Exhibit (17)(a)

MASSMUTUAL SELECT FUNDS

This Prospectus describes the following Funds:

Fund Name | Class I | Class R5 | Service Class | Administrative Class | Class A | Class R4 | Class R3 | |||||||

MassMutual Select Total Return Bond Fund | MSPZX | MSPSX | MSPHX | MSPLX | MPTRX | MSPGX | MSPNX | |||||||

MassMutual Select Strategic Bond Fund | MSBZX | MBSSX | MBSYX | MSBLX | MSBAX | MSBRX | MSBNX | |||||||

MassMutual Select BlackRock Global Allocation Fund | MGJIX | MGSSX | MGSYX | MGSLX | MGJAX | MGJFX | MGJRX | |||||||

MassMutual Select Diversified Value Fund | MDDIX | MDVSX | MDVYX | MDDLX | MDDAX | MDDRX | MDVNX | |||||||

MassMutual Select Fundamental Value Fund | MFUZX | MVUSX | MFUYX | MFULX | MFUAX | MFUFX | MFUNX | |||||||

MassMutual Select Large Cap Value Fund | MLVZX | MLVSX | MMLYX | MLVLX | MMLAX | MLVFX | MLVNX | |||||||

MM S&P 500® Index Fund | MMIZX | MIEZX | MMIEX | MIEYX | MMFFX | MIEAX | MMINX | |||||||

MassMutual Select Focused Value Fund | MFVZX | MFVSX | MMFYX | MMFVX | MFVAX | MFVFX | MFVNX | |||||||

MassMutual Select Fundamental Growth Fund | MOTZX | MOTCX | MOTYX | MOTLX | MOTAX | MFGFX | MOTNX | |||||||

MassMutual Select Blue Chip Growth Fund | MBCZX | MBCSX | MBCYX | MBCLX | MBCGX | MBGFX | MBCNX | |||||||

MassMutual Select Growth Opportunities Fund | MMAZX | MGRSX | MAGYX | MAGLX | MMAAX | MMGFX | MMANX | |||||||

MassMutual Select Mid-Cap Value Fund | MLUZX | MLUSX | MLUYX | MLULX | MLUAX | MLUFX | MLUNX | |||||||

MassMutual Select Small Cap Value Equity Fund | MMQIX | MMQSX | MMQYX | MMQLX | MMQAX | MMQFX | MMQTX | |||||||

MassMutual Select Small Company Value Fund | MSVZX | MSVSX | MMVYX | MMYLX | MMYAX | MMVFX | MSVNX | |||||||

MM S&P® Mid Cap Index Fund | MDKZX | MDKIX | MDKSX | MDKYX | MDKAX | MDKFX | MDKTX | |||||||

MM Russell 2000® Small Cap Index Fund | MCJZX | MCJIX | MCJSX | MCJYX | MCJAX | MCJFX | MCJTX | |||||||

MassMutual Select Mid Cap Growth Equity II Fund | MEFZX | MGRFX | MEFYX | MMELX | MEFAX | MEFFX | MEFNX | |||||||

MassMutual Select Small Cap Growth Equity Fund | MSGZX | MSGSX | MSCYX | MSGLX | MMGEX | MSERX | MSGNX | |||||||

MassMutual Select Diversified International Fund | MMZIX | MMZSX | MMZYX | MMZLX | MMZAX | MMZFX | MMZTX | |||||||

MM MSCI EAFE® International Index Fund | MKRZX | MKRIX | MKRSX | MKRYX | MKRAX | MKRFX | MKRTX | |||||||

MassMutual Select Overseas Fund | MOSZX | MOSSX | MOSYX | MOSLX | MOSAX | MOSFX | MOSNX |

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this Prospectus. Any statement to the contrary is a crime.

PROSPECTUS

February 1, 2017

– 1 –

MASSMUTUAL SELECT FUNDS

Supplement dated May 8, 2017 to the

Prospectus dated February 1, 2017

This supplement provides new and additional information beyond that contained in the Prospectus and any previous supplements. It should be retained and read in conjunction with the Prospectus and any previous supplements.

Effective immediately, the following information replaces similar information found on page 150 in the fourth paragraph of the section titled Buying, Redeeming, and Exchanging Shares:

Generally, you can exchange shares of one Fund for the same class of shares of another Fund, except in the case of the Total Return Bond Fund and S&P 500 Index Fund. For individual retirement accounts described in Code Section 408, Class R4 shares of the Total Return Bond Fund and S&P 500 Index Fund may only be exchanged for Class A shares of another Fund and Class A shares of any other Fund may only be exchanged for Class R4 shares of these Funds. An exchange is treated as a sale of shares in one Fund and a purchase of shares in another Fund at the NAV next determined after the exchange request is received and accepted by the transfer agent, MML Advisers, a broker-dealer, or another intermediary authorized for this purpose. Exchange requests involving a purchase into any Fund (except the Strategic Bond Fund), however, will not be accepted if you have already made a purchase followed by a redemption involving the same Fund within the last 60 days. This restriction does not apply to rebalancing trades executed by any of the MassMutual RetireSMARTSM Funds. This restriction does not apply to exchanges made pursuant to certain asset allocation programs, systematic exchange programs, and dividend exchange programs. If you place an order to exchange shares of one Fund for another through a broker-dealer or other intermediary then, in order for your exchange to be effected based on the Funds’ next determined NAVs, the broker-dealer or other intermediary must receive your request before the close of regular trading on the NYSE, and the broker-dealer or other intermediary must subsequently communicate the request properly to the Funds.

Effective immediately, the following information replaces similar information found on page 152 in the first paragraph of the section titled Determining Net Asset Value:

The NAV of each Fund’s shares is determined once daily as of the close of regular trading on the NYSE, on each Business Day. A “Business Day” is every day the NYSE is open. If the NYSE is scheduled to close early, the Business Day will be considered to end as of the time of the NYSE’s scheduled close. A Fund will not treat an intraday disruption in NYSE trading or other event that causes an unscheduled closing of the NYSE as a close of business of the NYSE for these purposes and will instead fair value securities in accordance with procedures approved annually by the Trustees, and under the general oversight of the Trustees. The NYSE normally closes at 4:00 p.m. Eastern Time, but may close earlier on some days. The NYSE currently is not open for trading on New Year’s Day, Martin Luther King, Jr. Day, President’s Day, Good Friday, Memorial Day, Independence Day, Labor Day, Thanksgiving Day, and Christmas Day. Each Fund calculates the NAV of each of its classes of shares by dividing the total value of the assets attributable to that class, less the liabilities attributable to that class, by the number of shares of that class that are outstanding. On holidays and other days when the NYSE is closed, each Fund’s NAV generally is not calculated and the Funds do not anticipate accepting buy or sell orders. However, the value of each Fund’s assets may still be affected on such days to the extent that a Fund holds foreign securities that trade on days that foreign securities markets are open.

PLEASE RETAIN THIS SUPPLEMENT FOR FUTURE REFERENCE

B3001M-17-05

– 2 –

MASSMUTUAL SELECT FUNDS

Supplement dated May 8, 2017 to the

Statement of Additional Information dated February 1, 2017

This supplement provides new and additional information beyond that contained in the Statement of Additional Information (“SAI”) and any previous supplements. It should be retained and read in conjunction with the SAI and any previous supplements.

Effective March 1, 2017, Michael Eldredge resigned as a Vice President of the Trust.

Effective immediately, the following information replaces similar information found on page B-6 under the heading S&P 500 Index Fund, S&P Mid Cap Index Fund, Russell 2000 Small Cap Index Fund, and MSCI EAFE International Index Fund in the section titled Additional Investment Policies:

Tracking Error. There are several reasons why the performance of the S&P 500 Index Fund, S&P Mid Cap Index Fund, Russell 2000 Small Cap Index Fund, and MSCI EAFE International Index Fund may not track its respective index exactly. Unlike the indexes, the Funds incur administrative expenses and transaction costs in trading stocks. In addition, the composition of the indexes and each Fund’s portfolio may occasionally diverge. Furthermore, the timing and magnitude of cash inflows from investors buying shares could create balances of uninvested cash for the Funds. Conversely, the timing and magnitude of cash outflows to investors selling shares could require ready reserves of uninvested cash. Either situation would likely cause a Fund’s performance to deviate from the “fully invested” index. The Funds’ subadviser, NTI, expects that, under normal circumstances, the annual performance of each Fund, before fees and expenses, will track the performance of the index within a 0.95 correlation coefficient.

