UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

10-K

(Mark One)

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2021

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number

001-39894

GREENLIGHT BIOSCIENCES HOLDINGS, PBC

(Exact name of registrant as specified in its charter)

Delaware | 200 Boston Avenue Medford, MA 02155 (617) 616-8188 | 85-1914700 | ||

(State or other jurisdiction of incorporation or organization) | (Address, including offices) | (I.R.S. Employer Identification No.) |

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||

| Common stock, par value $0.0001 per share | GRNA | The Nasdaq Stock Market LLC | ||

Warrants, each exercisable for one share of Common Stock for $11.50 per share | GRNAW | The Nasdaq Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act

. Y

es

☐ No☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act

. Y

es

☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days

. Yes

☒

No

☐Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation

S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes

☒

No

☐Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule12b-2

of the Exchange Act.| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Securities Act

. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report

. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule

12b-2

of the Act). Yes ☐ No

☒

The aggregate market value of the voting common shares held

by non-affiliates of

the registrant was approximately$193,257,000, computed by reference t

o the closing sale price of the Common Stock on The Nasdaq Capital Market on June 30, 2021, the last trading day of the registrant’s most recently completed second fiscal quarter.The number of shares of the registrant’s Common Stock outstanding as of March 15, 2022 was

122,839,613.

DOCUMENTS INCORPORATED BY REFERENCE

None.

| Auditor Firm Id: 100 | Name of Auditor: WithumSmith+Brown, PC | Auditor Location: New York, New York |

EXPLANATORY NOTE

The registrant, a Delaware corporation formerly known as Environmental Impact Acquisition Corp. (“”), was incorporated on July 2, 2020 as a special purpose acquisition company, a type of blank check company formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization, or other similar business combination with one or more target businesses. On February 2, 2022, a date subsequent to the end of the fiscal year for which this Annual Report on Form”) is being filed, ENVI consummated the Business Combination (as defined below). In accordance with the rules of the Securities and Exchange Commission (the “”), because the Business Combination was consummated after December 31, 2021, the end of ENVI’s fiscal year, this Annual Report provides the consolidated financial statements of ENVI for the year ended December 31, 2021 and the period from July 2, 2020 (inception) to December 31, 2020, which are discussed in “.”

ENVI

10-K

(the “Annual Report

SEC

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

On January 19, 2021, ENVI consummated its initial public offering (“”) of 20,700,000 units (the “”), including 2,700,000 Units issued to the underwriters upon full exercise of their over-allotment option. Each Unit consisted of one share of ENVI’s Class A common stock, par value $0.0001 per share (“”), and”), with each whole warrant entitling the holder thereof to purchase one share of Class A Common Stock for $11.50 per share. The Units were sold at a price of $10.00 per Unit, generating gross proceeds to ENVI of $207.0 million. Simultaneously with the closing of the IPO, ENVI completed the private sale of an aggregate of 2,000,000 warrants (the “”) at a purchase price of $1.00 per Private Placement Warrant, generating gross proceeds of $2.0 million. At the closing of the IPO, ENVI also issued 600,000 Private Placement Warrants to its sponsor and 50,000 Private Placement Warrants to each of its three independent directors. A total of $207.0 million, comprised of $206,750,000 of the proceeds from the IPO and $250,000 of the proceeds of the sale of the Private Placement Warrants, was placed in a U.S.-based trust account (the “”) maintained by Continental Stock Transfer & Trust Company, acting as trustee.

IPO

Units

ENVI Class

A Common Stock

one-half

of one redeemable warrant (“warrant

Private Placement Warrants

trust account

On August 9, 2021, ENVI entered into a Business Combination Agreement (the “”), by and among ENVI, Honey Bee Merger Sub, Inc., a Delaware corporation and wholly owned subsidiary of ENVI (“”), and GreenLight Biosciences, Inc., a Delaware corporation (“”). On February 2, 2022 (the “”), pursuant to the terms of the Business Combination Agreement, Merger Sub merged with and into GreenLight, with GreenLight surviving the merger as a wholly owned subsidiary of ENVI (the “” or “”). In connection with the consummation of the Merger on the Closing Date, ENVI changed its name to GreenLight Biosciences Holdings, PBC (“”) and became a public benefit corporation.

Business Combination Agreement

Merger Sub

GreenLight

Closing Date

Merger

Business Combination

New GreenLight

In accordance with the terms and subject to the conditions of the Business Combination Agreement, at the effective time of the Merger (the “”), each outstanding share of capital stock of GreenLight (other than treasury shares) was exchanged for shares of common stock, par value $0.0001 per share, of New GreenLight (“”), and outstanding GreenLight options and warrants to purchase shares of capital stock of GreenLight (whether vested or unvested) were converted into comparable options (the “”) and warrants to purchase shares of New GreenLight Common Stock, in each case, based on an implied GreenLight fully diluted equity value of $1.2 billion. In connection with the consummation of the Business Combination, all of the issued and outstanding shares of ENVI Class A Common Stock and all of the issued and outstanding shares of ENVI Class B common stock, par value $0.0001 per share (“”), became shares of New GreenLight Common Stock.

Effective Time

New GreenLight Common Stock

Rollover Options

ENVI Class

B Common Stock

In connection with the Business Combination, New GreenLight completed the sale and issuance of 12,425,000 shares of New GreenLight Common Stock in a private placement at a purchase price of $10.00 per share pursuant to subscription agreements (the “”) that had been entered into between

Subscription Agreements

i

New GreenLight and certain institutional accredited investors (the “”) either concurrently with the execution of the Business Combination Agreement or subsequently in November 2021 (the “”).

PIPE Investors

PIPE Financing

Also in connection with the Business Combination, 19,489,626 shares of ENVI Class A Common Stock were redeemed for an aggregate payment of approximately $194.9 million. The redemption price was paid from the trust account, the remaining balance of the trust account was disbursed to New GreenLight, and the trust account was closed.

As a result of the Business Combination, GreenLight is considered the accounting predecessor of New GreenLight. The audited consolidated financial statements of GreenLight as of and for the years ended December 31, 2021 and 2020 have been filed as Exhibit 99.1 to the Current Report on Form

8-K

filed by New GreenLight on the date hereof. For filings made after the Closing Date (other than this Annual Report), the consolidated financial statements of GreenLight will be the consolidated financial statements of New GreenLight.Unless otherwise stated or the context indicates otherwise, the financial information contained in this Annual Report, other than the consolidated financial statements and “”, are those of GreenLight.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

ii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report includes forward-looking statements regarding, among other things, the business and financial plans, strategies and prospects of New GreenLight. These statements are based on the beliefs and assumptions of the management of New GreenLight. Although New GreenLight believes that the plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, it cannot assure you that it will achieve or realize these plans, intentions or expectations. Generally, statements that are not historical facts, including statements concerning possible or assumed future actions, business strategies, events or results of operations, and any statements that refer to projections, forecasts, or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. These statements may be preceded by, followed by or include the words “believes”, “estimates”, “expects”, “projects”, “forecasts”, “may”, “might”, “will”, “should”, “seeks”, “plans”, “scheduled”, “possible”, “anticipates”, “intends”, “aims”, “works”, “focuses”, “aspires”, “strives” or “sets out” or similar expressions. Forward-looking statements are not guarantees of performance. Forward-looking statements involve a number of risks, uncertainties (many of which are beyond the control of New GreenLight) or other factors that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. You should not place undue reliance on these statements, which speak only as of the date these statements were made. These risks and uncertainties include, but are not limited to, the following risks, uncertainties (some of which are beyond our control) or other factors:

| • | the anticipated need for additional capital to achieve New GreenLight’s business goals; |

| • | the need to obtain regulatory approval for New GreenLight’s product candidates; |

| • | the risk that preclinical studies and any ensuing clinical trials will not demonstrate that New GreenLight’s product candidates are safe and effective; |

| • | the risk that New GreenLight’s product candidates will have adverse side effects or other unintended consequences, which could impair their marketability; |

| • | the risk that New GreenLight’s product candidates do not satisfy other legal and regulatory requirements for marketability in one or more jurisdictions; |

| • | the risks of enhanced regulatory scrutiny of solutions utilizing messenger ribonucleic acid (“ mRNA ”) as a basis; |

| • | the potential inability to achieve New GreenLight’s goals regarding scalability, affordability and speed of commercialization of its product candidates; |

| • | the potential failure to realize anticipated benefits of the Business Combination or to realize estimated pro forma results and underlying assumptions; |

| • | changes in the industries in which New GreenLight operates; |

| • | changes in laws and regulations affecting the business of New GreenLight; |

| • | the potential inability to implement or achieve business plans, forecasts, and other expectations; |

| • | the potential inability to maintain the listing of New GreenLight’s securities with Nasdaq; |

| • | the outcome of any legal proceedings that may be instituted against New GreenLight related to the Business Combination; |

| • | unanticipated costs related to the Business Combination, which may reduce available cash; |

| • | the effect of the Business Combination on New GreenLight’s business relationships, operating results, and business generally; |

| • | risks that the Business Combination disrupts current plans and operations of New GreenLight; and |

iii

| • | other factors detailed in this annual report under the section entitled “ Risk Factors |

