| Exhibit 99.1 | ||||||||

Freddie Mac Reports Net Income of $2.7 Billion for Fourth Quarter 2021

and $12.1 Billion for Full-Year 2021

Making Home Possible for Nearly Five Million Households in 2021

•Enabled 1.4 million families, including over 553,000 first-time homebuyers, to purchase a home and nearly 2.9 million homeowners to refinance into more favorable terms

•Financed 655,000 rental units, with 94% of eligible units being affordable to low- to moderate-income families

Fourth Quarter 2021 Financial Results

Market Liquidity Provided - $298 Billion | Homes and Rental Units Financed - 1.2 Million | Net Worth - $28.0 Billion | Total Mortgage Portfolio - $3.2 Trillion | |||||||||||||||||

| Consolidated | •Net income of $2.7 billion, a decrease of 6% year-over-year, as higher net revenues were offset by an increase in credit-related expense •Net revenues of $5.6 billion, an increase of 11% year-over-year, driven by mortgage portfolio growth and higher average portfolio guarantee fee rates •Provision for credit losses of $0.1 billion, compared to a benefit for credit losses of $0.8 billion in the fourth quarter of 2020. The benefit for credit losses in the prior year was driven by a reserve release due to realized house price appreciation •New business activity of $271 billion, down 29% year-over-year, as refinance activity moderated from historically high levels in the prior year. Full-year 2021 activity of $1.2 trillion, up 12% year-over-year •Mortgage portfolio of $2,792 billion, up 20% year-over-year, driven by strong full-year new business activity and continued house price appreciation •Serious delinquency rate of 1.12%, down from 1.46% at September 30, 2021 and 2.64% at December 31, 2020, driven by a decline in loans in forbearance •Completed approximately 62,000 loan workouts •53% of mortgage portfolio covered by credit enhancements •New business activity of $25 billion, down 29% year-over-year. Full-year 2021 activity of $70 billion, down 16% year-over-year, driven by a reduced loan purchase cap •Mortgage portfolio of $415 billion, up 7% year-over-year, driven by ongoing loan purchase and securitization activity •Delinquency rate, which does not include loans in forbearance, of 0.08%, down from 0.12% at September 30, 2021 and 0.16% at December 31, 2020 •94% of mortgage portfolio covered by credit enhancements | “In 2021, Freddie Mac made significant progress responsibly advancing our mission of making home possible, helping nearly five million families rent, buy, or refinance a home. The company continued to build financial strength by adding nearly $12 billion to retained earnings, improving our safety and soundness, and moving us closer to our capital target. We accomplished this while effectively managing our risks, which allows us to support our mission through the economic cycle and particularly in times of crisis. We begin 2022 with much to be proud of—and even more to accomplish in the year ahead.” Michael J. DeVito Chief Executive Officer | ||||||||||||

Net Revenues $5.6 Billion Net Income $2.7 Billion Comprehensive Income $2.7 Billion | ||||||||||||||

| Single-Family | ||||||||||||||

Net Revenues $4.7 Billion Net Income $2.2 Billion Comprehensive Income $2.2 Billion | ||||||||||||||

| Multifamily | ||||||||||||||

Net Revenues $0.9 Billion Net Income $0.5 Billion Comprehensive Income $0.5 Billion | ||||||||||||||

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 2

McLean, VA — Freddie Mac (OTCQB: FMCC) today reported net income of $2.7 billion for the fourth quarter of 2021, a decrease of 6% year-over-year, as higher net revenues were offset by an increase in credit-related expense. The company reported comprehensive income of $2.7 billion for the fourth quarter of 2021, an increase of 8% year-over-year.

Net revenues for the fourth quarter of 2021 increased 11% year-over-year to $5.6 billion, primarily driven by higher net interest income. Net interest income for the fourth quarter of 2021 increased 30% year-over-year to $4.8 billion, primarily driven by continued mortgage portfolio growth and higher average portfolio guarantee fee rates in Single-Family.

Credit-related expense for the fourth quarter of 2021 was $0.6 billion, compared to credit-related income of $0.1 billion in the fourth quarter of 2020. Credit-related expense for the fourth quarter of 2021 included a provision for credit losses of $0.1 billion. Credit-related income for the fourth quarter of 2020 included a benefit for credit losses of $0.8 billion, which was primarily driven by a reserve release due to realized house price appreciation.

Full-Year 2021 Financial Results

Freddie Mac reported net income of $12.1 billion for full-year 2021, an increase of 65% year-over-year, primarily driven by higher net revenues and a credit reserve release in Single-Family. The company reported comprehensive income of $11.6 billion for full-year 2021, an increase of 54% year-over-year.

Net revenues for full-year 2021 increased 32% year-over-year to $22.0 billion, primarily driven by higher net interest income and higher net investment gains. Net interest income for full-year 2021 increased 38% year-over-year to $17.6 billion, primarily driven by continued mortgage portfolio growth, higher average portfolio guarantee fee rates, and higher deferred fee income recognition in Single-Family. The increase in net investment gains for full-year 2021 was primarily due to higher gains on Multifamily securitization activities.