Effective immediately, the following information replaces similar information found on page B-10 under the heading Banking Relationships in the section titled Additional Investment Policies:

NTI and its affiliates, including its parent Northern Trust Corporation, deal, trade, and invest for their own account and for the accounts of their clients in the types of securities in which the S&P 500 Index Fund, S&P Mid Cap Index Fund, Russell 2000 Small Cap Index Fund, and MSCI EAFE International Index Fund may invest and may have deposit, loan, and commercial banking relationships with the issuers of securities purchased by the Funds.

The following information replaces similar information found on page B-62 under the heading Trustee Compensation in the section titled Management of the Trust:

During 2016, the Trust, on behalf of each Fund, paid each of its Trustees who was not an officer or employee of MassMutual a fee of $18,375 per quarter plus a fee of $2,940 per in-person meeting attended plus a fee of $2,940 for the annual Contract Committee meeting. The Chairperson of the Board was paid an additional 50% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. The Chairpersons of each of the Audit Committee and the Contract Committee were paid an additional 10% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. The Chairpersons of each of the Nominating Committee and the Governance Committee were paid an additional 5% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. Such Trustees who served on the Audit Committee, other than the Chairperson, were paid an additional 4% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. No additional fees were paid for attending any other committee meetings or any special telephonic meetings. In addition, the Trust reimbursed out-of-pocket business travel expenses to such Trustees. Trustees who were officers or employees of MassMutual received no fees from the Trust.

Effective immediately, the following information replaces similar information found on page B-117 in the section titled Valuation of Portfolio Securities:

The NAV of each Fund’s shares is determined once daily as of the close of regular trading on the NYSE, on each day the NYSE is open for trading (a “business day”). The NYSE normally closes at 4:00 p.m. Eastern Time,

– 3 –

but may close earlier on some days. If the NYSE is scheduled to close early, the business day will be considered to end as of the time of the NYSE’s scheduled close. A Fund will not treat an intraday disruption in NYSE trading or other event that causes an unscheduled closing of the NYSE as a close of business of the NYSE for these purposes and will instead fair value securities in accordance with procedures approved annually by the Board, and under the general oversight of the Board. The NYSE currently is not open for trading on New Year’s Day, Martin Luther King, Jr. Day, President’s Day, Good Friday, Memorial Day, Independence Day, Labor Day, Thanksgiving Day, and Christmas Day. Each Fund calculates the NAV of each of its classes of shares by dividing the total value of the assets attributable to that class, less the liabilities attributable to that class, by the number of shares of that class that are outstanding. On holidays and other days when the NYSE is closed, each Fund’s NAV generally is not calculated and the Funds do not anticipate accepting buy or sell orders. However, the value of each Fund’s assets may still be affected on such days to the extent that a Fund holds foreign securities that trade on days that foreign securities markets are open.

PLEASE RETAIN THIS SUPPLEMENT FOR FUTURE REFERENCE

SAI B3001M-17-03

– 4 –

MASSMUTUAL SELECT FUNDS

Supplement dated June 30, 2017 to the

Statement of Additional Information dated February 1, 2017

This supplement provides new and additional information beyond that contained in the Statement of Additional Information (“SAI”) and any previous supplements. It should be retained and read in conjunction with the SAI and any previous supplements.

Effective immediately, the following information replaces similar information found on page B-42 under the heading Other Income- Producing Securities in the section titled Additional Investment Policies:

Other types of income-producing securities the Funds may purchase, include, but are not limited to, the following:

| • | Variable and floating rate obligations. Variable and floating rate securities are debt instruments that provide for periodic adjustments in the interest rate paid on the security and, under certain limited circumstances, may have varying principal amounts. Variable rate securities provide for a specified periodic adjustment in the interest rate, while floating rate securities have interest rates that may change with change to the level of prevailing interest rates or the issuer’s credit quality. These types of securities are relatively long-term instruments that often carry demand features permitting the holder to demand payment of principal at any time or at specified intervals prior to maturity. There is a risk that the current interest rate on variable and floating securities may not accurately reflect current market interest rates or adequately compensate the holder for the current creditworthiness of the issuer. Due to their variable- or floating-rate features, these instruments will generally pay higher levels of income in a rising interest rate environment and lower levels of income as interest rates decline. For the same reason, the market value of a variable- or floating-rate instrument is generally expected to have less sensitivity to fluctuations in market interest rates than a fixed-rate instrument, although the value of a floating-rate instrument may nonetheless decline as interest rates rise and due to other factors, such as changes in credit quality. Some variable or floating rate securities are structured with liquidity features such as (1) put options or tender options that permit holders (sometimes subject to conditions) to demand payment of the unpaid principal balance plus accrued interest from the issuers or certain financial intermediaries or (2) auction rate features, remarketing provisions, or other maturity-shortening devices designed to enable the issuer to refinance or redeem outstanding debt securities (market-dependent liquidity features). The market-dependent liquidity features may not operate as intended as a result of the issuer’s declining creditworthiness, adverse market conditions, or other factors or the inability or unwillingness of a participating broker-dealer to make a secondary market for such securities. As a result, variable or floating rate securities that include market-dependent liquidity features may lose value and the holders of such securities may be required to retain them for an extended period of time or until maturity. |

In order to use these investments most effectively, a Fund’s investment adviser or subadviser must correctly assess probable movements in interest rates. This involves different skills than those used to select most portfolio securities. If the investment adviser or subadviser incorrectly forecasts such movements, a Fund could be adversely affected by the use of variable or floating rate obligations.

| • | Standby commitments. These instruments, which are similar to a put, give a Fund the option to obligate a broker, dealer, or bank to repurchase a security held by the Fund at a specified price. |

| • | Tender option bonds. Tender option bonds are relatively long-term bonds that are coupled with the agreement of a third party, such as a broker, dealer, or bank, to grant the holders of such securities the option to tender the securities to the institution at periodic intervals. |

| • | Inverse floaters. Inverse floaters have variable interest rates that typically move in the opposite direction from movements in prevailing interest rates, most often short-term rates. Accordingly, the |

– 5 –

value of inverse floaters, or other obligations or certificates structured to have similar features, generally moves in the opposite direction from interest rates. The value of an inverse floater can be considerably more volatile than the value of other debt instruments of comparable maturity and credit quality. Inverse floaters incorporate varying degrees of leverage. Generally, greater leverage results in greater price volatility for any given change in interest rates. Inverse floaters may be subject to legal or contractual restrictions on resale and therefore may be less liquid than other types of securities. Similar to variable and floating rate obligations, effective use of inverse floaters requires skills different from those needed to select most portfolio securities. If movements in interest rates are incorrectly anticipated, a Fund could lose money or the NAV of its shares could decline by the use of inverse floaters.

| • | Strip bonds. Strip bonds are debt securities that are stripped of their interest, usually by a financial intermediary, after the securities are issued. The market value of these securities generally fluctuates more in response to changes in interest rates than interest-paying securities of comparable maturities. |

Standby commitments, tender option bonds, and instruments with demand features are primarily used by the Funds for the purpose of increasing the liquidity of a Fund’s portfolio.

Effective June 6, 2017, the following information supplements the information found under the heading Interested Trustee (which will now be known herewith as Interested Trustees) found on page B-55 in the section titled Management of the Trust:

| Teresa A. Hassara | Trustee of the Trust | |

| 100 Bright Meadow Blvd. | ||

Enfield, CT 06082-1981 Age: 55 Trustee since 2017 | ||

| Trustee of 93 portfolios in fund complex |

Head of Workplace Solutions (since 2017), MassMutual; President of Institutional Retirement (2009-2016), TIAA-CREF; Trustee (since 2017), MML Series Investment Fund (open-end investment company); Trustee (since 2017), MML Series Investment Fund II (open-end investment company); Trustee (since 2017), MassMutual Premier Funds (open-end investment company).

Effective June 7, 2017, the information for Brian K. Haendiges on page B-56 under the heading Principal Officers in the section titled Management of the Trust is hereby deleted.

Effective June 7, 2017, the following information supplements the information found on pages B-55 – B-57 under the heading Principal Officers in the section titled Management of the Trust:

Joseph Fallon 100 Bright Meadow Blvd. | Vice President of the Trust | |

Enfield, CT 06082-1981 Age: 42 Officer since 2015 | ||

Officer of 93 portfolios in fund complex |

Investment Director (since 2014), MML Advisers; Investment Director (since 2006), MassMutual; Vice President (since 2017), Assistant Vice President (2015-2017), MassMutual Premier Funds (open-end investment company); Vice President (since 2017), Assistant Vice President (2015-2017), MML Series Investment Fund (open-end investment company); Vice President (since 2017), Assistant Vice President (2015-2017), MML Series Investment Fund II (open-end investment company).