The risks described under the heading “” in this annual report are not exhaustive. New risk factors emerge from time to time, and it is not possible to predict all such risk factors, nor can we assess the impact of all such risk factors on the business of New GreenLight or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any forward-looking statements. All forward-looking statements attributable to New GreenLight or to persons acting on our behalf are expressly qualified in their entirety by the foregoing cautionary statements. Some of these risks and uncertainties may in the future be amplified by

Risk Factors

the COVID-19 pandemic,

and there may be additional risks that New GreenLight considers immaterial or which are unknown. New GreenLight does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.TRADEMARKS

This document contains references to trademarks, trade names and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this annual report on Form 10-K may appear without the

®

or TM symbols, but such references are not intended to indicate, in any way, that the applicable owner will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.iv

SELECTED DEFINITIONS

Unless otherwise stated in this Annual Report or the context otherwise requires, references to:

| • | “ Alternative Forum Consent |

| • | “ Business Combination |

| • | “ Business Combination Agreement |

| • | “ Business Combination Marketing Agreement |

| • | “ Bylaws |

| • | “ Canaccord |

| • | “ Charter |

| • | “ Closing |

| • | “ Closing Date |

| • | “ Continental |

| • | “ DGCL |

| • | “ Effective Time |

| • | “ ENVI |

| • | “ ENVI Board |

| • | “ ENVI Class A Common Stock |

| • | “ ENVI Class B Common Stock |

| • | “ ENVI common stock |

| • | “ ENVI Units one-half of one redeemable warrant entitling the holder of such warrant to purchase one share of ENVI Class A Common Stock at a price of $11.50 per share; |

| • | “ Exchange Act |

| • | “ Former Bylaws |

v

| • | “ Former Charter |

| • | “ Former Organizational Documents |

| • | “ GreenLight |

| • | “ GreenLight 2012 Equity Plan |

| • | “ GreenLight Common Stock |

| • | “ GreenLight Financial Statements 8-K filed by New GreenLight on the date hereof and which are incorporated herein by reference; |

| • | “ GreenLight MD&A Management’s Discussion and Analysis of Financial Condition and Results of Operations of GreenLight 8-K filed on the date hereof and which is incorporated herein by reference; |

| • | “ GreenLight Preferred Stock |

| • | “ GreenLight Series A Preferred Stock A-1 Preferred Stock, SeriesA-2 Preferred Stock and SeriesA-3 Preferred Stock, in each case with a par value $0.001 per share, of GreenLight; |

| • | “ GreenLight Series B Preferred Stock |

| • | “ GreenLight Series C Preferred Stock |

| • | “ GreenLight Series D Preferred Stock |

| • | “ GreenLight Shares |

| • | “ GreenLight stockholders |

| • | “ HB Strategies |

| • | “ initial public offering IPO |

| • | “ Initial Stockholders |

| • | “ Insider Warrants |

vi

| • | “ Instruments |

| • | “ Investment Agreement |

| • | “ Merger |

| • | “ Merger Sub |

| • | “ Nasdaq |

| • | “ New GreenLight |

| • | “ New GreenLight Board |

| • | “ New GreenLight Common Stock |

| • | “ New GreenLight Equity Plan |

| • | “ New GreenLight ESPP |

| • | “ PBC |

| • | “ PBC Purpose |

| • | “ PIPE Financing |

| • | “ PIPE Investors |

| • | “ PIPE Prepayment |

| • | “ Prepaying PIPE Investors |

vii

| • | “ Private Placement Warrants |

| • | “ pro forma |

| • | “ Promissory Note |

| • | “ public common stock |

| • | “ public stockholders |

| • | “ Public Warrants |

| • | “ redemption |

| • | “ SEC |

| • | “ Securities Act |

| • | “ SIIPL |

| • | “ Sponsor |

| • | “ Sponsor Warrants |

| • | “ Subscription Agreements |

| • | “ transfer agent |

| • | “ trust account |

| • | “ Warrant Subscription Agreement |

viii

PART I

ITEM 1. | Business |

GreenLight has a clear mission: To create products addressing some of humanity’s greatest challenges through the rigorous application of science.

We aim to achieve this goal through our cell-free biomanufacturing platform. This platform enables us to make complex biological molecules—nucleic acids, peptides, carbohydrates, and many others—in a manner that we believe will allow us to manufacture high-quality products at a lower cost than traditional methods using fermentation. We are using this platform to develop and commercialize products that, if they receive appropriate regulatory approvals, address agricultural, human health and animal health issues.

Humanity faces numerous challenges. There are more than seven and a half billion people sharing the diminishing resources of Earth. This growing population needs to produce more food with the same amount of land and, at the same time, honor the global desire—and increasing technical need—to replace chemical pesticides. Not only are these pesticides facing increased consumer opposition and threat of outright bans due to environmental damage, many are losing their effectiveness.

More than half the world’s population now lives in cities, breathing the same air that carries pathogens and causes infections. Humanity needs to adapt and tackle pandemics both for those who have and for those who do not have access to good health care around the planet.

To address these issues, we need to develop high-quality, cost-effective products that can be deployed widely, including to developing countries. We believe RNA can be the critical aspect to these products.

Ribonucleic acid, or RNA, recently gained broad global prominence as

the COVID-19 pandemic

swept through the world’s population, prompting messenger RNA, or mRNA, vaccines to move from a scientific theory to a medical reality. Vaccines made using mRNA proved among the fastest to develop and the easiest to update for newer strainsof COVID-19.

While the fast rollout of mRNA vaccines helped change the course of the pandemic, this is just one part of the story. The full potential for RNA in human health has not yet been been realized. Beyond human

health, RNA-based technology

can also be deployed to address other global issues, including agricultural needs for crop protection.Our technology platform, which was initially developed to produce agricultural crop protection products and is protected by patents and

know-how,

is capable of synthesizing building blocks (nucleotides), building tools (enzymes), and instructions (DNA templates) to make dsRNA within an integrated process. The manufacturing processknow-how

that we gained from our experience making dsRNA allows us to understand some of the key aspects of producing mRNAs. For more information on our manufacturing platform and technology, see“Item 1. Business – Our Manufacturing Platform.”

We have several dsRNA-based products in our agricultural pipeline that, if commercialized, we believe can change the way in which farmers protect crops, allowing them to better utilize the land dedicated to agriculture and produce foods with less or no pesticide residue. One of these products, Calantha which is designed to manage Colorado potato beetles, has been submitted to the EPA for approval. Our other dsRNA-based agricultural products are in various earlier stages of development as compared to Calantha, our Colorado potato beetle product, ranging from proof of concept in the lab to proof of technology in the greenhouse and proof of scale in the field. See “” for additional information on the development process. In order to commercialize a product for the U.S. agricultural market, we must complete specified toxicology studies, submit a registration dossier to the EPA

Item 1. Business — Plant Health Product Pipeline — Process for developing new products

1

demonstrating that the product does not pose unreasonable risks to human health or the environment, respond adequately to any deficiencies identified by the EPA through its risk assessment process and obtain the EPA’s approval of our labeling. The EPA must also establish a tolerance level for the product or issue a tolerance exemption. We must separately obtain any applicable state or foreign regulatory approvals. For more information regarding the regulatory process, “” and “”.

