliation to U.S. GAAP of our net income for the years ended 2006, 2007 and 2008, and shareholders’ equity as of December 31, 2006, 2007 and 2008. The operating data presented below is derived from our records and has not been subject to audit. The financial information and operating data presented below should be read in conjunction with “Item 5. Operating and Financial Review and Prospects—The Company,” the Financial Statements and the related notes thereto and other financial information included in this Annual Report.

3

As of and for the year ended December 31, | ||||||||||||||||||||

2004(2) | 2005(2) | 2006 | 2007 | 2008 | ||||||||||||||||

(In thousands of US$)(1) | ||||||||||||||||||||

| Income statement data: | ||||||||||||||||||||

| Peruvian GAAP | ||||||||||||||||||||

| Net sales of goods and services | 266,405 | 283,387 | 548,072 | 747,021 | 766,603 | |||||||||||||||

| Revenue associated with performance on executory gold delivery contracts | 20,187 | 28,064 | 50,325 | 5,393 | - | |||||||||||||||

| Royalty income | 37,797 | 46,094 | 48,475 | 34,014 | 48,760 | |||||||||||||||

| Total income | 324,389 | 357,545 | 646,872 | 786,428 | 815,363 | |||||||||||||||

| Operating costs: | ||||||||||||||||||||

| Cost of sales, without considering depreciation and amortization | (99,911 | ) | (103,881 | ) | (149,309 | ) | (182,007 | ) | (251,804 | ) | ||||||||||

| Exploration in units in operation | (36,668 | ) | (40,506 | ) | (38,264 | ) | (37,828 | ) | (57,003 | ) | ||||||||||

| Depreciation and amortization | (22,426 | ) | (34,300 | ) | (38,844 | ) | (49,550 | ) | (62,993 | ) | ||||||||||

| Total operating costs | (159,005 | ) | (178,687 | ) | (226,417 | ) | (269,385 | ) | (371,800 | ) | ||||||||||

| Gross income | 165,384 | 178,858 | 420,455 | 517,043 | 443,563 | |||||||||||||||

| Operating expenses: | ||||||||||||||||||||

| General and administrative expenses | (22,833 | ) | (34,350 | ) | (36,639 | ) | (59,205 | ) | (34,907 | ) | ||||||||||

| Exploration in non-operational areas | (25,877 | ) | (27,812 | ) | (36,190 | ) | (46,407 | ) | (55,231 | ) | ||||||||||

| Royalties | (9,254 | ) | (12,209 | ) | (24,420 | ) | (33,978 | ) | (35,694 | ) | ||||||||||

| Provision for impairment of long lived assets | - | - | - | - | (18,610 | ) | ||||||||||||||

| Selling expenses | (5,231 | ) | (4,800 | ) | (5,928 | ) | (10,818 | ) | (15,386 | ) | ||||||||||

| Total operating expenses | (63,195 | ) | (79,171 | ) | (103,177 | ) | (150,408 | ) | (159,828 | ) | ||||||||||

| Operating income before unusual item | 102,189 | 99,687 | 317,278 | 366,635 | 283,735 | |||||||||||||||

| Net loss from release of commitments in commercial contracts | - | - | - | (185,922 | ) | (415,135 | ) | |||||||||||||

| Operating income (loss) after unusual item | 102,189 | 99,687 | 317,278 | 180,713 | (131,400 | ) | ||||||||||||||

| Other income (expenses), net: | ||||||||||||||||||||

| Share in affiliated companies, net | 177,423 | 263,994 | 313,168 | 249,555 | 340,929 | |||||||||||||||

| Interest income | 3,558 | 3,523 | 7,949 | 11,772 | 17,851 | |||||||||||||||

| Gain (loss) on currency exchange difference | (3,706 | ) | 448 | (308 | ) | 5,190 | (12,198 | ) | ||||||||||||

| Gain (loss) on change in the fair value of gold certificates | - | - | (4,861 | ) | 5,126 | - | ||||||||||||||

| Loss from change in the fair value of derivative financial instruments | (17,360 | ) | (26,588 | ) | (13,268 | ) | - | - | ||||||||||||

| Interest expense | (4,273 | ) | (4,060 | ) | (5,948 | ) | (8,614 | ) | (33,934 | ) | ||||||||||

| Loss from exposure to inflation | (2,888 | ) | - | - | - | - | ||||||||||||||

| Other, net | (4,811 | ) | (3,227 | ) | (19,502 | ) | (8,686 | ) | (9,290 | ) | ||||||||||

| Total other income, net | 147,943 | 234,090 | 277,230 | 254,343 | 303,358 | |||||||||||||||

| Income before workers’ profit sharing, income tax and minority interest | 250,132 | 333,777 | 594,508 | 435,056 | 171,958 | |||||||||||||||

| Provision for workers’ profit sharing, net | (5,383 | ) | (2,593 | ) | (14,271 | ) | (19,931 | ) | 4,725 | |||||||||||

| Provision for income tax, net | (29,911 | ) | (22,816 | ) | (64,033 | ) | (43,975 | ) | 26,645 | |||||||||||

| Net income | 214,838 | 308,368 | 516,204 | 371,150 | 203,328 | |||||||||||||||

| Net income attributable to minority interest | (8,261 | ) | (19,971 | ) | (88,147 | ) | (96,389 | ) | (50,045 | ) | ||||||||||

| Net income attributable to Buenaventura | 206,577 | 288,397 | 428,057 | 274,761 | 153,283 | |||||||||||||||

Basic and diluted earnings per share(3) (4) | 0.81 | 1.13 | 1.68 | 1.08 | 0.60 | |||||||||||||||

Basic and diluted earnings per ADS(3)(4) | 0.81 | 1.13 | 1.68 | 1.08 | 0.60 | |||||||||||||||

| Dividends per share | 0.16 | 0.18 | 0.24 | 0.28 | 0.20 | |||||||||||||||

| Average number of shares outstanding | 254,459,688 | 254,459,688 | 254,442,328 | 254,442,328 | 254,442,328 | |||||||||||||||

4

| As of and for the year ended December 31, | ||||||||||||||||||||

2004(2) | 2005(2) | 2006 | 2007 | 2008 | ||||||||||||||||

(In thousands of US$)(1) | ||||||||||||||||||||

| U.S. GAAP | ||||||||||||||||||||

| Operating income (loss) | 96,961 | 97,225 | 302,277 | 345,618 | (122,667 | ) | ||||||||||||||

Net income – restated(5) | 206,685 | 288,488 | 424,697 | 225,458 | 160,170 | |||||||||||||||

Basic and diluted earnings per share – restated(3)(4) | 0.81 | 1.14 | 1.67 | 0.89 | 0.63 | |||||||||||||||

Basic and diluted earnings per ADS– restated(3)(4)(5) | 0.81 | 1.14 | 1.67 | 0.89 | 0.63 | |||||||||||||||

| Balance sheet data: | ||||||||||||||||||||

| Peruvian GAAP | ||||||||||||||||||||

| Total assets | 973,184 | 1,251,122 | 1,735,771 | 1,981,469 | 2,268,298 | |||||||||||||||

| Total debt | 18,803 | 8,517 | 10,606 | 84,119 | 327,295 | |||||||||||||||

| Shareholders’ equity | 587,023 | 862,959 | 1,300,506 | 1,580,216 | 1,728,992 | |||||||||||||||

| U.S. GAAP | ||||||||||||||||||||

Total assets – restated(5) | 972,712 | 1,250,741 | 1,732,030 | 1,972,207 | 2,222,985 | |||||||||||||||