Credit-related expense for full-year 2021 decreased 56% year-over-year to $1.0 billion, driven by a reserve release due to realized house price appreciation and improving economic conditions throughout 2021, partially offset by a decrease in credit enhancement recoveries. Credit-related expense for full-year 2020 was primarily driven by the negative economic effects of the COVID-19 pandemic.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 3

Summary of Consolidated Statements of Comprehensive Income (Loss)

| (Dollars in millions) | 4Q 2021 | 3Q 2021 | Change | 4Q 2020 | Change | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||

| Net interest income | $4,756 | $4,418 | $338 | $3,653 | $1,103 | $17,580 | $12,771 | |||||||||||||||||||||||||||||||||||||

| Guarantee income | 182 | 246 | (64) | 281 | (99) | 1,032 | 1,442 | |||||||||||||||||||||||||||||||||||||

| Investment gains (losses), net | 519 | 383 | 136 | 856 | (337) | 2,746 | 1,813 | |||||||||||||||||||||||||||||||||||||

| Other income (loss) | 108 | 200 | (92) | 232 | (124) | 593 | 633 | |||||||||||||||||||||||||||||||||||||

| Net revenues | 5,565 | 5,247 | 318 | 5,022 | 543 | 21,951 | 16,659 | |||||||||||||||||||||||||||||||||||||

| Benefit (provision) for credit losses | (138) | 243 | (381) | 813 | (951) | 1,041 | (1,452) | |||||||||||||||||||||||||||||||||||||

Other credit-related expense(1) | (466) | (437) | (29) | (722) | 256 | (2,072) | (884) | |||||||||||||||||||||||||||||||||||||

| Credit-related income (expense) | (604) | (194) | (410) | 91 | (695) | (1,031) | (2,336) | |||||||||||||||||||||||||||||||||||||

| Administrative expense | (734) | (627) | (107) | (706) | (28) | (2,651) | (2,535) | |||||||||||||||||||||||||||||||||||||

| Legislated 10 basis point fee expense | (636) | (602) | (34) | (495) | (141) | (2,342) | (1,836) | |||||||||||||||||||||||||||||||||||||

| Other expense | (156) | (178) | 22 | (243) | 87 | (728) | (723) | |||||||||||||||||||||||||||||||||||||

| Operating expense | (1,526) | (1,407) | (119) | (1,444) | (82) | (5,721) | (5,094) | |||||||||||||||||||||||||||||||||||||

| Income (loss) before income tax (expense) benefit | 3,435 | 3,646 | (211) | 3,669 | (234) | 15,199 | 9,229 | |||||||||||||||||||||||||||||||||||||

| Income tax (expense) benefit | (691) | (727) | 36 | (756) | 65 | (3,090) | (1,903) | |||||||||||||||||||||||||||||||||||||

| Net income (loss) | 2,744 | 2,919 | (175) | 2,913 | (169) | 12,109 | 7,326 | |||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss), net of taxes and reclassification adjustments | (22) | (10) | (12) | (391) | 369 | (489) | 205 | |||||||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | $2,722 | $2,909 | $(187) | $2,522 | $200 | $11,620 | $7,531 | |||||||||||||||||||||||||||||||||||||

(1) Other credit-related expense includes credit enhancement expense, benefit for (decrease in) credit enhancement recoveries, and REO operations income (expense). | ||||||||||||||||||||||||||||||||||||||||||||

| Conservatorship metrics (in billions) | ||||||||||||||||||||||||||||||||||||||||||||

| Net worth | $28.0 | $25.3 | $2.7 | $16.4 | $11.6 | $28.0 | $16.4 | |||||||||||||||||||||||||||||||||||||

| Senior preferred stock liquidation preference | 98.0 | 95.0 | 2.9 | 86.5 | 11.4 | 98.0 | 86.5 | |||||||||||||||||||||||||||||||||||||

| Remaining Treasury funding commitment | 140.2 | 140.2 | — | 140.2 | — | 140.2 | 140.2 | |||||||||||||||||||||||||||||||||||||

| Cumulative dividend payments to Treasury | 119.7 | 119.7 | — | 119.7 | — | 119.7 | 119.7 | |||||||||||||||||||||||||||||||||||||

| Cumulative draws from Treasury | 71.6 | 71.6 | — | 71.6 | — | 71.6 | 71.6 | |||||||||||||||||||||||||||||||||||||

Totals may not add due to rounding.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 4

| Single-Family Segment | ||

| Financial Results | ||

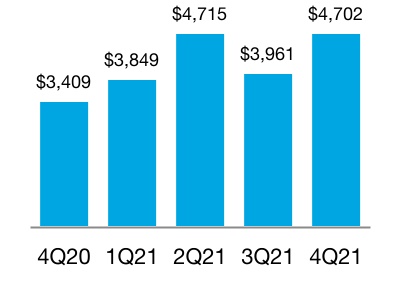

Net Revenues

(In millions)