Item 1.

Business –

Government Regulation – Agricultural Products

Item 1A.

Risk Factors – Risks Related to Our Plant Health Program

We are also in

pre-clinical

development ofRNA-based

vaccines directed at arresting the damage of the current viral pandemic and addressing emerging pathogens. The first candidate in this product pipeline that we hope to bring to market is aCOVID-19

vaccine, which is currently being tested on animals in toxicity studies in anticipation of filing a Clinical Trials Application, or CTA, with the South African Health Products Regulatory Authority, or SAHPRA, which, if approved, will allow clinical testing on human subjects. Depending on the results of any clinical testing in South Africa, we may decide to file an Investigational New Drug, or IND, application with the FDA for additional testing of ourCOVID-19

vaccine candidate. Other product candidates in the human health pipeline have yet to reach thePre-IND

phase. To get to thePre-IND

phase for our other product candidates in our human health pipeline, we must successfully design and test the product candidates in animal models, achieve positive results, select the product candidates to progress toIND-enabling

toxicology studies, develop chemistry, manufacturing, and controls protocols and create a development plan to discuss with the FDA as part ofpre-IND

consultations.AN INTRODUCTION TO RNA

RNA is present in all known life forms and plays an essential role in numerous biological processes but primarily provides a template by which proteins are constructed. In some organisms RNA can be the mechanism by which those templates are stored, but, in higher forms of life, it translates the code stored in the form of DNA and provides the template to convert that code into proteins by transcribing the DNA. Consequently, RNA molecules are being studied as potential products in many fields, such as agriculture (for pest control), animal health, and human health (messenger

RNA-based

vaccines and gene therapies).RNA can be transformative for human health and plant health:

| • | Human and animal health—where messenger RNA, or mRNA, can be used to express proteins which form the basis of vaccines as well as other therapies. |

| • | Plant health—where dsRNA can be leveraged to regulate the expression of a target protein by interfering with its message. Such RNA-mediated interference can form the basis for highly targeted pesticides or protection against parasites. |

RNA in agriculture

New crop-protection strategies are urgently needed as pests become resistant to existing pesticide products. Many existing products are also being limited through primary regulatory action (government regulations) or secondary regulations (food chain regulation) because of concerns about their effects on humans or the environment, with environmental concerns

including off-target toxicity

and long-term effects on crops, soil, and water. Together, these factors spur the need to develop alternative crop-protection products with new modes of action and improved safety profiles.Double-stranded RNA products in agriculture exploit a natural biological process called RNA interference (RNAi). This a biological process found in many eukaryotic organisms, which break down dsRNA that has been taken into a cell into short fragments known as

either micro-RNA or

small interfering RNA (siRNA). The presence of these small RNA fragments can lead to the degradation of the corresponding mRNA, thereby limiting or stopping the synthesis of protein specific to a particular harmful pest insect.2

RNA-based

pesticides may be able to give us more environmentally friendly ways to protect crops and beneficial insects while effectively stopping harmful pests. Much of our ability to design products that are intended to improve the environmental profile associated with crop protection products relies on our ability to design an RNA sequence that is only found in the organism(s) that we desire to manage. In this design process, we will compare the genome of our target species to the genome of other species that mayco-exist

with it, including humans. The goal is to have no overlap with the genome of other organisms by which our products would harm those organisms.RNA in human health

Messenger RNA’s features make it broadly valuable for human health. It is well known that mRNA has been used to make some of the most

effective COVID-19 vaccines

and that these vaccines have been developed quickly, which is critical for a pandemic response. More than one billion doses ofmRNA COVID-19 vaccine

have been produced. However,beyond COVID-19 vaccines,

mRNA’s features make it valuable for other vaccines and therapies. We are working on using mRNA in multiple vaccines and therapeutic applications such as an influenza vaccine, a sickle cell gene therapy and a shingles vaccine.DNA encodes the instructions for life to function. DNA is transcribed into mRNA in the cellular nucleus, and subsequently this mRNA is translated into proteins in the cellular cytoplasm. Instructions to make proteins that help perform many critical functions are transcribed from the DNA to mRNA. The mRNA consists of four ribonucleosides (Adenine, Guanine, Cytosine, and Uracil), the sequence of which determines the structure of the proteins encoded. Synthetic mRNA can be produced in manufacturing facilities for delivery into the cellular cytoplasm, enabling the cells to produce proteins as vaccines or for therapy.

mRNA has many advantages:

| • | Wide range of applications: mRNA can produce any encoded protein (intracellular, membrane-bound, or secreted), giving it many uses in vaccines, gene therapy, or for therapeutic proteins. |

| • | Transient expression: The body has mechanisms to degrade mRNA, allowing for repeat dosing and a dose response which can be tailored for the needs of the pharmaceutical product. |

| • | Fast development: Relatively simple changes to the mRNA molecule are needed to produce different therapeutic proteins, enabling a fast turnaround from gene selection to product with little need for manufacturing changes. For instance, if a booster vaccine is needed for a new variant, no changes will need to be made except to the mRNA sequence itself. |

| • | Flexible manufacturing: A single manufacturing facility can produce different vaccines and therapies, as the process is essentially the same regardless of the product. |

Until recently, it was very difficult to stabilize mRNA, understand its interaction with the human immune system, or deliver it in vivo. Addressing these challenges has allowed the development of the RNA industry and its rapid deployment as a global healthcare product.

THE IMPACT OF OUR

HIGH-QUALITY, LOW-COST RNA

We currently make multiple forms of dsRNA at a rate of 2,000 liters per batch using our cell-free manufacturing platform. We have increased our production rate from microliters to milliliters to liters to our current

2,000-liter

capacity with no material impact on quality or process yields. We believe our expertise and proprietary technology will allow us to increase batch sizes to 10,000 liters and beyond, which will allow us to reduce theper-liter

cost of our dsRNA products.3

Alternative RNA production methods are generally slow to develop and more expensive:

| • | Cell-based fermentation does not achieve the quality required for human health uses or the cost considerations for broadacre coverage in agriculture applications. |

| • | Conventional cell-free processes, such as in vitro transcription (IVT), are cost prohibitive for agricultural applications and require complex specialty input supply chains. |

GreenLight’s manufacturing platform uses:

| • | a proprietary cell-free methodology that enables production at less than $1/gram for the production of technical grade active ingredient dsRNA. |

| • | a flexible architecture that accommodates the manufacturing of a wide variety of products. |

For more information on our manufacturing platform and technology see the section titled “.”

Item 1. Business—Our Manufacturing Platform

OUR BUSINESS MODEL AND GROWTH STRATEGY

Given the advantages of our platform, we aim to make the benefits of RNA, and other biologics, accessible to everyone.

In human health, we are developing vaccines and RNA therapeutics to alleviate or cure critical diseases facing patients worldwide. In agriculture, we are developing products that promote sustainability and supplement or replace traditional pesticides and fungicides with RNA in farmers’ crop-protection programs.

Our platform gives rise to three distinct capabilities that underpin a sustainable business model and bring capabilities normally used in advanced pharma discovery to agriculture and human health:

| • | Identification: Machine learning and proprietary algorithms are key tools as we work to identify the best gene target candidates. We become more efficient and innovative as we accumulate data, and our algorithms learn. |

| • | Develop and optimize: We run parallel trials on thousands of distinct RNA sequences to design our agricultural products, which gives us many more opportunities to develop the best products. |

| • | Manufacturing: We can produce dsRNA products through our proprietary cell-free system. Our current production capacity is 2,000 liters per batch, and we are planning to build the capacity to produce dsRNA at a rate of at least 10,000 liters per batch. Production at larger capacities will allow us to achieve economies of scale by reducing labor costs and the fixed costs that we allocate to each liter of RNA that we produce. |

In the next five years, our pipeline includes seven agricultural products planned for launch and five human health products with clinical milestones, including Phase I clinical trials.