Shareholders’ equity – restated(5) | 574,649 | 839,162 | 1,205,328 | 1,360,984 | 1,486,288 | |||||||||||||||

| Operating data (unaudited): | ||||||||||||||||||||

Production(6) | ||||||||||||||||||||

| Gold (oz.) | 357,562 | 388,042 | 405,383 | 403,955 | 425,257 | |||||||||||||||

| Silver (oz.) | 15,095,562 | 16,429,816 | 22,179,552 | 19,430,511 | 18,606,478 | |||||||||||||||

Proven and probable reserves(7) | ||||||||||||||||||||

| Gold (oz.) | 931,924 | 1,036,543 | 1,032,063 | 1,315,925 | 1,080,506 | |||||||||||||||

| Silver (oz.) | 95,862,405 | 116,452,462 | 117,808,602 | 102,195,344 | 128,431,875 | |||||||||||||||

| (1) | Except per share, per ADS, outstanding shares and operating data. |

| (2) | Until December 31, 2005, our financial books and records were maintained in Nuevos Soles, the functional and reporting currency as of such date. Effective January 1, 2006, we changed the functional and reporting currency from Nuevos Soles to U.S. Dollars. See Note 2.1(f) to the Financial Statements. For comparative purposes, all prior years are presented assuming that U.S. Dollars were used as the reporting currency. |

| (3) | Income per share has been calculated for each year as net income divided by average number of shares outstanding during the year. As of December 31, 2004 and 2005, the total number of Common Shares outstanding was 137,444,962, including 10,585,130 treasury shares, and the total number of Investment Shares outstanding was 372,320, including 15,933 treasury shares. During 2005, we acquired 15,055 Investment Shares that are held as treasury shares. On July 23, 2008, we conducted a two-for-one stock split of our outstanding Common Shares, Investment Shares and ADSs. As a result, we had 274,889,924 outstanding Common Shares, including 21,130,260 treasury shares, and 744,640 outstanding Investment Shares, including 61,976 treasury shares, as of December 31, 2008. In accordance with our accounting policy related to basic and diluted earnings per share, the net income per basic and diluted share has been adjusted retroactively for all periods reported to reflect the stock split. See Note 2.1(x) to the Financial Statements. |

| (4) | We have no outstanding options, warrants or convertible securities that would have a dilutive effect on earnings per share. As a result, there is no difference between basic and diluted earnings per share or ADS. |

| (5) | Net income, total assets and shareholders’ equity for the year ended December 31, 2004 have been adjusted retroactively to comply with APB Opinion No. 18 – The Equity Method of Accounting for Investments in Common Stock, due to the change in the accounting treatment of Cerro Verde’s investment during 2005. |

| (6) | The amounts in this table reflect the total production of all of our consolidated subsidiaries, including El Brocal, in which we owned a 35.78% controlling equity interest as of December 31, 2008. The production data in this table reflects 100% of El Brocal’s production. For the years ended December 31, 2004 to 2008, El Brocal produced 3.4, 4.4, 10.3, 7.1 and 4.6 million ounces of silver, respectively, of which our equity share was 1.1, 1.5, 3.5, 2.4 and 1.7 million ounces of silver. |

| (7) | Proven and probable reserves for our wholly-owned mines as of December 31, 2004, 2005, 2006, 2007 and 2008 were audited by an independent consultant, Algon Investment S.R.L. Proven and probable reserves for El Brocal’s mines as of December 31, 2004, 2005, 2006, 2007 and 2008 were audited by an independent consultant, AMEC plc. |

5

Yanacocha Selected Financial Information and Operating Data

The following table presents selected financial information and operating data for Yanacocha at the dates and for each of the periods indicated. This information should be read in conjunction with, and is qualified in its entirety by reference to, Yanacocha’s audited financial statements as of December 31, 2007 and 2008 and for the years ended December 31, 2006, 2007 and 2008, or the Yanacocha Financial Statements, which Dongo-Soria Gaveglio y Asociados (a member firm of PricewaterhouseCoopers) audited. The report of Dongo-Soria Gaveglio y Asociados on the Yanacocha Financial Statements appears elsewhere in this Annual Report. The selected information as of and for the years ended December 31, 2004 and 2005 has been derived from financial statements and related notes thereto which are not included in this Annual Report. The Yanacocha Financial Statements are prepared and presented in accordance with U.S. GAAP, which differ in certain respects from Peruvian GAAP. The significant differences between U.S. GAAP and Peruvian GAAP applicable to Yanacocha have been quantified in determining Yanacocha’s reported Peruvian GAAP selected financial data. The operating data presented below, which is based on 100 percent of Yanacocha’s production and reserves, is derived from Yanacocha’s records and has not been subject to audit. The financial information presented below should be read in conjunction with “Item 5. Operating and Financial Review and Prospects—Yanacocha,” the Yanacocha Financial Statements and the related notes thereto and other financial information included in this Annual Report.

6

As of and for the year ended December 31, | ||||||||||||||||||||

2004 | 2005 | 2006 | 2007 | 2008 | ||||||||||||||||

(In thousands of US$)(1) | ||||||||||||||||||||

| Income statement data: | ||||||||||||||||||||

| U.S. GAAP | ||||||||||||||||||||

| Revenues | 1,249,882 | 1,490,402 | 1,543,212 | 1,093,347 | 1,612,618 | |||||||||||||||

| Costs and expenses: | ||||||||||||||||||||

| Costs applicable to sales | (450,825 | ) | (507,806 | ) | (468,027 | ) | (506,261 | ) | (659,867 | ) | ||||||||||

| Depreciation, depletion and amortization | (179,441 | ) | (193,587 | ) | (171,730 | ) | (159,148 | ) | (169,131 | ) | ||||||||||

| Exploration costs | (35,236 | ) | (32,884 | ) | (32,254 | ) | (28,234 | ) | (28,151 | ) | ||||||||||

| General and administrative costs | (4,986 | ) | (5,453 | ) | (5,589 | ) | (2,928 | ) | (3,168 | ) | ||||||||||

| Other expenses | (6,135 | ) | 6,669 | (108,646 | ) | (80,941 | ) | (83,424 | ) | |||||||||||

| Total operating expenses | (676,623 | ) | (733,061 | ) | (786,246 | ) | (777,512 | ) | (943,741 | ) | ||||||||||

| Operating income | 573,259 | 757,341 | 756,966 | 315,835 | 668,877 | |||||||||||||||

| Interest expense and other | (1,392 | ) | 3,540 | 6,825 | 12,698 | 3,642 | ||||||||||||||

| Pre-tax income | 571,867 | 760,881 | 763,791 | 328,533 | 672,519 | |||||||||||||||

| Income tax provision | (181,563 | ) | (235,407 | ) | (238,343 | ) | (107,044 | ) | (196,057 | ) | ||||||||||

| Net income before cumulative effect of change in accounting principles | 390,304 | 525,474 | 525,448 | 221,489 | 476,462 | |||||||||||||||

| Cumulative effect of change in accounting principle, net | - | - | - | - | - | |||||||||||||||

| Net income and comprehensive income | 390,304 | 525,474 | 525,448 | 221,489 | 476,462 | |||||||||||||||

| Peruvian GAAP | ||||||||||||||||||||

Revenues(2) | 1,266,550 | 1,527,609 | 1,636,009 | 1,148,546 | 1,641,301 | |||||||||||||||

| Operating income | 605,019 | 675,293 | 886,373 | 379,541 | 709,234 | |||||||||||||||

