Exhibit 99.3

FELDMAN FINANCIAL ADVISORS, INC.

1001 CONNECTICUT AVENUE, NW— SUITE 840

WASHINGTON, DC 20036

202-467-6862— (FAX) 202-467-6963

Eagle Bancorp Montana, Inc.

Helena, Montana

Conversion Valuation Appraisal Report

Valued as of December 3, 2009

Prepared By

Feldman Financial Advisors, Inc.

Washington, D.C.

FELDMAN FINANCIAL ADVISORS, INC.

| 1001 CONNECTICUT AVENUE, NW — SUITE 840 | ||

| WASHINGTON, DC 20036 | ||

| 202-467-6862— (FAX) 202-467-6963 | ||

| December 3, 2009 | ||

Board of Directors

Eagle Bancorp Montana

1400 Prospect Avenue

Helena, Montana 59601

Members of the Board:

At your request, we have completed and hereby provide an updated independent appraisal (the “Appraisal”) of the estimated pro forma market value of the common stock to be issued (the “Stock Offering”) by Eagle Bancorp Montana, Inc. (“Eagle Montana” or the “Company”), Helena, Montana, as of December 3, 2009, in connection with the mutual-to-stock conversion of Eagle Financial, MHC (the “MHC”). Currently, the MHC’s principal activity is the ownership of the majority interest approximating 60.4% in Eagle Bancorp, Inc. (“Bancorp” or “Mid-Tier”), the mid-tier holding company for American Federal Savings Bank (the “Bank”). The remainder of the Mid-Tier’s shares (39.6%) is owned by public stockholders. Bancorp owns a 100% interest in the common stock of the Bank. At the conclusion of the conversion, the MHC will no longer exist. Eagle Montana is offering for sale common stock representing the majority ownership interest Bancorp that is currently held by Eagle Financial, MHC in a subscription offering to Eligible Account Holders, Supplemental Eligible Account Holders and Other Members. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale in a community offering to current holders of Bancorp shares as of the Record Date, members of the local community and the public at large. At the conclusion of the conversion, existing public stockholders of Bancorp, Inc. will receive new shares of common stock of the Company in exchange for their existing Bancorp Shares. This Appraisal has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” of the OTS.

Feldman Financial Advisors, Inc. (“Feldman Financial”) is a financial consulting and economic research firm that specializes in financial valuations and analyses of business enterprises and securities in the thrift, banking, and mortgage industries. The background of Feldman Financial is presented in Exhibit I. In preparing the Appraisal, we conducted an analysis of the Company that included discussions with the Company’s management, the Company’s legal counsel, Nixon Peabody LLP, and the Company’s independent auditor, Davis, Kinard & Co., P.C. In addition, where appropriate, we considered information based on other available published sources that we believe are reliable; however, we cannot guarantee the accuracy and completeness of such information.

FELDMAN FINANCIAL ADVISORS, INC.

Board of Directors

Eagle Bancorp Montana, Inc.

December 3, 2009

Page Two

We also reviewed, among other factors, the economy in the Company’s primary market area and compared the Company’s financial condition and operating performance with that of selected publicly traded thrift institutions. We reviewed conditions in the securities markets in general and in the market for thrift institution common stocks in particular.

The Appraisal is based on the Company’s representation that the information contained in the Prospectus and additional evidence furnished to us by the Company and its independent auditor are truthful, accurate, and complete. We did not independently verify the financial statements and other information provided by the Company and its independent auditor, nor did we independently value the assets or liabilities of the Company. The Appraisal considers the Company only as a going concern and should not be considered as an indication of the liquidation value of the Company.

It is our opinion that, as of December 3, 2009, the estimated pro forma market value of the Company on a fully converted basis was within a range (the “Valuation Range”) of $33,801,360 to $45,731,250 with a midpoint of $39,766,300. Assuming an additional 15% increase above the maximum value would result in an adjusted maximum of $52,590,930. After consideration of the exchange of existing publicly held shares and the offering of the MHC’s 60.4% ownership interest to the public, assuming an offering price of $10.00 per share of common stock, the Company will offer a minimum of 2,040,00 shares, a midpoint of 2,400,000 shares, a maximum of 2,760,000 shares, and an adjusted maximum of 3,174,000 shares.

OTS regulations provide that in a conversion of a mutual holding company, the minority stockholders are entitled to exchange their current shares for newly issued shares of the fully converted Company. It is our understanding that the exchange ratio has been designed to preserve the current aggregate percentage ownership in Bancorp equal to 39.6%. The actual exchange ratio to be received by the existing minority shareholders of Bancorp will be determined at the end of the offering, based on the total number of shares sold in the subscription and community offerings. Based on this calculation, and the valuation offering range above, the Company’s legal exchange ratio would be 3.1548 shares, 3.7009 shares, 4.256 shares and 4.8944 shares at the minimum, midpoint, maximum and adjusted maximum of the offering range, respectively. Feldman Financial has no opinion on the proposed exchange ratio applied to the minority shares exchanged for newly issued shares of the Company.

FELDMAN FINANCIAL ADVISORS, INC.

Board of Directors

Eagle Bancorp Montana, Inc.

December 3, 2009

Page Three

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of common stock in the Stock Offering. Moreover, because the Appraisal is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of stock in the Stock Offering will thereafter be able to sell such shares at prices related to the foregoing estimate of the Company’s pro forma market value. Feldman Financial is not a seller of securities within the meaning of any federal or state securities laws and any report prepared by Feldman Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities.

The valuation reported herein will be updated as appropriate. Further updates will consider, among other factors, any developments or changes in the Company’s operating performance, financial condition, or management policies, and current conditions in the securities markets for thrift institution common stocks. Should any such new developments or changes be material, in our opinion, to the valuation of the Company, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in detail at that time.

Respectfully submitted, |

Feldman Financial Advisors, Inc. |

|

| Trent R. Feldman |

President |

|

| Greg E. Izydorczyk |

| Senior Vice President |

FELDMAN FINANCIAL ADVISORS, INC.

TABLE OF CONTENTS

TAB | PAGE | |||||

| INTRODUCTION | 1 | |||||

| I. | Chapter One – BUSINESS OF EAGLE BANCORP MONTANA | |||||

| General Overview | 4 | |||||

| Financial Condition | 7 | |||||

| Income and Expense Trends | 31 | |||||

| Interest Rate Risk Management | 41 | |||||

| Asset Quality | 43 | |||||

| Market Area | 49 | |||||

| Summary Outlook | 54 | |||||

| II. | Chapter Two – COMPARISONS WITH PUBLICLY HELD THRIFTS | |||||

| General Overview | 55 | |||||

| Selection Criteria | 56 | |||||

| Recent Financial Comparisons | 60 | |||||

| III. | Chapter Three – MARKET VALUE ADJUSTMENTS | |||||

| General Overview | 72 | |||||

| Earnings Prospects | 72 | |||||

| Financial Condition | 74 | |||||

| Market Area | 75 | |||||

| Management | 75 | |||||

| Dividend Policy | 76 | |||||

| Liquidity of the Issue | 76 | |||||

| Subscription Interest | 76 | |||||

| Stock Market Conditions | 78 | |||||

| Recent Acquisition Activity | 81 | |||||

| Marketability Discount | 81 | |||||

| Effect of Government Regulations and Regulatory Reform | 84 | |||||

| Adjustments Conclusion | 84 | |||||

| Valuation Approach | 85 | |||||

| Valuation Conclusion | 88 | |||||

| IV. | Appendix – EXHIBITS | |||||

| I | Background of Feldman Financial Advisors, Inc. | I-1 | ||||

| II-1 | Statement of Financial Condition | II-1 | ||||

| II-2 | Statement of Operations | II-2 | ||||

| II-3 | Loan Portfolio Composition | II-3 | ||||

| II-4 | Investment Portfolio Composition | II-4 | ||||

| II-5 | Deposit Account Distribution | II-5 | ||||

| III | Financial and Market Data for All Public Thrifts | III-1 | ||||

| IV-1 | Pro Forma Assumptions for Second-Stage Conversion Valuation | IV-1 | ||||

| IV-2 | Pro Forma Second-Stage Conversion Valuation Range | IV-2 | ||||

| IV-3 | Pro Forma Second-Stage Conversion Analysis at Midpoint | IV-3 | ||||

| IV-4 | Comparative Discount and Premium Analysis | IV-4 | ||||

i

FELDMAN FINANCIAL ADVISORS, INC.