We anticipate this pipeline will demonstrate:

| • | Fast development of agricultural products.Calantha will, if approved in 2022, have taken four years from start to market compared to a typical 10-year cycle at major agribusinesses. |

| • | Rapid integration of acquisitions. We acquired Bayer’s topical RNA treatment for honeybees in December 2020. By May 2021, we were conducting further field trials and intend to be ready for regulatory submission in 2022. |

| • | Validation of our mRNA platform. We are working toward clinical proof of concept of our COVID-19 and influenza mRNA vaccines. |

4

| • | Innovative approaches to gene editing. We have the potential to tackle grave diseases such as sickle cell, for which we received a $3.3 million grant from the Bill & Melinda Gates Foundation. |

| • | Expansion of production capabilities. Our Rochester RNA manufacturing facility can produce 500 kg of dsRNA per year with the capability to expand to 1,000 kg. It currently provides samples for our field trials. |

These factors allow us to access the following major markets (with estimated total addressable market size in parentheses):

| • | Insecticides ($17 billion) |

| • | Fungicides ($16.5 billion) |

| • | Vaccines ($93 billion) |

| • | Gene therapies ($3 billion) |

Our growth strategy in plant health is to pursue significant market opportunities where RNA has the greatest potential to provide growers with improved pest control and the sustainable nature of our products (e.g., benefits to honeybees and low to no residue) delivers the most impact for society and aligns most closely with macro trends from consumers and regulators. When we use the term ‘sustainable,’ we refer to our efforts to align economic development with environmental protection and human well-being as well as our anticipated obligations as a Public Benefit Corporation under § 362(a) of the Delaware General Corporation Law.

For our plant health products, we define total addressable market as the global revenue opportunity available to pesticide solutions controlling a target pest or disease. In most instances, we do this by defining a relevant active ingredient market for the crop or crops where we intend to market our products and then making an assumption as to the percentage of that market that is spent on controlling the target pest or disease. We use data from AgBioinvestor and FAOSTAT (a database run by the Food and Agriculture Organization of the United Nations), and data purchased from third party consultants is used to quantify the market and underpin assumptions. In order to address the total insecticide and fungicide markets we identify pests or diseases in that market, develop targeted dsRNA sequences for them and attempt to develop the best delivery mechanism for that dsRNA. Over time, we intend to expand beyond RNA, building on our capabilities. In human health, we intend to pursue markets where RNA can provide better products (faster, cost effective or more efficacious) to improve standards of care for patients.

Planned products and milestones

Agricultural programs we currently have planned for launch in the next five years include protection against:

| • | Colorado potato beetle, 2022 |

| • | Varroa mite, 2024 |

| • | Botrytis, 2025 |

| • | Fusarium, 2025 |

| • | Powdery mildew, 2025 |

| • | Diamondback moth, 2026 |

| • | Two-spotted spider mite, 2026 |

Key planned human health clinical milestones in the next five years include Phase I clinical trials currently targeted for:

| • | COVID-19 vaccine, 2022 (currently in animal toxicity studies) |

5

| • | Seasonal flu vaccine, late 2022/early 2023 (currently in pre-toxicity study development) |

| • | Shingles, 2024 (currently in early stages of concept evaluation) |

| • | Supra-seasonal flu, 2024 (currently in early stages of concept evaluation) |

| • | Antibody therapy, 2024 (currently in early stages of concept evaluation) |

| • | Sickle cell disease product concept, 2025 (currently in early stages of concept evaluation) |

Our

Covid-19

vaccine has successfully completed preclinical testing and we are preparing a Clinical Trials Application, or CTA, with the South African Health Products Regulatory Authority, or SAHPRA, which, if approved, will allow clinical testing on human subjects. Depending on the results of any clinical testing in South Africa, we may decide to file an Investigational New Drug, or IND, application with the FDA for ourCOVID-19

vaccine candidate. Our other product candidates in the human health pipeline have yet to reach thePre-IND

phase. To get to thePre-IND

phase for our other product candidates in our human health pipeline, we must design and test the product candidates in animal models, select the product candidates to progress toIND-enabling

toxicology studies, develop chemistry, manufacturing, and controls protocols, and create a development plan to discuss with the FDA as part ofpre-IND

consultations.In order to begin any Phase I clinical trials, we must first successfully complete the toxicity study for the product candidate, submit an IND application to the FDA, which will include the scope of our proposed Phase I clinical trial, and satisfy any conditions the FDA may require for the IND to become effective. Additionally, in order to begin our Phase I clinical trials, we must first produce the Phase I clinical drug substance for each of the product candidates, which will require us to complete the.” Our Burlington facility completed the production of the drug substance for the Phase I clinical trial of our COVID-19 vaccine product candidate. Fill and finish manufacturing is planned for the first and second quarter of 2022.

start-up

of the two clean room suites that we recently leased in Burlington, Massachusetts, including compliance with applicable GMP regulations and conformity to our chemistry, manufacturing and controls protocols. Our Burlington facility is currentlyGMP-ready.

See “Item 1A. Risk Factors — Risks Relating to Our Manufacturing Platform

OUR MANUFACTURING PLATFORM

Our platform, developed through 13 years of research and technology development, is protected by foundational patents and

know-how

that address barriers cell-free technologies have faced for many years.Biologic production through living cells faces a range of constraints. These include the cell’s priority for self-preservation, which fights against RNA production, reducing yield and quality.

Conventional cell-free production breaks open the cells and removes the need to balance bioprocessing against self-preservation. But energy management in this method limits yield and quality, making RNA production prohibitive for many agricultural applications in terms of cost, scale, and speed.

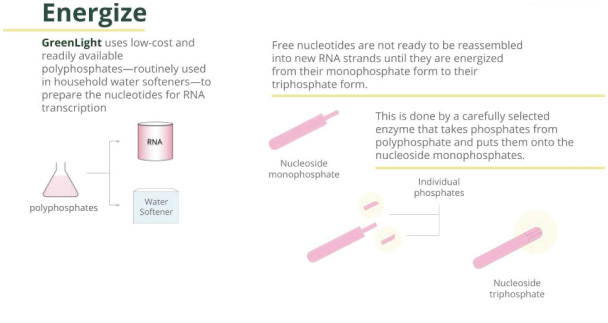

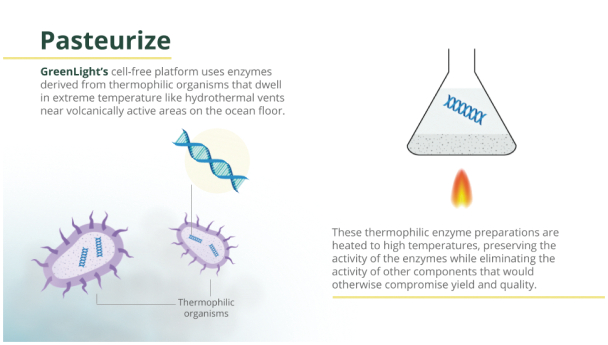

Our proprietary cell-free process regenerates the energy needed for bioprocessing using ingredients that can include polyphosphates and enzymes.

Each step in the GreenLight bioproduction processes has been developed or selected with cost and functionality in mind.

| • | The key raw material for dsRNA can be obtained in large quantities from such sources as industrial fermentation processes (e.g., derived from yeast). |

| • | Our proprietary process allows us to energize naturally occurring nucleoside monophosphates at low cost using inorganic polyphosphate, which is readily available and affordable. |

6

| • | Thermophilic enzymes are employed to facilitate the production of high-energy nucleotides. The utilization of thermally stable enzymes allows high temperature to be incorporated in their preparation, providing a way to mitigate undesirable contaminating activities (e.g., RNA-degrading enzymes,DNA-degrading enzymes, nucleotide-degrading/altering enzymes, protein-degrading enzymes) from entering the RNA synthesis portion of the process and affecting quality and yield. |

| • | We believe our process know-how and the technology we developed can be leveraged for our mRNA platform. |

Overview of manufacturing process for agriculture

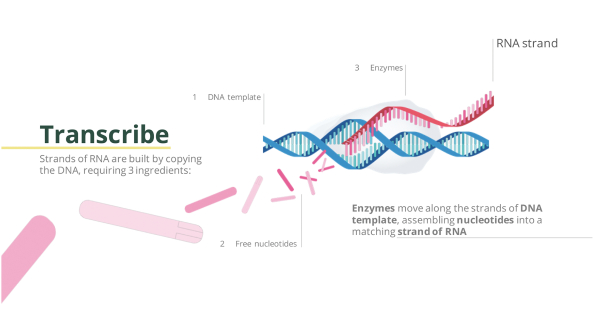

Our proprietary dsRNA manufacturing process for agriculture begins with a cellular RNA (e.g., from yeast).