| Net income | 427,975 | 535,476 | 567,659 | 244,192 | 463,814 | |||||||||||||||

| Balance sheet data: | ||||||||||||||||||||

| U.S. GAAP | ||||||||||||||||||||

| Total assets | 1,207,748 | 1,549,583 | 1,824,853 | 1,895,884 | 1,891,963 | |||||||||||||||

| Total debt | 37,316 | 3,160 | 200,000 | 218,111 | 205,618 | |||||||||||||||

| Partners’ equity | 811,174 | 1,156,648 | 1,196,409 | 1,326,325 | 1,212,787 | |||||||||||||||

| Peruvian GAAP | ||||||||||||||||||||

| Total assets | 1,091,571 | 1,473,255 | 1,823,480 | 1,925,125 | 1,911,583 | |||||||||||||||

| Total debt | 36,553 | 2,850 | 200,000 | 218,111 | 205,618 | |||||||||||||||

| Partners’ equity | 735,203 | 1,090,679 | 1,200,562 | 1,353,180 | 1,226,994 | |||||||||||||||

| Operating data (unaudited): | ||||||||||||||||||||

| Gold produced (oz.) | 3,017,303 | 3,333,088 | 2,612,199 | 1,563,669 | 1,810,338 | |||||||||||||||

| Gold proven and probable reserves (thousands of oz.) | 32,257 | 32,620 | 29,327 | 27,594 | 24,850 | |||||||||||||||

| (1) | Except operating data. |

| (2) | Under U.S. GAAP, Yanacocha recognizes revenues when the price is determinable and upon delivery and transfer of title of gold to the customer. In addition, revenues from silver sales are credited to costs applicable to sales as a by-product credit. Under Peruvian GAAP, revenues, including gold and silver sales, are recognized when doré is delivered to the shipper. |

7

Cerro Verde Selected Financial Information and Operating Data

The following table presents selected financial information and operating data for Cerro Verde at the dates and for each of the periods indicated. This information should be read in conjunction with, and is qualified in its entirety by reference to, Cerro Verde’s audited financial statements as of December 31, 2007 and 2008 and for the years ended December 31, 2006, 2007 and 2008, or the Cerro Verde Financial Statements. Medina, Zaldívar, Paredes & Asociados (a member firm of Ernst & Young Global) audited the Cerro Verde Financial Statements for 2007 and 2008 and the report of Medina, Zaldívar, Paredes & Asociados on Cerro Verde’s financial statements appears elsewhere in this Annual Report. The Cerro Verde Financial Statements for years prior to 2006 were audited by Dongo-Soria Gaveglio y Asociados (a member firm of Pricewaterhouse Coopers). The selected information as of and for the years ended December 31, 2004 and 2005 has been derived from financial statements and related notes thereto which are not included in this Annual Report. The Cerro Verde Financial Statements are prepared and presented in accordance with Peruvian GAAP, which differs in certain respects from U.S. GAAP. Note 26 to the Cerro Verde Financial Statements provides a description of the principal differences between Peruvian GAAP and U.S. GAAP as such differences relate to Cerro Verde, and Note 27 to the Cerro Verde Financial Statements provides a reconciliation to U.S. GAAP of Cerro Verde’s net income for the years ended 2006, 2007 and 2008 and shareholders’ equity as of December 31, 2007 and 2008. The operating data presented below, which is based on 100 percent of Cerro Verde’s production and reserves, is derived from Cerro Verde’s records and has not been subject to audit. The financial information presented below should be read in conjunction with “Item 5. Operating and Financial Review and Prospects—Cerro Verde,” the Cerro Verde Financial Statements and the related notes thereto and other financial information included in this Annual Report.

8

As of and for the year ended December 31, | ||||||||||||||||||||

2004 | 2005 | 2006 | 2007 | 2008 | ||||||||||||||||

(In thousands of US$)(1) | ||||||||||||||||||||

| Income statement data: | ||||||||||||||||||||

| Peruvian GAAP | ||||||||||||||||||||

| Net sales of goods | 260,782 | 358,928 | 667,671 | 1,794,559 | 1,835,911 | |||||||||||||||

| Total revenues | 260,782 | 358,928 | 667,671 | 1,794,559 | 1,835,911 | |||||||||||||||

| Costs of sales | ||||||||||||||||||||

| Total costs of sales | (119,482 | ) | (133,715 | ) | (140,423 | ) | (418,108 | ) | (596,741 | ) | ||||||||||

| Gross margin | 141,300 | 225,213 | 527,248 | 1,376,451 | 1,239,170 | |||||||||||||||

| Operating expenses | ||||||||||||||||||||

| Selling expenses | (1,089 | ) | (1,295 | ) | (3,538 | ) | (54,405 | ) | (78,190 | ) | ||||||||||

| Negotiated payment (Voluntary contribution) | - | - | - | (48,674 | ) | (29,496 | ) | |||||||||||||

| Other operating expenses | - | - | (48,100 | ) | (2,432 | ) | (29,956 | ) | ||||||||||||

| Total operating expenses | (1,089 | ) | (1,295 | ) | (51,638 | ) | (105,511 | ) | (137,642 | ) | ||||||||||

| Operating income | 140,211 | 223,918 | 475,610 | 1,270,940 | 1,101,528 | |||||||||||||||

| Other income (expenses), net | ||||||||||||||||||||

| Financial expense | (1,975 | ) | (14 | ) | (2,984 | ) | (23,346 | ) | (7,853 | ) | ||||||||||

| Financial income | 1,148 | 7,063 | 10,899 | 33,168 | 20,278 | |||||||||||||||

| Other, net | (31 | ) | 169 | (550 | ) | (426 | ) | (2,366 | ) | |||||||||||

| Total other income (expenses), net | (858 | ) | 7,218 | 7,365 | 9,396 | 10,059 | ||||||||||||||

| Profit before workers’ profit sharing and income tax | 139,353 | 231,136 | 482,975 | 1,280,336 | 1,111,587 | |||||||||||||||

| Workers’ profit sharing | (11,502 | ) | (18,578 | ) | (42,805 | ) | (106,846 | ) | (88,349 | ) | ||||||||||

| Income tax | (40,188 | ) | 22,105 | 4,451 | (368,805 | ) | (304,805 | ) | ||||||||||||

| Net income | 87,663 | 234,663 | 444,621 | 804,685 | 718,433 | |||||||||||||||

| Basic and diluted earnings per share | 0.386 | 0.785 | 1.270 | 2.300 | 2.052 | |||||||||||||||

| Dividends per share | 0.066 | 0.492 | - | 1.77 | 2.399 | |||||||||||||||

| Average number of shares outstanding | 227,309,099 | 298,911,465 | 350,056,012 | 350,056,012 | 350,056,012 | |||||||||||||||

| U.S. GAAP | ||||||||||||||||||||

| Operating income (loss) | 141,967 | 224,715 | 476,432 | 1,284,612 | 1,101,528 | |||||||||||||||

| Net income | 88,794 | 235,460 | 445,443 | 573,726 | 718,433 | |||||||||||||||

| Basic and diluted earnings per share | 0.391 | 0.788 | 1.272 | 1.640 | 2.05 | |||||||||||||||

| Balance sheet data: | ||||||||||||||||||||

| Peruvian GAAP | ||||||||||||||||||||

| Total assets | 364,043 | 908,800 | 1,651,256 | 2,035,576 | 1,983,572 | |||||||||||||||

| Total debt | - | 1,906 | 183,667 | 73,764 | - | |||||||||||||||

| Shareholders’ equity | 265,611 | 816,436 | 1,261,057 | 1,445,742 | 1,324,175 | |||||||||||||||

| U.S. GAAP | ||||||||||||||||||||

| Total assets | 347,857 | 893,851 | 1,637,584 | 2,035,576 | 1,983,572 | |||||||||||||||

| Shareholders’ equity | 255,187 | 806,809 | 1,252,252 | 1,205,978 | 1,084,411 | |||||||||||||||

| Operating data (unaudited): | ||||||||||||||||||||

| Production: | ||||||||||||||||||||

| Copper (in thousands of recoverable pounds) | 195,108 | 206,245 | 221,726 | 594,227 | 694,486 | |||||||||||||||

| Proven and probable reserves | ||||||||||||||||||||

| Copper (in thousands of metric tons) | 1,646,742 | 1,594,184 | 1,741,432 | 1,765,634 | 3,022,581 | |||||||||||||||

(1) Except per share and operating data

9

Exchange Rates

The following table sets forth the high and low month-end rates and the average and end-of-period offered rates for the sale of Nuevos Soles in U.S. Dollars for the period indicated, as published by the Superintendencia de Bancos y Seguros (Superintendent of Bank and Insurance, or the SBS). The Federal Reserve Bank of New York does not report a noon buying rate for Nuevos Soles.