LIST OF TABLES

TAB | PAGE | |||||

| I. | Chapter One – BUSINESS OF EAGLE BANCORP MONTANA | |||||

Table 1 | Selected Financial Condition Data | 7 | ||||

Table 2 | Selected Income Statement Information | 8 | ||||

Table 3 | Selected Financial and Performance Ratios | 9 | ||||

Table 4 | Loan Portfolio | 14 | ||||

Table 5 | Loan Originations | 21 | ||||

Table 6 | Securities Portfolio | 24 | ||||

Table 7 | Securities Portfolio by Contractual Maturity | 26 | ||||

Table 8 | Deposit Portfolio | 27 | ||||

Table 9 | Borrowings | 30 | ||||

Table 10 | Summary Income Statement Data | 31 | ||||

Table 11 | Average Balances and Yields | 32 | ||||

Table 12 | Rate/Volume Analysis | 34 | ||||

Table 13 | Interest Rate Risk Analysis | 42 | ||||

Table 14 | Nonperforming Asset Summary | 44 | ||||

Table 15 | Allowance for Loan Loss Summary | 45 | ||||

Table 16 | Allocation of Allowance for Loan Losses | 46 | ||||

Table 17 | Selected Demographic Data | 51 | ||||

Table 18 | Deposit Market Share by County | 53 | ||||

| II. | Chapter Two – COMPARISONS WITH PUBLICLY HELD THRIFTS | |||||

Table 19 | Comparative Group Operating Summary | 59 | ||||

Table 20 | Key Financial Comparisons | 62 | ||||

Table 21 | General Financial Performance Ratios | 66 | ||||

Table 22 | Income and Expense Analysis | 67 | ||||

Table 23 | Yield-Cost Structure and Growth Rates | 68 | ||||

Table 24 | Balance Sheet Composition | 69 | ||||

Table 25 | Regulatory Capital, Credit Risk, and Loan Composition | 70 | ||||

| III. | Chapter Three – MARKET VALUE ADJUSTMENTS | |||||

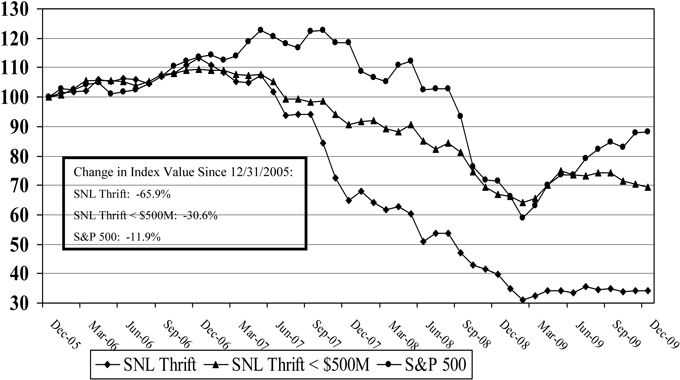

Table 26 | Comparative Stock Index Performance | 80 | ||||

Table 27 | Summary of Recent Acquisition Activity | 83 | ||||

Table 28 | Summary of Recent Second-Step Stock Offerings | 84 | ||||

Table 29 | Pro Forma Comparative Market Valuation Analysis | 89 | ||||

ii

FELDMAN FINANCIAL ADVISORS, INC.

INTRODUCTION

At your request, we have completed and hereby provide an independent appraisal (the “Appraisal”) of the estimated pro forma market value of the common stock to be issued (the “Stock Offering”) by Eagle Bancorp Montana, Inc. (“Eagle Montana” or the “Company”), Helena, Montana, as of December 3, 2009, in connection with the mutual-to-stock conversion of Eagle Financial, MHC (the “MHC”). Currently, the MHC’s principal activity is the ownership of the majority interest approximating 60.4% in Eagle Bancorp (“Bancorp” or “Mid-Tier”), the mid-tier holding company for American Federal Savings Bank (the “Bank”). Public stockholders own the remainder of the Mid-Tier’s shares (39.6%). Bancorp owns a 100% interest in the common stock of the Bank. At the conclusion of the conversion, the MHC will no longer exist. As part of the conversion, the Company is offering for sale common stock representing the majority ownership interest in Bancorp currently held by Eagle Financial, MHC in a subscription offering to Eligible Account Holders, Supplemental Eligible Account Holders and Other Members. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale in a community offering to current holders of Bancorp shares as of the Record Date, members of the local community and the public at large. At the conclusion of the conversion, existing public stockholders of Bancorp will receive new shares of common stock (adjusted for an exchange ratio) of the Company in exchange for their existing Bancorp Shares. This Appraisal has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” of the Office of Thrift Supervision (“OTS”).

1

FELDMAN FINANCIAL ADVISORS, INC.

In the course of preparing the Appraisal, we reviewed and discussed with the Company’s management and the Company’s independent accountants, Davis, Kinard & Co., P.C., the audited financial statements of the Company’s operations for the years ended June 30, 2008 and 2009 and unaudited financials for the three-month period ended September 30, 2009. We also reviewed and discussed with management other financial matters of the Bank.

Where appropriate, we considered information based upon other available public sources, which we believe to be reliable; however, we cannot guarantee the accuracy or completeness of such information. We visited the Company’s primary market area and examined the prevailing economic conditions. We also examined the competitive environment within which the Company operates and assessed the Company’s relative strengths and weaknesses.

We examined and compared the Company’s financial performance with selected segments of the thrift industry and selected publicly traded thrift institutions. We reviewed conditions in the securities markets in general and the market for thrift institution common stocks in particular. We included in our analysis an examination of the potential effects of the Stock Offering on the Company’s operating characteristics and financial performance as they relate to the estimated pro forma market value of the Company.

In preparing the Appraisal, we have relied upon and assumed the accuracy and completeness of financial and statistical information provided by the Company and its independent accountants. We did not independently verify the financial statements and other information provided by the Company and its independent accountants, nor did we independently value the assets or liabilities of the Company. The Appraisal considers the Company only as a going concern and should not be considered as an indication of the liquidation value of the Company.

2

FELDMAN FINANCIAL ADVISORS, INC.

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of common stock in the Stock Offering. Moreover, because such the Appraisal is necessarily based on estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of common stock in the Stock Offering will thereafter be able to sell such shares at prices related to the foregoing estimate of the Company’s pro forma market value. Feldman Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by Feldman Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities.

The valuation reported herein will be updated as appropriate. Future updates will consider, among other factors, any developments or changes in the Company’s financial performance or management policies, and current conditions in the securities market for thrift institution common stocks. Should any such developments or changes be material, in our opinion, to the Stock Offering valuation of the Company, appropriate adjustments to the estimated pro forma market value may be made. The reasons for any such adjustments will be explained in detail at that time.

3

FELDMAN FINANCIAL ADVISORS, INC.

I. BUSINESS OF EAGLE BANCORP MONTANA, INC.

General Overview

Eagle Montana is a newly formed Delaware corporation incorporated in December 2009 to be the successor corporation to Eagle Bancorp upon completion of the conversion. Eagle Montana will own all of the outstanding shares of common stock of American Federal Savings Bank upon completion of the conversion. Currently, Eagle Bancorp, the mid-tier stock holding company formed in 2000 owns all of the capital stock of the Bank. The mid-tier holding company is 60.4% owed by Eagle Financial, MHC and 39.6% owned by public shareholders. After the conversion, Eagle Financial, MHC will no longer exist. In addition, as part of the conversion, existing public stockholders of Bancorp will receive new shares of common stock in Eagle Montana in exchange for their existing shares of common stock of Bancorp. Eagle Montana’s executive offices are located at 1400 Prospect Avenue, Helena, Montana 59601.

American Federal Savings Bank is a federally chartered savings bank headquartered in Helena, Montana. The Bank was founded in 1922 as a Montana chartered building and loan association. In 1975, the Bank adopted a federal thrift charter and, in 2000, reorganized from the mutual (meaning no stockholders) structure into the mutual holding company structure, thereby becoming partially stockholder-owned. American Federal Savings Bank became the wholly owned subsidiary of Eagle Bancorp, a federal corporation, in 2000. The Bank currently operates seven retail-banking locations and seven automated teller machines in south central Montana. The Office of Thrift Supervision and the Federal Deposit Insurance Corporation regulate the Bank. At September 30, 2009, the Company had total assets of $300.7 million, deposits of $195.1 million and equity capital of $30.4 million.

4

FELDMAN FINANCIAL ADVISORS, INC.

The Bank’s primary lines of business are:

| • | Retail Lending.The Bank originates residential mortgage loans, home equity loans, and consumer loans primarily through its community banking office network. The Bank also offers its customers the choice of submitting online mortgage loan applications and receiving pre-approvals through the Bank’s website. |

| • | Commercial Lending.The Bank continues to place an emphasis on growing its commercial business and commercial real estate loan portfolios. In addition to commercial real estate loans, the Bank offers traditional business loans structured as unsecured lines of credit or loans secured by inventory, accounts receivable or other business assets. The Bank seeks to provide exceptional service with local decision-making and personal attention. |

| • | Deposit Products and Services.The Bank offers a full range of traditional deposit products such as checking accounts, savings accounts, money market accounts, retirement accounts, and certificates of deposit. These products can have additional features such as direct deposit, ATM and check card services, overdraft protection, telephone banking and Internet banking, thereby providing customers multiple channels to access their accounts. |

| • | Mortgage Servicing.The Bank provides loan servicing for other institutions. These services generally consist of collecting mortgage payments, maintaining escrow accounts, disbursing payments to investors and foreclosure processing. |

The Bank faces strong competition in its primary market area for the attraction of retail deposits and the origination of loans. Historically, Montana was a unit banking state. This means that the ability of Montana state banks to create branches was either prohibited or significantly restricted. As a result of unit banking, Montana has a significant number of independent financial institutions serving a single community in a single location. While the state’s population is approximately 973,000 people, there are 59 credit unions in Montana as well as two federally chartered thrift institutions, and 77 commercial banks as of June 30, 2009.

5

FELDMAN FINANCIAL ADVISORS, INC.

The Bank’s most direct competition for depositors has historically come from locally owned and out-of-state commercial banks, thrift institutions and credit unions operating in the Bank’s primary market area. The number of such competitor locations has increased significantly in recent years. Competition for loans also comes from banks, thrifts and credit unions in addition to mortgage bankers and brokers. The Bank’s principal market areas can be characterized as markets with moderately increasing incomes, relatively low unemployment, increasing wealth (particularly in the growing resort areas such as Bozeman), and moderate population growth. The ability of the Company to compete successfully is a significant factor affecting growth potential and profitability.

