Exhibit (c)(12)

Project Titan | Discussion materials November 06, 2020

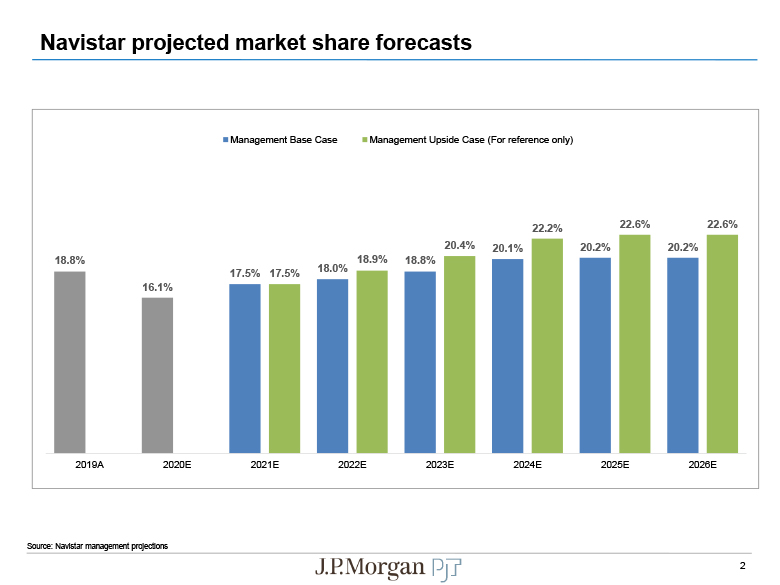

Overview of Management Forecasts Management Base Case Management Upside Case Navistar management has advised that the Management Base Case represents its higher probability financial forecast and directed that it should form the basis of the valuation analysisBoth the Management Base Case and Upside Case assume that the TRATON Alliance continues throughout the forecast periodManagement has indicated that a termination of the TRATON Alliance would reduce the Company’sforecasted earnings and cash flowsManagement has indicated that the Management Base Case represents its best current estimate and judgment as to its financial forecast for the Company for 2020E – 2026E and will form the basis of Management’s next Strategic PlanAssumes Navistar increases North American market share to 20.2% by 2026E and WholeCoEBITDA margin to 10.9% by 2026EManagement Base Case forms the basis for our discounted cash flow analysisManagement has indicated that the Management Upside Case was developed to highlightpotential upside in the business but in the materially lower probability financial scenarioAssumes Navistar increases North American market share to 22.6% by 2026E and WholeCo EBITDA margin to 12.7% by 2026EManagement Upside Case discounted cash flow analysis presented for reference purposes only Source: Navistar management projections 2

Navistar projected market share forecasts 18.8% 16.1% 18.0% 18.8% 20.1% 20.2% 20.2% 17.5% 17.5% 18.9% 20.4% 22.2% 22.6% 22.6% 2019A 2020E 2021E 2022E 2023E 2024E 2025E 2026E Management Base Case Management Upside Case (For reference only) Source: Navistar management projections 3

$370 $700 $1,064 $1,432 $1,337 $1,464 9.9% 11.6% 11.2% 11.6% 12.7% Management forecast comparison ($mm) Source: Company information and Navistar management projections. Analyst consensus per CapIQ as of 11/04/20 Management Case 2019 $11,251 $9,603 $10,498 $11,170 $12,387 $12,055 $1,119 $1,451 $1,448 10.0% 11.7% 12.0% $882 $740 $877 7.8% 7.7% 8.4% 2019 2020 2021 2022 2023 2024 Management projections pre-COVID Adjusted base case with revised estimates Management Upside Case (For reference only) $7,400 $8,729 $10,732 $12,315 $11,887 $12,600 $12,600 $1,604 Adjusted base case with revised estimates Management Base Case (16.9%) (6.3%) (5.7%) (7.1%) $7,400 $8,729 $10,465 $11,681 $11,203 $11,756 $11,756 nue eRev $7,414 $8,679 $9,536 $377 $612 $788 0.2% Δ vs..Mgmt. Upside case Δ vs..Mgmt. 0.2%Base case (0.6%) (11.1%) 2.0% (12.6%) (26.0%) (0.6%) (8.9%) 2.0% (12.6%) (22.2%) Current analyst consensus 2020 2021 2022Consensus revenue 5.1% 7.0% 8.0% 2020 2021 2022Consensus Adj. EBITDA $370 $700 $1,013 $1,295 $1,190 $1,291 $1,282 5.0% 11.1% 10.6% 11.0% 10.9% 8.0% 9.7% 5.0% 8.0% 2021 2022 2023 2024 2025 2026 2020 2021 2022 2023 2024 2025 2026 2020 Adj. EBITDA Revenue 2019 2020 2021 2022 2023 2024 2020 2021 2022 2023 2024 2025 2026 2020 2021 2022 2023 2024 2025 2026 % growth (14.6%) 9.3% 6.4% 10.9% (2.7%) (34.2%) 18.0% 19.9% 11.6% (4.1%) 4.9% 0.0% (34.2%) 18.0% 22.9% 14.8% (3.5%) 6.0% 0.0% Δ vs..Mgmt. (49.9%) (20.2%) (9.5%) (10.8%) (17.8%) Δ vs..Mgmt. (49.9%) (20.2%) (4.9%) (1.3%) (7.7%)case 2019 case 2019 Δ vs..Mgmt.. (22.9%) (16.9%) (3.9%) (0.6%) (1.4%) Δ vs..Mgmt. (22.9%) case 2019 case 2019 Note: Financials reflect forecasted as of 10/31 FYE 4