– 6 –

| Jill Nareau Robert | Vice President and Assistant Secretary of the Trust | |

| 100 Bright Meadow Blvd. | ||

| Enfield, CT 06082-1981 | ||

| Age: 45 | ||

| Officer since 2008 | ||

| Officer of 93 portfolios in fund complex |

Assistant Vice President and Counsel (since 2009), MassMutual; Assistant Secretary (since 2015), MML Advisers; Vice President and Assistant Secretary (since 2017), Assistant Secretary (2008-2017), MassMutual Premier Funds (open-end investment company); Vice President and Assistant Secretary (since 2017), Assistant Secretary (2008-2017), MML Series Investment Fund (open-end investment company); Vice President and Assistant Secretary (since 2017), Assistant Secretary (2008-2017), MML Series Investment Fund II (open-end investment company).

Effective June 7, 2017, the following information replaces similar information for Tina Wilson found on page B-57 under the heading Principal Officers in the section titled Management of the Trust:

| Tina Wilson | Vice President of the Trust | |

| 100 Bright Meadow Blvd. | ||

| Enfield, CT 06082-1981 | ||

| Age: 46 | ||

| Officer since 2016 | ||

| Officer of 93 portfolios in fund complex |

Vice President and Head of Investments (since 2016), MML Advisers; Senior Vice President (since 2014), Vice President (2009-2014), MassMutual; Vice President (since 2016), MassMutual Premier Funds (open-end investment company); President (since 2017), Vice President (2016-2017), MML Series Investment Fund (open-end investment company); President (since 2017), Vice President (2016-2017), MML Series Investment Fund II (open-end investment company).

Effective June 6, 2017, the following information replaces similar information found on page B-57 in the section titled Management of the Trust:

Each Trustee of the Trust serves until the next meeting of shareholders called for the purpose of electing Trustees and until the election and qualification of his or her successor or until he or she dies, resigns, or is removed. Notwithstanding the foregoing, unless the Trustees determine that it is desirable and in the best interest of the Trust that an exception to the retirement policy of the Trust be made, a Trustee shall retire and cease to serve as a Trustee upon the conclusion of the calendar year in which such Trustee attains the age of seventy-five years, however, with the exception of Mr. Robert E. Joyal, an interested Trustee of the Trust shall no longer serve as a Trustee if or when they are no longer an employee of MassMutual or an affiliate.

Effective June 6, 2017, the following information supplements the information found on pages B-57 and B-58 under the heading Additional Information About the Trustees in the section titled Management of the Trust:

Teresa A. Hassara – As an executive of financial services companies with over 30 years of experience, Ms. Hassara’s deep industry expertise includes executive roles encompassing all aspects of relationship management and service delivery, as well as in strategy and planning, product and services management, customer loyalty analytics, and participant education and advisory solutions for clients in both the public and private sectors. Ms. Hassara has spent the majority of that time with three companies: Bankers Trust, Fidelity Investments, and, most recently, TIAA-CREF, where she led the company’s Institutional Retirement business serving more than 16,000 higher education, state government, and other nonprofit organizations. Ms. Hassara has FINRA Series 6, 24, 26, and 63 registrations and holds a BA from Vanderbilt University and an MBA from The Wharton School.

– 7 –

Effective June 6, 2017, the Nominating Committee and the Governance Committee have been combined into one committee, which is now called the Nominating and Governance Committee.

Effective June 6, 2017, the following information replaces similar information found on pages B-58 – B-60 under the heading Board Committees and Meetings in the section titled Management of the Trust:

Nominating and Governance Committee. The Trust has a Nominating and Governance Committee, consisting of each Trustee who is not an “interested person” of the Trust. There are no regular meetings of the Nominating and Governance Committee, but rather meetings are held as appropriate. During the fiscal year ended September 30, 2016, while they were both individual committees (formerly the Nominating Committee and the Governance Committee), the Nominating Committee and Governance Committee each met once. The Nominating and Governance Committee (a) identifies individuals qualified to become independent members of the Funds’ Board in the event that a position currently filled by an Independent Trustee is vacated or created; (b) evaluates the qualifications of Independent Trustee candidates; (c) nominates Independent Trustee nominees for election or appointment to the Board; (d) sets any standards necessary or qualifications for service on the Board; (e) recommends periodically to the full Board an Independent Trustee to serve as Chairperson; (f) evaluates at least annually the independence and overall performance of counsel to the Independent Trustees; (g) annually reviews the compensation of the Independent Trustees; and (h) oversees board governance issues including, but not limited to, (i) evaluating the board and committee structure and the performance of Trustees, (ii) considering and addressing any conflicts, (iii) considering the retirement policies of the Board, and (iv) considering and making recommendations to the Board at least annually concerning the Trust’s directors and officers liability insurance coverage.

The Nominating and Governance Committee will consider and evaluate nominee candidates properly submitted by shareholders of the Trust in the same manner as it considers and evaluates candidates recommended by other sources. The Nominating and Governance Committee may also consider any other facts and circumstances attendant to such shareholder submission as may be deemed appropriate by the Nominating and Governance Committee, including, without limitation, the value of the Funds’ securities owned by the shareholder and the length of time such shares have been held by the shareholder. A recommendation of a shareholder of the Trust must be submitted as described below to be considered properly submitted for purposes of the Nominating and Governance Committee’s consideration. The shareholders of the Trust must submit any such recommendation (a “Shareholder Recommendation”) in writing to the Trust’s Nominating and Governance Committee, to the attention of the Secretary, at the address of the principal executive offices of the Trust, which is 100 Bright Meadow Blvd., Enfield, CT 06082-1981. The Shareholder Recommendation must be delivered to or mailed and received at the principal executive offices of the Trust at least 60 calendar days before the date of the meeting at which the Nominating and Governance Committee is to select a nominee for Independent Trustee. The Shareholder Recommendation must include: (i) a statement in writing setting forth: (A) the name, age, date of birth, phone number, business address, residence address, nationality, and pertinent qualifications of the person recommended by the shareholder (the “Shareholder Candidate”), including an explanation of why the shareholder believes the Candidate will make a good Trustee; (B) the class or series and number of all shares of the Funds owned of record or beneficially by the Shareholder Candidate, as reported to such shareholder by the Shareholder Candidate; (C) any other information regarding the Shareholder Candidate called for with respect to director nominees by paragraphs (a), (d), (e), and (f) of Item 401 of Regulation S-K or paragraph (b) of Item 22 of Rule 14a-101 (Schedule 14A) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), adopted by the SEC (or the corresponding provisions of any regulation or rule subsequently adopted by the SEC or any successor agency applicable to the Funds); (D) any other information regarding the Shareholder Candidate that would be required to be disclosed if the Shareholder Candidate were a nominee in a proxy statement or other filing required to be made in connection with solicitation of proxies for election of trustees or directors pursuant to Section 14 of the Exchange Act and the rules and regulations promulgated thereunder; and (E) whether the recommending shareholder believes that the Shareholder Candidate is or will be an “interested person” (as defined in Section 2(a)(19) of the 1940 Act) of the Funds and, if not an “interested person,” information regarding the Shareholder Candidate that will be sufficient for the Funds to make such determination; (ii) the written and signed consent of the Shareholder Candidate to be named as a nominee, consenting to (1) the disclosure, as may be necessary or appropriate, of such Shareholder Candidate’s information submitted in

– 8 –

accordance with (i) above; and (2) service as a Trustee if elected; (iii) the recommending shareholder’s name as it appears on the Funds’ books, the number of all shares of each series of the Funds owned beneficially and of record by the recommending shareholder; (iv) a description of all arrangements or understandings between the recommending shareholder and the Shareholder Candidate and any other person or persons (including their names) pursuant to which the Shareholder Recommendation is being made by the recommending shareholder; and (v) such other information as the Nominating and Governance Committee may require the Shareholder Candidate to furnish as it may reasonably require or deem necessary to determine the eligibility of such Shareholder Candidate to serve as a Trustee or to satisfy applicable law.

Shareholders may send other communications to the Trustees by addressing such correspondence directly to the Secretary of the Trust, c/o Massachusetts Mutual Life Insurance Company, 100 Bright Meadow Blvd., Enfield, CT 06082-1981. When writing to the Board, shareholders should identify themselves, the fact that the communication is directed to the Board, the Fund they are writing about, and any relevant information regarding their Fund holdings. Except as provided below, the Secretary shall either (i) provide a copy of each shareholder communication to the Board at its next regularly scheduled meeting or (ii) if the Secretary determines that the communication requires more immediate attention, forward the communication to the Board promptly after receipt. The Secretary will also provide a copy of each shareholder communication to the Trust’s Chief Compliance Officer.