The Company’s primary reasons for converting to the stock holding company structure and raising additional capital through the offering are:

| • | to fund a loan to the employee stock ownership plan to purchase shares of common stock in the offering; |

| • | to finance, where opportunities are presented, the acquisition of financial institutions or other financial service companies as opportunities arise, particularly in, or adjacent to, south central Montana, although the Company does not currently have any agreements or understandings regarding any specific acquisition transaction and it is impossible to determine when, if ever, such opportunities may arise; |

| • | to pay cash dividends to stockholders; |

| • | to repurchase shares of our common stock for, among other things, the funding of our stock-based incentive plan; |

| • | to invest in securities; and |

| • | to use the additional capital for other general corporate purposes. |

The remainder of Chapter I examines in more detail the trends addressed in this section, including the impact of changes in the Company’s economic and competitive environment, and recent management initiatives. The discussion is supplemented by the exhibits in the Appendix. Exhibit II-1 summarizes the Company’s consolidated balance sheets as of the years ended June 30, 2008 and 2009 and the three month period ended September 30, 2009. Exhibit II-2 presents the Company’s consolidated income statements for the years ended June 30, 2007 to 2009 and the three-month periods ended September 30, 2008 and 2009.

6

FELDMAN FINANCIAL ADVISORS, INC.

Financial Condition

Table 1 presents selected data concerning the Company’s financial position as of September 30, 2009 and June 30 2005 to 2009 while Table 2 details selected income statement data for the three month periods ended September 30, 2008 and 2009 and for the years ended June 30, 2005 to 2009. Table 3 details selected financial performance data for the three-month periods ended September 30, 2008 and 2009 and for the years ended June 30, 2005 to 2009.

Table 1

Selected Financial Condition Data

As of September 30, 2009 and June 30, 2005 to 2009

| At Sept. 30, | At June 30, | |||||||||||||||||

| 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||

| (in thousands) | ||||||||||||||||||

Balance Sheet Data: | ||||||||||||||||||

Total assets | $ | 300,680 | $ | 289,709 | $ | 279,907 | $ | 244,686 | $ | 226,178 | $ | 206,414 | ||||||

Investment securities, available-for-sale | 92,100 | 82,263 | 78,417 | 64,774 | 64,198 | 75,227 | ||||||||||||

Investment securities, held-to-maturity | 265 | 375 | 697 | 921 | 1,018 | 1,201 | ||||||||||||

Loans receivable, net: | ||||||||||||||||||

Residential mortgages | 76,711 | 79,216 | 86,751 | 81,958 | 75,913 | 56,533 | ||||||||||||

Real estate construction | 6,119 | 4,642 | 7,317 | 8,253 | 6,901 | 2,723 | ||||||||||||

Home equity | 28,836 | 28,676 | 28,034 | 24,956 | 20,191 | 16,801 | ||||||||||||

Consumer | 11,074 | 10,835 | 11,558 | 11,438 | 11,820 | 10,909 | ||||||||||||

Commercial (1) | 46,005 | 44,254 | 34,699 | 31,987 | 26,509 | 20,347 | ||||||||||||

Total loans receivable, net | 168,185 | 167,197 | 168,149 | 158,140 | 140,858 | 106,839 | ||||||||||||

Mortgage loans held for sale | 3,494 | 5,349 | 7,370 | 1,175 | 918 | 2,148 | ||||||||||||

Mortgage servicing rights, net | 2,315 | 2,208 | 1,652 | 1,628 | 1,722 | 1,857 | ||||||||||||

Deposits | 195,080 | 187,199 | 178,851 | 179,647 | 174,342 | 172,497 | ||||||||||||

FHLB advances | 66,639 | 67,056 | 65,222 | 30,000 | 22,371 | 9,885 | ||||||||||||

Subordinated debentures | 5,155 | 5,155 | 5,155 | 5,155 | 5,155 | — | ||||||||||||

Shareholders’ equity | 30,427 | 27,792 | 25,634 | 24,088 | 22,545 | 22,265 | ||||||||||||

| (1) | Includes commercial real estate and land loans and commercial business loans. |

Source: Eagle Montana, preliminary prospectus.

7

FELDMAN FINANCIAL ADVISORS, INC.

Table 2

Selected Income Statement Information

For the Three Months Ended September 30, 2008 and 2009

For the Years Ended December 31, 2005 to 2009

| For the Three Months Ended September 30, | For the Year Ended June 30, | ||||||||||||||||||||||

| 2009 | 2008 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||||

| (Dollars in thousands, except per share amounts) | |||||||||||||||||||||||

Operating Data: | |||||||||||||||||||||||

Total interest income | $ | 3,724 | $ | 3,816 | $ | 15,348 | $ | 14,098 | $ | 12,651 | $ | 10,506 | $ | 9,043 | |||||||||

Total interest expense | 1,341 | 1,580 | 6,115 | 6,662 | 5,966 | 3,792 | 2,563 | ||||||||||||||||

Net interest income | 2,383 | 2,236 | 9,233 | 7,436 | 6,685 | 6,714 | 6,480 | ||||||||||||||||

Provision (credit) for loan losses | 135 | — | 257 | (175 | ) | — | — | — | |||||||||||||||

Net interest income after provision for loan losses | 2,248 | 2,236 | 8,976 | 7,611 | 6,685 | 6,714 | 6,480 | ||||||||||||||||

Noninterest income | 1,061 | (504 | ) | 2,999 | 2,224 | 2,261 | 2,165 | 2,059 | |||||||||||||||

Noninterest expense | 2,103 | 1,849 | 8,563 | 7,063 | 6,614 | 6,465 | 6,181 | ||||||||||||||||

Income (loss) before income taxes | 1,206 | (117 | ) | 3,412 | 2,772 | 2,332 | 2,414 | 2,358 | |||||||||||||||

Income tax expense (benefit) | 362 | (17 | ) | 1,024 | 662 | 554 | 629 | 615 | |||||||||||||||

Net income (loss) | $ | 844 | $ | (100 | ) | $ | 2,388 | $ | 2,110 | $ | 1,778 | $ | 1,785 | $ | 1,743 | ||||||||

Earnings (loss) per share: | |||||||||||||||||||||||

Basic | $ | 0.79 | $ | (0.09 | ) | $ | 2.23 | $ | 1.97 | $ | 1.66 | $ | 1.66 | $ | 1.55 | ||||||||

Diluted | $ | 0.69 | $ | (0.08 | ) | $ | 1.96 | $ | 1.74 | $ | 1.47 | $ | 1.48 | $ | 1.45 | ||||||||

Source: Eagle Montana, preliminary prospectus.

8

FELDMAN FINANCIAL ADVISORS, INC.

Table 3

Selected Financial and Performance Ratios

For the Three Months Ended September 30, 2008 and 2009

For the Years Ended December 31, 2005 to 2009

| At or For the Three Months Ended September 30, (1) | At or For the Year Ended June 30, | ||||||||||||||||||||

| 2009 | 2008 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||

Financial Ratios and Other Data: | |||||||||||||||||||||

Return on average assets (2) | 1.14 | % | (0.14 | )% | 0.84 | % | 0.83 | % | 0.75 | % | 0.83 | % | 0.86 | % | |||||||

Return on average equity (3) | 11.60 | % | (1.59 | )% | 9.19 | % | 8.25 | % | 7.41 | % | 7.88 | % | 7.48 | % | |||||||

Net interest rate spread (4) | 3.40 | % | 3.26 | % | 3.34 | % | 2.84 | % | 2.76 | % | 3.21 | % | 3.36 | % | |||||||

Net interest margin (5) | 3.58 | % | 3.50 | % | 3.52 | % | 3.15 | % | 3.06 | % | 3.41 | % | 3.51 | % | |||||||

Noninterest expense to average assets | 2.86 | % | 2.67 | % | 3.00 | % | 2.77 | % | 2.79 | % | 3.01 | % | 3.06 | % | |||||||

Efficiency ratio | 63.55 | % | 106.76 | % | 71.51 | % | 71.81 | % | 73.93 | % | 72.81 | % | 72.39 | % | |||||||

Noninterest income to average assets | 1.44 | x | (0.73 | )x | 1.05 | x | 0.87 | x | 0.95 | x | 1.01 | x | 1.02 | x | |||||||

Dividend payout ratio (6) | 13.15 | % | NM | 18.21 | % | 19.67 | % | 21.71 | % | 20.11 | % | 20.83 | % | ||||||||

Net interest income to noninterest expense | 1.13 | x | 1.21 | x | 1.08 | x | 1.05 | x | 1.01 | x | 1.04 | x | 1.05 | x | |||||||

Average interest-earning assets to average interest-bearing liabilities | 1.085 | x | 1.096 | x | 1.078 | x | 1.108 | x | 1.107 | x | 1.107 | x | 1.112 | x | |||||||

Nonperforming loans to net loans receivable | 0.93 | % | 0.04 | % | 0.75 | % | 0.02 | % | 0.13 | % | 0.33 | % | 0.47 | % | |||||||

Nonperforming assets to total assets | 0.52 | % | 0.03 | % | 0.43 | % | 0.01 | % | 0.09 | % | 0.20 | % | 0.24 | % | |||||||

Allowance for loan losses to net loans receivable | 0.37 | % | 0.17 | % | 0.31 | % | 0.18 | % | 0.33 | % | 0.38 | % | 0.54 | % | |||||||

Allowance for loan losses to nonperforming loans | 39.56 | % | 400.00 | % | 41.90 | % | 937.50 | % | 244.34 | % | 141.91 | % | 132.03 | % | |||||||

Average capital to average assets | 9.78 | % | 9.06 | % | 9.09 | % | 10.02 | % | 10.12 | % | 10.54 | % | 11.55 | % | |||||||

Capital to total assets | 10.12 | % | 8.51 | % | 9.59 | % | 9.16 | % | 9.84 | % | 9.97 | % | 10.79 | % | |||||||

Tangible equity to tangible assets | 10.12 | % | 8.51 | % | 9.59 | % | 9.16 | % | 9.84 | % | 9.97 | % | 10.49 | % | |||||||

Number of branch offices | 7 | 5 | 6 | 5 | 5 | 5 | 5 | ||||||||||||||

| (1) | Ratios are annualized where appropriate. |

| (2) | Represents net income divided by average total assets. |

| (3) | Represents net income divided by average equity. |

| (4) | Represents average yield on interest-earning assets less average cost of interest-bearing liabilities. |

| (5) | Represents net interest income as a percentage of average interest-earning assets. |

| (6) | The dividend payout ratio represents dividends declared per share divided by net income per share. |

Source: Eagle Montana, preliminary prospectus.