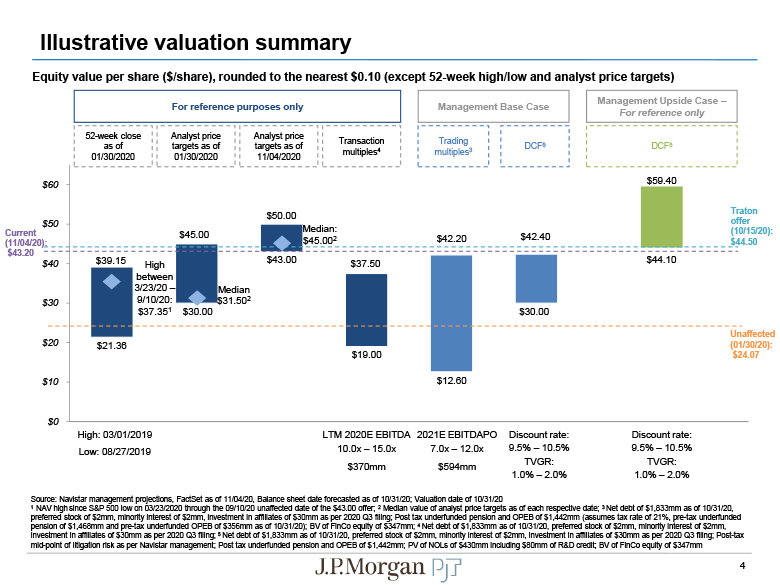

Illustrative valuation summary $21.36 $30.00 $43.00 $19.00 $12.60 $30.00 $44.10 $39.15 $45.00 $50.00 $37.50 $42.20 $42.40 $59.40 $0 $10 $20 $30 $40 $50 $60 Unaffected (01/30/20):$24.07 Discount rate: 9.5% – 10.5% TVGR:1.0% – 2.0% Source: Navistar management projections, FactSet as of 11/04/20, Balance sheet date forecasted as of 10/31/20; Valuation date of 10/31/201 NAV high since S&P 500 low on 03/23/2020 through the 09/10/20 unaffected date of the $43.00 offer; 2 Median value of analyst price targets as of each respective date; 3 Net debt of $1,833mm as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; Post tax underfunded pension and OPEB of $1,442mm (assumes tax rate of 21%, pre-tax underfunded pension of $1,468mm and pre-tax underfunded OPEB of $356mm as of 10/31/20); BV of FinCo equity of $347mm; 4 Net debt of $1,833mm as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; 5 Net debt of $1,833mm as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; Post-tax Current (11/04/20): $43.20 Equity value per share ($/share), rounded to the nearest $0.10 (except 52-week high/low and analyst price targets)Management Upside Case –For reference only 7.0x – 12.0x$594mm LTM 2020E EBITDA 2021E EBITDAPO 10.0x – 15.0x$370mm Discount rate: 9.5% – 10.5% TVGR:1.0% – 2.0% Management Base Case Trading multiples3 DCF5 DCF5 Traton offer (10/15/20):$44.50 High: 03/01/2019 Low: 08/27/2019 High between 3/23/20 –9/10/20:$37.351 Median $31.502 Median: $45.002 For reference purposes only 52-week close as of 01/30/2020 Analyst price Analyst pricetargets as of targets as of01/30/2020 11/04/2020 Transaction multiples4 mid-point of litigation risk as per Navistar management; Post tax underfunded pension and OPEB of $1,442mm; PV of NOLs of $430mm including $80mm of R&D credit; BV of FinCo equity of $347mm 5