The Secretary may, in good faith, determine that a shareholder communication should not be provided to the Board because it does not reasonably relate to the Trust or its operations, management, activities, policies, service providers, Board, officers, shareholders, or other matters relating to an investment in the Funds or is otherwise ministerial in nature (such as a request for Fund literature, share data, or financial information). The Secretary will provide to the Board on a quarterly basis a summary of the shareholder communications not provided to the Board by virtue of this paragraph.

Effective June 6, 2017, the following information replaces similar information found on page B-62 under the heading Trustee Compensation in the section titled Management of the Trust:

During 2017, the Trust, on behalf of each Fund, pays each of its Trustees who is not an officer or employee of MassMutual a fee of $20,000 per quarter plus a fee of $3,000 per in-person meeting attended plus a fee of $3,000 for the annual Contract Committee meeting. The Chairperson of the Board is paid an additional 50% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. The Chairpersons of each of the Audit Committee and the Contract Committee are paid an additional 10% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. The Chairperson of the Nominating and Governance Committee is paid an additional 5% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. Such Trustees who serve on the Audit Committee, other than the Chairperson, are paid an additional 4% of the quarterly fee, the in-person meeting fee, and the Contract Committee meeting fee. No additional fees are paid for attending any other committee meetings or any special telephonic meetings. In addition, the Trust reimburses out-of-pocket business travel expenses to such Trustees. Trustees who are officers or employees of MassMutual receive no fees from the Trust.

Effective immediately, the information related to Charles Ko found on page B-315 under the heading Other Accounts Managed in the section titled Appendix C—Additional Portfolio Manager Information is hereby removed.

Effective immediately, the following information supplements similar information for Invesco Advisers, Inc. related to the MassMutual Select Small Company Value Fund found on page B-315 under the headings Other Accounts Managed and Ownership of Securities in the section titled Appendix C—Additional Portfolio Manager Information:

The portfolio managers of the Small Company Value Fund are Glen Murphy, Donna Chapman Wilson, Michael Abata, and Kenneth Masse.

– 9 –

Other Accounts Managed:

| Number of Accounts Managed* | Total Assets* | Number of Accounts Managed for which Advisory Fee is Performance- Based* | Total Assets* | |||||||||||||

Kenneth Masse | ||||||||||||||||

Registered investment companies** | 2 | | $94.3 million | | 0 | $ | 0 | |||||||||

Other pooled investment vehicles | 3 | | $124.0 million | | 0 | $ | 0 | |||||||||

Other accounts | 0 | $0 | 0 | $ | 0 | |||||||||||

| * | The information provided is as of April 30, 2017. |

| ** | Does not include the Small Company Value Fund. |

Ownership of Securities:

As of April 30, 2017, the portfolio manager did not own any shares of the Small Company Value Fund.

PLEASE RETAIN THIS SUPPLEMENT FOR FUTURE REFERENCE

SAI B3001M-17-04

– 10 –

MASSMUTUAL SELECT FUNDS

Select Diversified Value Fund

Supplement dated August 10, 2017 to the

Prospectus dated February 1, 2017 and the

Summary Prospectus dated February 1, 2017

This supplement provides new and additional information beyond that contained in the Prospectus and Summary Prospectus, and any previous supplements. It should be retained and read in conjunction with the Prospectus and Summary Prospectus, and any previous supplements.

Effective immediately, the information related to Adam C. Liebhoff for the Select Diversified Value Fund found under the heading Portfolio Managers in the section titled Management (Page 27 of the Prospectus), is hereby removed.

Effective immediately, the information related to Adam C. Liebhoff of Loomis, Sayles & Company, L.P. found under the heading Subadvisers and Portfolio Managers in the section titled Management of the Funds (page 137 of the Prospectus), is hereby removed.

PLEASE RETAIN THIS SUPPLEMENT FOR FUTURE REFERENCE

B3001M-17-08

DV-17-01

– 11 –

MASSMUTUAL SELECT FUNDS

Supplement dated August 10, 2017 to the

Statement of Additional Information dated February 1, 2017

This supplement provides new and additional information beyond that contained in the Statement of Additional Information (“SAI”) and any previous supplements. It should be retained and read in conjunction with the SAI and any previous supplements.

Effective immediately, the information related to Adam C. Liebhoff found on page B-324 under the heading Other Accounts Managed in the section titled Appendix C – Additional Portfolio Manager Information is hereby removed.

PLEASE RETAIN THIS SUPPLEMENT FOR FUTURE REFERENCE

SAI B3001M-17-06

– 12 –

MASSMUTUAL SELECT FUNDS

Supplement dated September 22, 2017 to the

Prospectus dated February 1, 2017

This supplement provides new and additional information beyond that contained in the Prospectus and any previous supplements. It should be retained and read in conjunction with the Prospectus and any previous supplements.

The following information pertains to the Large Cap Value Fund:

The Board of Trustees of the MassMutual Select Funds has approved the reorganization of the MassMutual Select Large Cap Value Fund (the “Fund”) into the MassMutual Select Diversified Value Fund. The reorganization is subject to approval by Massachusetts Mutual Life Insurance Company (“MassMutual”), in its capacity as the majority shareholder of the Fund. MassMutual anticipates approving the reorganization by written consent in January 2018. No assurance can be given that the reorganization will occur.

Under the terms of the proposed Agreement and Plan of Reorganization, the Fund’s assets and liabilities would be transferred to the MassMutual Select Diversified Value Fund in return for shares of the MassMutual Select Diversified Value Fund. Those shares would be distributed pro rata to shareholders of the Fund in exchange for their Fund shares. Shareholders of the Fund would thus become shareholders of the MassMutual Select Diversified Value Fund and would receive shares of the MassMutual Select Diversified Value Fund with a value equal to their shares of the Fund at the time of the reorganization. The reorganization is expected to be a tax-free event for federal income tax purposes.

The Fund seeks both capital growth and income as its investment objective, while the MassMutual Select Diversified Value Fund seeks as its objective to achieve long-term growth of capital and income by investing primarily in a diversified portfolio of equity securities of larger, well-established companies.

Descriptions of the MassMutual Select Diversified Value Fund and the terms of the reorganization will be contained in a combined prospectus/information statement, which is expected to be mailed to shareholders of the Fund in December 2017.

The foregoing is not an offer to sell, nor a solicitation of an offer to buy, shares of the MassMutual Select Diversified Value Fund, nor is it a solicitation of any proxy. For more information regarding the MassMutual Select Diversified Value Fund, or to receive a free copy of a prospectus/information statement relating to the reorganization (and containing important information about fees, expenses, and risk considerations) once a registration statement relating to the reorganization has been filed with the Securities and Exchange Commission and becomes effective, please call 1-888-309-3539. The prospectus/information statement will also be available for free on the Securities and Exchange Commission’s Web site (http://www.sec.gov). Please read the prospectus/information statement carefully before making any investment decisions.

Effective immediately, the section entitled “Purchase and Sale of Fund Shares” found on page 36 is restated in its entirety as follows:

PURCHASE AND SALE OF FUND SHARES

Shares of the Fund are generally available to retirement plans, other institutional investors, and individual retirement accounts. Fund shares are redeemable on any business day by written request, telephone, or internet (available to certain customers).

The Board of Trustees of the MassMutual Select Funds has approved the reorganization of the Fund into the MassMutual Select Diversified Value Fund. The reorganization is subject to approval by Massachusetts Mutual Life Insurance Company, in its capacity as the majority shareholder of the Fund, by written consent expected to be executed in January 2018. No assurance can be given that the reorganization will occur.

– 13 –

Descriptions of the MassMutual Select Diversified Value Fund and the terms of the reorganization will be contained in a combined prospectus/information statement, which is expected to be mailed to shareholders of the Fund in December 2017.

Effective September 21, 2017, T. Rowe Price Associates, Inc. (“T. Rowe Price”) replaced Loomis, Sayles & Company, L.P. (“Loomis Sayles”) as a co-subadviser of the Diversified Value Fund.

Effective September 21, 2017, the following information replaces similar information found on pages 24-25 for the Diversified Value Fund under the heading Principal Investment Strategies in the section titled Investments, Risks, and Performance:

The Fund invests primarily in stocks of companies that the subadvisers believe are undervalued in the marketplace. While the Fund does not limit its investments to issuers in a particular capitalization range, the subadvisers currently focus on securities of larger size companies. The Fund normally invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in stocks, securities convertible into stocks, and other securities, such as warrants and stock rights, whose value is based on stock prices. The Fund typically invests most of its assets in securities of U.S. companies, but may invest up to 25% of its total assets in foreign securities and American Depositary Receipts (“ADRs”), including emerging market securities. The Fund is managed by two subadvisers, T. Rowe Price Associates, Inc. (“T. Rowe Price”) and Brandywine Global Investment Management, LLC (“Brandywine Global”), each being responsible for a portion of the portfolio, but not necessarily equally weighted. The Fund may hold a portion of its assets in cash or cash equivalents.