This is then broken up (depolymerized) into RNA building blocks (commonly known as NMPs) using a nuclease enzyme. Our cell-free production process uses carefully selected enzymes to energize and polymerize the building blocks into a desired RNA according to a corresponding DNA template.

Cell-free production of dsRNA for agriculture

While the advantages of dsRNA for agriculture have been known for some time, production cost has been a barrier.

The dsRNA production process, simplified

7

8

The outcome from our system is fast, with reaction times of two hours. We have successfully increased production from 50 microliters to more than 1,000 liters without significant loss in performance.

Overview of manufacturing process for human health

We have deep understanding and expertise in RNA manufacturing, design, and analysis. The many years of experience from our dsRNA platform are applicable to our human health mRNA platform. We are continually leveraging what we learn and applying it to mRNA production for human health applications.

State-of-the art

Covid-19

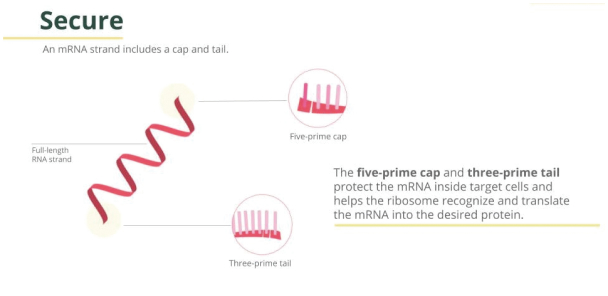

mRNA vaccines) employs in vitro transcription (IVT). The process depends on a ready supply of highly purified reagents, including chemically produced nucleoside triphosphates (NTPs), an RNA polymerase enzyme, and a DNA template. RNA is synthesized, capped, and tailed for protein translation and encapsulated in lipid nanoparticles (LNP) for delivery to target cells in the patient. Importantly, mRNA used for human health requires purification steps to reach the highest quality levels expected by regulatory agencies.Encapsulation

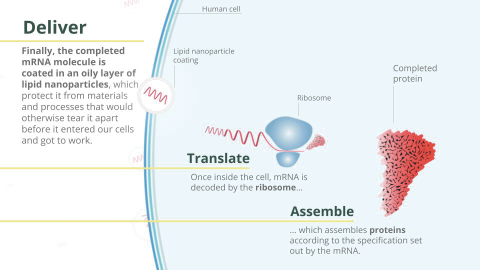

Our current mRNA drug product is based on lipid nanoparticles that encapsulate mRNA molecules, protecting them from degradation. Those nanoparticles enable mRNA uptake into the cells so that the mRNA can be used to express the protein of interest.

Our current nanoparticles are made of four lipids: the ionizable lipid that drives encapsulation and release of mRNA, two “helper” lipids that mainly provide stability to the particle itself, and a polyethylene-glycol lipid that prevents particle aggregation as well as opsonization once those particles are injected in the bloodstream.

The manufacturing process

for mRNA-LNP involves

two liquid streams colliding at high velocity ina jet-mixing chamber.

One of the streams contains the lipids in organic solvents and the other stream contains the mRNA in acidified water. The mixing at high velocity reduces solubility of the lipids so that homogeneous nanoparticles are formed around a core made of mRNA and ionizable lipid.9

After the mixture is quenched to stop particle growth, the organic solvent is removed, the pH is neutralized, and

the mRNA-LNP is

concentrated.A cryoprotectant is added at the end of the process before the product is sterile-filtered and stored in ultra-cold conditions.

10

Supply for research and development

We have a team dedicated to the manufacturing of materials for discovery and preclinical research in Massachusetts. Our team produces 1 to 20 mg of mRNA with a turnaround time of a few weeks, and we have

technology-transferred in-house LNP

manufacturing capability to support preclinical and clinical studies.Supply for clinical trials

In August 2021, we began activating a manufacturing facility in Massachusetts that is capable of producing material for clinical trials and is implementing current good manufacturing practice (cGMP) systems to support the use of these materials in human trials. The first clinical materials to be produced in this facility, which were for our

COVID-19

vaccine candidate, were manufactured in 2021, and we expect to follow with production for other programs entering the clinical phase. We have also produced mRNA and LNP formulations forIND-enabling

toxicology studies under Good Laboratory Practice (GLP) procedures. We contract specialized third parties that meet our requirements and are experienced in cGMP fill-finish operations.Our manufacturing for agriculture: Rochester (dsRNA)

Our dsRNA manufacturing facility in Rochester, New York, is designed for process development while generating samples for research and market development with a 1,000 kg dsRNA production design basis. The facility has a raw material storage and handling area, high

bay wet-processing area

with floor drains, two,1,200-liter

fermenters,2,000-liter

cell-free reactors, NMP preparation tanks, formulation, packaging, development laboratory, analytical laboratory, loading dock, and cold storage areas. This plant currently has 15 process engineers, technicians, research associates, and quality-control personnel for commercial production of plant health products.In the third quarter of 2021, we increased production of dsRNA from microliter, milliliter and liter quantities in the lab to 2,000 liters per batch using a single bioreactor installed at our Rochester facility with no material impact on quality or process yields. We estimate that we can currently produce 500 kg of dsRNA per year with this capacity. We have also installed a second

2,000-liter

bioreactor at our Rochester facility as part of our plan to increase manufacturing capacity. If brought online, this bioreactor would double our capacity to 1,000 kg of dsRNA per year. If we obtain the appropriate regulatory approvals to commercialize our products as we project in our agricultural product pipeline, we expect that this capacity will enable us to meet our agricultural product needs throughmid-2024.

We are currently designing an expansion of our Rochester facility to further increase our manufacturing capacity of dsRNA for agricultural use and have recently leased an additional 5,577 square feet of laboratory space in Rochester for this added capacity.11

Our manufacturing for human health (mRNA)

We currently make mRNA at our cleanroom facility in Burlington, Massachusetts. We have scaled our production to approximately three liters and plan to use a contract development and manufacturing organization, or CDMO, to produce mRNA in larger quantities.

We have agreements to produce early clinical materials for the

COVID-19

program, which are expected to be filled, labeled, and packaged for the clinic by contract manufacturing organizations.Our Burlington facility completed the production of the drug substance for the Phase I clinical trial of our COVID-19 vaccine product candidate. Fill and finish manufacturing is planned for the first and second quarter of 2022.

We are implementing cGMP systems to support clinical production using our process.

We produced our first

3-liter

clinical batch using our proprietary process and will use the wild-type WuhanCOVID-19

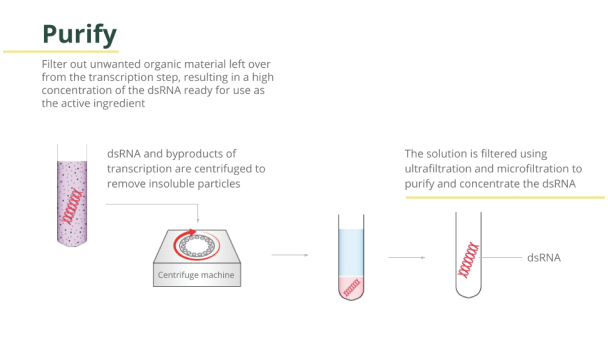

strain. This material will follow the same supply chain but will use an IVT production process currently in development, akin to existing vaccines, in the upstream.The downstream purification process consists of filtration and chromatography steps. The purified material is formulated in a lipid nanoparticle system. The material is then sent to a contract manufacturer to fill into vials and is stored frozen.