Illustrative discounted cash flow bridge Management Base Case $3.50 $4.30 ($18.00) ($14.40) ($3.90) PV of cash flow PV of Terminal Book value of FinCo PV of NOLs incl. Net debt Tax-affected Post-tax litigation Share price value equity R&D credit pension & OPEB expenses adjustment Source: Navistar management projections; Note: Assumes valuation date as of 10/31/20; assumes mid-period discounting convention; assumes tax rate of 27%; Equity value per share ($/share), PV of NOLs of$430mm including $80mm of R&D credit; Net debt of $1,833mm as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; Post-tax mid-point of litigation risk as per Navistar management; Post tax underfunded pension and OPEB of $1,442mm; PV of NOLs of $430mm including $80mm of R&D credit; BV of FinCo equity of $347mm; rounded to the nearest Discount rate: 9.5% – 10.5%TGR: 1.0% – 2.0% $31.00 – $32.40 $27.70 – $38.60 $30.00 – $42.40 $0.10 6

Revenue CAGR 21E' - 25E' 8.7% 8.2% 7.7% 7.2% 6.7% 21E' - 25E' 8.7% 8.2% 7.7% 7.2% 6.7% 21E' - 30E' 4.8% 4.3% 3.8% 3.3% 2.8% 21E' - 30E' 4.8% 4.3% 3.8% 3.3% 2.8% Long term manufacturing EBITDA margin 11.5% $40 $38 $35 $33 $30 11.0% $38 $35 $33 $30 $28 10.5% $35 $32 $30 $28 $25 10.0% $32 $30 $27 $25 $23 9.5% $29 $27 $25 $23 $21 Illustrative standalone discounted cash flow sensitivity analysis Revenue CAGR Long term manufacturing EBITDA margin 11.5% $47 $44 $41 $39 $36 11.0% $44 $41 $38 $36 $33 10.5% $41 $38 $35 $33 $30 10.0% $38 $35 $33 $30 $28 9.5% $35 $32 $30 $27 $25 High Long term manufacturing EBITDA margin Low Mid-point Discount rate: 10.50%; TVGR: 1.0% Discount rate: 10.00%; TVGR: 1.5% Discount rate: 9.50%; TVGR: 2.0% Management Base Case Source: Navistar management projections 6

September 11, 2020:MAN announces an “extensive restructuring” plan stating up to 25% of employees jobs could be cut 5yr 3yr 1yr YTD Since Since Returns 01/30 09/09 NAV S&P 500 229%64% 3%33% 27%12% 49%7% 79%5% 21%1% Navistar broker targets and historical performance 7 January 30, 2020: Navistar receives $35 bid from TRATON after market close01/30/2020 unaffected share price of $24.07 September 10,2020:Navistar receives revised $43 bid from TRATON Current broker target prices as of 11/04/2020(2) Navistar share price performance – 5 years(rebased to NAV share price) Broker Date Rec. Targetprice ($) Prem. / (Disc.)to current(1) Jefferies 10/22/20 Hold $44.50 3.0% Melius Research 10/16/20 Hold 46.00 6.5% RBC Capital Markets 10/16/20 Hold 44.50 3.0% Raymond James 10/15/20 Hold – – Loop Capital Markets 10/13/20 Hold 46.00 6.5% Vertical Research 10/09/20 Hold 45.00 4.2% Wolfe research 10/09/20 Buy 50.00 15.7% BMO Capital Markets 9/14/20 Hold 43.00 (0.5%) Median $45.00 4.2% Average NAV price $28.97 $33.81 $30.84 $30.66 $31.06 $42.69March 11, 2020:WHO declares COVID-19 a global pandemic Broker Date Rec. Target price ($) Prem. / (Disc.) to unaffected(4) BMO Capital Markets 12/20/19 Hold $30.00 24.6% Baird 12/18/19 Buy 34.00 41.3% Vertical Research 12/18/19 Hold 30.00 24.6% Raymond James 12/17/19 Hold – – Loop Capital Markets 12/17/19 Buy 38.00 57.9% Jefferies 12/17/19 Buy 45.00 87.0% RBC Capital Markets 12/17/19 Hold 32.00 32.9% Melius Research 12/17/19 Hold 31.00 28.8% Wells Fargo 12/17/19 Hold 30.00 24.6% Median $31.50 30.9% Unaffected broker target prices as of 01/30/2020(2),(3) Navistar & TRATON reaction to proposals – since 01/01/2020 (Indexed to 100)NAV 1st offer 2nd offer TRATON 49% (28%) July 11, 2020:CEO Andres Renschler to step down immediately, will be succeeded by Matthias Grundler Navistar broker target price progression Source: Press releases; Factset as of 11/04/2020(1) Based on 11/04/2020 closing price of $43.20; (2) Excludes J.P. Morgan research; $45.00 (3) Pre-proposal 1/30/2020; (4) Based on 01/30/2020 closing price of $24.07