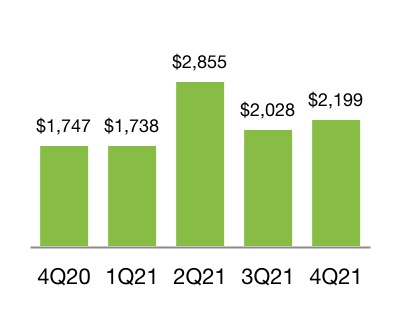

Net Income

(In millions)

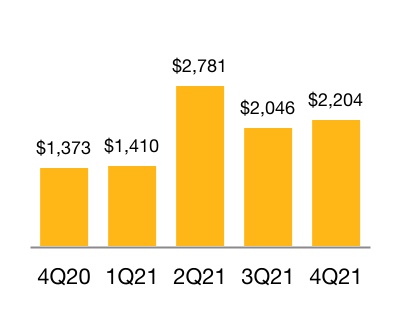

Comprehensive Income

(In millions)

| (Dollars in millions) | 4Q 2021 | 3Q 2021 | Change | 4Q 2020 | Change | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||

| Net interest income | $4,425 | $4,080 | $345 | $3,349 | $1,076 | $16,273 | $11,592 | |||||||||||||||||||||||||||||||||||||

| Non-interest income | 277 | (119) | 396 | 60 | 217 | 954 | 457 | |||||||||||||||||||||||||||||||||||||

| Net revenues | 4,702 | 3,961 | 741 | 3,409 | 1,293 | 17,227 | 12,049 | |||||||||||||||||||||||||||||||||||||

| Credit-related income (expense) | (605) | (177) | (428) | 80 | (685) | (1,086) | (2,200) | |||||||||||||||||||||||||||||||||||||

| Operating expense | (1,343) | (1,251) | (92) | (1,288) | (55) | (5,070) | (4,543) | |||||||||||||||||||||||||||||||||||||

| Income (loss) before income tax (expense) benefit | 2,754 | 2,533 | 221 | 2,201 | 553 | 11,071 | 5,306 | |||||||||||||||||||||||||||||||||||||

| Income tax (expense) benefit | (555) | (505) | (50) | (454) | (101) | (2,251) | (1,094) | |||||||||||||||||||||||||||||||||||||

| Net income (loss) | 2,199 | 2,028 | 171 | 1,747 | 452 | 8,820 | 4,212 | |||||||||||||||||||||||||||||||||||||

| Total other comprehensive income (loss), net of taxes and reclassification adjustments | 5 | 18 | (13) | (374) | 379 | (379) | 104 | |||||||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | $2,204 | $2,046 | $158 | $1,373 | $831 | $8,441 | $4,316 | |||||||||||||||||||||||||||||||||||||

Fourth Quarter 2021 Key Drivers

Net income and comprehensive income increased year-over-year, mainly driven by:

•Higher net interest income primarily due to continued mortgage portfolio growth and higher average portfolio guarantee fee rates, partially offset by

•Credit-related expense compared to credit-related income in the fourth quarter of 2020. Credit-related income in the fourth quarter of 2020 was primarily driven by a reserve release due to realized house price appreciation.

Full-Year 2021 Key Drivers

Net income and comprehensive income increased year-over-year, mainly driven by:

•Higher net interest income primarily due to continued mortgage portfolio growth, higher average portfolio guarantee fee rates, and higher deferred fee income recognition.

•Lower credit-related expense driven by a reserve release due to realized house price appreciation and improving economic conditions throughout 2021, partially offset by a decrease in credit enhancement recoveries. Credit-related expense in full-year 2020 was primarily driven by the negative economic effects of the COVID-19 pandemic.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 5

| Single-Family Segment | ||

| Business Results | ||

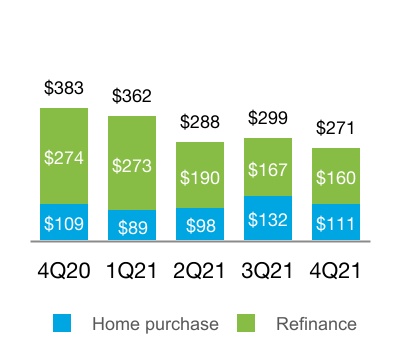

New Business Activity

(UPB in billions)

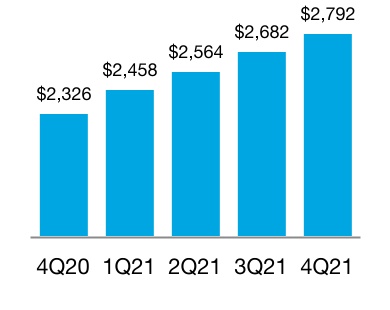

Mortgage Portfolio

(UPB in billions)