9

FELDMAN FINANCIAL ADVISORS, INC.

Asset Composition

The Company’s total assets experienced relatively steady growth, increasing by a compound annual rate of 8.5% from $206.4 million at June 30, 2005 to $300.7 million at September 30, 2009. The net asset expansion of approximately $94.3 million over this period occurred primarily in the loan portfolio. The loan portfolio increased from $106.8 million at June 30, 2005 to $168.2 million at September 30, 2009, an increase of $61.3 million. The ratio of loans to total assets increased from 51.8% at June 30, 2005 to 55.9% at September 30, 2009.

Comparison of Financial Condition at September 30, 2009 and June 30, 2009

Total assets increased by $10.97 million, or 3.79%, to $300.68 million at September 30, 2009, from $289.71 million at June 30, 2009. Total liabilities increased by $8.34 million to $270.25 million at September 30, 2009, from $261.92 million at June 30, 2009. Total equity increased $2.64 million to $30.43 million at September 30, 2009, from $27.79 million at June 30, 2009.

Loans receivable increased $988,000, or 0.59%, to $168.19 million at September 30, 2009 from $167.20 million at June 30, 2009. Commercial real estate loans were the loan category with the largest increase, $2.05 million, while residential mortgage loans decreased $2.51 million. Real estate construction loans also increased $1.48 million. Most other loan categories showed modest changes. Total loan originations were $43.07 million for the three months ended September 30, 2009, with single family mortgages accounting for $29.02 million of the total. Home equity and construction loan originations totaled $4.17 million and $2.5 million, respectively, for the same period. Commercial real estate and land loan originations totaled $3.47 million. Loans held-for-sale decreased to $3.49 million at September 30, 2009, from $5.35 million at June 30, 2009.

10

FELDMAN FINANCIAL ADVISORS, INC.

Deposits grew $7.88 million, or 4.21%, to $195.08 million at September 30, 2009 from $187.20 million at June 30, 2009. Growth in certificates of deposit and non-interest checking, interest-bearing checking accounts, and savings accounts contributed to the increase in deposits. Money market accounts declined slightly. Advances from the Federal Home Loan Bank of Seattle and other borrowings decreased $417,000, or 0.62%, to $66.64 million at September 30, 2009 from $67.06 million at June 30, 2009.

The increase in total equity was the result of net income of $844,000 for the three months ended September 30, 2009 and an increase in other comprehensive income of $1.89 million (mainly due to an increase in net unrealized gain on securities available-for-sale), offset by dividends paid, consisting of a $0.26 per share regular cash dividend, and treasury stock purchases.

Comparison of Financial Condition at June 30, 2009 and June 30, 2008

Total assets increased $9.80 million, or 3.50%, to $289.71 million at June 30, 2009, compared to $279.91 million at June 30, 2008. Total liabilities increased by $7.64 million, or 3.01%, to $261.92 million at June 30, 2009, from $254.27 million at June 30, 2008. The loan portfolio decreased $952,000 during the year. Total deposits increased $8.35 million. Noninterest checking increased $385,000 or 2.63%, to $15.00 million at June 30, 2009, and money market accounts increased $1.61 million, or 6.37%. Interest bearing checking and certificates of deposits increased $1.94 million, or 7.68%, and $1.87 million, or 2.22%, respectively. These increased deposits funded much of the asset growth.

11

FELDMAN FINANCIAL ADVISORS, INC.

Loans receivable decreased $952,000, or 0.57% to $167.20 million from $168.15 million. Significant refinancing activity contributed to the lower loan balances. $131.23 million in loans were sold during fiscal year 2009, an increase of $79.16 million from fiscal year 2008’s amount of $52.07 million. Origination activity on all loan categories with the exception of real estate construction loans and home equity loans increased in the current fiscal year. Commercial real estate and land loans increased $8.51 million during the year, and residential mortgage loans decreased $7.52 million. The available-for-sale investment portfolio increased $3.85 million, or 4.90%, to $82.26 million at June 30, 2009 from $78.42 million at June 30, 2008. The investment category with the largest increase was municipal obligations, which increased $6.70 million.

Total deposits increased $8.35 million. Of that amount, certificates of deposit increased $1.87 million, to $86.20 million at June 30, 2009 from $84.33 million at June 30, 2008. The Bank had no brokered deposits as of June 30, 2009. Interest-earning checking accounts increased $1.94 million while noninterest checking increased $385,000. Money market accounts increased $1.61 million and savings accounts increased $2.54 million. Deposit growth is expected to continue to be difficult to achieve due to fierce competition among financial institutions in the Bank’s markets. Advances from the Federal Home Loan Bank and other borrowings decreased to $67.06 million at year-end 2009 from $68.22 million at year-end 2008, a decrease of $1.17 million.

Total shareholders’ equity was $27.79 million at June 30, 2009, an increase of $2.16 million. This increase was the result of net income for the year and a decrease in accumulated other comprehensive loss of $240,000 (mainly due to a decrease in net unrealized loss on securities available-for-sale), partially offset by the purchase of treasury stock and dividends paid during the year.

12

FELDMAN FINANCIAL ADVISORS, INC.

Table 4 and Exhibit II-3 analyze the composition of the loan portfolio by loan category at the dates indicated. American Federal Savings Bank primarily originates one- to four-family residential real estate loans and, to a lesser extent, commercial real estate loans, real estate construction loans, home equity loans, consumer loans and commercial loans. Commercial real estate loans include loans on multi-family dwellings, loans on nonresidential property and loans on developed and undeveloped land. Home equity loans include loans secured by the borrower’s primary residence. Typically, the property securing such loans is subject to a prior lien. Consumer loans consist of loans secured by collateral other than real estate, such as automobiles, recreational vehicles and boats. Personal loans and lines of credit are made on deposits held by American Federal Savings Bank and on an unsecured basis. Commercial loans consist of business loans and lines of credit on a secured and unsecured basis.

13

FELDMAN FINANCIAL ADVISORS, INC.

Table 4

Loan Portfolio

As of September 30, 2009 and June 30, 2005 to 2009

(Dollars in Thousands)

| At June 30, | ||||||||||||||||||||||||||||||||||||||||||

| At September 30, 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||||||||||||||||||||||||

| Amount | Percent of Total | Amount | Percent of Total | Amount | Percent of Total | Amount | Percent of Total | Amount | Percent of Total | Amount | Percent of Total | |||||||||||||||||||||||||||||||

Real estate loans: | ||||||||||||||||||||||||||||||||||||||||||

Residential mortgage (1-4 family) | $ | 76,711 | 45.46 | % | $ | 79,216 | 47.26 | % | $ | 86,751 | 51.53 | % | $ | 81,958 | 51.68 | % | $ | 75,913 | 53.71 | % | $ | 56,533 | 52.68 | % | ||||||||||||||||||

Real estate construction | 6,119 | 3.63 | % | 4,642 | 2.77 | % | 7,317 | 4.35 | % | 8,253 | 5.20 | % | 6,901 | 4.88 | % | 2,723 | 2.54 | % | ||||||||||||||||||||||||

Commercial real estate and land | 38,761 | 22.97 | % | 36,713 | 21.90 | % | 28,197 | 16.75 | % | 25,621 | 16.16 | % | 18,648 | 13.20 | % | 14,779 | 13.77 | % | ||||||||||||||||||||||||

Total real estate loans | 121,591 | 72.06 | % | 120,571 | 71.93 | % | 122,265 | 72.62 | % | 115,832 | 73.04 | % | 101,462 | 71.79 | % | 74,035 | 68.99 | % | ||||||||||||||||||||||||

Other loans: | ||||||||||||||||||||||||||||||||||||||||||

Home equity | 28,836 | 17.09 | % | 28,676 | 17.11 | % | 28,034 | 16.65 | % | 24,956 | 15.74 | % | 20,191 | 14.29 | % | 16,801 | 15.66 | % | ||||||||||||||||||||||||

Consumer | 11,074 | 6.56 | % | 10,835 | 6.46 | % | 11,558 | 6.87 | % | 11,438 | 7.21 | % | 11,820 | 8.36 | % | 10,909 | 10.16 | % | ||||||||||||||||||||||||

Commercial business | 7,244 | 4.29 | % | 7,541 | 4.50 | % | 6,502 | 3.86 | % | 6,366 | 4.01 | % | 7,861 | 5.56 | % | 5,568 | 5.19 | % | ||||||||||||||||||||||||

Total other loans | 47,154 | 27.94 | % | 47,052 | 28.07 | % | 46,094 | 27.38 | % | 42,760 | 26.96 | % | 39,872 | 28.21 | % | 33,278 | 31.01 | % | ||||||||||||||||||||||||

Total gross loans | $ | 168,745 | 100.00 | % | $ | 167,623 | 100.00 | % | $ | 168,359 | 100.00 | % | $ | 158,592 | 100.00 | % | $ | 141,334 | 100.00 | % | $ | 107,313 | 100.00 | % | ||||||||||||||||||

Less: | ||||||||||||||||||||||||||||||||||||||||||

Deferred loan fees | (65 | ) | (99 | ) | (90 | ) | (66 | ) | (59 | ) | (99 | ) | ||||||||||||||||||||||||||||||

Allowance for loan losses | 625 | 525 | 300 | 518 | 535 | 573 | ||||||||||||||||||||||||||||||||||||

Total loans, net | $ | 168,185 | $ | 167,197 | $ | 168,149 | $ | 158,140 | $ | 140,858 | $ | 106,839 | ||||||||||||||||||||||||||||||

Source: Eagle Montana, preliminary prospectus.