Exchange Rates

(Nuevos Soles per US$)(1)

| Year | High(2) | Low(2) | Average(3) | Period end(4) | ||||||||||||

| 2004 | 3.499 | 3.277 | 3.413 | 3.277 | ||||||||||||

| 2005 | 3.427 | 3.253 | 3.303 | 3.427 | ||||||||||||

| 2006 | 3.355 | 3.194 | 3.264 | 3.194 | ||||||||||||

| 2007 | 3.201 | 2.967 | 3.123 | 2.995 | ||||||||||||

| 2008 | 3.141 | 2.690 | 2.922 | 3.139 | ||||||||||||

High(5) | Low(5) | Average(6) | Period end(7) | |||||||||||||

| 2008 | ||||||||||||||||

| December | 3.140 | 3.075 | 3.113 | 3.139 | ||||||||||||

| 2009 | ||||||||||||||||

| January | 3.174 | 3.130 | 3.1504 | 3.174 | ||||||||||||

| February | 3.251 | 3.193 | 3.235 | 3.248 | ||||||||||||

| March | 3.258 | 3.107 | 3.173 | 3.159 | ||||||||||||

| April | 3.146 | 2.989 | 3.083 | 2.989 | ||||||||||||

| May | 3.038 | 2.954 | 2.992 | 2.992 | ||||||||||||

| (1) | Expressed in nominal (not inflation adjusted) Nuevos Soles. |

| (2) | Highest and lowest of the twelve month-end exchange rates for each year based on the offered rate. |

| (3) | Average of month-end exchange rates based on the offered rate. |

| (4) | End of period exchange rates based on the offered rate. |

| (5) | Highest and lowest of the exchange notes based on the offered rate on the last day of each month. |

| (6) | Average of the exchange rates based on the offered rate on the last date of each day in the relevant month. |

| (7) | The exchange rate based on the offered rate on the last day of each relevant month. |

Source: SBS

On June 2, 2009, the offered rate for Dollars as published by the SBS was S/2.967= US$1.00.

Capitalization and Indebtedness

Not applicable.

Reasons for the Offer and Use of Proceeds

Not applicable.

10

Risk Factors

Factors Relating to the Company

Dependence on Mining Exploration Agreements

An integral part of our operations is the participation in mining exploration projects with experienced mining companies. Such projects benefit us by providing a source of outside funds for exploration of mining rights, giving us access to the holdings of outside parties without the risks and costs of outright acquisition. They also enable us to expand the scope of knowledge and experience of our senior management, geologists and engineers through increased contact with their counterparts from other organizations. We can be highly dependent upon our partners, co-venturers or other shareholders in a joint mining exploration project carrying out their obligations under the applicable joint mining exploration agreement or mining operating agreement. Such partners, co-venturers and other shareholders in a joint mining exploration venture may contribute capital to cover the expenses of the joint venture project or provide critical technological expertise and/or management and organizational expertise. See “Item 4. Information on the Company—Yanacocha—Overview” for a description of how we and Newmont Mining Corporation, a Delaware corporation, or Newmont Mining, have joined together to participate in Yanacocha and how Yanacocha is dependent upon Newmont Peru Limited, Peruvian Branch, or Newmont Peru, to provide management and other expertise to the Yanacocha project. If, however, a partner, a co-venturer or in certain cases another shareholder does not carry out its obligations under the applicable joint venture agreement, joint mining operating agreement, by-laws or shareholders agreement, the value of our investment in the joint mining exploration project could be adversely affected and we could incur significant expense in enforcing our rights or pursuing remedies. There can be no assurance that our current or future partners will fulfill their obligations under such agreements. See “Item 4. Information on the Company—Yanacocha” and “Item 4. Information on the Company—The Company—Business Overview—Exploration.”

Investment in International Operations

Foreign operations are subject to certain risks inherent in conducting business abroad, including, among others, exposure to foreign currency fluctuations, devaluations or supply restrictions, exchange control regulations, government policies, price and wage controls, taxation, intervention, social instability and other political, economic or diplomatic developments beyond our control. There can be no assurance that our foreign exploration activities will not be adversely affected in the future.

Prices of Gold, Silver and Copper

Because our revenues are derived primarily from the sale of ore concentrates containing gold and silver, Yanacocha’s revenues are derived primarily from the sale of gold and silver and Cerro Verde’s revenues are derived primarily from copper sales, the prices we, Yanacocha and Cerro Verde obtain for gold, silver, copper and ore concentrates containing such metals, and our, Yanacocha’s and Cerro Verde’s earnings, are directly related to world market prices for such metals. Such prices have historically fluctuated widely and are affected by numerous factors beyond our control, including the overall demand for and worldwide supply of gold, silver, copper and other metals; the availability and price of competing commodities, international economic trends, currency exchange fluctuations, expectations of inflation, actions of commodity markets participants, consumption and demand patterns and political events in major producing countries. We have in the past engaged in hedging activities, such as forward sales and option contracts, to minimize our exposure to fluctuations in the prices of gold, silver and other metals. Due to actions taken in 2007 and early 2008 to release our gold hedge book from specified fixed prices, we are now completely unhedged as to the price at which our gold and silver will be sold. As a result, we are fully exposed to the effects of changes in prevailing market prices of gold and silver. See “Risk Factors—Factors Relating to the Company—Hedging,” “Item 11. Quantitative and Qualitative Disclosures About Market Risk” and Note 29 to the Financial Statements. For information on gold and silver prices for each of the years in the five-year period ended December 31, 2008, see “Item 4. Information on the Company—The Company—Business Overview—Sales of Metal Concentrates.” On December 31, 2008 and May 29, 2009, the morning fixing price for gold on the London Bullion Market was US$865 per ounce and US$972 per ounce, respectively. On December 31, 2008 and May 29, 2009, the afternoon fixing spot price of silver on the London market, or London Spot, was US$10.79 per ounce and US$15.52 per ounce, respectively. On December 31, 2008 and May 29, 2009, the London Metal Exchange Settlement price for copper was US$2,902 per metric ton and US$4,776 per metric ton, respectively.

11

The world market prices of gold, silver and copper have historically fluctuated widely and there is no assurance that the prices for these metals will continue to maintain their current high historical levels. We cannot predict whether metal prices will rise or fall in the future. A decline in the market price of one or more of these metals could adversely impact our revenues, net income and cash flows and adversely affect our ability to repay our debt and meet our other financial obligations.