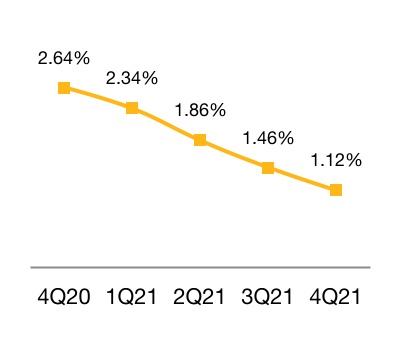

Serious Delinquency Rate

| 4Q 2021 | 3Q 2021 | Change | 4Q 2020 | Change | 2021 | 2020 | ||||||||||||||||||||||||||||||||||||||

| New Business Statistics: | ||||||||||||||||||||||||||||||||||||||||||||

| Average guarantee fee rate charged (bps) | 47 | 48 | (1) | 47 | — | 49 | 47 | |||||||||||||||||||||||||||||||||||||

| Weighted average original loan-to-value (LTV) (%) | 71 | 72 | (1) | 70 | 1 | 71 | 71 | |||||||||||||||||||||||||||||||||||||

| Weighted average original credit score | 748 | 750 | (2) | 761 | (13) | 753 | 759 | |||||||||||||||||||||||||||||||||||||

First-time homebuyers (%)(1) | 46 | 46 | — | 45 | 1 | 46 | 46 | |||||||||||||||||||||||||||||||||||||

| Single-Family homes funded (in thousands) | 955 | 1,027 | (72) | 1,292 | (337) | 4,236 | 3,798 | |||||||||||||||||||||||||||||||||||||

| Purchase borrowers (in thousands) | 357 | 415 | (58) | 356 | 1 | 1,378 | 1,131 | |||||||||||||||||||||||||||||||||||||

| Refinance borrowers (in thousands) | 598 | 612 | (14) | 936 | (338) | 2,858 | 2,667 | |||||||||||||||||||||||||||||||||||||

| UPB covered by new CRT issuance (in billions) | $242 | $167 | $75 | $167 | $75 | $828 | $477 | |||||||||||||||||||||||||||||||||||||

| Portfolio Statistics: | ||||||||||||||||||||||||||||||||||||||||||||

| Average guarantee fee rate charged (bps) | 46 | 46 | — | 44 | 2 | 46 | 44 | |||||||||||||||||||||||||||||||||||||

| Weighted average current LTV (%) | 55 | 55 | — | 58 | (3) | 55 | 58 | |||||||||||||||||||||||||||||||||||||

| Weighted average current credit score | 756 | 756 | — | 754 | 2 | 756 | 754 | |||||||||||||||||||||||||||||||||||||

| Loan count (in millions) | 13.1 | 12.8 | 0.3 | 12.0 | 1.1 | 13.1 | 12.0 | |||||||||||||||||||||||||||||||||||||

| Credit-Related Statistics: | ||||||||||||||||||||||||||||||||||||||||||||

| Loan workout activity (in thousands) | 62 | 73 | (11) | 133 | (71) | 317 | 426 | |||||||||||||||||||||||||||||||||||||

| Loans in forbearance, based on loan count (%) | 0.57 | 1.15 | (0.58) | 2.70 | (2.13) | 0.57 | 2.70 | |||||||||||||||||||||||||||||||||||||

| Credit enhancement coverage (%) | 53 | 50 | 3 | 50 | 3 | 53 | 50 | |||||||||||||||||||||||||||||||||||||

(1) First-time homebuyers as a percentage of purchase borrowers with loans secured by primary residences.

Business Highlights

•The company provided funding for approximately 1.0 million single-family loans, nearly 598,000 of which were refinance loans. First-time homebuyers represented 46% of new single-family home purchase loans.

•Single-Family loan workout activity decreased to 62,000 from 133,000 in the fourth quarter of 2020, as the demand for pandemic-related borrower assistance declined throughout 2021.

•0.57% of loans in the Single-Family mortgage portfolio, based on loan count, were in forbearance as of December 31, 2021, down from 2.70% in the fourth quarter of 2020. More than 858,000 forbearance plans have been initiated to help borrowers since January 1, 2020. As of December 31, 2021, approximately 791,000 of these loans have exited forbearance, including 330,000 through reinstatement or payoff and 374,000 through payment deferral.

•Credit enhancement coverage of the Single-Family mortgage portfolio increased to 53% from 50% in the fourth quarter of 2020, primarily due to the new business activity included in credit risk transfer (CRT) transactions.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 6

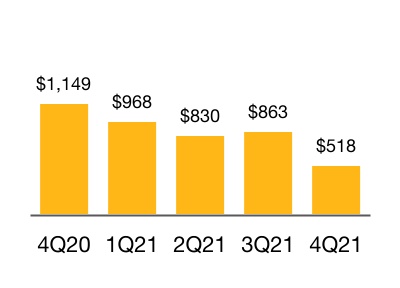

| Multifamily Segment | ||

| Financial Results | ||

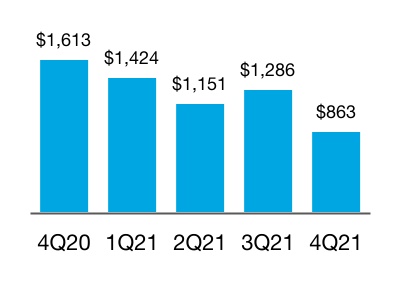

Net Revenues

(In millions)