14

FELDMAN FINANCIAL ADVISORS, INC.

Residential Lending. American Federal Savings Bank’s primary lending activity consists of the origination of one- to four-family residential mortgage loans secured by property located in American Federal Savings Bank’s market area. Approximately 45.46% of American Federal Savings Bank’s total loan portfolio as of September 30, 2009 was comprised of such loans. American Federal Savings Bank generally originates one- to-four-family residential mortgage loans in amounts up to 80% of the lesser of the appraised value or the selling price of the mortgaged property without requiring private mortgage insurance. A mortgage loan originated by American Federal Savings Bank, whether fixed rate or adjustable rate, can have a term of up to 30 years. American Federal Savings Bank holds substantially all of its adjustable rate and its 8, 10 and 12-year fixed rate loans in portfolio. Adjustable rate loans limit the periodic interest rate adjustment and the minimum and maximum rates that may be charged over the term of the loan. American Federal Savings Bank’s fixed rate 15-year and 20-year loans are held in portfolio or sold in the secondary market depending on market conditions. Generally, all 30-year fixed rate loans are sold in the secondary market.

American Federal Savings Bank obtains a significant portion of its noninterest income from servicing loans sold. American Federal Savings Bank offers many of the fixed rate loans it originates for sale in the secondary market on a servicing retained basis. This means that we process the borrower’s payments and send them to the purchaser of the loan. This retention of servicing enables American Federal Savings Bank to increase fee income and maintain a relationship with the borrower. At September 30, 2009, American Federal Savings Bank had $272.30 million in residential mortgage loans and $12.33 million in commercial real estate loans sold with servicing retained. American Federal Savings Bank does not ordinarily purchase home mortgage loans from other financial institutions.

15

FELDMAN FINANCIAL ADVISORS, INC.

State certified and licensed independent appraisers who are approved annually by the board of directors make property appraisals on real estate securing American Federal Savings Bank’s single-family residential loans. Appraisals are performed in accordance with applicable regulations and policies. American Federal Savings Bank generally obtains title insurance policies on all first mortgage real estate loans originated. On occasion, refinancings of mortgage loans are approved using title reports instead of title insurance. Title reports are also allowed on home equity loans. Borrowers generally remit funds with each monthly payment of principal and interest, to a loan escrow account from which American Federal Savings Bank makes disbursements for such items as real estate taxes and hazard and mortgage insurance premiums as they become due.

Home Equity Loans. American Federal Savings Bank also originates home equity loans. These loans are secured by the borrowers’ primary residence, but are typically subject to a prior lien, which may or may not be held by American Federal Savings Bank. At September 30, 2009, $28.84 million or 17.1% of the Bank’s total loans were home equity loans. Borrowers may use the proceeds from American Federal Savings Bank’s home equity loans for many purposes, including home improvement, debt consolidation, or other purchasing needs. American Federal Savings Bank offers fixed rate, fixed payment home equity loans as well as variable and fixed rate home equity lines of credit. Fixed-rate home equity loans typically have terms of no longer than fifteen years.

16

FELDMAN FINANCIAL ADVISORS, INC.

Although home equity loans are secured by real estate, they carry a greater risk than first lien residential mortgages because of the existence of a prior lien on the property securing the loan, as well as the flexibility the borrower has with respect to the loan proceeds. American Federal Savings Bank attempts to minimize this risk by maintaining conservative underwriting policies on such loans. The Bank generally makes home equity loans for up to only 85% of appraised value of the underlying real estate collateral, less the amount of any existing prior liens on the property securing the loan.

Commercial Real Estate and Land Loans. American Federal Savings Bank originates commercial real estate mortgage and land loans, including both developed and undeveloped land loans, and loans on multi-family dwellings. Commercial real estate and land loans made up 22.97% of American Federal Savings Bank’s total loan portfolio, or $38.76 million at September 30, 2009. The majority of these loans are non-residential commercial real estate loans. American Federal Savings Bank’s commercial real estate mortgage loans are primarily permanent loans secured by improved property such as office buildings, retail stores, commercial warehouses and apartment buildings. The terms and conditions of each loan are tailored to the needs of the borrower and based on the financial strength of the project and any guarantors. Generally, commercial real estate loans originated by American Federal Savings Bank will not exceed 75% of the appraised value or the selling price of the property, whichever is less. Typically, the loans have fixed rates of interest and 5- to 15-year maturities. Upon maturity, the loan is repaid or the terms and conditions are renegotiated. Generally, all originated commercial real estate loans are within the market area of American Federal Savings Bank and all are within the state of Montana. American Federal Savings Bank’s largest single commercial real estate loan had a balance of approximately $1.65 million on September 30, 2009, and is secured by a residential lot subdivision.

17

FELDMAN FINANCIAL ADVISORS, INC.

Real Estate Construction Lending. American Federal Savings Bank also lends funds for the construction of one- to four-family homes and commercial real estate. Real estate construction loans are made both to individual homeowners for the construction of their primary residence and, to a lesser extent, to local builders for the construction of pre-sold houses or houses that are being built for sale in the future. Real estate construction loans accounted for $6.12 million or 3.63% of American Federal Savings Bank’s total loan portfolio at September 30, 2009.

Consumer Loans. As part of its strategy to invest in higher yielding shorter term loans, American Federal Savings Bank emphasized growth of its consumer lending portfolio in recent years. This portfolio includes personal loans secured by collateral other than real estate, unsecured personal loans and lines of credit, and loans secured by deposits held by American Federal Savings Bank. As of September 30, 2009, consumer loans totaled $11.07 million or 6.56% of American Federal Savings Bank’s total loan portfolio. These loans consist primarily of auto loans, RV loans, boat loans, personal loans and credit lines and deposit account loans. Consumer loans are originated in American Federal Savings Bank’s market area and generally have maturities of up to seven years. For loans secured by savings accounts, American Federal Savings Bank will lend up to 90% of the account balance on single payment loans and up to 100% for monthly payment loans.

Consumer loans have a shorter term and generally provide higher interest rates than residential mortgage loans. Consumer loans can be helpful in improving the spread between average loan yield and cost of funds and at the same time improve the matching of the maturities of rate sensitive assets and liabilities. Increasing its consumer loans has been a major part of American Federal Savings Bank’s strategy of operating more like a commercial bank than a traditional savings bank.

18

FELDMAN FINANCIAL ADVISORS, INC.

The underwriting standards employed by American Federal Savings Bank for consumer loans include a determination of the applicant’s credit history and an assessment of the applicant’s ability to meet existing obligations and payments on the proposed loan. The stability of the applicant’s monthly income may be determined by verification of gross monthly income from primary employment, and additionally from any verifiable secondary income. Creditworthiness of the applicant is of primary consideration; however, the underwriting process also includes a comparison of the value of the collateral in relation to the proposed loan amount.

Commercial Business Loans. Commercial business loans amounted to $7.24 million, or 4.29% of American Federal Savings Bank’s total loan portfolio at September 30, 2009. American Federal Savings Bank’s commercial business loans are traditional business loans and are not secured by real estate. Such loans may be structured as unsecured lines of credit or may be secured by inventory, accounts receivable or other business assets. While the commercial business loan portfolio amounted to only 4.29% of the total portfolio at September 30, 2009, American Federal Savings Bank intends to increase such lending by focusing on market segments which it has not previously emphasized, such as business loans to doctors, lawyers, architects and other professionals as well as to small businesses within its market area. Management believes that this strategy provides opportunities for growth, without significant additional cost outlays for staff and infrastructure.

19

FELDMAN FINANCIAL ADVISORS, INC.

Commercial business loans of this nature usually involve greater credit risk than one- to four-family residential mortgage loans the Bank originates. The collateral we receive is typically related directly to the performance of the borrower’s business, which means that repayment of commercial business loans is dependent on the successful operations and income stream of the borrower’s business. Such risks can be significantly affected by economic conditions. In addition, commercial lending generally requires substantially greater oversight efforts compared to residential real estate lending.

Loans to One Borrower. Under federal law, savings institutions have, subject to certain exemptions, lending limits to one borrower in an amount equal to the greater of $500,000 or 15% of the institution’s unimpaired capital and surplus. As of September 30, 2009, the Bank’s largest aggregation of loans to one borrower was approximately $8.47 million, consisting of two commercial real estate loans secured by detention facilities. Ninety percent, or $6.49 million, of one loan was sold to the Montana Board of Investments, leaving a net balance of $1.97 million for the two loans, which was below American Federal Savings Bank’s federal legal lending limit to one borrower of approximately $4.20 million. At September 30, 2009, these loans were performing in accordance to their terms. American Federal Savings Bank maintains the servicing for these loans.

Table 5 on the following page details total loans originated, purchased, sold and repaid during the periods indicated. Gross loan originations totaled $228.0 million for the fiscal year ended June 30, 2009 compared to $143.6 million for the year ended June 30, 2008. For the first three months of 2009, originations have totaled $43.1 million as compared to 36.7 million in the first three months of 2008. As compared to prior years, loan originations have increased, primarily in the category of residential mortgages.