In addition, sustained low gold, silver or copper prices could: reduce revenues further through production declines due to cessation of the mining of deposits, or portions of deposits, that have become uneconomic at the then-prevailing market price; reduce or eliminate the profit that we currently expect from reserves; halt or delay the development of new projects; reduce funds available for exploration; and reduce existing reserves by removing ores from reserves that can no longer be economically processed at prevailing prices. Such declines in price and/or reductions in operations could also cause significant volatility in our financial performance and adversely affect the trading prices of our Common Shares and ADSs.

Impact of Government Regulation

Our, Yanacocha’s and Cerro Verde’s activities in Peru depend on mining concessions for exploration, which we refer to as mining concessions, being obtained from the Peruvian Ministry of Energy and Mines, or MEM, in our case, and through the assignment of concessions granted to a related entity by the Peruvian government, in the case of Yanacocha. In addition, our and Yanacocha’s activities in Peru depend on provisional permits, obtained from the MEM, for exploration rights of the area of the claim, which we refer to as provisional permits, and together with mining concessions, referred to as mining rights, and/or processing concessions, obtained from the MEM, for treatment of mining ores, or processing concessions, as well as compliance by us and Yanacocha with certain agreements entered into with the Peruvian government. Under Peru’s current legal and regulatory regime, our mining rights have an indefinite term and Yanacocha’s assigned mining rights have a term of 20 years, contingent upon payment of the annual concession fee for each mining right, with an option to renew for an additional term of 20 years. The mining rights are maintained by meeting a minimum annual level of production or investment and by the annual payment of a concession fee. A fine is payable for the years in which minimum production or investment requirements are not met. In addition if, in any year, the concession fee is not paid, payment may be made the following year within the term provided for making such payment. Any payment made will be applied to the prior year if such prior year payment was not paid. Failure to pay such concession fees or fines for two consecutive years could result in the loss of one or more of the mining rights. However, mining and processing concessions will not lapse if the administrative authority failed to issue a resolution declaring the termination of the concession within the first five years following the date on which such payment failure occurred. Our and Yanacocha’s processing concessions enjoy the same duration and tenure as the mining rights, subject to payment of a fee based on nominal capacity for the processing plant. Failure to pay such processing fees or fines for two consecutive years could result in the loss of the processing concessions. We are, and Yanacocha has informed us that Yanacocha is, current in the payment of all amounts due in respect to its mining and processing concessions.

12

On June 24, 2004, the Peruvian Congress approved Law No. 28258 – Mining Royalties Law. This law established a mining royalty that owners of mining concessions must pay to the Peruvian government for the exploitation of metallic and non-metallic resources. The mining royalties are calculated on a sliding scale with rates ranging from 1 to 3 percent over the value of mineral concentrates based on international market prices. As provided by Law No. 28969, effective since January 26, 2007, government tax agencies are responsible for the collection of mining royalties. See “Item 4. Information on the Company—The Company—Business Overview—Regulatory Framework—Mining Royalties.” We made our first payment of the mining royalty pursuant to Law No. 28258 in 2004. Yanacocha and Cerro Verde were exempt from this payment pursuant to its Mining Law Stabilization Agreements under the General Mining Law with the Peruvian government. There can be no assurance that the Peruvian government will not impose additional mining royalties on us, Yanacocha or Cerro Verde in the future or that such mining royalties will not have an adverse effect on our, Yanacocha’s or Cerro Verde’s results of operations or financial condition.

In addition, during 2006 Peruvian mining companies, represented by the Sociedad Nacional de Minería, Petróleo y Energía, agreed to a mining payment equivalent to 3.75 percent of income after taxes. The payment was negotiated with the Peruvian government and is intended to support government efforts to alleviate poverty. On December 21, 2006, the Peruvian government issued Supreme Decree No. 071-2006-EM, which approved the form of agreement to be entered by mining companies and the Peruvian government and authorized the Minister of Economy and Finance and the Minister of Energy and Mines to sign such agreements. The form of agreement contains the conditions under which the negotiated payment will be paid by Peruvian mining companies. The payment amounts to 3.75 percent of Peruvian income after income tax, including 2.75 percent to be paid to a local mining fund and 1 percent to be paid to a regional mining fund. This payment is payable from 2006 through 2010, contingent on the price of gold. Payments shall be made on or before April 30 of each year, after the income tax sworn declaration is submitted to the Peruvian tax authority. Pursuant to the Supreme Decree 033-2007-EM, mining companies can make the payments to the local and regional funds after such deadline, provided the prior approval of the Ministry of Energy and Mines and the Ministry of Economy and Finance is obtained. Fulfillment of the payment obligations will be reviewed by an audit entity by performing certain agreed-upon procedures to verify the validity of the payment amounts recorded as such with the Comisión Nacional Supervisora de Empresas y Valores (National Supervisory Commission of Business and Securities, or CONASEV) to be agreed between the mining company, the Ministry of Energy and Mines and the Ministry of Economy and Finance.

In 2007, Cerro Verde negotiated an agreement with the Peruvian government that allowed a credit against contributions to the local mining fund for Cerro Verde’s work in constructing water and sewage treatment facilities in the Arequipa region in 2006. However, during the third quarter of 2007, Cerro Verde’s agreement with the government was modified to exclude this credit. Cerro Verde recorded an expense of US$48.7 million in 2007, of which US$16.7 million was related to contributions for 2006 and US$32.0 million was related to contributions for 2007. Cerro Verde recorded an expense of US$29.5 million in 2008. As of December 31, 2008, Cerro Verde’s liability associated with the local mining fund contributions totaled US$27.9 million.

13

Environmental and other Regulatory Matters

Our, Yanacocha’s and Cerro Verde’s exploration, mining and milling activities, as well our and Yanacocha’s smelting and refining activities, are subject to a number of Peruvian laws and regulations, including environmental laws and regulations. Additional matters subject to regulation include, but are not limited to, concession fees, transportation, production, water use and discharges, power use and generation, use and storage of explosives, surface rights, housing and other facilities for workers, reclamation, taxation, labor standards, mine safety and occupational health.

We anticipate additional laws and regulations will be enacted over time with respect to environmental matters. The development of more stringent environmental protection programs in Peru could impose constraints and additional costs on our, Yanacocha’s and Cerro Verde’s operations and require us, Yanacocha and Cerro Verde to make significant capital expenditures in the future. Although we believe we are substantially in compliance, and Yanacocha and Cerro Verde have advised us that Yanacocha and Cerro Verde are substantially in compliance, with all applicable environmental regulations, there can be no assurance that future legislative or regulatory developments will not have an adverse effect on our, Yanacocha’s or Cerro Verde’s business or results of operations. See “Item 4. Information on the Company—The Company—Business Overview—Regulatory Framework—Environmental Matters” and “—Permits” and “Item 4. Information on the Company—Yanacocha—Regulation, Permit and Environmental Matters.”

Hedging

Since 2003, we have been modifying the terms of certain derivative instruments in order to qualify them as normal sales contracts. On January 15, 2007, we modified the schedule of commitments for gold with two of our clients. As a consequence of this modification, we transferred 208,000 and 108,000 gold ounces that had been committed for sale in 2007 and 2008, respectively, and committed them for sale in 2012 instead, without any cash disbursement. In March and May 2007, we negotiated with several counterparties to eliminate the fixed or maximum price component on determined commitments for a total of 971,000 gold ounces scheduled for delivery from 2008 to 2012, which required us to make aggregate payments of US$315.69 million. Additionally, in January and February 2008, we negotiated with several counterparties to eliminate the fixed or maximum price component on all of our outstanding gold commitments, representing 922,000 gold ounces, which required us to make aggregate payments of US$517.15 million. As a result, we are fully exposed to the effects of changes in prevailing market prices of gold, silver and copper. See “—Factors Relating to the Company—Prices of Gold, Silver and Copper.”