In November 2021, we engaged Samsung Biologics Co., Ltd. (“basis for each year under that agreement, for our minimum purchase commitments, as determined pursuant to the terms of the Samsung Agreements. Based on our minimum purchase commitments, we expect to pay Samsung a minimum of approximately $11.5 million in service fees under the Samsung Agreements, excluding the cost of raw materials, which we must supply to Samsung separately. These fees include initial technology and analytical method transfer fees, process development and

Samsung

”) as a contract development and manufacturing organization for our mRNACOVID-19

vaccine pursuant to a Master Services Agreement (the “MSA

”) and a Product Specific Agreement (the “PSA

”, and together with the MSA, the “Samsung Agreements

”). Under the Samsung Agreements, Samsung will perform pharmaceutical development and manufacturing services for us over a period of years at its South Korean facility in exchange for service fees. Under these agreements, we must purchase certain minimum quantities of drug products. We agreed that, if we enter into a purchase agreement for commercial quantities of drug product, we will pay Samsung, on a minimumtake-or-pay

scale-up

fees, process characterization fees, an annual project management fee, andper-batch

engineering and cGMP run fees. Based on our current schedule, we expect to incur the substantial majority of these expenses in 2022 and a portion in 2023. If we move to commercial production, the agreement provides for additional process validation, inspection, cleaning, stability testing and commercial production fees, most of which would be incurred on aper-batch

basis.The Samsung Agreements will terminate on December 31, 2026, unless earlier terminated or extended in accordance with their terms. If we terminate the Samsung Agreements, we will generally be responsible for paying the purchase price for our aggregate product commitment for the remainder of the term, less any amounts we have already paid. Samsung agreed that, at or before the end of the term of the Samsung Agreements, it will assist us to transfer the commercial scale manufacturing process to a facility designated by us. The Samsung Agreements impose limits on Samsung’s liability to us for breaches of the agreements.

HUMAN HEALTH PRODUCT PIPELINE

Our mRNA platform consists of:

| • | The manufacturing process used to produce the product (described above) |

| • | The mRNA molecule |

| • | The delivery vehicle it uses to reach the target tissue |

12

All elements of the platform affect product characteristics, such as purity, potency, and immunogenicity, so our teams work on optimizing mRNA molecules and delivery vehicles for a given indication, and the performance and cost of the manufacturing process.

mRNA molecule design

Changes in the mRNA molecule will result in changes in the protein we are looking to express, the immune response to the product, and mRNA stability and potency.

First, we must choose the right target protein, after which an mRNA has to be designed for it. A well-designed mRNA molecule can carry instructions for the relevant protein, to be expressed efficiently and for the desired duration. The mRNA composition can be optimized to avoid undesirable immune responses while increasing protein expression, referred to as product potency.

Delivery vehicles

To facilitate the mRNA to reach its destination without degradation, we must formulate it into a delivery vehicle. The delivery system’s design can influence potency, immunogenicity, and the product’s shelf life.

One such delivery system consists of encapsulating mRNA in lipid nanoparticles (LNPs). We work with several established companies that have extensive experience in clinical LNPs for our vaccine candidates. We are able to routinely produce our mRNA-containing LNPs to support our research and development efforts. In addition, we work on stabilizing the LNPs to improve the storage conditions and shelf life of our products.

Our human health pipeline

We are currently working on two modalities:

| • | Prophylactic vaccines for infectious diseases |

| • | Gene therapies |

We are exploring ways to expand our pipeline to include additional therapeutic areas, including using antibodies, in the future.

Prophylactic vaccines for infectious diseases

The objective of a prophylactic vaccine is to expose the body to a protein which is present in the disease-causing virus or bacterium, called the antigen, so that it can generate an immune response in the absence of the pathogen and be prepared to fight the actual infection, should it occur in the future. mRNA can potentially be used to encode the antigen as a way to expose the body to a component of the pathogen, avoiding the use of a whole infectious agent.

Vaccines that use mRNAs present significant advantages compared

to non-mRNA vaccines,

including:| • | The antigen expressed is a true match to the protein present in the pathogen, thus increasing the potential for quality of the immune response as compared to vaccines produced through other methods, in which manufacturing processes may result in changes to the antigen. |

| • | The short development time from antigen selection to clinical trials makes mRNA ideal for emerging epidemics or pandemic response. This is why mRNA vaccines have been among the fastest developed for COVID-19. |

| • | The same manufacturing plant can be used to produce different mRNA vaccines. |

13

Opportunity

Immunization with prophylactic vaccines has become one of the most successful of all healthcare interventions. It is estimated that vaccines prevent 6 million deaths every year. The global vaccine market in 2019 was estimated at $33 billion, with the surge of

the COVID-19 pandemic

representing a significant growth in the market to $93 billion in 2020.Our COVID-19 vaccine

candidateUnmet need

Although a large portion of the population in high-income countries has been vaccinated

against COVID-19, widespread

vaccination is not expectedin mid- and low-income countries

until mid-2022 or

early 2023. Tokeep COVID-19 at

bay, a periodic booster may be necessary as global herd immunity is unlikely to be achieved. Current research is ongoing to determine if booster shots will be necessary to cover waning immunity or new variants.Product concept

Our COVID-19 vaccine

candidate,GLB-CoV-2-043,

a SARS-CoV-2 variant

Achievements to date and future milestones

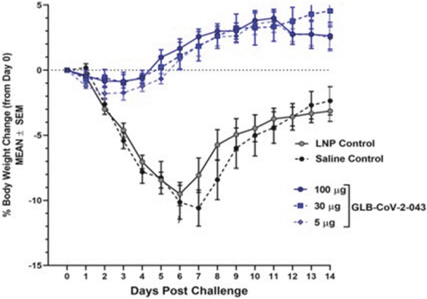

Ourvirus (isolateprovided protection fromchallenge using percent body weight (% BW) change as a criterion. We observed a statistically significant (p < 0.0001) reduction in weight loss, compared to controls on Day 6, the peak of disease, and Day 14, the end of the challenge study.

COVID-19

vaccine candidate has successfully completed preclinical testing, and we are preparing to file a Clinical Trials Application, or CTA, with the South African Health Products Regulatory Authority, or SAHPRA, seeking approval to initiate phase 1 clinical studies in South Africa. Hamsters (16/group) were immunized at day 0 and 21 at three dose levels of 5 µg, 30 µg, and 100 µg of vaccine or controls of saline or LNP. At day 40 of the study the animals were intra-nasally challenged with liveSARS-CoV-2

USA-WA1/2020).

Animals were followed for 14 days, and their weights were taken daily. This hamster challenge study revealed that all doses ofGLB-CoV-2-043

SARS-CoV-2

Body weight changes of vaccinated hamsters afterviral challenge,the GreenLight vaccine candidate.

SARS-CoV-2

GLB-CoV-2-043:

14

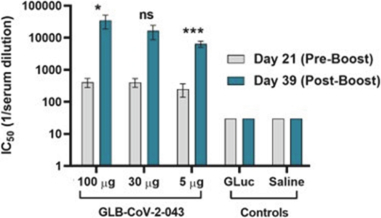

Hamsters (8/group) were immunized at day 0 and 21 at three dose levels of 5 µg, 30 µg, and 100 µg of vaccine or controls of saline or LNP (GLuc). Blood draws at day 21virus (isolate

(pre-boost:

before injection of the second vaccine dose), and day 39 (post-boost: that is, 18 days after the second dose) were tested for neutralizing antibody titers against liveSARS-CoV-2

USA-WA1/2020).

All vaccine doses tested induced significantly higher levels ofneutralization titer compared to controls, both Pre and Post-Boost. The 100 µg and 30 µg doses ofinduced statistically significantly or trending towards statistically significantly higher titers of neutralizing antibodies compared to control immunized animals. Thevaccine displayed a clear dose response after boost. These results demonstratedvaccine candidate induces high titers of functionalcapable of neutralizing virus entry into cells.

SARS-CoV-2

GLB-CoV-2-043

GLB-CoV-2-043

that GLB-CoV-2-043 mRNA

anti-SARS-CoV-2

*: p<0.05

***: p<0.001

ns: p=0.0523 (not significant)

The above chart presentsserum neutralizing antibody titers (ICat day 21 (three weeks after the first vaccination dose) and at day 39 (18 days after the second vaccination dose).is the GreenLight vaccine candidate.