Brandywine Global invests in securities that meet its value criteria, primarily, price-to-earnings, price-to-book, price momentum, and share change and quality, based on both quantitative and fundamental analysis. Brandywine Global expects to hold approximately 150-250 stocks under normal market conditions.

Brandywine Global invests in securities of companies that meet its value criteria based on both quantitative and fundamental analysis. Brandywine Global’s investment process begins with a valuation screen that identifies large cap stocks with favorable financial ratios. A quantitative deselection process is then applied to eliminate equities that have poor price momentum or high share issuance. Finally Brandywine Global performs a thorough fundamental analysis which seeks to identify and eliminate (de-select) companies with deteriorating fundamentals, anticipated earnings declines, or material write-offs. Brandywine Global may also consider additional factors in its selection process.

Brandywine Global typically sells a security of a company when Brandywine Global believes it is no longer a large capitalization value company, if the company’s fundamentals deteriorate, when an investment opportunity arises that Brandywine Global believes is more compelling, or in order to realize gains or limit potential losses. However, Brandywine Global may retain securities of companies that no longer meet its initial purchase criteria.

T. Rowe Price typically employs a “value” approach in selecting investments, using internal research to identify companies that appear to be undervalued by various measures and may be temporarily out of favor but have good prospects for capital appreciation and dividend growth. T. Rowe Price generally looks for companies in the aggregate with one or more of the following: an established operating history; above-average dividend yield and low price/earnings ratio relative to the S&P 500® Index; a sound balance sheet and other positive financial characteristics; and low stock price relative to T. Rowe Price’s view of the company’s underlying value as measured by assets, cash flow, or business franchises. T. Rowe Price generally seeks investments in large-capitalization companies and the yield of the portion of the Fund managed by T. Rowe Price is expected to normally exceed the yield of the S&P 500 Index. T. Rowe Price may sell securities for a variety of reasons, such as to secure gains, limit losses, or redeploy assets into more promising opportunities.

In pursuing its investment objective, each of Brandywine Global and T. Rowe Price has the discretion to purchase some securities that do not meet its normal investment criteria, as described above, when it believes there is an opportunity for substantial appreciation (such as, for example, Brandywine Global or T. Rowe Price believes a security could increase in value as a result of a change in management, an extraordinary corporate event, a new product introduction or innovation, or a favorable competitive development).

– 14 –

Effective September 21, 2017, the REIT Risk found on page 26 is hereby deleted for the Diversified Value Fund under the heading Principal Risks in the section titled Investments, Risks, and Performance.

Effective September 21, 2017, the following information replaces the information found on page 27 for the Diversified Value Fund under the heading Portfolio Managers in the section titled Management:

Subadvisers: Brandywine Global Investment Management, LLC (“Brandywine Global”)

T. Rowe Price Associates, Inc. (“T. Rowe Price”)

Portfolio Managers:

Joseph J. Kirby is a Portfolio Manager at Brandywine Global. He has managed the Fund since January 2010.

Henry F. Otto is a Managing Director and Portfolio Manager at Brandywine Global. He has managed the Fund since January 2010.

Steven M. Tonkovich is a Managing Director and Portfolio Manager at Brandywine Global. He has managed the Fund since January 2010.

John D. Linehan, CFA, is a Vice President and Portfolio Manager at T. Rowe Price. He has managed the Fund since September 2017.

Effective September 21, 2017, the following information supplements the information for Loomis Sayles found under the heading Subadvisers and Portfolio Managers on page 137 in the section titled Management of the Funds:

Effective September 21, 2017, T. Rowe Price replaced Loomis Sayles as a co-subadviser of the Diversified Value Fund, therefore all references to Loomis Sayles as subadviser for the Diversified Value Fund are removed.

Effective September 21, 2017, the following information replaces the first sentence found on page 140 for T. Rowe Price under the heading Subadvisers and Portfolio Managers in the section titled Management of the Funds:

T. Rowe Price Associates, Inc. (“T. Rowe Price”), located at 100 East Pratt Street, Baltimore, Maryland 21202, manages a portion of the portfolio of the Diversified Value Fund, Equity Opportunities Fund, Blue Chip Growth Fund, Mid Cap Growth Fund, and Small Company Value Fund.

Effective September 21, 2017, the following information supplements the information found on pages 140-141 for T. Rowe Price under the heading Subadvisers and Portfolio Managers in the section titled Management of the Funds:

T. Rowe Price replaced Loomis Sayles as a co-subadviser of the Diversified Value Fund on September 21, 2017.

Effective September 21, 2017, the following information replaces similar information for John D. Linehan, CFA found on pages 140-141 for T. Rowe Price under the heading Subadvisers and Portfolio Managers in the section titled Management of the Funds:

John D. Linehan, CFA

is the portfolio manager of a portion of the Diversified Value Fund and Equity Opportunities Fund. Mr. Linehan, investment advisory committee chairman, has day-to-day responsibility for managing the portfolio and works with the committee in developing and executing the portfolio’s investment program. He is a Vice President and Portfolio Manager for T. Rowe Price. Mr. Linehan joined T. Rowe Price in 1998 and has 25 years of investment experience. During the past five years, he has served as a portfolio manager and the head of U.S. Equity for T. Rowe Price.

PLEASE RETAIN THIS SUPPLEMENT FOR FUTURE REFERENCE

B3001M-17-09

– 15 –

MASSMUTUAL SELECT FUNDS

Supplement dated September 22, 2017 to the

Statement of Additional Information dated February 1, 2017

This supplement provides new and additional information beyond that contained in the Statement of Additional Information (“SAI”) and any previous supplements. It should be retained and read in conjunction with the SAI and any previous supplements.

Effective September 21, 2017, T. Rowe Price Associates, Inc. (“T. Rowe Price”) replaced Loomis, Sayles & Company, L.P. (“Loomis Sayles”) as a co-subadviser of the Diversified Value Fund.

Effective September 21, 2017, the following information replaces similar information for the Diversified Value Fund found on page B-3 in the section titled General Information:

The subadvisers for the Diversified Value Fund are Brandywine Global Investment Management, LLC (“Brandywine Global”), located at 2929 Arch Street, 8th Floor, Philadelphia, Pennsylvania 19104, and T. Rowe Price Associates, Inc. (“T. Rowe Price”), located at 100 East Pratt Street, Baltimore, Maryland 21202.

Effective September 21, 2017, the following information replaces the first sentence of the third paragraph on page B-43 in the section titled Additional Investment Policies under the heading Other Investment Companies:

T. Rowe Price may invest the assets of the Diversified Value Fund, Equity Opportunities Fund, Blue Chip Growth Fund, Mid Cap Growth Fund, or Small Company Value Fund, respectively, into money market funds managed pursuant to applicable SEC exemptive orders.

Effective September 21, 2017, the following information replaces similar information found on page B-52 in the section titled Investment Restrictions of the Funds under the heading Non-Fundamental Investment Restrictions of the Funds:

(4) to the extent that shares of the Fund are purchased or otherwise acquired by other series of the Trust, acquire any securities of registered open-end investment companies or registered unit investment trusts in reliance on Section 12(d)(1)(F) or Section 12(d)(1)(G) of the 1940 Act, except this restriction shall not prohibit the investment by the Diversified Value Fund, Equity Opportunities Fund, Blue Chip Growth Fund, Mid Cap Growth Fund, or the Small Company Value Fund in money market funds managed by T. Rowe Price pursuant to an exemptive order.

Effective September 21, 2017, the following information replaces the second paragraph under the heading Unaffiliated Subadvisers found on page B-97 in the section titled Investment Advisory and Other Service Agreements:

Brandywine Global and T. Rowe Price both act as subadvisers for the Diversified Value Fund. Brandywine Global is a wholly-owned, independently operated subsidiary of Legg Mason, Inc., and is headquartered in Philadelphia with an office in San Francisco. Brandywine Global also operates two affiliated companies with offices in Singapore and London. T. Rowe Price is a wholly-owned subsidiary of T. Rowe Price Group, Inc., a publicly traded financial services holding company.