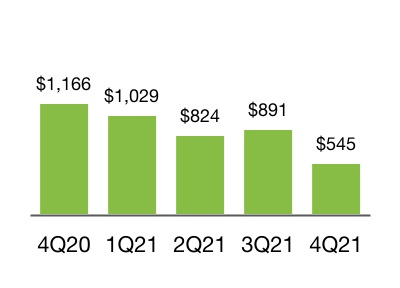

Net Income

(In millions)

Comprehensive Income

(In millions)

| (Dollars in millions) | 4Q 2021 | 3Q 2021 | Change | 4Q 2020 | Change | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||

| Net interest income | $331 | $338 | $(7) | $304 | $27 | $1,307 | $1,179 | |||||||||||||||||||||||||||||||||||||

| Guarantee income | 147 | 266 | (119) | 251 | (104) | 918 | 1,330 | |||||||||||||||||||||||||||||||||||||

| Investment gains (losses), net | 348 | 630 | (282) | 1,013 | (665) | 2,385 | 1,925 | |||||||||||||||||||||||||||||||||||||

| Other income (loss) | 37 | 52 | (15) | 45 | (8) | 114 | 176 | |||||||||||||||||||||||||||||||||||||

| Net revenues | 863 | 1,286 | (423) | 1,613 | (750) | 4,724 | 4,610 | |||||||||||||||||||||||||||||||||||||

| Credit-related income (expense) | 1 | (17) | 18 | 11 | (10) | 55 | (136) | |||||||||||||||||||||||||||||||||||||

| Operating expense | (183) | (156) | (27) | (156) | (27) | (651) | (551) | |||||||||||||||||||||||||||||||||||||

| Income (loss) before income tax (expense) benefit | 681 | 1,113 | (432) | 1,468 | (787) | 4,128 | 3,923 | |||||||||||||||||||||||||||||||||||||

| Income tax (expense) benefit | (136) | (222) | 86 | (302) | 166 | (839) | (809) | |||||||||||||||||||||||||||||||||||||

| Net income (loss) | 545 | 891 | (346) | 1,166 | (621) | 3,289 | 3,114 | |||||||||||||||||||||||||||||||||||||

| Total other comprehensive income (loss), net of taxes and reclassification adjustments | (27) | (28) | 1 | (17) | (10) | (110) | 101 | |||||||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | $518 | $863 | $(345) | $1,149 | $(631) | $3,179 | $3,215 | |||||||||||||||||||||||||||||||||||||

Fourth Quarter 2021 Key Drivers

Net income and comprehensive income decreased year-over-year, mainly driven by:

•Lower guarantee income as continued growth in the Multifamily guarantee portfolio was offset by the impacts of adverse spread changes and loan prepayment activity on the fair values of guarantee assets.

•Lower net investment gains due to spread widening and a smaller volume of loan purchase and securitization activity.

Full-Year 2021 Key Drivers

Net income increased and comprehensive income decreased year-over-year, mainly driven by:

•Lower guarantee income as continued growth in the Multifamily guarantee portfolio was offset by the impacts of higher interest rates on the fair values of guarantee assets.

•Higher net investment gains primarily due to higher pricing margins for new loan purchases and greater spread tightening, partially offset by a smaller volume of new loan purchases as a result of a reduced Multifamily loan purchase cap in 2021.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 7

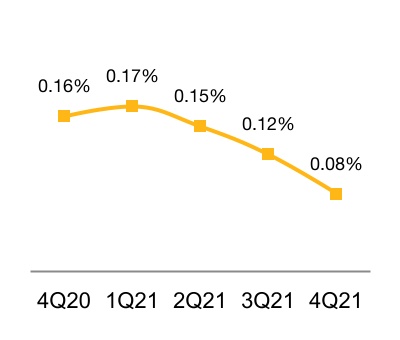

| Multifamily Segment | ||

| Business Results | ||

New Business Activity

(UPB in billions)

Mortgage Portfolio

(UPB in billions)