SARS-Cov-2

50

, or inhibition concentration at 50%) for hamsters vaccinated withGLB-Cov-2-043

GLB-COV-2043

We have had

a pre-IND consultation

with the FDA regarding our approach to IND and Phase I clinical testing. We commencedIND-enabling

toxicology studies in the third quarter of 2021. We have a license for an LNP from an established company forour COVID-19 vaccine

candidate.Upon approval of our CTA by SAHPRA, we expect to initiate a phase 1 safety and immunogenicity clinical trial in South Africa in the first half of 2022. We are also seeking partnership opportunities with a pharmaceutical company to conduct late-stage clinical trials and commercialize our vaccine. If we successfully complete our planned clinical trials, we plan to analyze the data and assess whether to submit an application package to regulatory authorities in jurisdictions outside the U.S. for emergency or full marketing authorization. It is possible that the regulatory authorities will no longer be accepting Emergency Use Authorization (EUA) submissions (or their equivalent) for

COVID-19

vaccines at that time. If that is the case, we would need to assess whether and to what extent additional data would be needed to submit a Biologics License Application (BLA), or its equivalent in other jurisdictions, for full marketing authorization.15

Our seasonal influenza vaccine candidate

Unmet need

Commercial influenza vaccines typically have a mismatch between the strains selected for the season and the strains circulating during the season, because selection occurs six months before influenza season—given the time required to manufacture vaccines. This, along with the viral mutations that occur in eggs during the manufacturing process, results in a variable vaccine efficacy of between 40% and 60%.

Along with manufacturing-process

challenges, egg-based vaccines

are slow to produce and there would likely be an insufficient supply of eggs to produce the vaccines necessary in a pandemic setting.Our product concepts

Our influenza vaccine candidate is a multivalent vaccine consisting of mRNA encoding for two types of antigens, hemagglutinin (HA) and neuraminidase (NA), formulated in LNPs. We believe this combination of antigens has the potential to provide a protective immune response to influenza viruses.

Achievements to date and future milestones

We have formulation design and testing activities underway for our seasonal influenza mRNA vaccine program. We are testing prototype formulations in mice and ferret models, and plan to evaluate resulting data and consult with the FDA to select a candidate for

pre-clinical,

IND-enabling,

toxicology testing. Based on our current projected timeline, and if our preclinical studies are successful, we anticipate selecting a clinical candidate, in the first half of 2022 to undertakeIND-enabling

toxicology studies for a clinical Phase I trial starting in 2023 . We have an option to license LNP for our influenza vaccine candidate from an established LNP company. We will seek partnership with an established pharmaceutical company to conduct clinical development trials and, if our clinical studies are successful, commercialize our influenza vaccine.Gene therapies

There are thousands of genetic diseases caused by mutations in single genes. Patients with many of these diseases are not yet well-served by existing therapies. Although there are treatments for certain genetic diseases, sometimes the treatments alleviate symptoms temporarily or require organ, bone marrow, or stem cell transplants. These are costly, time-consuming, and logistically challenging. We aspire to develop our technology to edit the specifically targeted gene to treat such diseases by simple injections of mRNA/LNP formulations consisting of the gene and molecular machinery for its integration into the genome.

Our sickle cell disease gene product concept

Unmet need

Sickle cell disease affects about 100,000 people in just the United States and is prevalent in people of African and Middle Eastern descent. There is no cure for sickle cell disease, and current treatments focus on managing the pain crises and other effects such as anemia. Current treatment regimens—including blood transfusions and bone marrow transplants—are costly, invasive, and impractical for treating large segments of affected patient populations. Gene therapies currently in development for sickle cell disease are cell therapies, which require facilities close to the patient that can edit the cells outside of the body, posing an additional challenge for populations in remote areas or without adequate facilities to perform the editing.

Current approaches to gene therapy have challenges to overcome. Therapies that use adeno-associated viruses (AAVs) as vectors can encapsulate and deliver genetic material of up to 5,000 base pairs only, which limits the diseases to which this technology can be applied.

16

Product concept

Our RNA-based gene

product concept is to design a product candidate to deliver a healthy copy of the gene to stem cells. We believe our gene therapy concept has the potential to be:| • | Accessible: Based on our cost-competitive RNA platform and with an in vivo administration, we believe our therapy will enable us to bypass the need for facilities required to edit the cells ex vivo. |

| • | Targeted: The delivery technology targets specific cells in tissue. |

| • | One dose and done: Our strategy is to target precursor stem cells to provide long-lasting expression. |

| • | Versatile: Our therapy has the potential to encode for full-length genes and address genetic indications that require therapy in nondividing cells. |

Our work in gene therapy is supported by the Bill and Melinda Gates Foundation. This work involves reduction to practice of novel approaches for gene therapy using mRNA and cell/tissue targeting. We anticipate being ready for preclinical toxicology studies at the end of 2024.

Early Stage R&D

Our supra-seasonal influenza and antibody therapy targets utilize the mRNA platform technology used for our

SARSCoV-2

vaccine candidate. These targets are currently in the early stages of concept evaluation in terms of antigen or protein design andin-vitro

testing. If we succeed in these endeavors we anticipate selecting clinical candidates in 2024.GLOBAL RNA MANUFACTURING NETWORK

Our vision is to enable Africa, Asia, and Latin America to meet local demand through production outside the United States and Europe, from drug substance to product to fill and finish of mRNA vaccines and therapies, ideally in the country where the vaccine will be sold. If our vaccines and therapies are approved in these jurisdictions, we intend to contract with local manufacturers to produce our products, which we believe will enable the accessibility and cost competitiveness of our products.

If we obtain applicable regulatory approvals, we intend to create an interoperable network with local production facilities deploying our manufacturing process using modular design concepts that can be

constructed off-site and

set up more quickly than traditional construction models, so each facility will rely less on international supply chains to create vaccines and therapies for local needs.STRATEGIC COLLABORATIONS

Collaborators are part of our core strategy as we seek to accelerate our development of RNA therapies. We have relationships with research hospitals, universities, foundations, biotechnology companies, pharmaceutical companies, and nongovernmental organizations with expertise in our pipeline programs. During research and development stages, we seek collaborators to complement our preclinical studies and manufacturing capabilities. At the clinical development stage, we will seek established collaborators to codevelop or commercialize our product candidates. For vaccines, we are seeking companies with commercial capabilities that will receive rights to develop and commercialize our vaccine candidate. In this way, we can share the risk and reward of our portfolio while acquiring the capabilities required to launch commercial products. We seek partners aligned with our mission of making RNA accessible to the world.

Our decision to partner will be determined by the partner’s geographic scope and the complementary capabilities that partner can bring to support the commercialization of products. We have yet to choose either the

17

products for which we choose to partner, or the partners themselves; however, we may also choose to commercialize some early-stage programs without partners, as large-scale commercial capabilities may not be required for programs with a small patient population.

PLANT HEALTH PRODUCT PIPELINE

Overview

We plan to design, build, and sell a complete portfolio of products that growers can use throughout the food chain, from field to fork, to enhance, protect, and preserve produce and animals.

Our product pipeline is based on double-stranded RNA, or dsRNA, which works by regulating the expression of a carefully selected protein in the target organism, be it in plants, fungi, or animals (primarily insects or arachnids). This method can, with careful selection of the appropriate target, potentially be used to control a wide range of unwanted pests and problems.

An introduction to dsRNA and agriculture

As a tool for crop protection, dsRNA has several advantages. It is designed to impact the target pest and limit harm to, there is a long-established view that dietary intake of nucleic acids, including dsRNAs from plant viruses, does not present a health risk to humans and other vertebrates, and, as a result, the adoption of RNAi technology in agriculture is likely to present a lower human health risk than the use of conventional pesticides.

any non-targeted organisms.

Unlike many other pesticides, dsRNA degrades quickly in the environment, so it is typically undetectable after a few days, meaning in typical use, treated produce would contain low to no pesticide residue. Finally, in the event any residue remains, there is an established history of safe consumption of RNA molecules in human and animal food. According to a September 2020 report published by the Environmental Directorate of the Organization for Economic Cooperation and Development entitled Considerations for the Environmental Risk Assessment of the Application of Sprayed or Externally AppliedPesticides

ds-RNA-Based

Based on our toxicity testing and these advantages of dsRNA, GreenLight has requested a tolerance exemption from the EPA for the active ingredient contained in its first dsRNA product, GS2, which seeks to control Colorado Potato Beetle in potatoes and other solanaceous crops. If granted, such an exemption would be consistent with a category IV toxicity level, the EPA’s lowest level of pesticide toxicity under FIFRA.