Commercial vehicle trading multiples 9.7x 9.3x 7.3x 7.1x 5.6x 3.4x 11.8x(2)11.0x(3)10.4x Median 2021E Adj. TEV / EBITDAPO(Excl. NAV)7.3x Source: Company filings, Wall Street Research, Capital IQNote: Market data as of 11/4/20. Navistar multiples represent unaffected share price as of 9/9/20 and balance sheet as of 7/31/20. Median trading multiple excludes Navistar multiplesAdjusted TEV defined as market cap plus net debt, preferred stock, minority interest and tax-affected pension & OPEB less investments in affiliates and book value of FinCo EquityBased on consensus 2021E Manufacturing EBITDA of $554mmAssumes 2021E Manufacturing EBITDAPO of $594mm based on 2021E WholeCo Adj. EBITDA of $700mm, 2021E FinCo EBITDA of $126mm, and 2021E non-service pension cost of $20mm per Navistar management projections 2021E ADJ. TEV / EBITDAPO(1) (Consensus) Unaffected NAV TEV as of 9/9/20 (Management Base Case) 9

Commercial vehicle transaction multiples – For reference only 9.7x 8.4x 6.1x4.5x 9.7x TEV / LTM EBITDA15.6x12.8x11.6x Year 2000 – 2014 2019 2006 2016 2006 – 2012 2016 2000 Target Scania WABCO Scania Navistar MAN Blue Bird Renault V.I. Acquirer Volkswagen ZF MAN Volkswagen Volkswagen American Securities Volvo Transaction Size ($bn)Announced Synergies ($mm)(5) Weighted Avg.(1) $7.4 $16.6(2) $5.9(3) Weighted Avg.(1) $0.4(4) $1.6 $1,170 NA $630 $200 NA NA $360 Source: Company filings, Capital IQRepresents weighted average multiple based on size of acquired stake for all of Volkswagen’s stake purchases in Scania and MANTransaction ultimately evolved into Volkswagen takeovers of Scania and MAN separatelyImplied based on 16.6% ownership stakeImplied based on 57% ownership stakeReflects annual run-rate synergies. Synergy amount converted to USD based on conversion rate on announcement date Median TEV / LTM EBITDA 10

Navistar implied acquisition multiples Including NOLs and potential litigation liabilities ($ in millions, except per share) Navistar Offer Price $44.50 Premium to unaffected price of $24.07 as of 1/30/20 84.9% Premium to unaffected 52-week high of $39.15 as of 1/30/20 13.7% FDSO (mm) 100.2 Implied Equity Value $4,459 Plus: Industrial Net Debt and Other⁽¹⁾ 1,768 Implied Enterprise Value $6,227 Plus: Tax Affected Unfunded Pension & OPEB⁽²⁾ 1,442 Implied Adj. Enterprise Value $7,668 Less: Book Value of FinCo Equity⁽³⁾ (347) Implied Adj. Manufacturing Enterprise Value $7,321 Valuation Multiples TEV / EBITDA Metric 2020E $370 16.8x 2021E $700 8.9x Adj. TEV / EBITDAPO 2020E $433 17.7x 2021E $720 10.6x Adj. Manufacturing TEV / Manufacturing EBITDAPO 2020E $308 23.8x 2021E $594 12.3x Source: Company Filings, Navistar Management Projections, BloombergNet debt of $1,833mm forecasted as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; $391mm post-tax mid-point of litigation risk as perNavistar management; PV of NOLs of $430mm including $80mm of R&D creditPost tax underfunded pension and OPEB of $1,442mm (assumes tax rate of 21%, pre-tax underfunded pension of $1,468mm and pre-tax underfunded OPEB of $356mm forecasted as of 10/31/20 (3) Assumes 1.0x FinCo. book value of $347mm which reflect reduction in Fin Co. value to account for intercompany loan to Manufacturing Co. as per Navistar management 11