Loomis Sayles and T. Rowe Price both act as subadvisers for the Blue Chip Growth Fund. Loomis Sayles is an indirect subsidiary of Natixis Global Asset Management, L.P. which owns, in addition to Loomis Sayles, a number of other asset management and distribution and service entities. Natixis Global Asset Management, L.P. is part of Natixis Global Asset Management, an international asset management group based in Paris, France, that is in turn owned by Natixis, a French investment banking and financial services firm. Natixis is principally owned by BPCE, France’s second largest banking group. The group includes two autonomous and complimentary retail banking networks consisting of the Caisse d’Epargne regional savings banks and the

– 16 –

Banque Populaire regional cooperative banks. Loomis Sayles also provides subadvisory services for the MML Equity Fund, a series of MML Series Investment Fund II, a registered, open-end investment company for which MML Advisers serves as investment adviser.

Effective September 21, 2017, the information for Loomis Sayles related to the Diversified Value Fund found on page B-97 in the section titled Unaffiliated Subadvisers is hereby removed.

Effective September 21, 2017, the information under Loomis Sayles related to the Diversified Value Fund found on page B-324 in the section titled Appendix C—Additional Portfolio Manager Information is hereby removed.

Effective September 21, 2017, the following information supplements similar information for T. Rowe Price related to the Diversified Value Fund found on page B-341 in the section titled Appendix C—Additional Portfolio Manager Information:

The portfolio manager of the Diversified Value Fund is John D. Linehan.

Other Accounts Managed:

| Number of Accounts Managed* | Total Assets* | Number of Accounts Managed for which Advisory Fee is Performance- Based* | Total Assets* | |||||||||||||

John D. Linehan | ||||||||||||||||

Registered investment companies** | 9 | $ | 42,560,659,764 | 0 | $ | 0 | ||||||||||

Other pooled investment vehicles | 6 | $ | 11,543,013,307 | 0 | $ | 0 | ||||||||||

Other accounts | 41 | $ | 6,271,814,922 | 0 | $ | 0 | ||||||||||

| * | The information provided is as of July 31, 2017. |

| ** | Does not include the Diversified Value Fund. |

Ownership of Securities:

As of July 31, 2017, the portfolio manager did not own any shares of the Diversified Value Fund.

PLEASE RETAIN THIS SUPPLEMENT FOR FUTURE REFERENCE

SAI B3001M-17-07

– 17 –

| Table Of Contents | Page | |||

About the Funds | ||||

| 20 | ||||

| 26 | ||||

| 32 | ||||

| 40 | ||||

| 44 | ||||

| 48 | ||||

| 54 | ||||

| 58 | ||||

| 62 | ||||

| 66 | ||||

| 72 | ||||

| 76 | ||||

| 82 | ||||

| 86 | ||||

| 92 | ||||

| 96 | ||||

| 100 | ||||

| 104 | ||||

| 110 | ||||

| 116 | ||||

| 122 | ||||

Additional Information Regarding Investment Objectives and Principal Investment Strategies | 127 | |||

| 130 | ||||

| 130 | ||||

Management of the Funds | ||||

| 146 | ||||

| 146 | ||||

About the Classes of Shares – I, R5, Service, Administrative, A, R4, and R3 Shares | 160 | |||

| 161 | ||||

| 163 | ||||

Distribution Plans, Shareholder Servicing, and Payments to Intermediaries | 164 | |||

| 166 | ||||

| 167 | ||||

| 167 | ||||

| 168 | ||||

| 170 | ||||

| 173 | ||||

| 195 | ||||

– 18 –

[THIS PAGE INTENTIONALLY LEFT BLANK]

MassMutual Select Total Return Bond Fund

INVESTMENT OBJECTIVE

This Fund seeks maximum total return, consistent with preservation of capital and prudent investment management.

FEES AND EXPENSES OF THE FUND

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. For Class A shares, you may qualify for sales charge discounts if you invest, or agree to invest in the future, at least $25,000 in MassMutual funds. More information about these and other discounts is available in the section titled Sales Charges by Class beginning on page 145 of the Fund’s Prospectus or from your financial professional.

Shareholder Fees (fees paid directly from your investment)

| Class I | Class R5 | Service Class | Administrative Class | Class A | Class R4 | Class R3 | ||||||||

Maximum Sales Charge (Load) Imposed on Purchases (as a % of offering price) | None | None | None | None | 4.75% | None | None | |||||||

Maximum Deferred Sales Charge (Load) (as a % of the lower of the original offering price or redemption proceeds) | None | None | None | None | None | None | None |

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

| Class I | Class R5 | Service Class | Administrative Class | Class A | Class R4 | Class R3 | ||||||||

Management | .30% | .30% | .30% | .30% | .30% | .30% | .30% | |||||||

Distribution and Service (Rule 12b-1) Fees | None | None | None | None | .25% | .25% | .50% | |||||||

Other Expenses | .04% | .14% | .24% | .34% | .34% | .24% | .24% | |||||||

Total Annual Fund Operating Expenses | .34% | .44% | .54% | .64% | .89% | .79% | 1.04% |

| (1) | Management Fees have been restated to reflect current fees. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. It assumes that you invest $10,000 in each share class of the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. For Class A shares, the example includes the initial sales charge. The example also assumes that your investment earns a 5% return each year and that the Fund’s operating expenses are exactly as described in the preceding table. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

Class I | $ | 35 | $ | 109 | $ | 191 | $ | 431 | ||||||||

Class R5 | $ | 45 | $ | 141 | $ | 246 | $ | 555 | ||||||||

Service Class | $ | 55 | $ | 173 | $ | 302 | $ | 677 | ||||||||

Administrative Class | $ | 65 | $ | 205 | $ | 357 | $ | 798 | ||||||||

Class A | $ | 562 | $ | 745 | $ | 945 | $ | 1,519 | ||||||||

Class R4 | $ | 81 | $ | 252 | $ | 439 | $ | 978 | ||||||||

Class R3 | $ | 106 | $ | 331 | $ | 574 | $ | 1,271 | ||||||||

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 264% of the average value of its portfolio.

INVESTMENTS, RISKS, AND PERFORMANCE

Principal Investment Strategies

Under normal circumstances, the Fund invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in a diversified portfolio of investment grade fixed income securities (rated Baa3 or higher by Moody’s, BBB- or higher by Standard & Poor’s, BBB- or higher by Fitch, or A-2 by S&P, P-2 by Moody’s, or F-2 by Fitch for short-term debt obligations, or, if unrated, determined

– 20 –

by the Fund’s subadviser, Metropolitan West Asset Management, LLC (“MetWest”), to be of comparable quality). These typically include bonds, notes, collateralized bond obligations, collateralized debt obligations, mortgage-related and asset-backed securities, municipal securities, private placements, and securities subject to legal restrictions on resale pursuant to Rule 144A. These investments may have interest rates that are fixed, variable, or floating. The Fund invests in securities of varying maturities issued by domestic and foreign corporations and governments (and their agencies and instrumentalities). MetWest focuses the Fund’s portfolio holdings in areas of the bond market (based on quality, sector, coupon, or maturity) that the subadviser believes to be relatively undervalued.

The Fund may invest up to 20% of its net assets in below investment grade debt securities (“junk” or “high yield” bonds), including securities in default and bank loans. In the event that a security is downgraded after its purchase by the Fund, the Fund may continue to hold the security if MetWest considers doing so would be consistent with the Fund’s investment objective.

The Fund may invest up to 25% of its total assets in foreign securities that are denominated in U.S. dollars. The Fund may also invest up to 15% of its total assets in foreign securities that are not denominated in U.S. dollars and up to 10% of its total assets in emerging market foreign securities.

The Fund may but will not necessarily engage in foreign currency forward transactions to take long or short positions in foreign currencies in order to seek to enhance the Fund’s investment return or to seek to hedge or to attempt to protect against adverse changes in currency exchange rates. In pursuing its investment objective, the Fund may (but is not obligated to) use a wide variety of exchange-traded and over-the-counter derivatives, including options, futures contracts, and swap contracts for hedging or investment purposes as a substitute for investing directly in securities or to adjust various portfolio characteristics, including the duration (interest rate volatility) of the Fund’s portfolio. Use of derivatives by the Fund may create investment leverage.

The Fund may purchase and sell securities on a when-issued, delayed delivery, or forward commitment basis. The Fund may normally short sell up to 25% of the value of its total assets for hedging or investment purposes.

The Fund may also invest in money market securities, including commercial paper. The Fund may enter into repurchase agreement transactions. The Fund may hold a portion of its assets in cash or cash equivalents. The Fund may enter into dollar roll or reverse repurchase agreement transactions.