At El Brocal, we implemented a base metal hedging policy for a maximum of 25 percent of El Brocal’s total payable metal contained per year, for up to three years. As of March 31, 2009 all transactions entered have been forward pricing operations through non-delivery (Asian) swaps. Outstanding hedging commitments for 2009 to 2011 amount to 10 percent of payable metal and are as follows: (i) 5,200 metric tons of copper at an average price of US$8,147 per metric ton, (ii) 14,300 metric tons of lead at an average price of US$2,302 per metric ton and (iii) 12,000 metric tons of zinc at an average price of US$2,637 per metric ton. See “Item 11. Quantitative and Qualitative Disclosures About Market Risk” and Note 28 to the Financial Statements.

Yanacocha and Cerro Verde have not engaged in, and are currently not engaged in, gold or copper price hedging activities, such as forward sales or option contracts, to minimize its exposure to fluctuations in the price of gold or copper. No assurance can be given, however, that Yanacocha or Cerro Verde will not enter into hedging transactions in the future or that such transactions, if entered into, will have the desired effect.

14

Speculative Nature of Metals Exploration

Precious metals exploration, particularly gold exploration, is highly speculative in nature, involves many risks and frequently is unsuccessful. There can be no assurance that our, Yanacocha’s or Cerro Verde’s metals exploration efforts will be successful. Once mineralization is discovered, it may take a number of years from the initial phases of drilling before production is possible, during which time the economic feasibility of production may change. Substantial expenditures are required to establish proven and probable ore reserves through drilling, to determine metallurgical processes to extract the metals from the ore and, in the case of new properties, to construct mining and processing facilities. As a result of these uncertainties, no assurance can be given that our or Yanacocha’s exploration programs will result in the expansion or replacement of current production with new proven and probable ore reserves.

Advanced exploration projects have no operating history upon which to base estimates of proven and probable ore reserves and estimates of future cash operating costs. Such estimates are, to a large extent, based upon the interpretation of geologic data obtained from drill holes and other sampling techniques, and feasibility studies which derive estimates of cash operating costs based upon anticipated tonnage and grades of ore to be mined and processed, the configuration of the ore body, expected recovery rates of the mineral from the ore, comparable facility and equipment operating costs, anticipated climatic conditions and other factors. As a result, it is possible that actual cash operating costs and economic returns based upon proven and probable ore reserves may differ significantly from those originally estimated. Moreover, significant decreases in actual over expected prices may mean reserves, once found, will be uneconomical to produce. It is not unusual in new mining operations to experience unexpected problems during the start up phase. Yanacocha and Cerro Verde used US$725 per ounce of gold and US$1.60 per pound of copper to calculate their gold and copper reserves, respectively, as of December 31, 2008; we use a fixed price of US$725 per ounce of gold and a three-year average historic price of US$13.00 per ounce of silver to calculate our proven and probable ore reserves.

Increased Costs Could Affect Profitability

Costs at any particular mining location frequently are subject to variation due to a number of factors, such as changing ore grade, changing metallurgy and revisions to mine plans in response to the physical shape and location of the ore body. In addition, costs are affected by the price of commodities, such as fuel, electricity and labor. Commodity costs are at times subject to volatile price movements, including increases that could make production at certain operations less profitable. Reported costs may be affected by changes in accounting standards. A material increase in costs at any significant location could have a significant effect on our profitability.

Indebtedness

We incurred significant indebtedness during 2007 and 2008 in connection with the unwinding of our gold hedge book. The agreements governing our indebtedness contain covenants that restrict our ability to:

| § | incur additional indebtedness; |

| § | engage in transactions with affiliates; |

| § | create liens on our assets; |

| § | make certain investments; |

15

| § | sell assets, subject to certain exceptions; |

| § | acquire other companies or dissolve, liquidate or merge with or into other companies; |

| § | enter into unrelated businesses; |

| § | make guarantees; |

| § | enter into burdensome agreements; and |

| § | enter into certain hedging transactions other than in the ordinary course of business. |

In addition, we are required to maintain certain financial ratios and operating metrics.

Any failure to comply with the restrictions under any agreement governing our other indebtedness may result in an event of default. Such default may allow the creditors to accelerate the related debt, which may trigger cross-acceleration or cross-default provisions in other debt agreements. Our assets and cash flow may not be sufficient to fully repay borrowings under our debt instruments that are accelerated upon an event of default.

If we are unable to repay, refinance or restructure our indebtedness under, or amend the covenants contained in, our loan or credit agreements at maturity or in the event of a default, the lenders could declare all borrowings outstanding (together with accrued interest and other fees) immediately due and payable and institute foreclosure proceedings against the security. Any such actions could force us into bankruptcy or liquidation.

Capital Intensive Nature of Precious Metals Exploration

Precious metals exploration requires substantial capital expenditures for the exploration, extraction, production and processing stages and for machinery, equipment and experienced personnel. There can be no assurance that we or Yanacocha will generate sufficient cash flow and/or that we will have access to sufficient external sources of funds in the form of outside investment or loans to continue exploration activities at the same or higher levels than in the past.

Reserves Estimates

The proven and probable ore reserve figures presented in this Annual Report are our, Yanacocha’s and Cerro Verde’s estimates, and there can be no assurance that the level of recovery of gold, silver, copper and certain other metals will be realized. Reserve estimates may require revision based on actual production experience. Market price fluctuations of gold, silver and other metals, as well as increased production costs or reduced recovery rates, may render proven and probable ore reserves containing relatively lower grades of mineralization uneconomic to exploit and may ultimately result in a restatement of proven and probable ore reserves. Moreover, short-term operating factors relating to the reserves, such as the processing of different types of ore or ore grades, could adversely affect our or Yanacocha’s profitability in any particular accounting period. See “Item 4. Information on the Company—Property, Plants and Equipment—Our Property—Reserves” and “Item 4. Information on the Company—Property, Plants and Equipment—Yanacocha’s Properties—Reserves.”

16

Replacement of Reserves

As we produce gold, silver, zinc and other metals, we deplete our ore reserves for such metals. To maintain production levels, we must replace depleted reserves by exploiting known ore bodies and locating new deposits. Success in exploration for gold, silver and the other metals we produce is very uncertain and there is a risk that our depletion of reserves will not be offset by new discoveries.

As of December 31, 2008, Yanacocha’s proven and probable reserves (excluding Conga’s proven and probable reserves) were estimated to be 13.0 million ounces of gold, representing a 17.4 percent decrease over Yanacocha’s proven and probable reserves as of December 31, 2007, which were estimated to be 15.8 million ounces of gold. The decrease in reserves of gold was mainly due to a mining depletion of 2.6 million ounces, as well as a decrease of 0.1 million ounces of gold reserves due to unit cost increases, additional drilling, updated block models, revised pit designs, leach pad inventory adjustments, transfer of reserves to non-reserve mineralization due to social issues and leach pad capacity limitations, partially offset by metal price increases, an increase in the expected recoverable ounces in leach pads and the improvement of pit design.

As of December 31, 2008, our proven and probable reserves were estimated to be 1.1 million ounces of gold, which represented a 15% decrease from an estimated 1.3 million ounces of gold reserves as to December 31, 2007. The decrease in reserves of gold was mainly due to depletion of reserves in our Antapite and Porcota mines.