APPENDIX

Illustrative standalone discounted cash flow analysis Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% $3,743 $3,978 $4,244 10.0% 3,350 3,551 3,777 10.5% 2,999 3,172 3,365 Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% $37.40 $39.73 $42.37 10.0% $33.49 $35.49 $37.73 10.5% $29.99 $31.71 $33.64 PV of terminal value PV of cash flows + Firm value Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% 6.7x 7.1x 7.6x 10.0% 6.3x 6.7x 7.2x 10.5% 6.0x 6.4x 6.8x Equity value Implied value per share Book value of FinCo1 + Implied TV / 2030E Adj. EBITDA = Discount rate 9.5% ($3,209) 10.0% (3,209) 10.5% (3,209) Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% $3,366 $3,601 $3,867 10.0% 3,045 3,245 3,471 10.5% 2,763 2,936 3,129 Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% $6,953 $7,187 $7,453 10.0% 6,559 6,760 6,986 10.5% 6,208 6,381 6,575 Discount rate 9.5% $3,239 10.0% 3,168 10.5% 3,098 Management projections Management extrapolations CAGR E l ) ) )) Discount rate 9.5% $347 10.0% 347 10.5% 347 Net debt and NOLs2 = - Management Base Case – 10.5% Manufacturing long term margin; Assumed discount rate of 9.5% - 10.5% ($mm) Oct-21E Oct-22E Oct-23E Oct-24E Oct-25E Oct-26 Oct-27E Oct-28E Oct-29E Oct-30E Termina 21E' - 25E' 21E' - 30E' Manufacturing revenue $8,504 $10,185 $11,386 $10,903 $11,454 $11,454 $11,497 $11,584 $11,714 $11,890 $12,068 7.7% 3.8% % growth 17.6% 19.8% 11.8% (4.2%) 5.1% 0% 0.4% 0.8% 1.1% 1.5% 1.5% Manufacturing Adj. EBITDA $574 $837 $1,111 $1,008 $1,108 $1,100 $1,212 $1,221 $1,235 $1,253 $1,272 17.9% 9.1% % margin 6.7% 8.2% 9.8% 9.2% 9.7% 9.6% 10.5% 10.5% 10.5% 10.5% 10.5% Plus: Non-service pension expenses 20 16 12 8 6 0 (4) 0 0 0 0 Manufacturing EBITDAPO $594 $853 $1,123 $1,017 $1,114 $1,100 $1,208 $1,221 $1,235 $1,253 $1,272 % margin 7.0% 8.4% 9.9% 9.3% 9.7% 9.6% 10.5% 10.5% 10.5% 10.5% 10.5% Less: Manufacturing D&A (132) (171) (185) (194) (185) (185 (193) (201) (209) (217) (217 ) Manufacturing EBITPO $463 $682 $938 $823 $929 $915 $1,015 $1,020 $1,026 $1,037 $1,055 % margin 5.4% 6.7% 8.2% 7.5% 8.1% 8.0% 8.8% 8.8% 8.8% 8.7% 8.7% Tax expense (36) (184) (253) (222) (251) (247 (274) (275) (277) (280) (285 ) EBIAT $427 $498 $685 $601 $678 $668 $741 $745 $749 $757 $770 Add: Manufacturing D&A 132 171 185 194 185 185 193 201 209 217 217 % capex 43.8% 57.1% 61.6% 64.6% 61.7% 61.7% 64.3% 67.0% 69.6% 72.3% 72.3% Less: Capex (300) (300) (300) (300) (300) (300 (300) (300) (300) (300) (300 ) 0.0% 0.0% Less: Δ(NWC) & Other (53) 22 97 (96) (54) (83 (5) (5) (5) (5) (5 ) Unlevered FCF $205 $391 $666 $399 $509 $470 $629 $641 $653 $668 $682 Source: Navistar management projections; Note: Assume valuation date as of 10/31/20; assumes mid-period discounting convention; assumes tax rate of 27%1 Assumes 1.0x FinCo. book value of $347mm which reflect reduction in Fin Co. value to account for intercompany loan to Manufacturing Co. as per Navistar management2 Net debt of $1,833mm forecasted as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; $387mm post-tax mid-point of litigation risk as per Navistar management; Post tax underfunded pension and OPEB of $1,442mm (assumes tax rate of 21%, pre-tax underfunded pension of $1,468mm and pre-tax underfunded OPEB of $356mm forecasted as of 10/31/20); PV of NOLs of $430mm including $80mm of R&D credit 13