MetWest intends for the Fund’s portfolio duration to be between two to eight years. The dollar-weighted average maturity of the Fund’s portfolio is expected to range from two to fifteen years. Duration measures the price sensitivity of a bond to changes in interest rates. Duration is the dollar weighted average time to maturity of a bond utilizing the present value of all future cash flows.

MetWest employs a value-oriented fixed income management philosophy with a goal of consistently outperforming the portfolio benchmark while maintaining volatility similar to the benchmark. The investment process is predicated on a long-term economic outlook, which is determined by the investment team on a quarterly basis and is reviewed constantly. Investments are characterized by diversification among the sectors of the fixed income marketplace. The investment management team seeks to achieve the desired outperformance through the measured and disciplined application of five fixed income management strategies which include duration management, yield curve positioning, sector allocation, security selection, and opportunistic execution.

The first three strategies are top-down in orientation and start with a decision of where within the plus-or-minus one year range around the benchmark the duration should be established. Then comes a determination of how the overall average duration is to be effected – with a concentration of intermediate maturity issues or a combination of long- and short-term issues. The relative value decision regarding where to overweight/underweight sectors, including governments, agencies, corporates, mortgages, or asset-backed securities, is dependent on the current market environment. Bottom-up security selection involves the day-to-day fundamental analysis of available bond market opportunities, while execution is characterized by the aggressive and informed negotiation of the prices at which transactions take place.

The Fund expects that it will engage in active and frequent trading and so will typically have a relatively high portfolio turnover rate.

– 21 –

Principal Risks

The following are the Principal Risks of the Fund. The value of your investment in the Fund could go down as well as up. You can lose money by investing in the Fund.

Bank Loans Risk Many of the risks associated with bank loans are similar to the risks of investing in below investment grade debt securities. Changes in the financial condition of the borrower or economic conditions or other circumstances may reduce the capacity of the borrower to make principal and interest payments on such instruments and may lead to defaults. Senior secured bank loans are typically supported by collateral; however the value of the collateral may be insufficient to cover the amount owed to the Fund, or the Fund may be prevented or delayed from realizing on the collateral. Some loans may be unsecured; unsecured loans generally present a greater risk of loss to the Fund if the issuer defaults. If the Fund relies on a third party to administer a loan, the Fund is subject to the risk that the third party will fail to perform its obligations. In addition, if the Fund holds only a participation interest in a loan made by a third party, the Fund’s receipt of payments on the loan will depend on the third party’s willingness and ability to make those payments to the Fund. The settlement time for certain loans is longer than the settlement time for many other types of investments, and the Fund may not receive the payment for a loan sold by it until well after the sale; that cash would be unavailable for payment of redemption proceeds or for reinvestment. Interests in other bank loans may not be readily marketable and may be subject to restrictions on resale. In some cases, negotiations involved in disposing of indebtedness may require weeks to complete. Consequently, some indebtedness may be difficult or impossible to dispose of readily at what the Fund believes to be a fair price.

Below Investment Grade Debt Securities Risk Below investment grade debt securities, commonly known as “junk” or “high yield” bonds, have speculative characteristics and involve greater volatility of price and yield, greater risk of loss of principal and interest, and generally reflect a greater possibility of an adverse change in financial condition that could affect an issuer’s ability to honor its obligations.

Cash Position Risk If the Fund holds a significant portion of its assets in cash or cash equivalents, its investment returns may be adversely affected and the Fund may not achieve its investment objective.

Credit Risk Credit risk is the risk that an issuer, guarantor, or liquidity provider of a fixed-income

security held by the Fund may be unable or unwilling, or may be perceived (whether by market participants, ratings agencies, pricing services or otherwise) as unable or unwilling, to make timely principal and/or interest payments, or to otherwise honor its obligations. The Fund may also be exposed to the credit risk of its counterparty to repurchase agreements, reverse repurchase agreements, swap transactions, and other derivatives transactions, and to the counterparty’s ability or willingness to perform in accordance with the terms of the transaction. The value of such transactions to the Fund will depend on the willingness and ability of the counterparty to perform its obligations, including among other things the obligation to return collateral or margin to the Fund.

Defaulted and Distressed Securities Risk Because the issuer of such securities is in default and is likely to be in distressed financial condition, repayment of defaulted securities and obligations of distressed issuers (including insolvent issuers or issuers in payment or covenant default, in workout or restructuring, or in bankruptcy or insolvency proceedings) is uncertain.

Derivatives Risk Derivatives can be highly volatile and involve risks different from, and potentially greater than, direct investments, including risks of imperfect correlation between the value of derivatives and underlying assets, counterparty default, potential losses that partially or completely offset gains, and illiquidity. Derivatives can create investment leverage. Losses from derivatives can be substantially greater than the derivatives’ original cost and can sometimes be unlimited. If the value of a derivative does not correlate well with the particular market or asset class the derivative is designed to provide exposure to, the derivative may not have the effect anticipated. Derivatives can also reduce the opportunity for gains or result in losses by offsetting positive returns in other investments. Many derivatives are traded in the over-the-counter market and not on exchanges.

Dollar Roll and Reverse Repurchase Agreement Transaction Risk These transactions generally create leverage and subject the Fund to the credit risk of the counterparty.

Fixed Income Securities Risk The values of fixed income securities typically will decline during periods of rising interest rates, and can also decline in response to changes in the financial condition of the issuer, borrower, counterparty, or underlying collateral assets, or changes in market, economic, industry, political, and regulatory conditions

– 22 –

affecting a particular type of security or issuer or fixed income securities generally. Certain events, such as market or economic developments, regulatory or government actions, natural disasters, terrorist attacks, war, and other geopolitical events can have a dramatic adverse effect on the debt market and the overall liquidity of the market for fixed income securities. During those periods, the Fund may experience high levels of shareholder redemptions, and may have to sell securities at times when the Fund would otherwise not do so, and potentially at unfavorable prices. Certain securities may be difficult to value during such periods. Fixed income securities are subject to interest rate risk (the risk that the value of a fixed income security will fall when interest rates rise), extension risk (the risk that the average life of a security will be extended through a slowing of principal payments), prepayment risk (the risk that a security will be prepaid and the Fund will be required to reinvest at a less favorable rate), and credit risk. These risks may be heightened due to the current historically low interest rate environment.

Foreign Investment Risk; Emerging Markets Risk; Currency Risk Investments in securities of non-U.S. issuers (including depositary receipts) entail risks not typically associated with investing in securities of U.S. issuers. Similar risks may apply to securities traded on a U.S. securities exchange that are issued by companies with significant exposure to non-U.S. countries. In certain countries, legal remedies available to investors may be more limited than those available with regard to U.S. investments. Because non-U.S. securities are normally denominated and traded in currencies other than the U.S. dollar, the value of the Fund’s assets may be affected favorably or unfavorably by currency exchange rates, exchange control regulations, and restrictions or prohibitions on the repatriation of non-U.S. currencies. Income and gains with respect to investments in certain countries may be subject to withholding and other taxes. There may be less information publicly available about a non-U.S. company than about a U.S. company, and many non-U.S. companies are not subject to accounting, auditing, and financial reporting standards, regulatory framework and practices comparable to those in the U.S. Foreign investments may be subject to the risks of seizure by a foreign government, imposition of restrictions on the exchange or export of foreign currency, other economic sanctions, and tax increases. The securities of some non-U.S. companies, especially those in emerging markets, are less liquid and at times more volatile than securities of

comparable U.S. companies. Emerging markets securities are subject to greater risks than securities issued in developed foreign markets, including less liquidity, greater price volatility, higher relative rates of inflation, greater political, economic, and social instability, greater custody and operational risks, and greater volatility in currency exchange rates. Non-U.S. transaction costs, such as brokerage commissions and custody costs may be higher than in the United States. In addition, there may be a possibility of nationalization or expropriation of assets, imposition of currency exchange controls, confiscatory taxation, political or financial instability, and diplomatic developments that could adversely affect the values of the Fund’s investments in certain non-U.S. countries.

Frequent Trading/Portfolio Turnover Risk Portfolio turnover generally involves some expense to the Fund and may result in the realization of taxable capital gains (including short-term gains). The trading costs and tax effects associated with portfolio turnover may adversely affect the Fund’s performance.

Inflation Risk The value of assets or income from the Fund’s investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the Fund’s distributions.

Leveraging Risk Instruments and transactions, including derivatives, dollar rolls, and reverse repurchase agreement transactions, that create leverage may cause the value of an investment in the Fund to be more volatile, could result in larger losses than if they were not used, and tend to compound the effects of other risks.