20

FELDMAN FINANCIAL ADVISORS, INC.

Table 5

Loan Originations

For the Three Months Ended September 30, 2008 and 2009

For the Years Ended June 30, 2008 to 2009

(Dollars in Thousands)

| Three Months Ended September 30, | Year Ended June 30, | ||||||||||||||

| 2009 | 2008 | 2009 | 2008 | ||||||||||||

Loans originated | |||||||||||||||

Real estate loans: | |||||||||||||||

Residential mortgage (1-4 family) | $ | 29,017 | $ | 17,981 | $ | 164,657 | $ | 72,385 | |||||||

Real estate construction | 2,504 | 1,934 | 4,672 | 15,504 | |||||||||||

Commercial real estate and land | 3,466 | 9,042 | 21,500 | 19,375 | |||||||||||

Home equity | 4,167 | 4,860 | 20,043 | 20,461 | |||||||||||

Consumer | 2,000 | 1,748 | 8,341 | 7,637 | |||||||||||

Commercial business | 1,913 | 1,143 | 8,789 | 8,243 | |||||||||||

Total loans originated | 43,067 | 36,708 | 228,002 | 143,605 | |||||||||||

Loans purchased | |||||||||||||||

Whole loans | — | — | — | — | |||||||||||

Participations | — | — | — | — | |||||||||||

Total loans purchased | — | — | — | — | |||||||||||

Loans sold | |||||||||||||||

Whole loans | 28,135 | 10,517 | 125,232 | 47,732 | |||||||||||

Participations | — | 6,000 | 6,000 | 4,341 | |||||||||||

Total loans sold | 28,135 | 16,517 | 131,232 | 52,073 | |||||||||||

Principal repayments and loan refinancings | 15,733 | 15,351 | 99,509 | 75,522 | |||||||||||

Deferred loan fees decrease (increase) | 34 | 5 | (9 | ) | (24 | ) | |||||||||

Allowance for losses decrease (increase) | (100 | ) | — | (225 | ) | 218 | |||||||||

Net loan increase (decrease) | ($ | 867 | ) | $ | 4,845 | ($ | 2,973 | ) | $ | 16,204 | |||||

Net loans receivable at end of period | |||||||||||||||

(includes loans held for sale) | $ | 171,679 | $ | 180,364 | $ | 172,546 | $ | 175,519 | |||||||

Source: Eagle Montana, preliminary prospectus.

21

FELDMAN FINANCIAL ADVISORS, INC.

Exhibit II-4 and Table 6 present a summary of the Company’s investment portfolio as of September 30, 2009 and June 30, 2007 to 2009. Federally chartered savings banks such as American Federal Savings Bank have the authority to invest in various types of investment securities, including United States Treasury obligations, securities of various Federal agencies (including securities collateralized by mortgages), certificates of deposits of insured banks and savings institutions, municipal securities, corporate debt securities and loans to other banking institutions.

American Federal Savings Bank maintains liquid assets that may be invested in specified short-term securities and other investments. Liquidity levels may be increased or decreased depending on the yields on investment alternatives. They may also be increased based on management’s judgment as to the attractiveness of the yields then available in relation to other opportunities. Liquidity levels can also change based on management’s expectation of future yield levels, as well as management’s projections as to the short-term demand for funds to be used in American Federal Savings Bank’s loan origination and other activities. American Federal Savings Bank maintains an investment securities portfolio and a mortgage-backed securities portfolio as part of its investment portfolio.

The investment policy of American Federal Savings Bank, which is established by the board of directors, is designed to foster earnings and liquidity within prudent interest rate risk guidelines, while complementing American Federal Savings Bank’s lending activities. The policy provides for available-for-sale (including those accounted for under FASB ASC 825), held-to-maturity, and trading classifications. However, American Federal Savings Bank does not hold any securities for purposes of trading. The policy permits investments in high credit quality instruments with diversified cash flows while permitting the Bank to maximize total return

22

FELDMAN FINANCIAL ADVISORS, INC.

within the guidelines set forth in the interest rate risk and liquidity management policies. Permitted investments include but are not limited to U.S. government obligations, government agency or government-sponsored enterprise obligations, state, county and municipal obligations, and mortgage-backed securities. Collateralized mortgage obligations, investment grade corporate debt securities, and commercial paper are also included. The Bank also invests in Federal Home Loan Bank overnight deposits and federal funds, but these instruments are not considered part of the investment portfolio.

The investment policy also includes several specific guidelines and restrictions to insure adherence with safe and sound activities. The policy prohibits investments in high-risk mortgage derivative products (as defined within the policy) without prior approval from the board of directors. Management must demonstrate the business advantage of such investments.

The Bank does not participate in hedging programs, interest rate swaps, or other activities involving the use of off-balance sheet derivative financial instruments, except interest rate caps and certain financial instruments designated as cash flow hedges related to loans committed to be sold in the secondary market. Further, American Federal Savings Bank does not invest in securities that are not initially rated investment grade.

The Board, through its asset liability committee, has charged the President and CEO to implement the investment policy. All transactions are reported to the board of directors monthly, as well as the current composition of the portfolio, including market values and unrealized gains and losses.

23

FELDMAN FINANCIAL ADVISORS, INC.

The Bank maintains a portfolio of investment securities, classified as either available-for-sale (including those accounted for under FASB ASC 825) or held-to-maturity to enhance total return on investments. At September 30, 2009, investment securities included U.S. government and agency obligations, Small Business Administration pools, municipal securities, mortgage-backed securities, collateralized mortgage obligations and corporate obligations, all with varying characteristics as to rate, maturity and call provisions. Investment securities held-to-maturity represented 0.28% of American Federal Savings Bank’s total investment portfolio. Securities available-for-sale totaled 96.91% of American Federal Savings Bank’s total investment portfolio. The largest categories of securities available-for-sale are collateralized mortgage obligations, 36.8% of total securities, and municipal obligations, which total 35.7% of total securities.

Table 6

Securities Portfolio

As of September 30, 2009 and June 30, 2007 to 2009

(Dollars in Thousands)

| At September 30, | At June 30, | |||||||||||||||||||||||

| 2009 | 2009 | 2008 | 2007 | |||||||||||||||||||||

| Carrying Value | of Total | Carrying Value | of Total | Carrying Value | of Total | Carrying Value | of Total | |||||||||||||||||

Securities available-for-sale, at fair value: | ||||||||||||||||||||||||

U.S. Government and agency obligations | $ | 4,930 | 5.17 | % | $ | 3,882 | 4.57 | % | $ | 2,232 | 2.70 | % | $ | 3,643 | 5.41 | % | ||||||||

Corporate obligations | 10,037 | 10.52 | % | 9,493 | 11.18 | % | 12,722 | 15.38 | % | 13,623 | 20.22 | % | ||||||||||||

Municipal obligations | 34,036 | 35.67 | % | 28,893 | 34.04 | % | 22,190 | 26.83 | % | 20,728 | 30.77 | % | ||||||||||||

Collateralized mortgage obligations | 35,112 | 36.80 | % | 31,551 | 37.17 | % | 28,224 | 34.17 | % | 17,075 | 25.35 | % | ||||||||||||

Mortgage-backed securities | 7,985 | 8.37 | % | 8,444 | 9.95 | % | 13,016 | 15.74 | % | 7,872 | 11.68 | % | ||||||||||||

Common Stock | — | — | — | — | 33 | — | — | — | ||||||||||||||||

Corporate preferred stock | — | — | — | — | — | — | 1,833 | 2.72 | % | |||||||||||||||

Total securities available for sale | 92,100 | 96.52 | % | 82,263 | 96.91 | % | 78,417 | 94.82 | % | 64,774 | 96.15 | % | ||||||||||||

Securities held-to-maturity, at book value: | ||||||||||||||||||||||||

Mortgage-backed securities | — | — | — | — | 22 | 0 | 95 | 0.14 | % | |||||||||||||||

Municipal obligations | 265 | 0.28 | % | 375 | 0.44 | % | 675 | 0.82 | % | 826 | 1.23 | % | ||||||||||||

Total securities held to maturity | 265 | 0.28 | % | 375 | 0.44 | % | 697 | 0.85 | % | 921 | 1.37 | % | ||||||||||||

Preferred stock | 108 | 0.11 | % | 25 | 0.03 | % | 1,321 | 1.60 | % | N/A | N/A | |||||||||||||

Total securities | 92,473 | 96.91 | % | 82,663 | 97.38 | % | 80,435 | 97.27 | % | 65,695 | 98.00 | % | ||||||||||||

FHLB stock, at cost | 2,000 | 2.10 | % | 2,000 | 2.36 | % | 1,715 | 2.07 | % | 1,315 | 1.95 | % | ||||||||||||

Interest-bearing deposits | 944 | 0.99 | % | 224 | 0.26 | % | 549 | 0.66 | % | 360 | 0.53 | % | ||||||||||||

Total | $ | 95,417 | 100.00 | % | $ | 84,887 | 100.00 | % | $ | 82,699 | 100.00 | % | $ | 67,370 | 100.00 | % | ||||||||

Source: Eagle Montana, preliminary prospectus.

24

FELDMAN FINANCIAL ADVISORS, INC.

Table 7 sets forth certain information regarding the carrying values, weighted average yields and maturities of the Bank’s securities portfolio at September 30, 2009. This table shows contractual maturities and does not reflect repricing or the effect of prepayments.