Process for developing new products

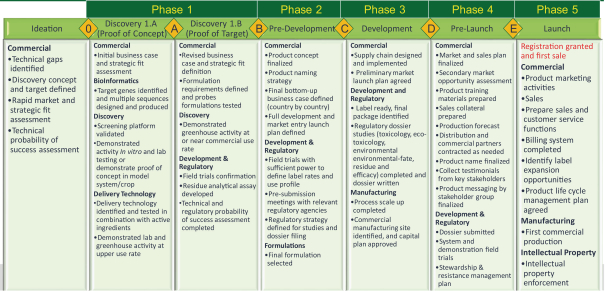

GreenLight uses a five-phase product development process for plant and animal health products as summarized in the following table. In general, in order for a product to move to a particular stage, it must successfully have met the requirements of the preceding stages.

18

Market opportunity

Given the versatility

of RNA-based solutions,

we believe that the markets for our products are large. In the near term, we intend to pursue more than $10 billion in addressable target markets for plant health, with the full launch of our first product anticipated in 2023.We define total addressable market as the global revenue opportunity available to pesticide solutions controlling a target pest or disease. In most instances, we do this by defining a relevant active ingredient market for the crop or crops where we intend to market our products and then making an assumption as to the percentage of that market that is spent on controlling the target pest or disease. We use data from AgbioInvestor and FAOSTAT (a database run by the Food and Agriculture Organization of the United Nations), and we use data purchased from third-party consultants to quantify the market and underpin assumptions.

We intend to develop products for our own distribution as well as for commercial partners. In doing so, we will focus our attention on the fresh fruits, vegetables, and nuts markets, which urgently need residue-free crop- protection products or have a strong association with the need to conserve honeybees. We will seek to serve the broadacre markets and international markets through partnerships with established multinational crop-protection companies and distributors. We intend to develop products that farmers trust and incorporate as a regular part of their annual crop-protection program.

Each of the initial products we are developing is intended to be specific to one target pest based on grower needs. We believe we can leverage our expertise in RNA in the future to target multiple pests as well as use our manufacturing platform and experience to make novel products at a cost that works for farmers.

What specific problems are we trying to solve?

Our Plant Health group is working to provide growers with highly effective tools to use within their normal cultural practices that avoid

disrupting non-target organisms

while leaving low to no residue in the treated produce. Today there are very few commercially available products that successfully combine these characteristics that growers, regulators, and consumers desire. Our primary focus for this mission is the successful deployment of carefully designed dsRNA. In order for our products to function successfully, the organism that needs to be managed must possess the appropriate cellular apparatus to process exogenous dsRNA to regulate protein biosynthesis. For these organisms, we intend to develop a portfolio of insecticides, acaricides, fungicides, and products that affect crop physiology and health, such as bio stimulants and herbicides.19

Insecticides and acaricides

Our insecticides and acaricides program is currently working on six major targets with a combined addressable target market size of $4.4 billion. These projects are distributed across various phases ranging from the most advanced, which is in

the pre-commercial phase

awaiting regulatory approval, to nascent candidates. We calculate addressable markets for our projects using market data from AgbioInvestor and FAOSTAT and information purchased from third-party consultants. We use this data as well as our industry knowledge to inform assumptions around expenditures to control the target pest or disease to arrive at the addressable market.Calantha, our program to control the Colorado potato beetle, has been submitted to the EPA for approval. Another, aimed at Varroa mites, is expected to be submitted to the EPA in 2022. We anticipate moving the program for diamond back moth to the field in 2022 or 2023, with EPA submission in 2023. Additionally, we project to submit our two spotted spider mite product to the EPA for approval in 2024.

Colorado potato beetle

Calantha, our product candidate for the Colorado potato beetle (), which decimates plants in the nightshade family and accounts for more than $500 million in crop loss annually, has gone from discovery to Environmental Protection Agency (EPA) submission in four years. The application is mixed with water and sprayed using standard agricultural practice over crops at a rate of 9.9 grams per hectare—less

Leptinotarsa decemlineata

than one-tenth the

rate at which many conventional industrial chemicals are normally used on fields. Consumption of the dsRNA, which itself degrades within days, causes the Colorado potato beetle to stop eating and expire from its own toxins while beneficial insects are unaffected. In the United States, we have tested this product over the last three annual growing seasons in Oregon, Washington, Wisconsin, New York, Maine and Idaho. We have also conducted field tests of the product in Spain, Germany and France.We believe the addressable market for protecting crops from the Colorado potato beetle is approximately $350 million. Assuming EPA approval in 2022, we anticipate full commercialization in 2023.

Widely recognized for its ability to develop resistance to pesticides, the Colorado potato beetle was first described as a pest in the United States in 1859.

We expect the price and performance of Calantha, the first-ever foliar RNA product—submitted for regulatory approval with the EPA in October 2020—to be competitive with other products currently available to farmers. We have conducted more than 100 field trials over four years to develop a product that is effective at just 9.9 g/hectare, an extremely low active ingredient use rate, equivalent to a spoonful of sugar spread on a football field.

Our testing has shown that Calantha is safe for honeybees, butterflies, and several

other non-target insects

and mammals at use rates 100 times higher than our recommended rate. It degrades in water and soil within three days to benign, natural nucleotides. The product works well with standard growers’ programs to control first- or second-generation Colorado potato beetle. It effectively controls all stages of the life of this beetle but is most effective on young larvae upto one-quarter inch

in length.In addition to being water soluble, this product contains additional inert ingredients to allow it to be mixed with other agricultural products and applied by farmers in a single spraying using common methods,

including low-water volume

(aerial or ground) or chemigation. Although conventional pesticides can require special protective equipment for farmers, we anticipate just basic work gloves will be required for this product.Varroa mites

Having acquired the rights to portions of Bayer’s topical RNA intellectual property portfolio, which

include bee-health assets,

we are developingan RNA-based syrup

that targets reproductive mites, is easy to use, and will add another tool in the limited Varroa-control market.20

We have been field testing our

RNA-based

product candidate for the Varroa destructor mite, which many beekeepers consider to be the top threat to honeybees and which has been detected in up to 90% of US hives, since March 2021 with the assistance of commercial beekeepers in Georgia, California, Florida, and Maine. To date, these tests demonstrate a measurable improvement in hive health. Hive health is measured by bee management personnel through a visual assessment of open broods (uncapped hive cells containing larvae) and closed broods (capped hive cells containing larvae) and the assignment of scores based on that assessment. The assessment also includes a scored evaluation of the overall health of the hive, including appearance and productivity of drones, brood health and queen health. Hive health measurements attempt to take into account a variety of factors other than mite count and include potential harmful effects from the pathogens mites can introduce into the hive, the potential harmful effects of chemical pesticides and other environmental factors that can affect overall hive health. Our tests measured hive health 12 weeks after application of our Varroa mite product and demonstrated a 20% improvement in open brood health (p=0.0193), a 20% improvement in closed brood health (p=0.0163) and a 17% improvement in overall hive health (p=0.0200), compared to hive health measured 12 weeks after application of the commercial standard chemical Varroa mite control product. As part of our hive health assessments, we also assess mite population and control before and after application of our product, using guidelines from the USDA’s Agricultural Research Services for measuring mite populations. Using these guidelines in our field tests, we observed a decline in mite population of 80% 6 weeks after treatment (p=0.0073) and 77% 12 weeks after treatment (p=0.0106) after the application of our product.About 3 million commercial honeybee colonies in the United States are used to pollinate more than 100 crops annually that are worth an estimated $15 billion, according to the U.S. Department of Agriculture. The parasitic Varroa mite reproduces in hives, feeds on honeybees, and spreads disease, destroying colonies across the globe. Now in the development phase, our product candidate targets the Varroa mite to protect bees, beekeepers, and pollination-dependent crops.