Liquidity Risk Certain securities may be difficult (or impossible) to sell or positions difficult to close out at a desirable time and price, and the Fund may be required to hold an illiquid investment that is declining in value, or it may be required to sell certain illiquid investments at a price or time that is not advantageous in order to meet redemptions or other cash needs. Some securities may be subject to restrictions on resale. There can be no assurance that there will be a liquid market for instruments held by the Fund at any time.

Management Risk The Fund relies on the manager’s investment analysis and its selection of investments to achieve its investment objective. There can be no assurance that the Fund will achieve the intended results and the Fund may incur significant losses.

– 23 –

Market Risk The value of the Fund’s portfolio securities may decline, at times sharply and unpredictably, as a result of unfavorable market-induced changes affecting particular industries, sectors, or issuers. Stock markets can decline significantly in response to issuer, market, economic, industry, political, regulatory, geopolitical and other conditions, as well as investor perceptions of these conditions. The Fund is subject to risks affecting issuers, such as management performance, financial leverage, industry problems, and reduced demand for goods or services.

Mortgage- and Asset-Backed Securities Risk Investments in mortgage- and asset-backed securities subject the Fund to credit risk, interest rate risk, extension risk, and prepayment risk, among other risks. Mortgage-backed and asset-backed securities not issued by a government agency generally involve greater credit risk than securities issued by government agencies. Payment of principal and interest generally depends on the cash flows generated by the underlying assets and the terms of the security. The types of mortgages (for example, residential or commercial mortgages) underlying securities held by the Fund may differ and be affected differently by market factors. Investments that receive only the interest portion or the principal portion of payments on the underlying assets may be highly volatile. The market for mortgage- and asset-backed securities has recently experienced high volatility and a lack of liquidity. As a result, the value of many of these securities has significantly declined.

Repurchase Agreement Risk These transactions must be fully collateralized at all times, but involve some risk to a Fund if the other party should default on its obligation and the Fund is delayed or prevented from recovering the collateral.

Short Sales Risk If the Fund sells a security short, it will make money if the security’s price goes down (in an amount greater than any transaction costs) and will lose money if the security’s price goes up. There is no limit on the amount of money the Fund may lose on a short sale. The Fund may not be able to close out a short sale when it might wish to do so, or may only do so at an unfavorable price. Short sales can involve leverage. If the Fund invests the proceeds from short positions in other securities the Fund could lose money both on the short positions and on the securities in which it has invested the short proceeds.

Sovereign Debt Obligations Risk Investments in debt securities issued by governments or by government

agencies and instrumentalities involve the risk that the governmental entities responsible for repayment may be unable or unwilling to pay interest and repay principal when due. Many sovereign debt obligations may be rated below investment grade (“junk” or “high yield” bonds). Any restructuring of a sovereign debt obligation held by the Fund will likely have a significant adverse effect on the value of the obligation. In the event of default of sovereign debt, the Fund may be unable to pursue legal action against the sovereign issuer or to realize on collateral securing the debt.

U.S. Government Securities Risk Obligations of certain U.S. Government agencies and instrumentalities are not backed by the full faith and credit of the U.S. Government, and there can be no assurance that the U.S. Government would provide financial support to such agencies and instrumentalities.

Valuation Risk The Fund is subject to the risk of mispricing or improper valuation of its investments, in particular to the extent that its securities are fair valued.

When-Issued, Delayed Delivery, TBA, and Forward Commitment Transaction Risk These transactions may create leverage and involve a risk of loss if the value of the securities declines prior to settlement.

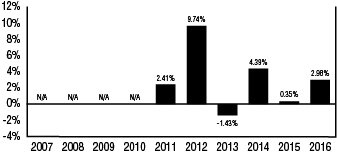

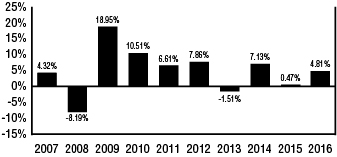

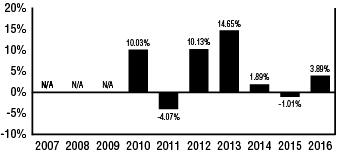

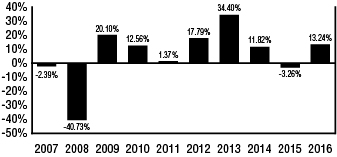

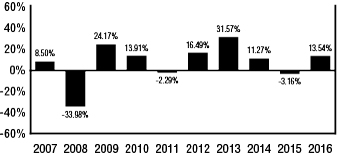

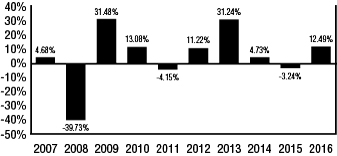

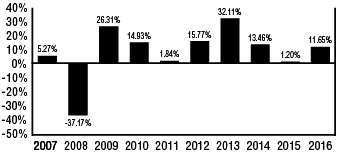

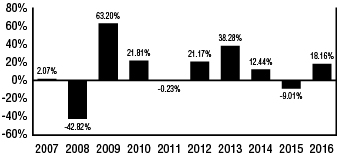

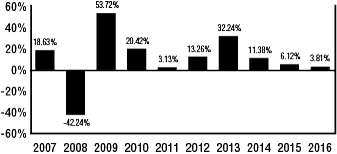

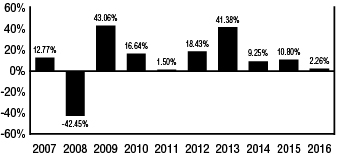

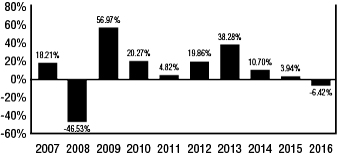

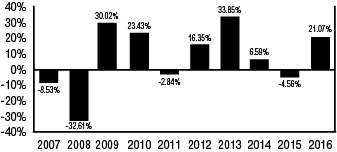

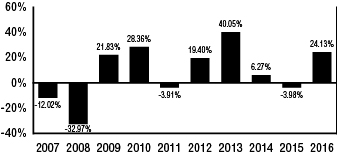

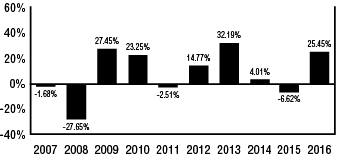

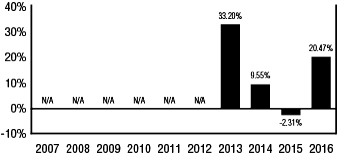

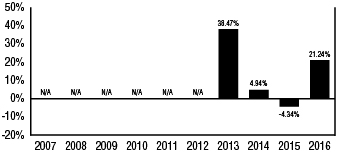

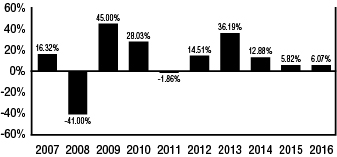

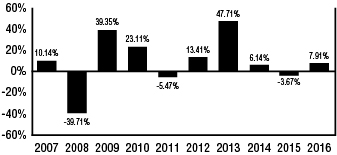

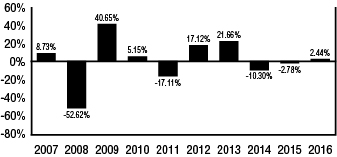

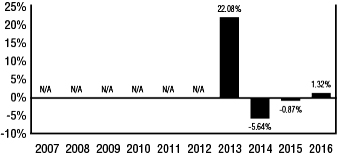

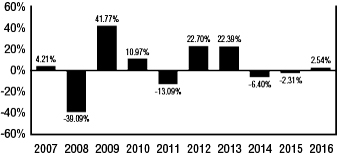

Performance Information

The following bar chart and table provide some indication of the risks of investing in the Fund. The bar chart shows changes in the Fund’s performance from year to year for Class I shares. The table shows how the Fund’s average annual returns for 1 and 5 years, and since inception, compare with those of a broad measure of market performance. The Fund’s name and investment strategy changed on October 27, 2014. The performance results shown below would not necessarily have been achieved had the Fund’s current investment strategy been in effect for the entire period for which performance results are presented. Performance for Class A shares of the Fund for periods prior to its inception date (04/01/14) is based on the performance of Class R5 shares, adjusted for Class A expenses. Performance for Class A shares of the Fund reflects any applicable sales charge. Past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. More up-to-date performance information is available at http://www.massmutual.com/funds or by calling 1-888-309-3539.

– 24 –

Annual Performance

Class I Shares

| Highest Quarter: | 3Q ’12, | 3.36% | Lowest Quarter: | 2Q ’13, | - | 3.30% |