Illustrative standalone discounted cash flow analysis Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% $5,343 $5,633 $5,962 10.0% 4,853 5,101 5,380 10.5% 4,415 4,629 4,868 PV of terminal value Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% $53.26 $56.13 $59.38 10.0% $48.40 $50.86 $53.62 10.5% $44.06 $46.18 $48.55 PV of cash flows + Firm value Equity value Terminal growth rate 1.0% 1.5% 2.0% Discount rate 9.5% $4,181 $4,471 $4,799 10.0% 3,781 4,029 4,308 10.5% 3,431 3,645 3,884 Terminal growth rate 1.0% 1.5% 2.0% 9.5% $8,553 $8,842 $9,171 10.0% 8,062 8,310 8,589 10.5% 7,624 7,838 8,077 Discountrate Discount rate 9.5% 7.0x 7.5x 8.1x 10.0% 6.6x 7.1x 7.6x 10.5% 6.3x 6.7x 7.1x Implied value per share Discount rate 9.5% ($3,209) 10.0% (3,209) 10.5% (3,209) Book value of FinCo1 Discount rate 9.5% $4,025 10.0% 3,934 10.5% 3,846 Implied TV / 2030E Adj. EBITDA Terminal growth rate 1.0% 1.5% 2.0% + = ($mm) Oct-21E Oct-22E Oct-23E Oct-24E Oct-25E Oct-26E Oct-27E Oct-28E Oct-29E Oct-30E Terminal 21E' - 25E' 21E' - 30E' Manufacturing revenue $8,504 $10,451 $12,020 $11,588 $12,298 $12,298 $12,344 $12,437 $12,577 $12,765 $12,957 9.7% 4.6% % growth 17.6% 22.9% 15.0% (3.6%) 6.1% 0% 0.4% 0.8% 1.1% 1.5% 1.5% Manufacturing Adj. EBITDA $574 $889 $1,249 $1,156 $1,282 $1,422 $1,427 $1,438 $1,454 $1,476 $1,498 22.3% 11.1% % margin 6.7% 8.5% 10.4% 10.0% 10.4% 11.6% 11.6% 11.6% 11.6% 11.6% 11.6% Plus: Non-service pension expenses 20 16 12 8 6 0 (4) 0 0 0 0 Manufacturing EBITDAPO $594 $905 $1,260 $1,164 $1,287 $1,422 $1,423 $1,438 $1,454 $1,476 $1,498 % margin 7.0% 8.7% 10.5% 10.0% 10.5% 11.6% 11.5% 11.6% 11.6% 11.6% 11.6% Less: Manufacturing D&A (132) (171) (185) (194) (185) (185) (193) (201) (209) (217) (217) Manufacturing EBITPO $463 $734 $1,075 $970 $1,102 $1,237 $1,230 $1,237 $1,245 $1,259 $1,281 % margin 5.4% 7.0% 8.9% 8.4% 9.0% 10.1% 10.0% 9.9% 9.9% 9.9% 9.9% Tax expense (36) (198) (290) (262) (298) (334) (332) (334) (336) (340) (346) EBIAT $427 $536 $785 $708 $805 $903 $898 $903 $909 $919 $935 Add: Manufacturing D&A 132 171 185 194 185 185 193 201 209 217 217 % capex 43.8% 57.1% 61.6% 64.6% 61.7% 61.7% 64.3% 67.0% 69.6% 72.3% 72.3% Less: Capex (300) (300) (300) (300) (300) (300) (300) (300) (300) (300) (300) 0.0% 0.0% Less: Δ(NWC) & Other (53) 49 128 (94) (42) (83) (5) (5) (5) (5) (5) Unlevered FCF $205 $456 $798 $508 $648 $705 $786 $799 $813 $831 $847 Discount rate 9.5% $347 10.0% 347 10.5% 347 Net debt and NOLs2 = - Management Upside Case – 11.4% Manufacturing long term margin; Assumed discount rate of 9.5% - 10.5%(For reference only) Management projections Management extrapolations CAGR Source: Navistar management projections; Note: Assume valuation date as of 10/31/20; assumes mid-period discounting convention; assumes tax rate of 27%1 Assumes 1.0x FinCo. book value of $347mm which reflect reduction in Fin Co. value to account for intercompany loan to Manufacturing Co. as per Navistar management2 Net debt of $1,833mm forecasted as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; $387mm post-tax mid-point of litigation risk as per Navistar management; Post tax underfunded pension and OPEB of $1,442mm (assumes tax rate of 21%, pre-tax underfunded pension of $1,468mm and pre-tax underfunded OPEB of $356mm forecasted as of 10/31/20); PV of NOLs of $430mm including $80mm of R&D credit 14

Illustrative discounted cash flow bridge $3.50 $4.30 ($18.00) ($14.40) ($3.90) PV of cash flow PV of Terminal Book value of FinCo PV of NOLs incl. Net debt Tax-affected Post-tax litigation Share price value equity R&D credit pension & OPEB expenses adjustment Management Upside Case (For reference only) Source: Navistar management projections; Note: Assumes valuation date as of 10/31/20; assumes mid-period discounting convention; assumes tax rate of 27%; Equity value per share ($/share), PV of NOLs of$430mm including $80mm of R&D credit; Net debt of $1,833mm as of 10/31/20, preferred stock of $2mm, minority interest of $2mm, investment in affiliates of $30mm as per 2020 Q3 filing; Post-tax mid-point of litigation risk as per Navistar management; Post tax underfunded pension and OPEB of $1,442mm; PV of NOLs of $430mm including $80mm of R&D credit; BV of FinCo equity of $347mm; rounded to the nearest Discount rate: 9.5% – 10.5%TGR: 1.0% – 2.0% $38.40 – $40.10 $34.30 – $47.80 $44.10 – $59.40 $0.10 15