Delinquency Rate

| 4Q 2021 | 3Q 2021 | Change | 4Q 2020 | Change | 2021 | 2020 | ||||||||||||||||||||||||||||||||||||||

| New Business Statistics: | ||||||||||||||||||||||||||||||||||||||||||||

| Weighted average original LTV (%) | 67 | 67 | — | 70 | (3) | 68 | 69 | |||||||||||||||||||||||||||||||||||||

| Weighted average original debt service coverage ratio | 1.33 | 1.35 | (0.02) | 1.38 | (0.05) | 1.35 | 1.40 | |||||||||||||||||||||||||||||||||||||

| Number of rental units financed (in thousands) | 223 | 161 | 62 | 306 | (83) | 655 | 803 | |||||||||||||||||||||||||||||||||||||

| Affordable ≤ 80% of AMI (% of eligible units acquired) | 57 | 68 | (11) | 71 | (14) | 69 | 71 | |||||||||||||||||||||||||||||||||||||

| Affordable ≤ 120% of AMI (% of eligible units acquired) | 91 | 94 | (3) | 96 | (5) | 94 | 95 | |||||||||||||||||||||||||||||||||||||

| UPB covered by new CRT issuance (in billions) | $23 | $18 | $5 | $26 | $(3) | $84 | $70 | |||||||||||||||||||||||||||||||||||||

| Portfolio Statistics: | ||||||||||||||||||||||||||||||||||||||||||||

| Average guarantee fee rate charged (bps) | 42 | 42 | — | 39 | 3 | 42 | 39 | |||||||||||||||||||||||||||||||||||||

| Unit count (in thousands) | 4,652 | 4,624 | 28 | 4,598 | 54 | 4,652 | 4,598 | |||||||||||||||||||||||||||||||||||||

| Credit-Related Statistics: | ||||||||||||||||||||||||||||||||||||||||||||

| Loans in forbearance, based on UPB (%) | 0.42 | 0.46 | (0.04) | 2.01 | (1.59) | 0.42 | 2.01 | |||||||||||||||||||||||||||||||||||||

| Credit enhancement coverage (%) | 94 | 94 | — | 89 | 5 | 94 | 89 | |||||||||||||||||||||||||||||||||||||

Business Highlights

•The company provided financing for 223,000 multifamily rental units. 57% of eligible multifamily rental units financed were affordable to families earning at or below 80% of area median income (AMI).

•As of December 31, 2021, 0.42% of Multifamily mortgage portfolio loans, based on UPB, were in a COVID-19 forbearance program. 68.7% of these loans were included in securitizations with credit enhancement provided by subordination.

•Credit enhancement coverage of the Multifamily mortgage portfolio increased to 94% from 89% in the fourth quarter of 2020.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 8

About Freddie Mac’s Conservatorship

Since September 2008, Freddie Mac has been operating under conservatorship with FHFA as Conservator. The support provided by Treasury pursuant to the Purchase Agreement enables the company to maintain access to the debt markets and have adequate liquidity to conduct its normal business operations. The amount of funding available to Freddie Mac under the Purchase Agreement was $140.2 billion at December 31, 2021.

Pursuant to the Purchase Agreement, Freddie Mac will not be required to pay a dividend to Treasury on the senior preferred stock until it has built sufficient capital to meet the capital requirements and buffers set forth in the Enterprise Regulatory Capital Framework. As a result, the company was not required to pay a dividend to Treasury on the senior preferred stock in December 2021. As the company builds capital during this period, the quarterly increases in its Net Worth Amount have been, or will be, added to the aggregate liquidation preference of the senior preferred stock. The liquidation preference of the senior preferred stock increased to $98.0 billion on December 31, 2021 based on the $2.9 billion increase in the Net Worth Amount during the third quarter of 2021, and will increase to $100.7 billion on March 31, 2022 based on the $2.7 billion increase in the Net Worth Amount during the fourth quarter of 2021.

Additional Information

For more information, including information related to Freddie Mac’s financial results, conservatorship, and related matters, see the company’s Annual Report on Form 10-K for the year ended December 31, 2021 and the company’s Fourth Quarter 2021 Financial Results Supplement. These documents are available on the Investor Relations page of the company’s website at www.FreddieMac.com.

Additional information about Freddie Mac and its business is also set forth in the company’s other filings with the SEC, which are available on the Investor Relations page of the company’s website at www.FreddieMac.com and the SEC’s website at www.sec.gov. Freddie Mac encourages all investors and interested members of the public to review these materials for a more complete understanding of the company’s financial results and related disclosures.

Webcast Announcement

Management will host a conference call at 9 a.m. Eastern Time on February 10, 2022, to share the company’s results with the media. The conference call will be concurrently webcast. To access the audio webcast, use the following link: https://edge.media-server.com/mmc/p/995zhgex. The replay will be available on the company’s website at www.FreddieMac.com for approximately 30 days. All materials related to the call will be available on the Investor Relations page of the company’s website at www.FreddieMac.com.

| Media Contact: Frederick Solomon (703) 903-3861 | Investor Contact: Laurie Garthune (571) 382-4732 | ||||