Industry Risks

The business of mining, smelting and refining gold, silver, copper and other metals is generally subject to a number of risks and hazards, including industrial accidents, labor disputes, unusual or unexpected geological conditions, changes in the regulatory environment, environmental hazards and weather and other natural phenomena such as earthquakes. Such occurrences could result in damage to, or destruction of, mining properties or production facilities, personal injury or death, environmental damage, delays in mining, monetary losses and possible legal liability. We, Yanacocha and Cerro Verde each maintain insurance against risks that are typical in the mining industry in Peru and in amounts that we and Yanacocha believe to be adequate but which may not provide adequate coverage in certain circumstances. Insurance against certain risks (including certain liabilities for environmental pollution or other hazards as a result of exploration and production) is not generally available to us or Yanacocha or to other companies within the industry.

Increased Equipment Costs and Shortages; Increase Production Costs

In recent years there has been a significant increase in mining activity worldwide in response to increased demand and significant increases in prices of natural resources. The opening of new mines and expansion of existing mines has led to increased demand for, and increased costs and shortages of, equipment, supplies and experienced personnel. These cost increases have significantly increased overall operating and capital budgets of companies like ours, and continuing shortages could affect the timing and feasibility of expansion projects.

Energy represents a significant portion of our production costs. Our principal energy sources are electricity, purchased petroleum products, natural gas and coal. An inability to procure sufficient energy at reasonable prices could adversely affect our profits, cash flow and growth opportunities. Our production costs are also affected by the prices of commodities we consume or use in our operations, such as sulfuric acid, grinding media, steel, reagents, liners, explosives and diluents. The prices of such commodities are influenced by supply and demand trends affecting the mining industry in general and other factors outside our control and such prices are at times subject to volatile movements. Increases in the cost of these commodities could make our operations less profitable, even in an environment of relatively high copper prices. Increases in the costs of commodities that we consume or use may also significantly affect the capital costs of new projects.

17

Labor Matters

Between 2002 and early 2007, we did not experience any strikes. On April 30, 2007, we experienced a five-day labor stoppage at the Uchucchacua mine, which coincided with a strike called by the National Mining and Metallurgical Union. In November 2007, unionized workers at Uchucchaccua engaged in a three-day strike called by the National Mining and Metallurgical Union.

On February 27, 2008, the unionized workers of our Uchucchacua, Orcopampa, Ishihuinca and Antapite mines went on strike for three days, demanding an increase in the amount of their statutorily-required 8 percent share of our annual pre-tax profits. On June 5, 2008, our Uchucchacua laborers went on a four-day strike to support their negotiating position in the collective bargaining process. On June 30, 2008, the union of contractor workers of our Uchucchacua mining unit commenced a 7-day strike promoted by the National Federation of Mining Unions, which was declared illegal by the Peruvian Work Ministry.

��

There can be no assurance that we will not experience strikes or other labor-related work stoppages that could have a material adverse effect on our operations and/or operating results in the future.

In February 2004, Yanacocha entered into its first collective bargaining agreement with Workers’ Union of Minera Yanacocha S.R.L., or the Union, which was created and registered before the Peruvian Labor Ministry on December 9, 2003. This collective bargaining agreement expired in February 2007. In May 2007, Yanacocha completed negotiations with the Union’s members and entered into a new collective bargaining agreement, which is applicable only to the Union’s members and effective from March 2007 to February 2010. Yanacocha has informed us that it considers its relations with its employees to be good. However, a small percentage of Union members engaged in a two-day strike in November 2007, called by the National Mining and Metallurgical Union. The strike did not have any material impact on Yanacocha’s operations; nevertheless there can be no assurance that Yanacocha will not experience other strikes or labor-related work stoppages that could have a material adverse effect on its operations or its operating results. See “Item 6. Directors, Senior Management and Employees—Employees” and “Item 4. Information on the Company—Yanacocha—Employees.”

On June 10, 2008, the Sindicato Unico de Trabajadores of Sociedad Minera de Cerro Verde S.A.A. commenced an 11-day strike at Cerro Verde. The strike, which was declared illegal by the Peruvian Work Ministry, ended on June 21, 2008 and did not negatively impact Cerro Verde’s operations. On November 15, 2008 Cerro Verde and the Sindicato Único de Trabajadores signed a union agreement that is retrospectively applicable from September 1, 2008 through August 31, 2011.

Political and Social Perception

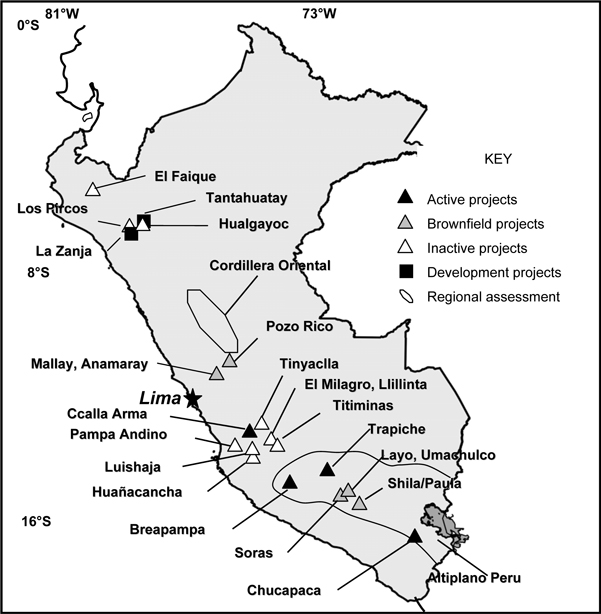

Our and Yanacocha’s exploration and production activities are potentially subject to political and social risks. Over the past several years, we and Yanacocha have been the target of local political protests, including community protests at our La Zanja project, a roadblock in protest of drilling activities at Yanacocha’s Cerro Quilish mine and a roadblock carried out by members of the Combayo community. In September 2004, due to the incidents at Cerro Quilish, Yanacocha suspended all drilling activities at this mine. In December 2004, Yanacocha removed the Cerro Quilish gold deposit from its proven and probable reserves. See “Item 4. Information on the Company—The Company—Business Overview—Greenfield Exploration Projects—La Zanja” and “Item 4. Information on the Company—Yanacocha—Legal Proceedings.” There can be no assurance that these incidents will not continue, or that similar incidents will not occur, or that the continuation or intensification of community protests would not adversely affect our or Yanacocha’s exploration and production activities or our or Yanacocha’s results of operations or financial condition.

18

Investment Company Act

As of December 31, 2008, we owned a 43.65 percent partnership interest in Yanacocha and a 19.05 percent equity interest in Cerro Verde. These interests may constitute “investment securities” for purposes of the U.S. Investment Company Act of 1940, as amended, or the Investment Company Act.

Under the Investment Company Act, an investment company is defined in relevant part to include (i) any company that is or holds itself out as being engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting or trading in securities and (ii) any company that owns or proposes to acquire investment securities having a value exceeding 40 percent of such company’s total assets (exclusive of certain items) on an unconsolidated basis. Issuers that are investment companies within the meaning of the Investment Company Act, and which do not qualify for an exemption from the provisions of such act, are required to register with the Commission and are subject to substantial regulations with respect to capital structure, operations, transactions with affiliates and other matters. If we were deemed to be an investment company and did not qualify for an exemption from the provisions of the Investment Company Act, we would be required to register with the Commission and would be subject to such regulations, which would be unduly burdensome and costly for us and possibly adversely impact us.

We received an order from the Commission on April 19, 1996 declaring us to be primarily engaged in a business other than that of an investment company and, therefore, not an investment company within the meaning of the Investment Company Act. We intend to conduct our operations and maintain our investments in a manner, and will take appropriate actions as necessary, to ensure we will not be deemed to be an investment company in the future. The Commission, however, upon its motion or upon application, may find that the circumstances that gave rise to the issuance of the order no longer exist, and as a result may revoke such order. There can be no assurance that such order will not be revoked.