Liability Composition

Deposits are the Company’s major external source of funds for lending and other investment purposes. Exhibit II-5 and Table 8 present a summary of the Company’s deposit composition as of June 30, 2007 to 2009 and September 30, 2009. Total deposits amounted to $195.1 million or 64.9% of total assets and 72.2% of total liabilities at September 30, 2009.

The Bank offers a variety of deposit accounts. Deposit account terms vary, primarily as to the required minimum balance amount, the amount of time that the funds must remain on deposit and the applicable interest rate.

Current deposit products include certificates of deposit accounts ranging in terms from 90 days to five years as well as checking, savings and money market accounts. Individual retirement accounts (IRAs) are included in certificates of deposit.

Deposits are obtained primarily from residents of Helena, Bozeman, Butte and Townsend. The Bank believes it is able to attract deposit accounts by offering outstanding service, competitive interest rates and convenient locations and service hours. The Bank uses traditional methods of advertising to attract new customers and deposits, including radio, television, print media advertising and sales training and incentive programs for employees. Management believes that non-residents of Montana hold an insignificant number of deposit accounts.

25

FELDMAN FINANCIAL ADVISORS, INC.

Table 7

Securities Portfolio by Contractual Maturity

As of September 30, 2009

(Dollars in Thousands)

| At September 30, 2009 | |||||||||||||||||||||||||||||||||

| One Year or Less | One to Five Years | Five to Ten Years | More than Ten Years | Total Investment Securities | |||||||||||||||||||||||||||||

| Carrying Value | Weighted Average Yield | Carrying Value | Weighted Average Yield | Carrying Value | Weighted Average Yield | Carrying Value | Weighted Average Yield | Carrying Value | Approximate Market Value | Weighted Average Yield | |||||||||||||||||||||||

Securities available-for-sale: | |||||||||||||||||||||||||||||||||

U.S. Gov’t and agency obligations | $ | 3,659 | 1.76 | % | $ | 831 | 1.06 | % | $ | 440 | 0.94 | % | $ | 4,930 | $ | 7,930 | 1.57 | % | |||||||||||||||

Corporate obligations | 7,263 | 4.90 | % | 1,053 | 5.45 | % | 1,721 | 7.51 | % | 10,037 | 10,037 | 5.41 | % | ||||||||||||||||||||

Municipal obligations | 2,399 | 2.78 | % | 7,532 | 5.59 | % | 24,105 | 6.70 | % | 34,036 | 34,036 | 6.18 | % | ||||||||||||||||||||

Collateralized mortgage obligations | $ | 106 | 2.60 | % | 3,697 | 3.20 | % | 31,309 | 4.70 | % | 35,112 | 35,112 | 4.54 | % | |||||||||||||||||||

Mortgage-backed securities | 194 | 4.29 | % | 396 | 3.75 | % | 101 | 5.38 | % | 7,294 | 5.20 | % | 7,985 | 7,985 | 5.11 | % | |||||||||||||||||

Total securities available for sale | 300 | 3.69 | % | 13,717 | 3.66 | % | 13,214 | 4.62 | % | 64,869 | 5.55 | % | 92,100 | 92,100 | 5.13 | % | |||||||||||||||||

Securities-held to-maturity: | |||||||||||||||||||||||||||||||||

Municipal obligations | 265 | 7.33 | % | 265 | 271 | 7.33 | % | ||||||||||||||||||||||||||

Total securities held to maturity | 265 | 7.33 | % | 265 | 271 | 7.33 | % | ||||||||||||||||||||||||||

Preferred – SFAS 159 | 108 | 108 | 108 | % | |||||||||||||||||||||||||||||

Total securities | 300 | 3.69 | % | 13,982 | 3.73 | % | 13,214 | 4.62 | % | 64,977 | 5.54 | % | 92,473 | 92,479 | 5.13 | % | |||||||||||||||||

Interest-bearing deposits & Federal funds sold | 4,155 | 0.59 | % | 4,155 | 4,155 | 0.59 | % | ||||||||||||||||||||||||||

Federal Home Loan Bank capital stock | 2,000 | ||||||||||||||||||||||||||||||||

Total | $ | 4,455 | 0.80 | % | $ | 13,982 | 3.73 | % | $ | 13,214 | 4.62 | % | $ | 66,977 | 5.37 | % | $ | 96,628 | $ | 96,634 | 4.93 | % | |||||||||||

Source: Eagle Montana, preliminary prospectus.

26

FELDMAN FINANCIAL ADVISORS, INC.

Table 8

Deposit Portfolio

As of September 30, 2009

And June 30, 2007 to 2009

| At September 30, 2009 | At June 30, | |||||||||||||||||||||||||||||||||||

| 2009 | 2008 | 2007 | ||||||||||||||||||||||||||||||||||

| Amount | Percent of Total | Weighted Average Rate | Amount | Percent of Total | Weighted Average Rate | Amount | Percent of Total | Weighted Average Amount | Amount | Percent of Total | Weighted Average Amount | |||||||||||||||||||||||||

Noninterest checking | $ | 18,902 | 9.69 | % | — | $ | 15,002 | 8.01 | % | — | $ | 14,617 | 8.17 | % | — | $ | 13,694 | 7.62 | % | — | ||||||||||||||||

Passbook savings | 26,979 | 13.83 | % | 0.41 | % | 26,445 | 14.13 | % | 0.41 | % | 23,906 | 13.37 | % | 0.65 | % | 22,521 | 12.54 | % | 0.65 | % | ||||||||||||||||

NOW account/Interest bearing checking | 34,785 | 17.83 | % | 0.25 | % | 32,665 | 17.45 | % | 0.33 | % | 30,721 | 17.18 | % | 0.38 | % | 30,954 | 17.23 | % | 0.21 | % | ||||||||||||||||

Money market accounts | 26,730 | 13.70 | % | 0.30 | % | 26,886 | 14.36 | % | 0.64 | % | 25,275 | 14.12 | % | 1.75 | % | 23,292 | 12.96 | % | 2.12 | % | ||||||||||||||||

Total | 107,395 | 55.05 | % | 0.26 | % | 100,997 | 53.95 | % | 0.38 | % | 94,518 | 52.85 | % | 0.76 | % | 90,460 | 50.35 | % | 0.78 | % | ||||||||||||||||

Certificates of deposit accounts: | ||||||||||||||||||||||||||||||||||||

IRA certificates | 23,447 | 12.02 | % | 2.85 | % | 23,121 | 12.35 | % | 2.96 | % | 22,108 | 12.36 | % | 3.15 | % | 21,534 | 11.99 | % | 3.97 | % | ||||||||||||||||

Brokered certificates | — | — | — | — | — | — | — | — | — | 4,411 | 2.46 | % | 5.30 | % | ||||||||||||||||||||||

Other certificates | 64,238 | 32.93 | % | 2.16 | % | 63,081 | 33.70 | % | 2.41 | % | 62,225 | 34.79 | % | 3.31 | % | 63,242 | 35.20 | % | 4.66 | % | ||||||||||||||||

Total certificates of deposit | 87,685 | 44.95 | % | 2.34 | % | 86,202 | 46.05 | % | 2.56 | % | 84,333 | 47.15 | % | 3.27 | % | 89,187 | 49.65 | % | 4.53 | % | ||||||||||||||||

Total deposits | $ | 195,080 | 100.00 | % | 1.19 | % | $ | 187,199 | 100.00 | % | 1.38 | % | $ | 178,851 | 100.00 | % | 1.94 | % | $ | 179,647 | 100.00 | % | 100.00 | % | ||||||||||||

Source: Eagle Montana, preliminary prospectus.

27

FELDMAN FINANCIAL ADVISORS, INC.

The Bank pays interest rates on deposits that are competitive in the market. Interest rates on deposits are set weekly by senior management, based on a number of factors, including: projected cash flow; a current survey of a selected group of competitors’ rates for similar products; external data which may influence interest rates; investment opportunities and loan demand; and scheduled certificate maturities and loan and investment repayments.

Core deposits are deposits that are more stable and somewhat less sensitive to rate changes. They also represent a lower cost source of funds than rate sensitive, more volatile accounts such as certificates of deposit. The Bank believes core deposits are its checking, as well as NOW accounts, statement savings accounts, money market accounts and IRA accounts. Based on historical experience, the Bank includes IRA accounts funded by certificates of deposit as core deposits because they exhibit the principal features of core deposits in that they are stable and generally are not rate sensitive. Core deposits amounted to $130.84 million or 67.07% of American Federal Savings Bank’s deposits at September 30, 2009 ($107.39 million or 55.05% if IRA certificates of deposit are excluded). The presence of a high percentage of core deposits and, in particular, transaction accounts, is part of the Bank’s strategy to restructure its liabilities to more closely resemble the lower cost liabilities of a commercial bank. However, a significant portion of deposits remains in certificate of deposit form. These certificates of deposit, should they mature and be renewed at higher rates, would result in an increase in the cost of funds.

To supplement deposits as a source of funds for lending or investment, the Bank also borrows funds in the form of advances from the Federal Home Loan Bank of Seattle and other borrowings from PNC Financial Services, Inc. to supplement the Bank’s supply of lendable funds and to meet deposit withdrawal requirements.

28

FELDMAN FINANCIAL ADVISORS, INC.

During the fiscal year ended June 30, 2006, Eagle Bancorp formed a special purpose subsidiary, Eagle Bancorp Statutory Trust I (the “Trust”), for the purpose of issuing trust preferred securities in the amount of $5.0 million. Eagle Bancorp has issued subordinated debentures to the Trust, and the coupon on the debentures matches the dividend payment on the trust preferred securities. For regulatory purposes, the securities qualify as Tier 1 Capital, while for accounting purposes they are recorded as long term debt. The securities have a 30 year maturity and carry a fixed coupon of 6.02% for the first five years, at which time the coupon becomes variable, at a spread of 142 basis points over 3 month LIBOR.