* * * *

This press release contains forward-looking statements, which may include statements pertaining to the conservatorship, the company’s current expectations and objectives for its Single-Family and Multifamily segments, its efforts to assist the housing market, liquidity and capital management, economic and market conditions and trends, the effects of the COVID-19 pandemic and actions taken in response thereto on its business, financial condition, and liquidity, its market share, the effect of legislative and regulatory developments and new accounting guidance, credit quality of loans the company owns or guarantees, the costs and benefits of the company’s CRT transactions, and results of operations and financial condition. Forward-looking statements involve known and unknown risks and uncertainties, some of which are beyond the company’s control. Management’s expectations for the company’s future necessarily involve a number of assumptions, judgments, and estimates, and various factors, including changes in market conditions, liquidity, mortgage spreads, credit outlook, uncertainty about the duration, severity, and effects of the COVID-19 pandemic and actions taken in response thereto, actions by the U.S. government (including FHFA, Treasury, and Congress) and state and local governments, and the impacts of legislation or regulations and new or amended accounting guidance, could cause actual results to differ materially from these expectations. These assumptions, judgments, estimates, and factors are discussed in the company’s Annual Report on Form 10-K for the year ended December 31, 2021, which is available on the Investor Relations page of the company’s website at www.FreddieMac.com and the SEC’s website at www.sec.gov. The company undertakes no obligation to update forward-looking statements it makes to reflect events or circumstances occurring after the date of this press release.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 9

Freddie Mac makes home possible for millions of families and individuals by providing mortgage capital to lenders. Since its creation by Congress in 1970, the company has made housing more accessible and affordable for homebuyers and renters in communities nationwide. The company is building a better housing finance system for homebuyers, renters, lenders, and taxpayers. Learn more at FreddieMac.com, Twitter @FreddieMac and Freddie Mac’s blog FreddieMac.com/blog.

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 10

FREDDIE MAC

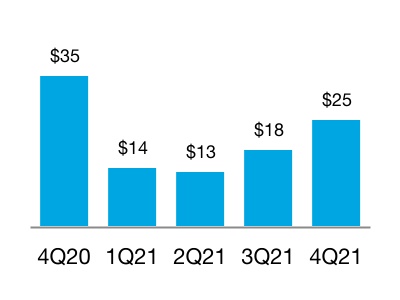

Consolidated Statements of Comprehensive Income (Loss)

(In millions, except share-related amounts) | 4Q 2021 | 3Q 2021 | 4Q 2020 | 2021 | 2020 | |||||||||||||||||||||||||||

| Net interest income | ||||||||||||||||||||||||||||||||

| Interest income | $16,604 | $15,791 | $14,183 | $61,527 | $62,340 | |||||||||||||||||||||||||||

| Interest expense | (11,848) | (11,373) | (10,530) | (43,947) | (49,569) | |||||||||||||||||||||||||||

| Net interest income | 4,756 | 4,418 | 3,653 | 17,580 | 12,771 | |||||||||||||||||||||||||||

| Non-interest income (loss) | ||||||||||||||||||||||||||||||||

| Guarantee income | 182 | 246 | 281 | 1,032 | 1,442 | |||||||||||||||||||||||||||

| Investment gains (losses), net | 519 | 383 | 856 | 2,746 | 1,813 | |||||||||||||||||||||||||||

| Other income (loss) | 108 | 200 | 232 | 593 | 633 | |||||||||||||||||||||||||||

| Non-interest income (loss) | 809 | 829 | 1,369 | 4,371 | 3,888 | |||||||||||||||||||||||||||

| Net revenues | 5,565 | 5,247 | 5,022 | 21,951 | 16,659 | |||||||||||||||||||||||||||

| Benefit (provision) for credit losses | (138) | 243 | 813 | 1,041 | (1,452) | |||||||||||||||||||||||||||

| Non-interest expense | ||||||||||||||||||||||||||||||||

| Salaries and employee benefits | (356) | (352) | (342) | (1,398) | (1,344) | |||||||||||||||||||||||||||

| Other administrative expense | (378) | (275) | (364) | (1,253) | (1,191) | |||||||||||||||||||||||||||

| Total administrative expense | (734) | (627) | (706) | (2,651) | (2,535) | |||||||||||||||||||||||||||

| Credit enhancement expense | (428) | (386) | (327) | (1,518) | (1,058) | |||||||||||||||||||||||||||

| Benefit for (decrease in) credit enhancement recoveries | (32) | (60) | (385) | (542) | 323 | |||||||||||||||||||||||||||

| REO operations income (expense) | (6) | 9 | (10) | (12) | (149) | |||||||||||||||||||||||||||

| Legislated 10 basis point fee expense | (636) | (602) | (495) | (2,342) | (1,836) | |||||||||||||||||||||||||||

| Other expense | (156) | (178) | (243) | (728) | (723) | |||||||||||||||||||||||||||

| Non-interest expense | (1,992) | (1,844) | (2,166) | (7,793) | (5,978) | |||||||||||||||||||||||||||

| Income (loss) before income tax (expense) benefit | 3,435 | 3,646 | 3,669 | 15,199 | 9,229 | |||||||||||||||||||||||||||

| Income tax (expense) benefit | (691) | (727) | (756) | (3,090) | (1,903) | |||||||||||||||||||||||||||

| Net income (loss) | 2,744 | 2,919 | 2,913 | 12,109 | 7,326 | |||||||||||||||||||||||||||