Factors Relating to Peru

Exposure to Peruvian Political Risk

All of our, Yanacocha’s and Cerro Verde’s operations are conducted in Peru. Accordingly, our, Yanacocha’s and Cerro Verde’s business, financial condition or results of operations could be affected by changes in economic or other policies of the Peruvian government or other political, regulatory or economic developments in Peru.

During the past several decades, Peru has had a history of political instability that has included military coups and a succession of regimes with differing policies and programs. Past governments have frequently played an interventionist role in the nation’s economy and social structure. Among other things, past governments have imposed controls on prices, exchange rates and local and foreign investment as well as limitations on imports, restricted the ability of companies to dismiss employees, expropriated private sector assets (including mining companies) and prohibited the remittance of profits to foreign investors.

19

During the 1980s, government policies restricted our ability, among other things, to repatriate funds and import products from abroad. In addition, currency exchange rates were strictly controlled, and all export sales were required to be deposited in Peru’s Banco Central de Reserva, or Central Bank, where they were exchanged from U.S. Dollars to Peruvian currency at less-than-favorable rates of exchange. These policies generally affected our results of operations. Controls on repatriation of funds limited the ability of our shareholders to receive dividends outside of Peru, but did not limit the ability of our shareholders to receive distributions of earnings in Peru. See “Item 10. Additional Information—Exchange Controls.”

In July 1990, Alberto Fujimori was elected president of Peru, and his administration implemented a broad-based reform of Peru’s political system, economy and social conditions, aimed at stabilizing the economy, restructuring the national government by reducing bureaucracy, privatizing state-owned companies, promoting private investment, developing and strengthening free markets, institutionalizing democratic representation and enacting programs for the strengthening of basic services related to education, health, housing and infrastructure. However, after Fujimori’s reelection to his third five-year term of office on May 29, 2000, Fujimori resigned from his post amid increasing social pressure. The Peruvian Congress appointed Valentin Paniagua as interim President. New elections were subsequently held on April 8, 2001 and a run-off election was held on June 3, 2001, in which Alejandro Toledo was elected President. President Toledo’s government largely retained the economic policies of the previous government, focusing on promoting private investment, privatizing state-owned companies in various sectors including energy, mining and public services.

At the elections held on April 9, 2006, no presidential candidate received the required 50 percent or more of the votes. As a result, a second round election between the top two presidential candidates, Ollanta Humala Tasso from the Partido Union por el Peru, or the UPP, and Alan García Pérez of the Partido Alianza Popular Revolucionaria, or APRA, was held on June 4, 2006. Alan García Pérez was elected, but he has no majority in Congress. The new government has continued the economic policies of its predecessor.

During 1980s and early 1990s the Sendero Luminoso, or SL, and the Movimiento Revolucionario Tupac Amaru, or MRTA, terrorist organizations were particularly active in Peru. Although SL and MRTA were almost de-activated in 1992 and 1997 respectively, we cannot guarantee that acts by these or other terrorist organizations will not adversely affect our operations in the future.

Risks of Inflation, Reduced Economic Growth and Currency Devaluation

Over the past several decades, Peru has experienced periods of high inflation, slow or negative economic growth and substantial currency devaluation. The inflation rate in Peru, as measured by the Indice de Precios al Consumidor, or IPC, and published by Instituto Nacional de Estadística e Informática, or INEI, has fallen from a high of 7,649.7 percent in 1990 to 3.5 percent in 2004, 1.5 percent in 2005, 1.1 percent in 2006, 3.93 percent in 2007 and 6.7 percent in 2008. The Peruvian currency has been devalued numerous times during the last 20 years. The devaluation rate has decreased from a high of 4,019.3 percent in 1990 to revaluation of 5.5 percent in 2004, a devaluation of 4.5 percent in 2005, a revaluation of 6.4 percent in 2006, a revaluation of 7.0 percent in 2007 and a devaluation of 5.4 percent in 2008. Our revenues and operating expenses are primarily denominated in U.S. Dollars. If inflation in Peru were to increase without a corresponding devaluation of the Nuevo Sol relative to the U.S. Dollar, our financial position and results of operations, and the market price of our Common Shares and American Depositary Shares, or ADSs, could be affected. Although the Peruvian government’s stabilization plan has significantly reduced inflation, and the Peruvian economy has experienced strong growth in recent years, there can be no assurance that inflation will not increase from its current level or that such growth will continue in the future at similar rates or at all.

20

Among the economic circumstances that could lead to a devaluation would be the decline of Peruvian foreign reserves to inadequate levels. Peru’s foreign reserves at December 31, 2008 were US$31.2 billion as compared to US$27.7 billion at December 31, 2007. Although actual foreign reserves must be maintained at levels that will allow the succeeding government the ability to manage the Peruvian economy and to assure monetary stability in the near future, there can be no assurance that Peru will be able to maintain adequate foreign reserves to meet its foreign currency denominated obligations, or that Peru will not devalue its currency should its foreign reserves decline. See “Item 3. Key Information—Selected Financial Data—Exchange Rates.”

Peru’s current account deficit is being funded partially by foreign direct investment. There can be no assurance that foreign direct investment will continue at current levels, particularly if adverse political or economic developments in Peru arise, a development that may also contribute to devaluation pressure.

Deterioration in Economic and Market Conditions in Latin America and Other Emerging Market Countries

The market for securities issued by Peruvian companies is influenced by economic and market conditions in Peru and, to varying degrees, market conditions in other Latin American and emerging market countries. Although economic conditions are different in each country, the reaction of investors to developments in one country is likely to cause the capital markets in other countries to fluctuate. For example, political and economic events, such as the crises in Venezuela, Ecuador, Bolivia, Brazil and Argentina, have influenced investors’ perceptions of risk with regard to Peru. The negative investor reaction to developments in our neighboring countries may adversely affect the market for securities issued by countries in the region, cause foreign investors to decrease the flow of capital into Latin America and introduce uncertainty about plans for further integration of regional economies.

Exchange and Investment Controls

Peruvian law currently imposes no restrictions on the ability of companies operating in Peru to transfer foreign currency from Peru to other countries, to convert Peruvian currency into foreign currency or foreign currency into Peruvian currency or to remit dividends abroad or on the ability of foreign investors to liquidate their investment and repatriate their capital. Prior to 1991, Peru had restrictive exchange controls and exchange rates. During the latter part of the 1980s, exchange restrictions prevented payment of dividends to our shareholders in the United States in U.S. Dollars. Accordingly, should such or similar controls be instituted, dividends paid to holders of Common Shares and, consequently, holders of American Depositary Receipts, or ADRs, could be affected. There can be no assurance that the Peruvian government will continue to permit such transfers, remittances or conversion without restriction. See “Item 10. Additional Information—Exchange Controls.”

Corporate Disclosure and Accounting Standards

We prepare our financial statements using Peruvian GAAP, which differs in certain material respects from U.S. GAAP. Thus, the presentation of Peruvian financial statements and reported earnings may not be comparable to those companies whose financial statements are prepared in accordance with U.S. GAAP. See Note 33 to the Financial Statements for a description of the significant differences between Peruvian GAAP and U.S. GAAP, as such differences relate to us, and Note 34 for a reconciliation to U.S. GAAP of our net income and shareholders’ equity for the period included therein. In addition, as a foreign private issuer in the United States, we have less intensive reporting requirements and information regarding us may not be as readily disseminated into the market.

21

Enforceability of Civil Liabilities