Revenue CAGR 21E' - 25E' 10.2% 9.7% 9.2% 8.7% 8.2% 21E' - 30E' 5.1% 4.6% 4.1% 3.6% 3.1% Long term manufacturing EBITDA margin 12.1% $50 $47 $44 $41 $39 11.6% $47 $44 $41 $39 $36 11.1% $44 $41 $39 $36 $34 10.6% $41 $39 $36 $34 $31 10.1% $38 $36 $33 $31 $29 Illustrative standalone discounted cash flow sensitivity analysis Revenue CAGR 21E' - 25E' 10.2% 9.7% 9.2% 8.7% 8.2% 21E' - 30E' 5.1% 4.6% 4.1% 3.6% 3.1% Long term manufacturing EBITDA margin 12.1% $57 $54 $51 $48 $45 11.6% $54 $51 $48 $45 $42 11.1% $51 $48 $45 $42 $39 10.6% $48 $45 $42 $39 $37 10.1% $44 $42 $39 $36 $34 Long term manufacturing EBITDA margin High Low Mid-point Discount rate: 10.50%; TVGR: 1.0% Discount rate: 10.00%; TVGR: 1.5% Discount rate: 9.50%; TVGR: 2.0% Management Upside Case (For reference only) Source: Navistar management projections 14

These materials were prepared by PJT Partners LP (“PJT Partners”, “we” or “us”) solely for the information and assistance of Navistar International Corporation (the “Company”). These materials contain highly confidential information and are solely for informational purposes.These materials and any oral information provided in connection with these materials (collectively, the “Information”), as well as any information derived from the Information, may not be communicated, reproduced, disclosed (in whole or in part) to, or relied upon by, any other person, referred to, or used for any purpose, other than as specifically contemplated by a written agreement with PJT Partners or with our prior written consent. If you are not the intended recipient of these materials, please delete and destroy all copies immediately.The information in these materials is based on information provided by or on behalf of the Company and/or other potential transaction participants or otherwise obtained from public sources. We assume no responsibility forindependent verification of any such information, and we have assumed and relied upon the accuracy and completeness of such information for purposes of these materials. Neither we nor any of our affiliates or agents, make any representation or warranty, express or implied, in relation to the accuracy, fairness, reasonableness or completeness of the Information, or any data it generates and expressly disclaim any and all liability in relation to any of such information or any errors or omissions therein to the fullest extent permitted by law. These materials are based on financial, economic, market and other conditions prevailing as of the date of these materials and are subject to change. We undertake no obligation or responsibility to update any of the information contained in these materials.Our analyses do not purport to be an appraisal of any assets or liabilities of the Company or any other party, nor have we evaluated the solvency of the Company or any other party under any laws relating to bankruptcy, insolvency or similar matters. These materials are qualified in their entirety by the terms, conditions, limitations, qualifications and disclosures set forth in the engagement letter entered into by the Company with us and in any opinion letter delivered by us in connection with these materials. These materials are incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by PJT Partners.These materials do not (i) constitute a recommendation to the Board, the Company or any other party in connection with any transaction; (ii) constitute advice or a recommendation to the Board, the Company, any holder ofsecurities of the Company or any other party in connection with any transaction; (iii) address the Company’s or any other party’s underlying business and/or financial decision to pursue any transaction, the relative merits of any such transaction as compared to any alternative business or financial strategies that might exist for the Company or any other party, or the effects of any other transaction in which the Company or any other party might engage; or (iv) express any view as to the potential effects of the unusual volatility currently being experienced in the credit, financial and stock markets on the Company or any proposed transaction related to the COVID-19 pandemic or otherwise. You should not rely upon or use these materials to form the definitive basis for any decision or action whatsoever, with respect to any proposed transaction or otherwise. The Board and the Company must make its own independent assessment and such investigation as it deems necessary to determine its interest in participating in any transaction. Any valuation, appraisal or conclusion of a financial nature contained in these materials results from the application by PJT Partners of techniques and principles generally adopted in the context of the preparation of financial presentations of this nature, and PJT Partners cannot and does not warrant that the use of different techniques and principles would not lead to a different result.PJT Partners engages in a wide range of financial services activities. In the ordinary course of these activities, PJT Partners may provide financial advisory, capital raising and other financial services to, without limitation, theCompany, any transaction counterparty, any other transaction participant, any other party who may be financially interested with respect to the Company or any transaction or any of the foregoing entities’ or parties’ respective affiliates, subsidiaries, investors, portfolio companies and representatives, for which services PJT Partners may have received, and may in the future receive, compensation.At any given time, PJT Partners may be engaged by one or more parties that may compete with, or otherwise be adverse to, the Company, any counterparty to a transaction to which these materials relate and/or the Company’s or such other party’s shareholders or other stakeholders in connection with matters unrelated to any such transaction or our engagement by the Company. It is possible that PJT Partners may from time to time be involved in one or more capacities that, directly or indirectly, are or may be perceived as being adverse to the interests of the Company, such counterparties and/or their respective shareholders or other stakeholders in the context of a potential transaction or otherwise. Moreover, PJT Partners may, in the course of other client relationships, have or in the future come into possession of information material to the interests of the Company and/or its shareholders or other stakeholders in the context of a potential or actual transaction or otherwise which, by virtue of such other client relationships, PJT Partners is not or will not be at liberty to disclose to the Company or its shareholders or other stakeholders.Furthermore, PJT Partners and its affiliates and its and their directors, officers, employees, consultants and agents may have investments in the Company, any transaction counterparty, any other transaction participant, any other financially interested party with respect to any transaction or any of the foregoing entities’ or parties’ respective affiliates, subsidiaries, investment funds, portfolio companies and representatives.In preparing these materials PJT Partners has acted as an independent contractor and nothing in these materials is intended to create or shall be construed as creating a fiduciary relationship between the recipient and PJT Partners. We are not legal, regulatory, accounting or tax advisors and these materials do not constitute legal, regulatory, accounting, tax or other specialist advice. These materials do not constitute and should not be considered any form of financial opinion or recommendation by us or any of our affiliates. This document is not a research report and should not be considered as such.These materials do not constitute an offer to sell or the solicitation of an offer to buy any security, nor does it constitute an offer or commitment to lend, syndicate or arrange a financing, underwrite or purchase any securities oract as an agent or advisor or in any other capacity with respect to any transaction, or commit capital to, or participate in, any trading strategies.This document may include information from the S&P Capital IQ Platform Service. Such information is subject to the following: “Copyright © 2020, S&P Capital IQ (and its affiliates, as applicable). This may contain informationobtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS ORLOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.This document may include information from SNL Financial LC. Such information is subject to the following: “CONTAINS COPYRIGHTED AND TRADE SECRET MATERIAL DISTRIBUTED UNDER LICENSE FROM SNL.FOR RECIPIENT’S INTERNAL USE ONLY.”By accepting these materials, the recipient agrees to be bound by the foregoing limitations.PJT Partners LP is a U.S. broker-dealer registered with FINRA and is a member of SIPC. PJT Partners is represented in the United Kingdom by PJT Partners (UK) Limited. PJT Partners (UK) Ltd is authorized and regulated by the UK Financial Conduct Authority. Its registered office is at One Curzon Street, London, W1J 5HD. PJT Partners (UK) Limited is registered in England and Wales as a Limited Company (Company number 942 4559). PJT Partners is represented in Hong Kong by PJT Partners (HK) limited, authorized and regulated by the Securities and Futures Commission.Copyright © 2020, PJT Partners LP (and its affiliates, as applicable).