| Other comprehensive income (loss), net of taxes and reclassification adjustments | (22) | (10) | (391) | (489) | 205 | |||||||||||||||||||||||||||

| Comprehensive income (loss) | $2,722 | $2,909 | $2,522 | $11,620 | $7,531 | |||||||||||||||||||||||||||

| Net income (loss) | $2,744 | $2,919 | $2,913 | $12,109 | $7,326 | |||||||||||||||||||||||||||

| Future increase in senior preferred stock liquidation preference | (2,722) | (2,909) | (2,522) | (11,620) | (7,291) | |||||||||||||||||||||||||||

| Net income (loss) attributable to common stockholders | $22 | $10 | $391 | $489 | $35 | |||||||||||||||||||||||||||

| Net income (loss) per common share | $0.01 | $0.00 | $0.12 | $0.15 | $0.01 | |||||||||||||||||||||||||||

| Weighted average common shares outstanding (in millions) | 3,234 | 3,234 | 3,234 | 3,234 | 3,234 | |||||||||||||||||||||||||||

Freddie Mac Fourth Quarter and Full-Year 2021 Financial Results

February 10, 2022

Page 11

FREDDIE MAC

Consolidated Balance Sheets

| December 31, | December 31, | |||||||||||||

(In millions, except share-related amounts) | 2021 | 2020 | ||||||||||||

| Assets | ||||||||||||||

| Cash and cash equivalents (includes $1,695 and $17,379 of restricted cash and cash equivalents) | $10,150 | $23,889 | ||||||||||||

| Securities purchased under agreements to resell | 71,203 | 105,003 | ||||||||||||

| Investment securities, at fair value | 53,015 | 59,825 | ||||||||||||

| Mortgage loans held-for-sale (includes $10,498 and $14,199 at fair value) | 19,778 | 33,652 | ||||||||||||

| Mortgage loans held-for-investment (net of allowance for credit losses of $4,947 and $5,732) | 2,828,331 | 2,350,236 | ||||||||||||

| Accrued interest receivable | 7,474 | 7,754 | ||||||||||||

| Deferred tax assets, net | 6,214 | 6,557 | ||||||||||||

| Other assets (includes $6,594 and $6,980 at fair value) | 29,421 | 40,499 | ||||||||||||

| Total assets | $3,025,586 | $2,627,415 | ||||||||||||

| Liabilities and equity | ||||||||||||||

| Liabilities | ||||||||||||||

| Accrued interest payable | $6,268 | $6,210 | ||||||||||||

| Debt (includes $2,478 and $2,592 at fair value) | 2,980,185 | 2,592,546 | ||||||||||||

| Other liabilities (includes $287 and $958 at fair value) | 11,100 | 12,246 | ||||||||||||

| Total liabilities | 2,997,553 | 2,611,002 | ||||||||||||

| Commitments and contingencies | ||||||||||||||

| Equity | ||||||||||||||

Senior preferred stock (liquidation preference of $97,959 and $86,539) | 72,648 | 72,648 | ||||||||||||

| Preferred stock, at redemption value | 14,109 | 14,109 | ||||||||||||

| Common stock, $0.00 par value, 4,000,000,000 shares authorized, 725,863,886 shares issued and 650,059,553 shares and 650,059,292 shares outstanding | — | — | ||||||||||||

| Additional paid-in capital | — | — | ||||||||||||

| Retained earnings (accumulated deficit) | (54,993) | (67,102) | ||||||||||||

| AOCI, net of taxes, related to: | ||||||||||||||

| Available-for-sale securities | 297 | 810 | ||||||||||||

| Other | (143) | (167) | ||||||||||||

| Total AOCI, net of taxes | 154 | 643 | ||||||||||||

| Treasury stock, at cost, 75,804,333 shares and 75,804,594 shares | (3,885) | (3,885) | ||||||||||||

| Total equity | 28,033 | 16,413 | ||||||||||||

| Total liabilities and equity | $3,025,586 | $2,627,415 | ||||||||||||

| The table below presents the carrying value and classification of the assets and liabilities of consolidated variable interest entities (VIEs) on the company's consolidated balance sheets. | ||||||||||||||

| December 31, | December 31, | |||||||||||||

| (In millions) | 2021 | 2020 | ||||||||||||

| Consolidated Balance Sheet Line Item | ||||||||||||||

| Assets: | ||||||||||||||

| Mortgage loans held-for-investment | $2,784,626 | $2,273,347 | ||||||||||||

| All other assets | 54,300 | 83,982 | ||||||||||||

| Total assets of consolidated VIEs | $2,838,926 | $2,357,329 | ||||||||||||

| Liabilities: | ||||||||||||||

| Debt | $2,803,054 | $2,308,176 | ||||||||||||

| All other liabilities | 5,823 | 5,610 | ||||||||||||

| Total liabilities of consolidated VIEs | $2,808,877 | $2,313,786 | ||||||||||||