Table 9 sets forth certain information regarding borrowings from the Federal Home Loan Bank of Seattle and PNC at the end of, and during, the periods indicated.

Equity Capital

As of September 30, 2009, American Federal Savings Bank’s regulatory capital was in excess of all applicable regulatory requirements and is considered “well capitalized” by regulatory standards. At September 30, 2009, American Federal Savings Bank’s tangible, core, and risk-based capital ratios amounted to 9.45%, 9.45, and 13.72%, respectively, compared to regulatory requirements of 1.5%, 3.0%, and 8.0%, respectively.

29

FELDMAN FINANCIAL ADVISORS, INC.

Table 9

Borrowings

At or for the Three Months Ended September 30, 2008 and 2009

and for the Years Ended June 30, 2007 to 2009

| At or For the Three Months Ended September 30, | At or For the Year Ended June 30, | |||||||||||||||||||

| 2009 | 2008 | 2009 | 2008 | 2007 | ||||||||||||||||

FHLB Advances: | ||||||||||||||||||||

Average balance | $ | 43,778 | $ | 40,351 | $ | 44,144 | $ | 21,964 | $ | 23,435 | ||||||||||

Maximum balance at any month-end | 43,917 | 45,919 | 46,889 | 42,222 | 29,487 | |||||||||||||||

Balance at period end | 43,639 | 45,919 | 44,056 | 42,222 | 16,000 | |||||||||||||||

Weighted average interest rate during the period | 3.70 | % | 3.72 | % | 3.54 | % | 4.21 | % | 5.13 | % | ||||||||||

Weighted average interest rate at period end | 3.69 | % | 3.70 | % | 3.69 | % | 3.57 | % | 4.99 | % | ||||||||||

Repurchase Agreements: | ||||||||||||||||||||

Average balance | 23,000 | 23,000 | 23,000 | 21,347 | 5,493 | |||||||||||||||

Maximum balance at any month-end | 23,000 | 23,000 | 23,000 | 23,000 | 14,000 | |||||||||||||||

Balance at period end | 23,000 | 23,000 | 23,000 | 23,000 | 14,000 | |||||||||||||||

Weighted average interest rate during the period | 4.66 | % | 4.66 | % | 4.66 | % | 4.81 | % | 4.64 | % | ||||||||||

Weighted average interest rate at period end | 4.66 | % | 4.66 | % | 4.66 | % | 4.66 | % | 4.69 | % | ||||||||||

Other: | ||||||||||||||||||||

Average balance | — | 1,081 | 628 | 401 | 143 | |||||||||||||||

Maximum balance at any month-end | — | 2,760 | 3,900 | 3,000 | 3,800 | |||||||||||||||

Balance at period end | — | — | — | 3,000 | 3,800 | |||||||||||||||

Weighted average interest rate during the period | 2.18 | % | 1.28 | % | 3.79 | % | 5.32 | % | ||||||||||||

Weighted average interest rate at period end | n/a | n/a | 3.15 | % | 5.32 | % | ||||||||||||||

Total borrowings: | ||||||||||||||||||||

Average balance | 66,778 | 64,432 | 67,772 | 43,712 | 29,071 | |||||||||||||||

Maximum balance at any month-end | 66,917 | 68,919 | 73,789 | 68,222 | 36,695 | |||||||||||||||

Balance at period end | 66,639 | 68,919 | 67,056 | 68,222 | 33,800 | |||||||||||||||

period | 4.03 | % | 4.03 | % | 3.90 | % | 4.50 | % | 5.04 | % | ||||||||||

Weighted average interest rate at period end | 4.03 | % | 4.02 | % | 4.02 | % | 3.94 | % | 4.90 | % | ||||||||||

Source: Eagle Montana, preliminary prospectus.

30

FELDMAN FINANCIAL ADVISORS, INC.

Income and Expense Trends

Table 10 displays the main components of the Company’s earnings performance over the years ended June 30, 2005 to 2009 and the three-month periods ending September 30, 2008 and 2009. Tables 11 set forth certain average balance and yield information relating to the Company at and for the periods indicated. The average yields and costs are derived by dividing income or expense by the daily average balance of assets or liabilities, respectively, for the periods presented. Table 12 reflects the sensitivity of the Company’s interest income and interest expense to changes in volume and in prevailing interest rates during the periods indicated.

Table 10

Summary Income Statement Data

For the Years Ended June 30, 2005 to 2009

And for the Nine Months Ended September 30, 2008 and 2009

(Dollars in Thousands)

| For the Three Months Ended September 30, | For the Year Ended June 30, | |||||||||||||||||||||

| 2009 | 2008 | 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

Total interest income | $ | 3,724 | $ | 3,816 | $ | 15,348 | $ | 14,098 | $ | 12,651 | $ | 10,506 | $ | 9,043 | ||||||||

Total interest expense | 1,341 | 1,580 | 6,115 | 6,662 | 5,966 | 3,792 | 2,563 | |||||||||||||||

Net interest income | 2,383 | 2,236 | 9,233 | 7,436 | 6,685 | 6,714 | 6,480 | |||||||||||||||

Provision (credit) for loan losses | 135 | — | 257 | -175 | — | — | — | |||||||||||||||

Net interest income after provision for loan losses | 2,248 | 2,236 | 8,976 | 7,611 | 6,685 | 6,714 | 6,480 | |||||||||||||||

Noninterest income | 1,061 | -504 | 2,999 | 2,224 | 2,261 | 2,165 | 2,059 | |||||||||||||||

Noninterest expense | 2,103 | 1,849 | 8,563 | 7,063 | 6,614 | 6,645 | 6,181 | |||||||||||||||

Income (loss) before income taxes | 1,206 | -117 | 3,412 | 2,772 | 2,332 | 2,414 | 2,358 | |||||||||||||||

Income tax expense | 362 | -17 | 1,024 | 662 | 554 | 629 | 615 | |||||||||||||||

Net income (loss) | $ | 844 | ($ | 100 | ) | $ | 2,388 | $ | 2,110 | $ | 1,778 | $ | 1,785 | $ | 1,743 | |||||||

Earnings per share: | ||||||||||||||||||||||

Basic | $ | 0.79 | ($ | 0.09 | ) | $ | 2.23 | $ | 1.97 | $ | 1.66 | $ | 1.66 | $ | 1.55 | |||||||

Diluted | $ | 0.69 | ($ | 0.08 | ) | $ | 1.96 | $ | 1.74 | $ | 1.47 | $ | 1.48 | $ | 1.45 | |||||||

Source: Eagle Montana, preliminary prospectus

31

FELDMAN FINANCIAL ADVISORS, INC.

Table 11

Average Balances and Yields

For the Three Months Ended September 30, 2008 and 2009

(Dollars in Thousands)

| For the Three Months Ended September 30, | |||||||||||||||||

| 2009 | 2008 | ||||||||||||||||

| Average Daily Balance | Interest and Dividends | Yield/ Cost(3) | Average Daily Balance | Interest and Dividends | Yield/ Cost(3) | ||||||||||||

Assets: | |||||||||||||||||

Interest-earning assets: | |||||||||||||||||

FHLB stock | $ | 2,000 | — | 0.00 | % | $ | 1,781 | $ | 7 | 1.57 | % | ||||||

Loans receivable, net | 171,262 | 2,708 | 6.32 | % | 174,370 | 2,837 | 6.50 | % | |||||||||

Investment securities | 84,983 | 1,008 | 4.74 | % | 79,004 | 968 | 4.91 | % | |||||||||

Interest-bearing deposits with banks | 8,123 | 8 | 0.44 | % | 665 | 4 | 2.41 | % | |||||||||

Total interest-earning assets | 266,368 | 3,724 | 5.59 | % | 255,820 | 3,816 | 5.97 | % | |||||||||

Noninterest-earning assets | 28,072 | 21,191 | |||||||||||||||

Total assets | $ | 294,440 | $ | 277,011 | |||||||||||||

Liabilities and Equity: | |||||||||||||||||

Interest-bearing liabilities: | |||||||||||||||||

Deposit accounts: | |||||||||||||||||

Money market | $ | 27,103 | 41 | 0.61 | % | $ | 25,692 | 111 | 1.73 | % | |||||||

Passbooks | 26,979 | 28 | 0.42 | % | 24,093 | 39 | 0.65 | % | |||||||||

Checking | 34,948 | 22 | 0.25 | % | 30,958 | 30 | 0.39 | % | |||||||||

Certificates of deposit | 85,772 | 521 | 2.43 | % | 84,415 | 682 | 3.23 | % | |||||||||

Advances from FHLB and subordinated debt | 70,647 | 730 | 4.13 | % | 68,298 | 718 | 4.21 | % | |||||||||

Total interest-bearing liabilities | 245,449 | 1,341 | 2.19 | % | 233,456 | 1,580 | 2.71 | % | |||||||||

Non-interest checking | 17,291 | 15,160 | |||||||||||||||

Other noninterest-bearing liabilities | 2,889 | 3,291 | |||||||||||||||

Total liabilities | 265,629 | 251,907 | |||||||||||||||

Total equity | 28,811 | 25,104 | |||||||||||||||

Total liabilities and equity | $ | 294,440 | $ | 277,011 | |||||||||||||

Net interest income/interest rate spread(1) | 2,383 | 3.40 | % | 2,236 | 3.26 | % | |||||||||||

Net interest margin(2) | 3.58 | % | 3.50 | % | |||||||||||||

Total interest-earning assets to interest bearing liabilities | 108.52 | % | 109.58 | % | |||||||||||||