This presentation was prepared exclusively for the benefit and internal use of the J.P. Morgan client to whom it is directly addressed and delivered (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating, on a preliminary basis, the feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by J.P. Morgan. Neither this presentation nor any of its contents may be disclosed or used for any other purpose without the prior written consent of J.P. Morgan.The information in this presentation is based upon any management forecasts supplied to us and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. J.P. Morgan’s opinions and estimates constitute J.P. Morgan’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. In addition, our analyses are not and do not purport to be appraisals of the assets, stock, or business of the Company or any other entity. J.P. Morgan makes no representations as to the actual value which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Unless expressly contemplated hereby, the information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which may have significant valuation and other effects.Notwithstanding anything herein to the contrary, the Company and each of its employees, representatives or other agents may disclose to any and all persons, without limitation of any kind, the U.S. federal and state income tax treatment and the U.S. federal and state income tax structure of the transactions contemplated hereby and all materials of any kind (including opinions or other tax analyses) that are provided to the Company relating to such tax treatment and tax structure insofar as such treatment and/or structure relates to a U.S. federal or state income tax strategy provided to the Company by J.P. Morgan.J.P. Morgan’s policies prohibit employees from offering, directly or indirectly, a favorable research rating or specific price target, or offering to change a rating or price target, to a subject company as consideration or inducement for the receipt of business or for compensation. J.P. Morgan also prohibits its research analysts from being compensated for involvement in investment banking transactions except to the extent that such participation is intended to benefit investors.Changes to Interbank Offered Rates (IBORs) and other benchmark rates: Certain interest rate benchmarks are, or may in the future become, subject to ongoing international, national and other regulatory guidance, reform and proposals for reform. For more information, please consult: https://www.jpmorgan.com/global/disclosures/interbank_offered_ratesIRS Circular 230 Disclosure: JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone not affiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.J.P. Morgan is the marketing name for the Corporate and Investment Banking activities of JPMorgan Chase Bank, N.A., JPMS (member, NYSE), J.P. Morgan PLC authorized by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority) and their investment banking affiliates.